|

1.

CENTRAL/ WEST AFRICA

Slow Start to year

The harsh winter weather in northern importing countries

has been the biggest influence on the timber trade in the

first weeks of 2010. Business is slow in most areas.

In Europe many companies closed for up to two weeks

over the Christmas and New Year period and the difficult

weather conditions with snow, ice and below freezing

temperatures are affecting resumption of normal working

of factories, schools and offices and building activity.

Although most consumer countries have technically

moved out of recession, there remain financial problems

especially in UK. Economists, as well as ordinary people,

are aware of a tough year ahead with prospects of higher

taxes and lower trade levels.

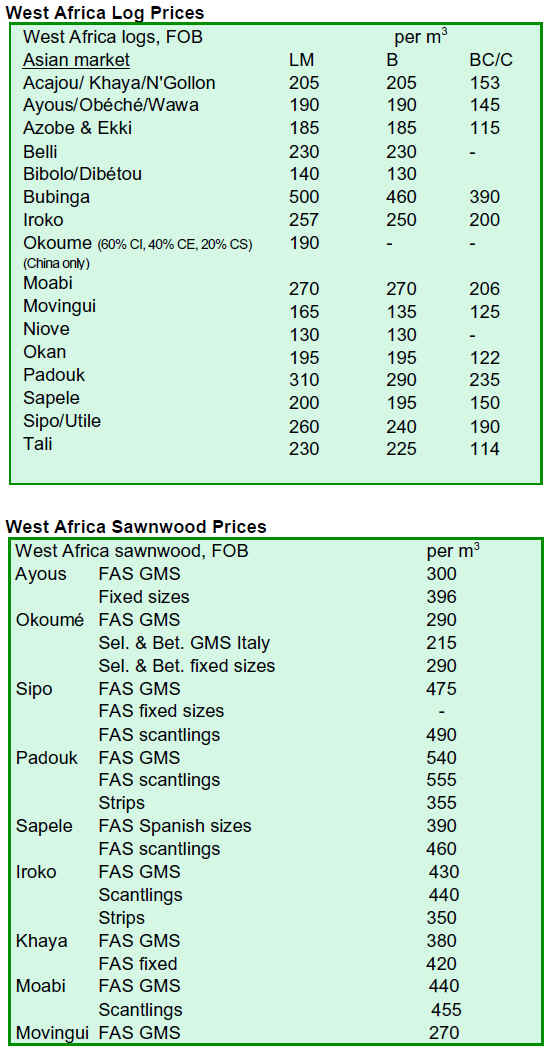

In the W. African timber trade the present situation

appears to be of not quite at a standstill but flat, with little

interest reported from buyers in chasing up new purchases.

Log prices have not moved over the past four weeks and

there are few indications as to how the markets will

develop in the first quarter. Sawn lumber prices also have

held very steady over the past few weeks although traded

volumes have been low and business continues at low

levels.

Gabon keeps trade waiting

The uncertain position in relation to the announced ban on

log exports by Gabon has, if anything, exacerbated the

near standstill in the timber sector. After the ban was

announced buyers did immediately begin seeking

alternative log sources but have held back until there is

clarification on the details of the ban.

The SEPBG, the port authority in Gabon has apparently

halted all loading of ships until the situation is made clear.

There are rumors that consideration is being given to

allowing the export of logs already cut until the end of

March.

Other rumours hint of heavy felling to have logs on the

ground in the hope that felled logs could be exported in a

grace period. Other sources hint at a possible

strengthening of existing regulations which require a

commitment to invest in local processing before log

exports are allowed. However, all this is pure speculation

by the trade.

Exports of non-premium logs

On the supply side, the unexpected but timely relaxation

of exports of logs of non-premium species from Cameroon

may well have been a stabilising factor for the W. African

trade. It remains to be seen if log exports from Liberia will

resume in any meaningful volume during 2010.

Logs are still exported from Congo Brazzaville and lately

also from the Democratic Republic of Congo. Whether

these countries can fill the supply gap resulting from a

Gabon ban is far from clear.

China would be the consumer country most affected in the

short term but no doubt would look to increase log

purchases from other countries such as Papua New Guinea

and Solomon Islands, though this would have to be in

alternative species some of which would not be a

substitute for okoume for peeling.

In the medium term the Gabon sawmills and plymills will

have to resume or step up to full production and place

much more emphasis on marketing their processed

timbers. This will not be easy given the slow market

conditions for processed timbers over the past 18 months.

