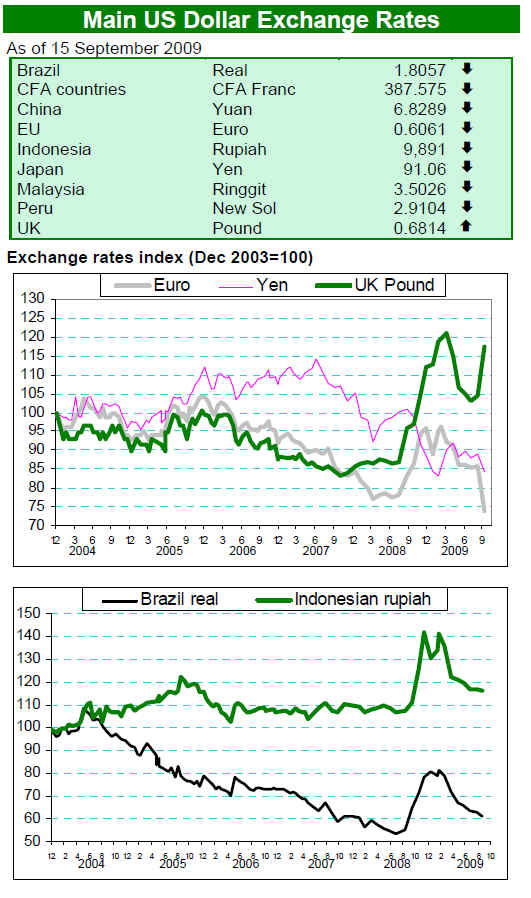

| Home: Global Wood | Industry News & Markets |

| Home: Global Wood | Industry News & Markets |

|

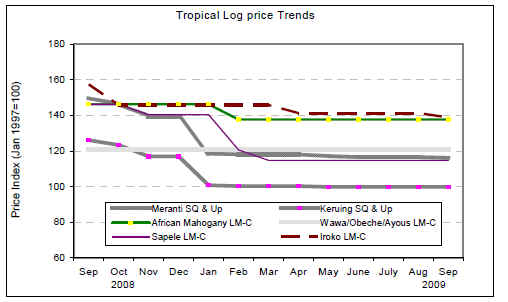

Tropical Timber Product Price

Trends |

|

|

|

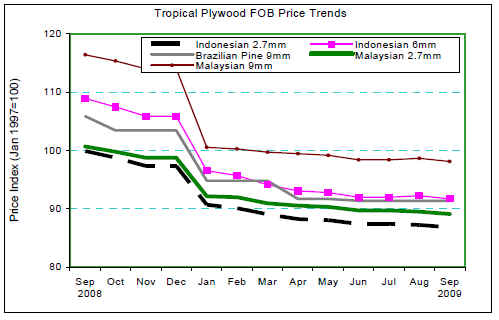

Note: Y-axis: Price index (Jan 1997=100) |

|

��Tropical Log Price Trends |

|

|

|

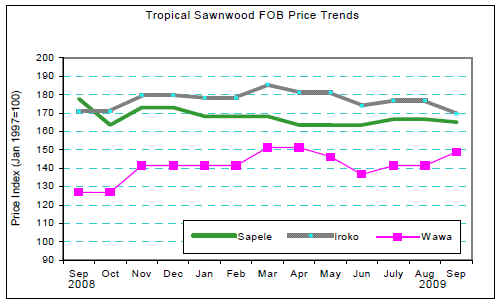

Tropical

Sawnwood Price Trends |

|

|

|

Tropical

Plywood Price Trends |

|

|

|

|

Source: ITTO' Tropical Timber Market Report |

CopyRight (C) Global Wood Trade Network. All rights reserved.