|

1.

CENTRAL/ WEST AFRICA

Exporters show slight optimism about current quarter

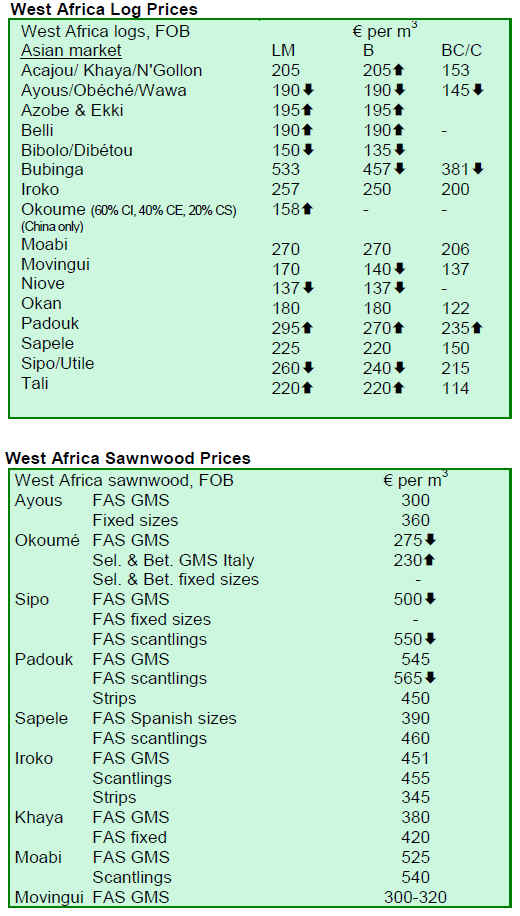

There were a few minor price changes through the end of

May. Log business with Asian countries had held very

firm through the month with possibly more activity than

producers and exporters had expected and some reports of

difficulty in filling buyers¡¯ orders for volume of species

such as padouk and belli. As a consequence, prices have

moved higher. Okoume also was in good demand.

Although some exporters had expected a weaker price

trend, demand was good enough to see a very slight price

gain for okoume logs at the month¡¯s end.

By contrast, most lumber prices were again unchanged

except for one or two species experiencing declines

because of low or no demand. As previously reported,

Europe was still very quiet, with very little demand as

importers continued to de-stock. This occurred even

though traders were becoming aware that replacement

costs were likely to be higher than consumer prices, which

they are having to accept in selling existing stock in

domestic markets.

Asian demand for sawn lumber appears to be less buoyant

than in recent months. While reported prices have changed

very little and appear stable, this was because of poor

demand rather than any substantial business by volume.

While importing countries can still find countries that

permit log exports, there will be always a tendency for the

importing countries to support local sawmilling industries.

During times of more difficult trading conditions, as in the

current crisis, there is an equal tendency for producer

countries to allow logs to be exported and temporarily

postpone plans for curtailments that might affect revenues.

Overall, the West African market appeared to be balanced

and stable. Exporters were if anything slightly more

optimistic for continued stability through the current

quarter.

ITTO and RRI conference in Yaound¨¦ draws attention to critical problem of forest tenure

Mr. Emmanuel Ze Meka, ITTO Executive Director,

indicated at a conference on forest tenure in Yaound¨¦ that

the ¡®slowness of reform¡¯ efforts on land tenure are a key

obstacle to reducing poverty and improving livelihoods.

According to a press release from the ITTO, a draft report

launched at the event, which was hosted by Cameroon and

organized by the ITTO and Rights and Resources

International (RRI), discussed the significant problem of

deforestation and slow tenure reform efforts in Africa. The

report also explained how progress on land tenure could

help slow deforestation and climate change and reduce

poverty.

The report showcased at the meeting indicated that

African nations had less control over land rights than did

other tropical nations. Although it noted that countries

such as Angola, Cameroon, and the Democratic Republic

of Congo had land tenure arrangements for community

land, the process needed to be scaled up. It suggested that

tenure arrangements could also assist countries in

benefiting from environmental services activities such as

carbon payments. The report will be finalized based on

input from conference participants.

