|

1.

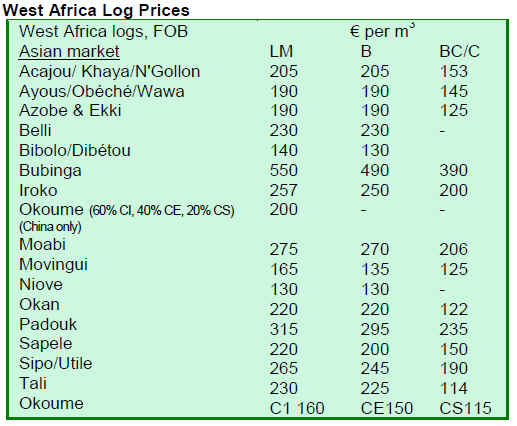

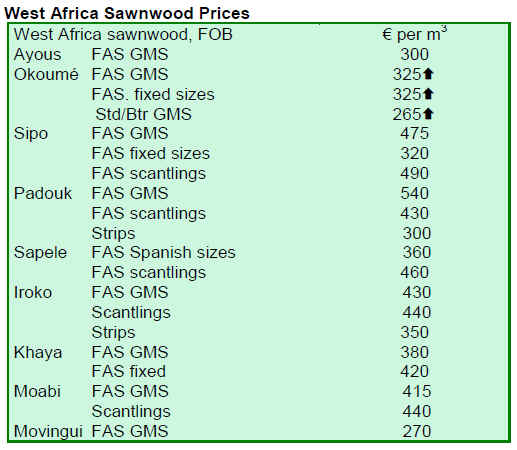

CENTRAL/ WEST AFRICA

FOB prices largely unchanged

Although details of the log export ban in Gabon have not

yet been totally finalised, the log markets have remained

remarkably calm. The prospect of the loss of such a major

player from the log market has not resulted, as yet, in

noticeable price movements for logs.

Price changes that have been recorded over the past four to

six weeks have more to do with improved demand from

Europe. However these increases are built on a very low

level of demand and are still very moderate. Better

demand in China and India has also supported the modest

movement in prices.

Return of S. African buyers

Analysts report that South African importers allowed

timber stocks to run low and have now returned to the

market and are actively buying sawn Okoume. This has

encouraged sawmillers in Congo Brazzaville and Gabon to

raise prices and there are indications that sawn Okoume

prices will continue upwards into the second quarter.

Clarification also is awaited on details of the log export

situation in Cameroon. There has been relaxation on

exports of lesser know species and, more recently, some

indication that special dispensations may be made in

respect of prime timbers.

Currently, production across W. Africa is relatively low

because of the rain season, so finalising a firm decision in

log exports in Cameroon is not so urgent.

Positive trade expectations

Traders are reportedly expecting that Okoume, Okan,

Sapele and Sipo log export prices will continue to firm.

Higher log prices should encourage sawmills in the

Central African Republic to resume production of top

quality Sapele for export through the port of Douala.

Because of the high cost of road transport for the almost

1,000km journey, sawnwood exports via Douala is viable

only when prices are some Euro 30 ¨C 50 above the very

low level of recent months.