In the meanwhile mills in Ghana and Cameroon have been

working under capacity and might well have a market

advantage, being able to quickly increase production in

response to any increase in demand.

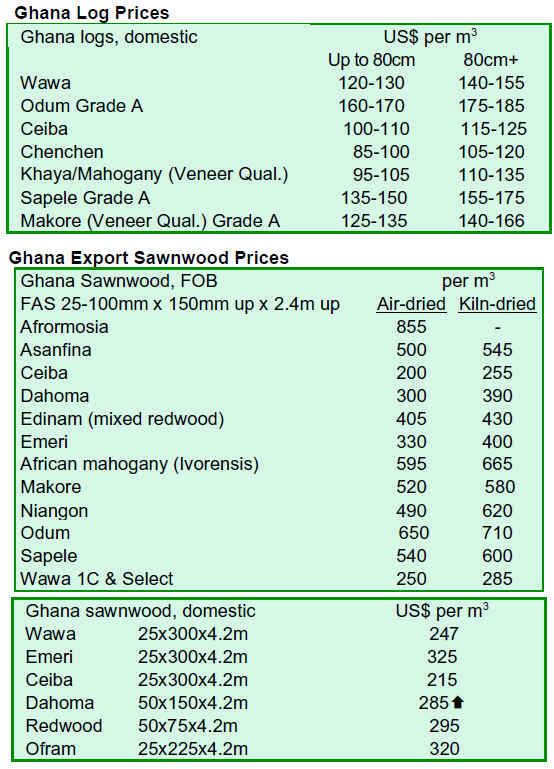

2. GHANA

Export performance

Ghana realised Euro 98 million from its export of

320,660cu.m of wood products in the first nine months of

2009. This compares to 430,081cu.m for the same period

in 2008.

Exports in 2009 (first nine months) fell 25.4% compared

to 2008. This was largely the result of deceased export

volumes in all trading products except air dried lumber,

curls veneer, and plywood.

In the same period there was a 32% drop in revenue

compared to the same period in 2008. The table below

summarises the export performance for the first three

quarters of 2009 compared to the same period in 2008.

Overland Export Trade

Ghana improved its overland trade performance to the

ECOWAS market in the three quarters to September 2009.

The main products in this trade are air dried lumber and

Plywood and the main markets are Nigeria, Senegal,

Niger, Gambia, Mali, Benin, Burkina Faso and Togo.

These countries altogether absorbed about Eur36 million

of Ghana¡¯s total wood export volumes to neighbouring

African countries. Total trade with other African countries

was worth Euro 42 million (for 168,390 cu.m).

Air dried lumber export by road in 2009 increased

dramatically to 29,000cu.m, from the previous year figures

of 2,514cu.m.

The main species were Chenchen, Mixed White Wood,

Ceiba, Dahoma, and Wawa. The bulk of the exports were

by Rahmusa Company Ltd and Moha-Tony Diasso

Brothers among others.

Overland plywood exports increased by 11% in value for

2009 compared to 2009. Ceiba, Mahogany, Asanfina,

Chenchen and Ofram plywood dominated this trade in

2009.

Inflation eases

The year on year inflation for Ghana fell to 17% in

November 2009, as announced by the Ghana Statistical

Service. In a statement, the Governor of the Central Bank

said Ghana¡¯s inflation rate will ¡¡ãdefinitely¡¡À fall in

December 2009 and will continue to ease throughout

2010. ¡¡ãInflation is coming down and it will continue to

come down in the next 12 months,¡¡À the governor told

reporters.

3.