2. GHANA

Ghana¡¯s first quarter trade slows to major markets

Ghana¡¯s first quarter wood products exports for 2009 were

worth about EUR30 million from a cumulative volume of

93,424 m³. By comparison, figures from the same period

in 2008 showed a contraction of 34.7% and 31.4% by

volume and value, respectively, due to low demand for

these products by the major markets of Germany, Italy,

Spain, the UK and the US.

During the first quarter of 2009, tertiary product exports

registered EUR1.90 million compared with EUR3.28

million over January to March 2008. Secondary products

generated a total of EUR21.95 million from January to

March 2009 against EUR37.60 million over January to

March 2008. Europe imported EUR12.17 million

(40.46%) by value and 29,815 m³ (31.91%) by volume.

However, a 44.7% rise by volume and a corresponding

3.6% increase by value was recorded for air dried (AD)

lumber, while all other wood products registered

reductions in both volume and value for the first quarter of

2009 against 2008. No exports were recorded for furniture

parts and profile boards within the period.

A larger percentage of Ghana¡¯s exports went to African

countries, particularly those within ECOWAS (mainly

Senegal, Nigeria, Niger, Gambia, Mali, Benin, Burkina

Faso and Togo), even though Ghana¡¯s overall exports to

the African region fell in 2009 compared to 2008. Ghana¡¯s

wood products exports increased by volume to 39.95% in

2009 from the previous 32.45% recorded in 2008 for the

same period. Plywood and air-dried lumber of ceiba and

chenchen were of particular interest to Nigeria and Niger.

Ghana also earned 38.20% of its export revenue from

African markets in the first quarter of 2009 compared to

28.69% in 2008.

The emerging markets in Asia and the Far East: India,

Malaysia, Taiwan, China, Singapore and Thailand together

contributed EUR3 million (10%) to the total wood export

value from January to March 2009. India continues to be

the leading importer of teak poles, billet and teak lumber

(AD).

The US accounted for 6.6% and 2.2% of Ghana¡¯s total

exports of wood products by value and volume,

respectively, from January to March 2009 compared to

12.3% and 9.0% in January to March 2008. The US

market has maintained its position as the most lucrative

destination for Ghana¡¯s lumber (KD) and rotary veneer

exports.

By value, the ECOWAS countries absorbed EUR10.28

million (89.45%) of Africa¡¯s EUR11.50 million wood

imports from Ghana from January to March 2009. Similar

to exports by value, plywood and air dried lumber

(chenchen and ceiba) continued to interest the Nigeria and

Niger markets.

The Middle Eastern countries, notably Saudi Arabia,

Lebanon, United Arab Emirates and Israel together

contributed EUR1.21 million (4.02%) to the total export

value from January to March 2009.

3.

MALAYSIA

MFPC Chair calls for new marketing strategies

As reported in the Business Times, Chairman of the

Malaysian Furniture Promotional Council (MFPC) Mr.

Merlyn Kasimir encouraged Malaysian furniture

manufacturers to enhance new marketing strategies to

reposition themselves globally while achieving higher

productivity and maintaining lower production costs.

In 2008, exports of Malaysian furniture grew by 2% and

were worth RM8.72 billion, while imports of furniture

grew 9.8% and valued at RM1.5 billion. However, trade in

Malaysian furniture exports declined by 14.2% in January

2009 and 13.8% in February 2009. On an annual basis,

Malaysian furniture exports were worth about 2.5% of the

world furniture trade.

Malaysian construction sector suffers continuing slump

Demand for construction materials in Malaysia continued

to decline, pushing down prices for construction materials.

Steel, a competitor with timber products, was expected to

further drop 25% in price in 2009. The trends, reported by

the Malaysian Iron & Steel Industry Federation in The

Star, showed declines in production of 10.7% to 7.8

million tons in 2008. Domestic prices of steel bars had

tumbled from RM3,800 per ton in July 2008 to RM2,000

in recent weeks.