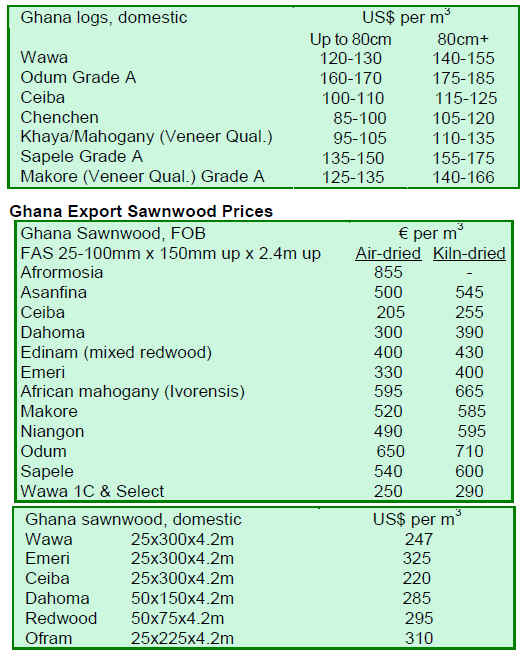

2. GHANA

Q4 timber contracts

Data available from the Timber Industry Development

Division of the Forestry Commission (TIDD) indicates

that contracts for a volume of 94,369 cubic metres (down

17% Qtr on Qtr) and 2,475 pieces of furniture parts were

processed and approved for export during the fourth

quarter of 2009.

There was a sharp increase in furniture parts export as a

result of two major parts shipments for the Togolese

market undertaken by Portal Limited, a Takoradi based

timber firm. The TIDD report indicates that Mim

Scanstyle Ltd, once the major furniture parts exporter,

submitted almost no contracts for export approval during

the same period.

In the fourth quarter 2009 there were declines in almost all

the major export wood products with the exception of

Finger Jointed/Laminated products, for which exports

(3,696 cubic metres) increased by 39% compared to the

previous quarter.

There were also declines in export volumes of sawnwood,

plywood, plantation poles/billets/logs, sliced veneer,

rotary veneer and mouldings compared to the previous

quarter.

Sawnwod continued to be the leading export wood product

from Ghana, contributing 47% of the total volume of

exports in the quarter.

Price and market performance

Overall there were no changes in prices during the quarter

under review. Prices were stable for most of the wood

products.

Though the global economic crisis, which led to a

meltdown of prices for wood products for most of 2009,

has eased, Ghana¡¯s exporters of wood products still find it

difficult to achieve prices above the TIDD Guiding Selling

Prices (GSP).

Prices of Mahogany (Khaya ivorensis), which is the main

sawnwood species for the US market, started to show

signs of improvement during the fourth quarter of 2009.

Most contract prices approved were at around US$750 per

cubic metres, with a few achieving as high as US$800 per

cubic metre. Prices in the previous quarter were in the

range of US$720 per cubic metre, well below the average

GSP level of US$860 per cubic metre.

China a major buyer

China is becoming one of the most important markets for

Ghana¡¯s wood products, especially for high density

sawnwood species. The majority of contracts for Denya

submitted for approval by the TIDD during the fourth

quarter 2009 were for the Chinese market. Prices were in

the region of US$400 per cubic metre. Previously, the best

average price was around US$350 per cubic metre.

Nigeria imports plywood

Nigeria continued to be the major consumer of Ghana¡¯s

plywood during the quarter under review. Due to the

depreciation of the US Dollar against the Euro, many

Nigerian buyers complained that the TIDD GSP for

plywood was on the high side, though TIDD prices quoted

in Euros had not changed.

New forest plan

According to a Ghana News Agency report, the Forestry

Commission is to update management plans for all forest

reserves in the country.

Apparently, plans over twenty forest reserves in the

country have been earmarked as pilot areas. Four pilot

areas namely, Nsuensa-Bediako, Esukawkaw, Pra-

Anuonand and Worebong South are in the Eastern Region.

At a 2-day planning workshop held to introduce a draft

management plan for the Nsuensa-Bediako Forest

Reserve, the Eastern Regional Forestry Manager, Mr. J E

Manu, said he wanted to bring all stakeholders in the

sector together for discussion on the plan to ensure the

effective and sustainable management of forest reserves.

Mr Manu said the Nsuensa-Bediako Forest Reserve

management plan was written in 1959 to cover a period of

five years but there had been no review undertaken since.

Ghana Log Prices

3.

