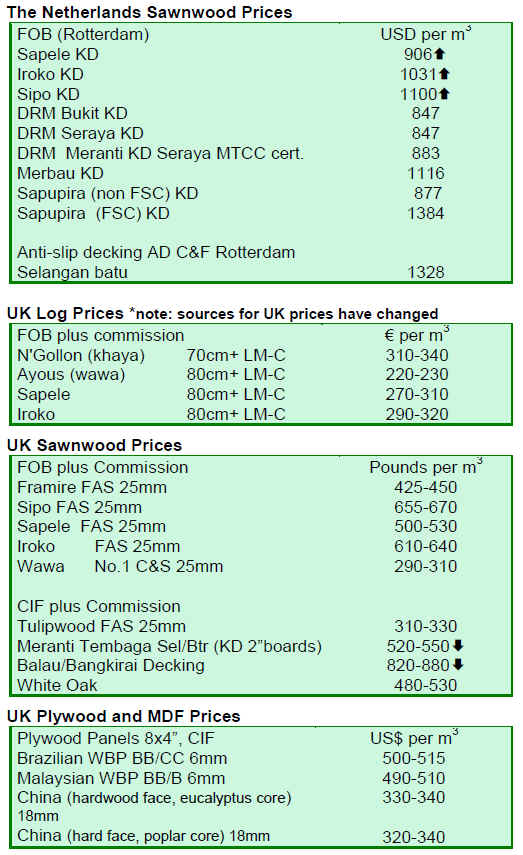

|

Report

from

Europe, the UK

and

Russia

No upturn yet in European forward demand

Reports from across the continent suggest very low levels

of consumption and forward purchasing activity. While

there have been moves by importers in some countries to

fill gaps in stocks, orders tend to focus on specialty

products and dimensions and volumes are generally low.

Existing landed stocks of mainstream items such as sapele

are still described as relatively high compared to the low

volume of consumption. Meanwhile there is intense

competition between importers for orders. End-users are

working on very low inventories and tend only to place

orders if they can be assured that products are already in

stock.

However, there is general awareness in the European

import sector that supplies in the major tropical producing

regions are now restricted due to very low levels of

logging activity this year and following widespread mill

closures. With respect to African sawn lumber, importers

report that delivery times to Europe now extend up to 5

months. Forward prices for key species of tropical

hardwood on offer to European buyers have remained

relatively stable over recent months, but the expectation

amongst European agents is that due to the extremely low

levels of production, prices would rise very quickly in the

event of any significant upsurge in demand.

French hardwood import levels show significant downturn

Of all European countries, only France has so far

published import trade data for the first quarter of 2009. A

preliminary analysis of this data indicates a very

significant downturn in the level of hardwood sawn

lumber imports this year. The analysis suggests that

overall French hardwood lumber imports reached only

121,000 m³ in the first 3 months of 2009, a figure which

compares to 159,000 m³ in the first 3 months of 2008 and

over 300,000 m³ in the same period of 2007. At the same

time, there have been large shifts in the source of tropical

sawn lumber imported into France this year. While direct

imports from Cameroon increased from around 17,000 m³

in the first quarter of 2008 to 21,000 m³ in the first quarter

of this year, direct imports from Brazil declined from

49,000 m³ to only 18,000 m³ during the same period.

Direct imports from Malaysia, Ghana and Côte d’Ivoire

were also well down on last year’s figures.

On the other hand, there appears to have been a very

strong increase in the level of indirect imports of tropical

sawn wood into France from the Netherlands and

Germany. French imports of tropical sawn lumber from

the Netherlands reached 25,000 m³ and from Germany

reached 3,000 m³ in the first quarter of 2009, up from

negligible levels in the same period last year. Such a shift

might be explained by the strong focus on just-in-time

ordering, which has encouraged a partial switch away

from the forward market in favor of heavier reliance on

large stockists in neighboring European countries.

Belgian, Dutch and UK importers see mixed fortunes

The very large European importers in the Benelux

countries and the UK have been very heavily exposed to

the downturn due to a business strategy that depends on

large stock holdings to iron out problems for

manufacturers and merchants associated with long lead

times in the hardwood import sector. The fact that these

companies have been selling off existing stocks of

standard items such as sapele at below replacement cost

has been a major factor deterring any significant increase

in forward demand during recent months.

But while these importers with large stock holdings are

heavily exposed to financial risk during the recession, the

recent very strong focus on just-in-time ordering among

manufacturers and builders merchants has also given them

an edge in the market place. Several of these companies

interviewed in a recent feature on the Belgian and Dutch

trade in the TTJ commented that their strategy of

providing customers with a very wide range of species and

specifications for immediate delivery has brought in many

new customers.

These companies are now building on this success through

continued strategic moves into a wider range of valueadded,

further processed and non-standard items with the

objective of tailing material more tightly to customers

needs. For example, one large Dutch importer interviewed

by the TTJ noted that they are developing as much

business as possible in boules, and square-edged and nonstandard-

sizes, especially thicker material for flooring and

other interior applications. These companies also comment

that the higher-quality end of the market has been holding

up reasonably well during the recession, boosted by

reasonable activity in the renovation portion of the market

even as the new-build sector has ground to a halt.

The TTJ interviewees also note that the certified wood

section of the market has been holding up well in the

Netherlands and the UK as public sector projects have

become relatively more important during the recession and

with growing concern for sustainable construction. One

large Belgian importer noted that ‘out of every 20

inquiries we get today, half are for FSC-certified [wood].

As a result, nearly all our tropical range is now FSC and

we’re getting good volumes in certified species, such as

sipo and sapele, in both dimension and random sizes’.

|