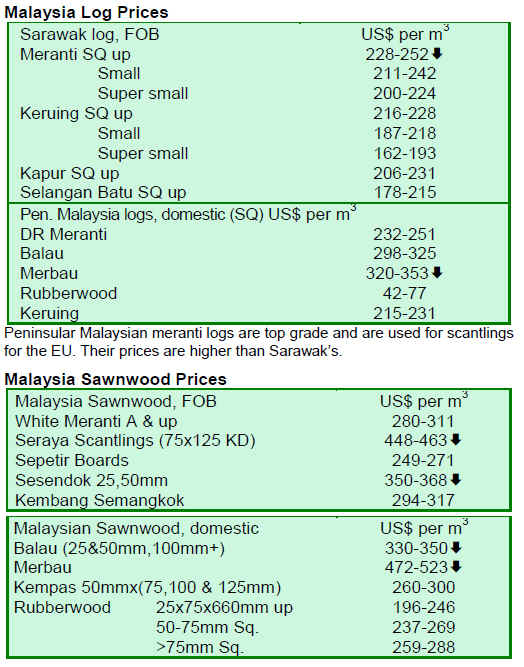

Sarawak scales back timber quota rate

According to Bernama News, Sarawak scaled back the

enforcement of its rules on the timber quota rate for the

first six months of 2009 to help timber exporters weather

the global recession. The standard royalty rate for timber

has already been reduced from RM65 to RM50 per meter

from January to December 2009. The payment period for

timber royalties has also been extended from two weeks to

three months.

Exports of timber products from Sarawak declined about

30% to RM1.3 billion in the first quarter of 2009,

compared to RM1.9 billion in the first quarter of 2008.

The volume of timber products also dropped 34% during

the same period. Royalties from timber products plunged

by about 39% to RM82.6 million in the first quarter of

2009, compared to RM134.9 million in the first quarter of

2008.

In 2008, the Sarawak timber industry registered a 2.6%

rise in export revenues worth RM7.9 billion compared to

RM7.7 billion in 2007.

4.

INDONESIA

Indonesian panel manufacturers hit by slump in demand

According to Bloomberg News, the Japanese economy

declined sharply in January to March 2009, with GDP

falling an annualized 15.2%. Meanwhile, Channel News

Asia reported US housing starts and building permits

dropped by 3.3% from March to April 2009 to an annual

rate of 494,000 units. The statistics, announced by the US

Commerce Department, showed the lowest results since

the data began to be collected in 1959. The weak demand

for products in both the US and Japan continue to hit

Indonesian plywood and panel-products manufacturers

hard.

However, as local spending expands rapidly and with GDP

standing at 4.4% for the first quarter of 2009, Indonesian

timber product manufacturers were beginning to look to

the local market to help mitigate the recession, as

consumer confidence reached a four-year high in April

2009. Bloomberg News reported that consumer spending

increased sharply by 5.8% in the first quarter of 2009,

from 4.8% in fourth quarter of 2008.

APHI warns too many levies hurt Indonesian competitiveness

The Association of Indonesian Forest Concessionaires

(APHI) has indicated total levies on forest-based

industries, including those imposed by local governments,

account for more than 30% of the production cost of local

forestry companies. APHI officials said the levies are not

only a burden to forestry companies but also render

Indonesian timber products less competitive in comparison

to Malaysia and China¡¯s timber products. According to

The Jakarta Post, total levies imposed on timber products

in neighboring countries in Southeast Asia stand at 15% or

less.

In addition, the levies could amount to as much as USD30

per m³ for every USD100 per m³ of timber product sold.

There are a total of 28 types of levies imposed on

Indonesian timber products, ranging from property taxes

to forestry commissions. Moreover, the federal

government mandates that timber product manufacturers

must source their raw materials from production forests

instead of natural forests. As a result, manufacturers have

lost access to an important raw material supply. Current

output from production forests are on a decline.

Statistics compiled by the Central Statistics Agency

(BPS), indicated that Indonesia¡¯s exports of plywood have

declined from a high of USD3.4 billion in 1997 to USD1.5

billion in 2008. Both sawnwood and other timber product

exports have also dropped by value from 1997 to 2008. A

forecast by the Association of Indonesian Wood Panel

Producers (Apkindo) indicated that the plywood industry

could contract by another 40% in 2009.