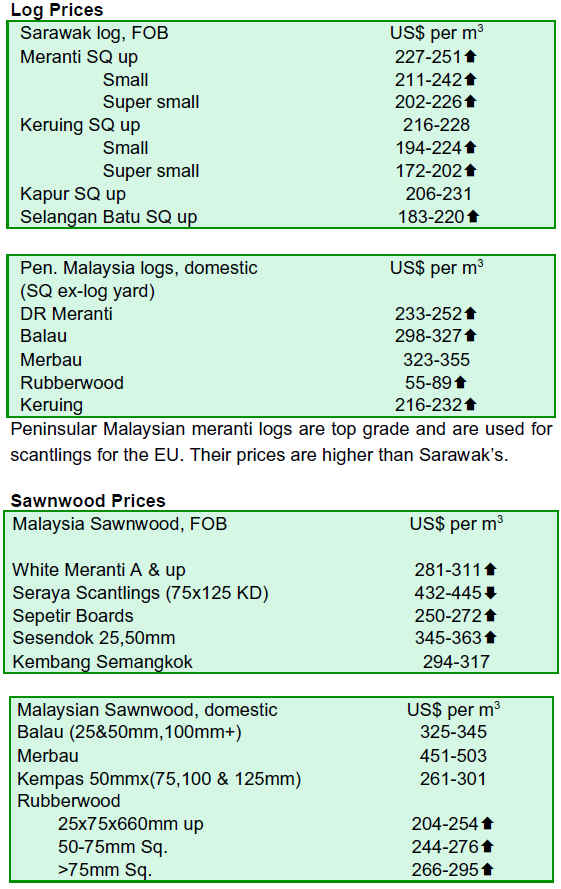

MALAYSIA

Optimism returns

Malaysian timber companies greeted the New Year in a

positive mood now there seems some improvement in

demand.

The global economic slowdown considerably weakened

the demand for Malaysian timber products. In the worst of

the crisis production in Malaysia fell almost 40%, with

plywood and other panel product manufacturers being

hardest hit.

The trade is anticipating growing demand for certified

timber products which will give a boost to products from

plantation timbers.

In addition to the modest improvements in demand for

primary products, producers report that demand for

Malaysian furniture seems to be picking up after a tough

2009.

International buyers are slowly returning to the Malaysian

market after a one year absence it seems. The trade in

Malaysia suggests that the main reasons for their return

even in continuing difficult trading conditions is the high

quality of workmanship and the ability of Malaysian

companies to deliver on time.

Although furniture from China is competitive in terms of

pricing, timely delivery remains a major problem for some

overseas buyers who want just in time deliveries.

ASEAN FTA

The secretary-general of the Malaysian Ministry of

International Trade and Industry (MITI) commented that

the country is ready for the full implementation of the

ASEAN-China free trade agreement (FTA).

Businesses in the country are ready to do business with the

trading bloc of almost 2 billion consumers in ASEAN,

with a combined gross domestic product (GDP) of around

US$5 trillion.

Beginning January 1, 2010, China and the Asean-6,

(Brunei, Indonesia, Malaysia, the Philippines, Singapore

and Thailand), will ensure full implementation of the FTA

by eliminating the duties on up to 90% of products

according to the agreement.

China is Malaysia's fourth largest trading partner, after

Singapore, the US and Japan, with trade in 2008 amounted

to RM130 billion, or 11% of Malaysia's global trade in

total. Malaysia's exports to China in 2008 amounted to

RM63 billion, which accounted for almost one-tenth of

global exports. In the first 3 quarters of 2009, trade with

China amounted to RM89 billion, with exports standing at

RM46.8 billion.

4.

INDONESIA

Competitive China

In contrast to the confident mood in Malaysia, the

chairman of the Association of Indonesian Furniture and

Handicraft Exporters (Asmindo), has reportedly said that

the furniture industry in all ten member countries of

ASEAN share a common appreciation of the challenges

and risks of the ASEAN-China FTA.

In particular Asmindo thinks that furniture producers are

not ready to face the competition from Chinese producers.

The fear expressed is that furniture imports into ASEAN

countries from China could capture a major slice of the

domestic market. Imports currently account for around

30% of the domestic market and this could grow as

imports become cheaper as tariffs are removed.

Currently, there are 314 tariff items from eight sectors

listed under the FTA. Asmindo is said to have been

lobbying the Indonesian authorities to modify or suspend

at least 5 of the 12 tariff items listed within the furniture

sector.

Export performance

Exports of Indonesian timber products, especially

sawnwood and plywood, have been on a decline since

2003, when exports were over 5 million cubic metre

However, exports in the following year fell to 4.5 million

cubic metre; to 3.5 million cubic metre in 2005; 3 million

cubic metre in 2006; 2.9 million cubic metre in 2007, and

1.68 million m3 in 2008.

Total exports for year 2009 only managed to reach 1.2

million cubic metres up to November 2009.

Indonesian timber companies have reportedly said that it is

inappropriate government policies and the failure to grasp

present day market realities had contributed to this decline.

The trade says that while the size of the international

timber market has expanded over the past decade,

Indonesia¡¯s share of that market had declined.