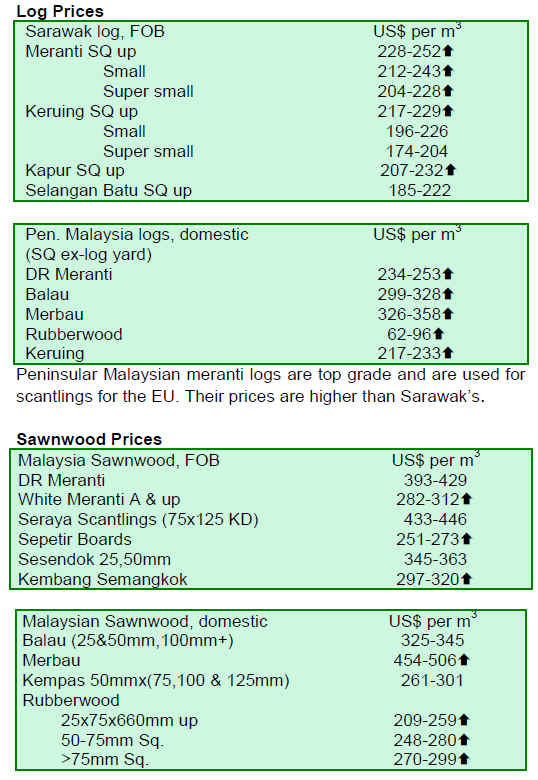

MALAYSIA

Furniture exports set to recover

Exports of Malaysian furniture are expected to reach

RM10 billion for the current year according to the

Malaysian Deputy Plantation Industries and Commodities

Minister.

In 2009 furniture exports declined 12% to RM7.62 billion,

while the decline of timber and rattan furniture, which

constituted 84% of all furniture exports, fell just 7%.

Alternative materials for Malaysian furniture

The Forest Research Institute of Malaysia (FRIM) will

promote several alternative materials as suitable raw

materials for the furniture industry. FRIM will display

these materials during the Malaysian International

Furniture Fair (MIFF) 2010.

The objective in displaying the new raw materials is to

help address raw material shortages facing the furniture

manufacturing sector.

FRIM, the leading forestry research organization in

Malaysia, is also a strategic business partner to the

Malaysian timber industry. It has been in the forefront of

research into fast growing tree species for the timber

industry. FRIM is also an important centre for furniture

testing.

Rubberwood from Thailand

The shortage of raw materials, particularly sawn

rubberwood, in Malaysia has forced a number of

manufacturers to purchase timber from neighbouring

Thailand. However, competition for sawn rubberwood in

Thailand is especially stiff as buyers for the Chinese

market are active and placing huge orders.

Thailand consumes vast amounts of natural rubber for its

production of vehicle tyres and automotive parts. Because

of this strong demand and good prices for latex, rubber

plantations are generating good returns and owners can

keep the plantations standing, even when latex yields

begin to decline. This is leading to a shortage of

rubberwood logs.

Encouraging signs from EU buyers

Sawnwood producers and traders report encouraging news

of orders originating from Europe. While the size of the

orders do not indicate a major revival of the construction

sector in the EU, these are being interpreted as indicating

better demand for raw material for the manufacture of

window and door frames.

Remodelling postponed

The financial crisis in Europe over the past two years

resulted in many homeowners postponing planned

remodelling or renovation work. As fears of another

financial blow in the EU arising from the Greek economic

situation fades, European homeowners are said to be

showing signs of growing confidence and are looking to

undertake repairs caused by storms over the past winter.

With news that prices of non-wood building material are

set to rise, European consumers are reportedly

reconsidering timber for reconstruction work.

Analysts forecast a modest increase in purchases of

plywood and a steady recovery in timber prices over the

next few months.

4.

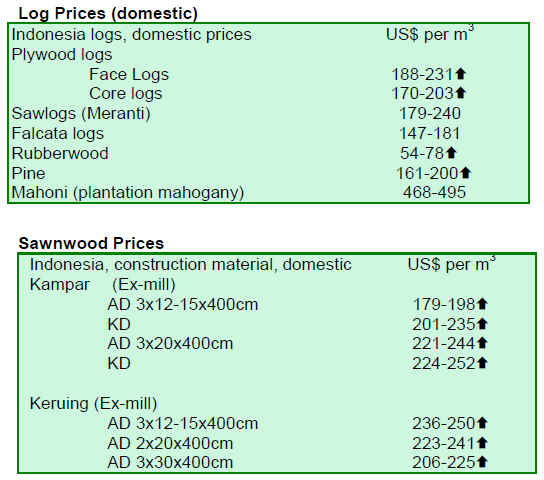

INDONESIA

Reforestation in Jambi

Indonesia, together with Australia, has launched an A$30

million reforestation project in Sumatra in a bid to address

greenhouse gas emissions and introduce a carbon-trading

scheme under the REDD programme.