5.

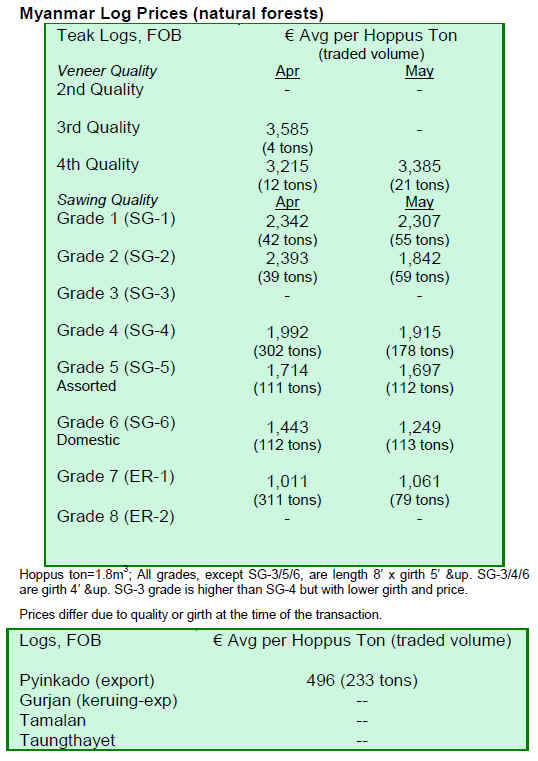

MYANMAR

6. BRAZIL

New opportunities for teak wood in Mato Grosso

According to Painel Florestal, consumers and producers

will have the opportunity to learn more about the use and

application of teak. Young teak is not commonly used in

Brazil by industries which, due to lack of knowledge about

its benefits, prioritize the production of mature teak wood

for furniture and other decorative items. To reverse the

situation, the Mato Grosso Forest Plantation Association

(Arefloresta) will hold the 10th Mato Grosso Reforestation

Meeting in early June to focus on the potential uses of

young teak. The event will discuss, among other issues,

the physical, environmental, silvicultural properties and

marketing of teak in Brazil and worldwide.

The state of Mato Grosso is the largest producer of teak in

Brazil, accounting for 90% of the supply, with world

demand currently exceeding the product¡¯s availability.

According to Arefloresta, this will be another topic of

discussion at the event. Many see the use of young teak as

a way to open the market for increasing product

consumption and consumer interest.

Currently, young teak in Brazil is used as firewood by

energy-producing companies, grain- and meat-processing

mills, and the ceramic industry, among others. The teak

plantation in Mato Grosso covers an area around 60,000

ha, with a potential sustainable production of 900,000 m³

per year, although with little utilization of young teak

wood. The objective is to expand this market, to maximize

the potential of young teak and encourage higher domestic

consumption, as currently the largest demand for young

teak still comes from other countries.

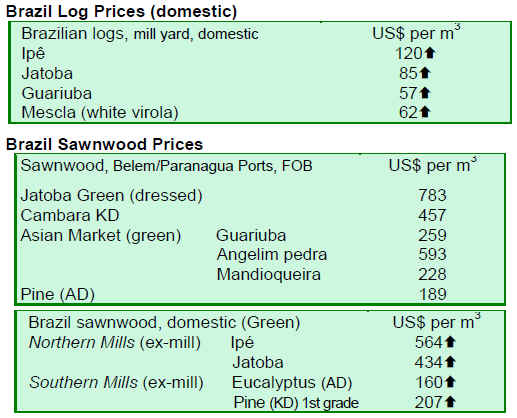

Export value plunges in April 2009

Brazil¡¯s wood products exports (except pulp and paper)

dropped 45.8% by value compared to the same period in

2008. The charts below show the volume and value of

Brazil¡¯s exports for April 2009 compared to the same

month a year earlier:

Mato Grosso timber exports plummet by volume

Timber products, which rank fifth in terms of exports from

Mato Grosso, decreased 45.5% by volume in the first

quarter of this year compared with the same period of

2008. According to Expresso MT, sales fell from USD55

million in 2008 (representing 4.3% of total exports

statewide) to USD25 million in 2009 (1.4% in 2009).