They added that China trade model was good as the sector

has diversified its products and improved its value-added

production technology.

The industry also said that Malaysia is another good

example to emulate; here industries manage pricing of

timber products by spreading costs over a range of

products including logs. Indonesian companies do not

have this opportunity because of a log export ban in

Indonesia.

5.

MYANMAR

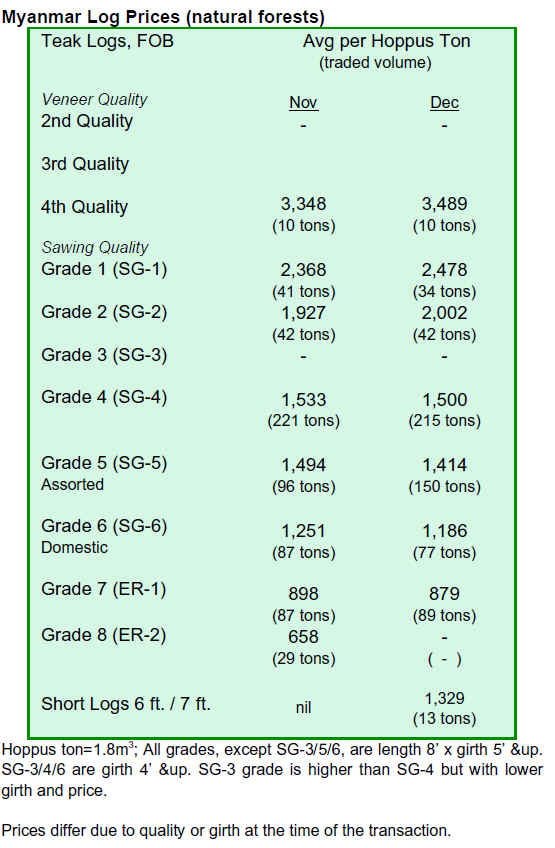

Monthly Teak sales

The monthly Teak sales involve a prior inspection by

buyers and the submission of written tenders for logs. The

logs are available for inspection at Myanmar Timber

Enterprise (MTE) log-yards. These log yards are roughly

within a maximum 30 mile radius from the ports.

Logs sold by tender are mostly shipped within two months

from purchase, but there are instances where shipments

may take longer. MTE may charge ground rent if the logs

are not shipped at the end of three months.

The majority of the shipments made using containers.

Containers are stuffed at MTE container yard and trucked

to the vessels. Buyers, singly or jointly with other buyers,

may also ship using break bulk carriers. The mode of

shipping is left to buyers¡¯ choice.

6. INDIA

Firmly on growth track

Indian exports grew 18% last month and industrial activity

figures show a continuous improvement over the first

three quarters of 2009 with an increase of 11% being

noted in October 2009. This positive economic activity is

helping enormously to create jobs in the country.

After coping with a tough 2009, progress is now seen on

all fronts and as the global economy appears to be

recovering GDP growth forecasts are optimistic. In

December 2009 GDP stood at 7.5% and for 2010-11 it is

expected to be around 9%.

Follow up on Copenhagen

India¡¯s minister for Environments and Forests, Mr.Jairam

Ramesh, has announced that the country¡¯s action plan, as

called for by the Copenhagen Accord, is ready.

India has shown preparedness to reduce emission by 20-25

percent of 2005 levels and that a low carbon growth

strategy will be developed. The minister noted that India¡¯s

per capita carbon emission is among the lowest globally.

Analysts report that builders and architects in India are

considering how to make use of traditional building

materials such as wood, bamboo, limestone and clay.

Consideration is also being given to rainwater harvesting

and the use of solar energy for lighting, water heating and

other purposes.

Industrial plantations

For absorption of carbon dioxide greening programmes are

being mooted. Currently, industrial plantations are being

increasingly established by large private enterprises and on

a small scale by farmers and other landowners.

The government is encouraging the planting of fast

growing and high carbon dioxide absorbing species like

bamboos which also provide raw materials for paper and

rayon pulp and also for rural housing and handicrafts.

The indications are that the government will soon

announce the constitution of an expert group to monitor

low carbon growth strategies in the industrial, transport,

agriculture, building, energy and forestry sectors.

ASEAN FTA activated

As of the1st January 2010 customs duties in India have

been reduced on goods imported from ASEAN countries.