The project will be in Jambi Province in Sumatra and will

be the second such project undertaken by the two

countries. Funds will be used to restore forests in a

province that is larger than the Netherlands and has lost

more than 60% of its forests through illegal logging, slash

and burn agriculture and clearing for oil palm plantations.

USAID helps interpret Lacy Act in Indonesia

USAID is working with the Forestry Ministry of Indonesia

and various timber product and trade associations to help

Indonesian timber companies better understand the US

Lacey Act. Many Indonesian timber companies are still

unfamiliar with the Lacey Act and welcome the assistance

on how to prepare the various export documents required.

Timber tracking

USAID is also providing support for the development of a

timber tracking system in Indonesia. This is to help

operationalise a new Indonesian verification law that

requires full documentation of the supply-chain for timber

products from the point of harvesting to the processing of

the product.

Positive signs in domestic housing sector

Some Indonesian real estate developers have voiced

optimism that the national economy is showing signs of

recovery and that will mean the housing market is set to

improve.

Interest rates held steady

The Indonesian Central Bank has maintained the

benchmark lending rate at 6.5% for the seventh straight

month in order to promote more bank lending. In another

move to aid the ailing construction sector, the National

Electricity Board is offering developers substantial

discounts for switching their account to industrial status.

With the current buoyant prices for agricultural

commodities, especially palm oil, housing developers

believe that the Indonesian economy is set to grow on a

longer term basis.

Order books in better state

Timber traders and producers have reported that new

orders are steadily arriving and plywood manufacturers

share the same optimism as the housing developers.

Further fuelling optimism is the view that orders for

Indonesian plywood from Japan and South Korea are set

to rise.

5.

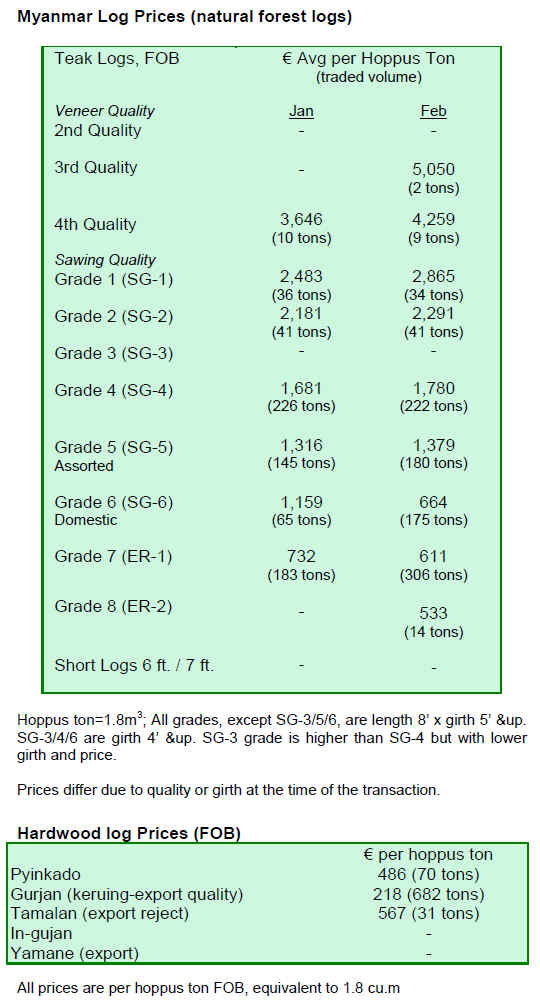

MYANMAR

Sawnwood market slow

Traders are saying that the market for sawn teak is very

slow, enquiries are being received but firm orders are not

being realised.