These data show the timber industry has already felt the

effects of the global financial slowdown. The

entrepreneurs of the sector have been negotiating with the

government to lower the official reference timber price,

the minimum price established for timber exports. They

contend that official reference prices are set too high,

thereby affecting competitiveness of the forest-based

sector.

Timber processing is considered a solid business.

However, if there are no buyers, the current crisis in the

sector is expected to get worse. A steep drop in sales

occurred in both the domestic and foreign markets. The

sector has stocked timber to sell, but the consumer is not

willing to pay a premium to cover the high production

costs of the product.

Timber industry seeks ways to reverse losses

Entrepreneurs of the timber sector and business leaders of

Paran¨¢ trade unions discussed solutions to address the

crisis in the timber sector and its business development

during a sectoral forum on the timber industry. The forum

was organized by the Federation of Industries of Paran¨¢

(FIEP) in Curitiba. Participants at the forum suggested

strategies to reverse declining sales in the sector such as

establishing a financing programme for residential

construction made from timber and investing in innovation

and technology.

At the forum, the Brazilian Association of Mechanically-

Processed Timber Industry (ABIMCI) presented data on

the situation of the timber industry in the Southern state of

Paran¨¢. Brazilian exports of solidwood products have been

decreasing since 2007, but the global financial crisis has

made the situation much worse. There was a 45% drop in

the volume of timber product exports in Paran¨¢ in the first

quarter of 2009 compared to the same period of 2008. The

problem worsened as the timber market in Paran¨¢ has

practically disappeared.

ABIMCI suggested a solution to foster and expand the

domestic market, by creating a programme for financing

timber-based construction. Other measures to address the

crisis included reducing high taxes, establishing proper

public policies in each state, and classifying the forestbased

industry in the category of agribusiness to enable it

to qualify for greater benefits.

7.

PERU

Government to distribute forest grants

The Ministry of Agriculture indicated that regional

governments would distribute new forest grants beginning

from 2010 to promote private investment in the forest

sector and help prevent illegal trade. The Director of the

Department of Forestry and Wildlife said there was

potential to consider nearly eight million hectares of

forests for the grants. He indicated the Ministry of

Agriculture would also transfer many forest-related duties

to the regions by 31 December 2009.

Peru clinches funding for forest conservation

Peru¡¯s Department of Environment has received EUR7

million from Germany to conserve forests and about

USD40 million from Japan to preserve forests that are

important to climate change mitigate. This will enable the

Peruvian government to set aside nearly USD50 million to

conserve forests in the Amazon and guarantee proper use

of wood resources, noted Minister of the Environment

Antonio Brack. The Minister also discussed the ongoing

process to address environmental services through

improved management of forest grants. He noted that

ecotourism was an important aspect of the conservation of

forests and should be considered an important

environmental service in Peru.

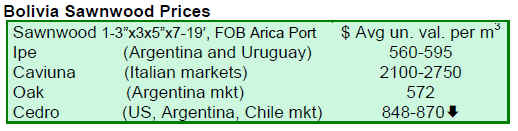

8. BOLIVIA

Bolivia reorganizes forestry agency

Under the new Bolivian Constitution, the

Superintendencia Forestal (SF), which was responsible for

the regulation and supervision of forestry matters in

Bolivia, will become subordinate to the Ministry of Rural

Development and Land. The new entity, ¡®the Authority for

Social Control of Forests and Land (ABT)¡¯, will regulate

activities associated with forests and agriculture and

ensure natural resources are used in a sustainable way. As

such, the functions of the ABT do not change much from

the old functions of the SF. It is not yet known whether the

headquarters for this new entity will be in Santa Cruz or in

the capital of La Paz. The rationale for the change,

according to some officials, is to generate additional

government savings and reduce bureaucracy.