The basic duty on logs has been reduced from 5% to 4%,

on sawn timber from 10% to 7.5 % and on MDF,

particleboards, plywood, veneer sheets and soft boards

from 10% to 7.5%.

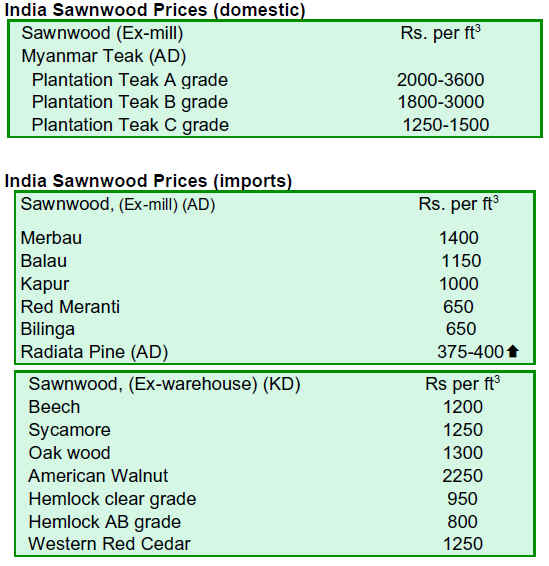

Trade news

Sales of Teak and other hardwoods by auctions have

continued in Gujarat, Central India and Kerala and reports

are confirming firm prices and brisk sales of freshly felled

timber that has been arriving post monsoon. Quality

standards are being well maintained it is reported.

For past several months the trade has said that the quality

of logs coming from Myanmar has not been very

satisfactory so local manufacturers are opting to pay a

little more and buy the local hardwoods.

Continuous PB line

Wood News in India has reported the awarding of a

contract for first ever continuous Particleboard Production

line by Star Panel Boards Ltd. Bangalore to Dieffenbacher

of Germany.

The plant is apparently designed for a daily capacity of

over 1000 cubic metres. Full commercial production is

forecast to begin in 2011. This domestic production will

narrow the gap between demand and local supply and

reduce India¡¯s dependence on imports.

Wood sailing vessels

In other news, the Economic Times of India has reported

brisk business for coastal sailing vessels being built at

Mandvi Kutch, an area famous for this craft for centuries,

because of the highly skilled local workforce and the

proximity of the Teak forests of Dangs. Timbers from

Malaysia are also used in the making of these boats which

comes to Kandla.

The size of vessels being built range from 150 to 1500

tones capacity and these vessels are used to carry goods

the Middle Eastern and North African countries. Ship

builders are saying that their order books are full up to

2012.

7. BRAZIL

Exports Drop in Alta Floresta

Contrary to exports in Sinop, Sorriso, Lucas do Rio Verde

and Nova Mutum, wood products export from the

municipality of Alta Floresta, a major regional timber

exporter, dropped between January and November 2009,

compared to the same period of 2008.

The value of exports reportedly dropped from US$ 12.7

million to US$ 10.8 million. The non-conifers products

trade was worth US$ 9.6 million, a 6.8% reduction

compared to 2008, when it reached US$ 10.3 million.

As for the main export product, sawnwood wood with a

thickness exceeding 6 mm, trade totaled US$ 363,800

(-81% from Jan-Nov 2009 compared to the previous

period); wood block, planks, veneer and wood

frames/profiles, however were traded for US$ 305,200

(+684%) and ip¡§º wood products earned just US$ 194,400

(-47%).

The main export destinations for products from Alta

Floresta are the United States (US$ 5.7 million), Canada

(US$ 1.7 million) and Spain (US$ 1 million).

Wood furniture cheaper

A tax exemption scheme on furniture has been in force

since November 27, 2009. The tax on such products varies

between 5% and 10%. Some furniture companies had

suggested that they could pass on to consumers a price

reduction greater than the tax break. According to the

Association of Furniture Industry of Rio Grande do Sul

(Movergs), the main cluster of the furniture industry in the

country, the measure may lead to a fall of about 20% in

prices consumer pay.

According to furniture entrepreneurs, even though it is too

early to analyze the impact, there are signs of a recovery in

sales.

The Brazilian Furniture Manufacturers Association

(ABIMÓVEL) says that the sector is facing a crisis as a

result of the average drop of 10% in sales in 2009. The

Association expects that between December 2009 and

March 2010 it will be possible to recover about 25% of

sales.

In the wood furniture clusters of Ub¡§¢, Linhares and

Arapongas, where there is a high proportion of exports,

there was a drop of up to 25% in sales in recent months.

With declining exports, the companies now began to

depend more on the domestic market.

Fighting Illegal Logging

By November 2009 the Brazilian Federal Police had

seized some 9,000 cubic metres of illegally transported

and processed timber in Northern Mato Grosso. The police

have mounted the longest operation to fight illegal logging

activities in the region.

The operations are coordinated by the Federal Police in

Mato Grosso, and also implemented in the states of Par¡§¢,

Rondônia and Maranhão, in the Brazilian Amazonia.

In Mato Grosso, there are two operational bases of the

"Arco de Fogo" operation: one each in the municipalities

of Ju¡§ªna and Sinop.

In this operation, 30 federal policemen and 30 officers

from the National Force for Public Safety are working. In

addition to the seized timber, 100 cubic metres of

illegally-produced charcoal were seized and 221 furnaces

destroyed.

The Brazilian Institute of Environment and Renewable

Resources (IBAMA) will soon reveal the total amount of

fines levied against companies in the "Arco de Fogo II

Operation", carried out between January and April 2009.

The fight against illegal logging and timber smuggling in

the Amazon has so far resulted in R$31.3 million in fines.

According to IBAMA, the majority of fines were imposed

on timber companies for raw material storage or sale

without license.

The Amazon Fund

The Brazilian Forest Service and the Chico Mendes

Institute for Biodiversity Conservation (ICMBio) may

receive Euro 15 million from the German government,

through the KfW Development Bank. This money would

be to develop the project ¡®Support Forest Management for

Sustainable Production in the Amazon¡¯.

The German donation would support activities in the

forest concessions and will help the Forest Service to

improve the infrastructure of regional units in Porto Velho

(RO) and Santar¡§¦m (PA), and to set up an additional four

offices in the Amazon.

The funds would also support the demarcation of some

national forests, preparation of management plans and

implementation of advisory boards for national forests

(FLONAs) by ICMBio, which are prerequisites for a forest

concession.

In other news, the Government of Norway has announced

an increase in its contribution to the Amazon Fund to US$

150 million in 2010, apparently after seeing evidence of

deforestation reduction in the region.

The Fund was created by the Brazilian government in

2008 aimed at reducing deforestation in the region and the

fund is managed by the National Development Bank

(BNDES).

According to recent data, deforestation in the Brazilian

Amazon between July 2008 and June 2009 was 65% less

than the average recorded between 1996 and 2005 and

over 40% below the deforestation rate of the previous

year. These results are yet to be verified.

8.

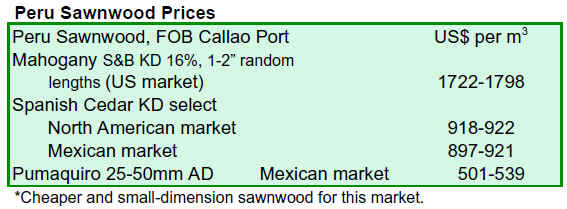

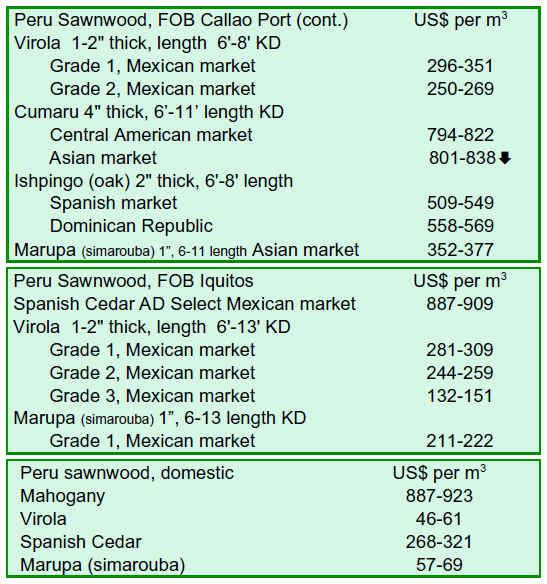

PERU

2009 exports down 34%

According to data from the Export Association of Peru

(ADEX), wood sector exports from January ¡§C November

2009 were of US$135.09 million FOB, down 33.6% on

the same period in 2008.