9. Mexico

PROCYMAF programme to invest over 128 million

pesos

The National Forest Agency (CONAFOR) will allocate

over 128 million pesos to projects under the 2009

Communitarian Forest Development Programme

(PROCYMAF). The programme has recently approved

around 1,380 technical proposals for financing, which are

designed to benefit 792 agrarian centers in 12 states of the

country. The National Forest Agency will promote actions

to conserve and sustainably manage national resources of

common lands and indigenous forest communities by

identifying and consolidating the process of local

development.

A total of 2,384 technical proposals were received from

1,117 agrarian centers or associations of common lands

and communities in the states of Oaxaca, Gurerrero,

Michoacan, Jalisco, Durango, Chihuahua, Quintana Roo,

Chiapas, Campeche, the state of Mexico, Puebla and

Veracruz. The technical state committees of PROCYMAF

evaluated the proposals to see which were most

technically and socially viable. The states of Oaxaca,

Jalisco, Michoacan, the state of Mexico, and Durango

account for 56% of the proposals that will be supported

this year. Contracts and agreements with the beneficiaries

of the projects are in the process of being formulated.

10.

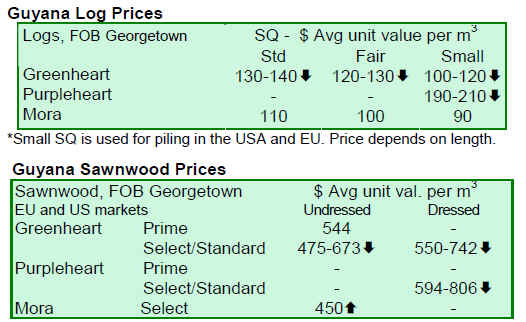

Guyana

Guyana¡¯s prices demonstrate stability over the

fortnight

Log prices for greenheart and purpleheart have remained

stable for the period of 1-15 May 2009 compared with 16¨C

31 April 2009. Prices for undressed sawnwood have also

remained fairly stable, while the prices for dressed

sawnwood (594/636) have marginally eased for the period

1-15 May 2009 as against 16-31 April 2009. Splitwood

prices for this period have been encouraging compared to

the last quarter prices.

Indoor furniture and craft items remained a stable

contributor to export value earnings compared to the

period 1-15 May 2009 as against the same period of 2008.

The Caribbean and European markets were the foremost

destinations for these value-added product categories.

The largest revenue earner from January to April 2009 was

sawnwood. Dressed sawnwood has dominated this product

category, representing 57% of total export revenue. Logs

have generated revenues accounting for approximately

10% of export revenue, down from 25% for the first four

months of last year. Value-added products, especially

doors, windows, spindles and other building components

remained stable, making an 8% contribution to export

earnings for both years. From all indications, export

revenues should increase in the third quarter and stabilize

in the last quarter of the year.

FPDMC hosts successful stakeholder forum

On 11 May 2009, the Forest Products Development and

Marketing Council (FPDMC) conducted a stakeholder

meeting to discuss the Council¡¯s strategic plan, which

includes working with stakeholders to improve the quality

and quantity of processed forest products both for the

domestic market and for export.

The meeting provided an opportunity for stakeholders to

share their views on a number of critical issues that impact

their business, the forestry sub-sector and the national

economy. The Council is also expected to monitor

marketing trends and engage stakeholders in this regard;

advise companies that need to diversify their product

range and markets; and intensify the promotion of the

Legal Verification System, which was started in 2007. The

newly formed FPDMC will also be at the forefront in

promulgating log export policy and training professionals

in relevant skills while continuing to support stakeholders¡¯

interests. It is expected that the FPDMC will assist the

forestry sector to be more competitive.

The Council¡¯s Chairperson noted the FPDMC had

deliberated on issues to take the industry forward. The

FPDMC will engage and work together with all

stakeholders, particularly to find ways to access markets

during the global economic slowdown. The Chairperson

added that the industry must be re-positioned to look

inwards for new market opportunities.

The FPDMC stakeholders¡¯ forum has broadened the

Council¡¯s mandate and guided the organization¡¯s strategic

and operational direction. It is now up to the Council to

organize itself and acquire the resources necessary to meet

relevant challenges and opportunities.

|