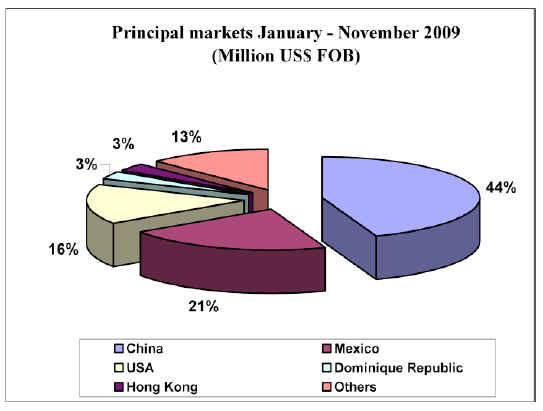

The three main export markets were China, Mexico and

the United States, accounting for over 80% exports of

wood products. The New Zealand market was significant

in 2009 taking volumes of railway ties. On the other hand,

the Mexican market remained subdued and imports from

Peru fell over 60% and no exports of mouldings were

recorded in 2009.

Peru¡¯s export data up to November 2009 shows the

weakening of Canadian demand (-65%) and a similar

picture emerged for the Hong Kong market which fell

38% in 2009.

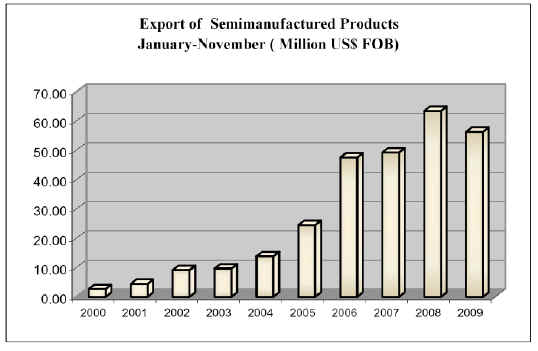

Semi-manufactured products accounted for 42% of

exports from January to November 2009 and were worth

US$56.38 million FOB compared to US$63.44 million

FOB for 2008 (-11%).

The main market for semi-finished wood products was

China represents 77% of the total. Chinese imports from

Peru grew almost 50% in 2009.

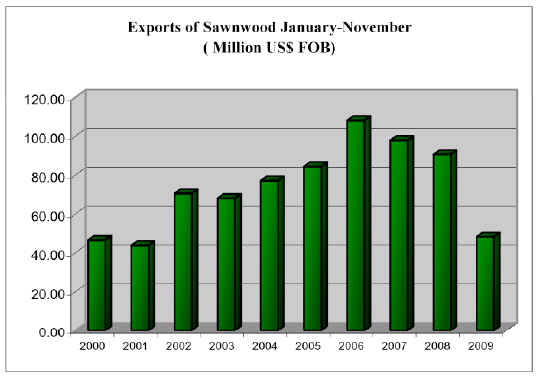

Sawnwood represented the second major wood product

export item in 2009. The value of exports of sawnwood

January ¡§C November 2009 was US $ 49.29 million FOB

down 46% on a year earlier.

The main market for sawnwood from Peru was China

which took around 34% of the total sawnwood exports.

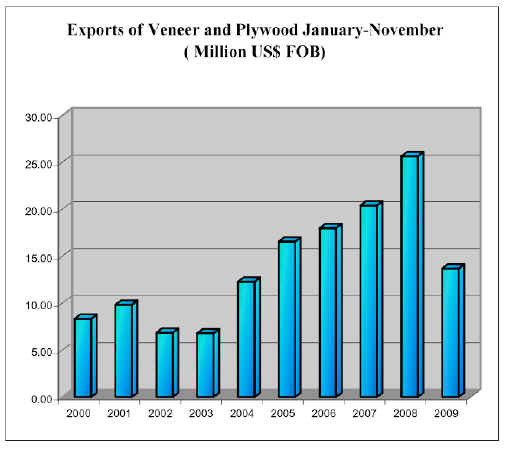

The value of veneer and plywood exports up to November

2009 stood at US$13.67 million FOB but this was down

47% on a year earlier.

The main destination for veneer and plywood from Peru

was Mexico (83% of total product exports). Mexican

imports from Peru were affected by weak demand in the

US for processed products and consequently Mexico¡¯s

imports from Peru declined.

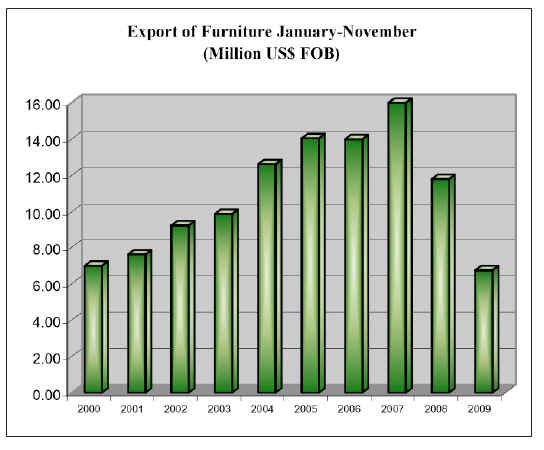

The exports of furniture and parts up to November 2009

were worth US$6.74 million FOB compared to US$11.81

million FOB in 2008 and this represents a fall 43%. The

main market for exports in this sub-sector is the United

States, accounting for 49% of all furniture and parts

exports but up to November 2009 US imports had dropped

53%.

8.

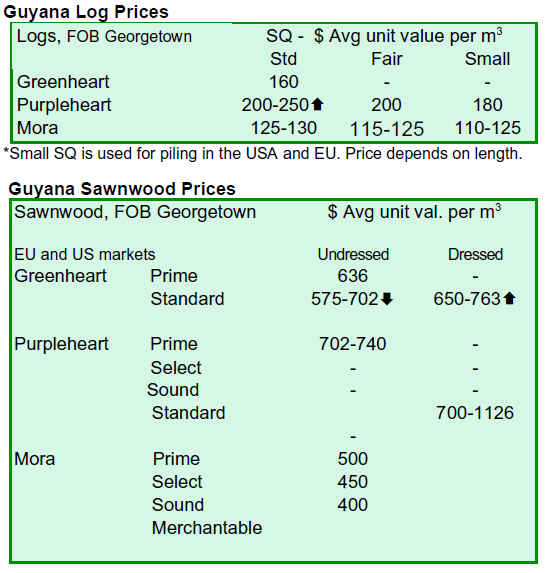

Guyana

Price movements

Prices for Greenheart logs remain were relatively stable.

Purpleheart standard sawmill quality prices climbed while

Mora log prices stayed firm.

Sawnwood prices were highly favourable over the past

weeks. Prices for dressed local Washiba, internationally

traded as Ipe, went as high as US$1600 per cu.m. Nondressed

Greenheart prices recorded modest gains in the

prime class while the select category experienced a decline

in prices.

Only prices for Purpleheart select moved up to a fairly

good average price while Mora prices remained stable.

Dressed Greenheart average prices were favourable

recently and dressed Purpleheart enjoyed buoyant prices.

Plywood prices eased slightly for BB/CC qualities.

Value added products, mainly door and door sets as well

as indoor furniture and mouldings recorded higher average

prices than in late 2009.

Log tracking strengthened

The Guyana Forestry Commission recently reported on

ITTO supported efforts to improve the detection and

prevention of illegal harvesting and trade in the country.

Part of this work involved the improvement of Guyana¡¯s

log tracking system. In 2001, a national log tracking

system was implemented and was monitored through

manual verification. Under this system, cut logs and

stumps are identified using a plastic barcode tag that is

attached immediately after logging or when logs are

converted into pieces at timber collection points.

The manual implementation of this system however, did

not allow for the full benefits of traceability and

verification of origin, to be realized. This aspect of the

work recently undertaken aimed at helping prevent illegal

logging and trade in illegally harvested timber by utilizing

a timber tracking system based on barcode utilization in

the harvesting of tropical forests, shipment and exporting

stages.

Forest carbon stock assessment

The Government of Guyana has embarked on a national

programme that aims to continue to maintain the

sustainable management of its forest as a contribution to

climate change mitigation. It is anticipated that this effort

will attract international resources to foster growth and

development along a low carbon emissions path.

As an initial step to the implementation of a monitoring,

reporting and verification (MRV) for Guyana, a road map

for the development of a MRV system for REDD+

participation for Guyana was designed following a

stakeholder participation session.

The Guyana Forestry Commission, on behalf of the

Government of Guyana, has indicated that it requires the

services of an experienced remote sensing and GIS

consultant to undertake comprehensive, consistent and

transparent assessment of forest area change.

More information on this call for proposal can be found at

the Guyana Forestry Commission¡¯s website at

www.forestry.gov.gy

|