Price drives Indian purchases

Teak logs, on the other hand, are in demand especially in

India but the catch in this market is ¡®reasonable price¡¯. If

teak log prices are right for the Indian market then buying

is active. This was reflected in last month¡¯s log auctions.

Grade VII logs are the most popular.

Pyinkado log stocks are currently being shipped out to

make room for the newly harvested logs in the log yards.

Buyers of the Pyinkado logs say shipment will be made

when the sales contracts are released by the authorities.

River transport of Gurjan

Gurjan logs from the four preferred areas Momeik,

Mawlaik, Monywa, and Mabein (known as the 4 M area)

have to be floated down the Chindwin and the Ayeyarwadi

rivers. These rivers will become more navigable in a

couple of months when the snow melts in the mountains

and river levels rise.

At the moment there is still a lot of log rafts and barges

waiting to be moved. Most will be sent to the auction

depots after the Myanmar New Year in April. The market

for Gurjan may become more active in April when more

buyers are expected to bid for the fresh logs. Analysts say

that Gurjan prices usually go down after April.

Gurjan logs are also shipped out in comparatively large

quantities from southern Tanintharyi (mainly Myeik

formerly known as Mergui) just before the onset of the

South-West Monsoon during which the sea becomes too

rough.

Design competition

The local journal ¡®Weekly Eleven¡¯ has reported that the

Myanmar Timber Merchants Association has extended the

deadline for the submission of furniture designs for its

competition. Designs may be sent to the Association

personally or by internet or mail. Winners will be

announced a Furniture Fair to be held on the 30th April

2010, at Nay Pyi Taw, the administrative capital of

Myanmar. Designers, both local and foreign, can

participate in the competition, the journal stated. Designs

can be submitted to the Timber Merchants Association at

mfptma@mptmail.net.mm or mfptma@gmail.com

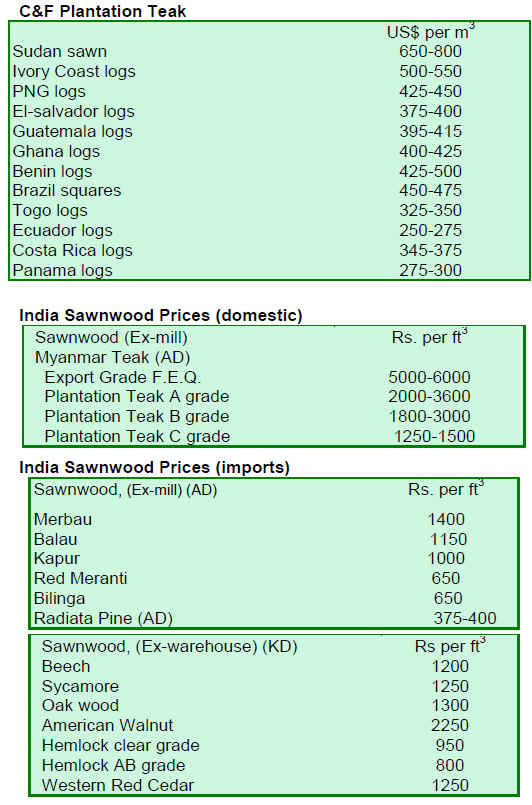

6. INDIA

Exports up three months in a row.

India¡¯s merchandise exports rose to US$14.34 billion in

January, up 11.5 % from US$12.86 billion in the same

month last year. Exporters are increasingly looking for

new products and new markets as growth in traditional

markets such as the USA and Europe is stagnant.

Imports surge

Imports also surged in January, increasing by 35% to US

$24.70 billion against US$18.22 billion a year ago. This is

a signal of strong domestic demand and investment.

India¡¯s Industrial Output Index has also risen thanks to

expanding output and new orders.

Housing market lifting prices

With the improving economic situation in India, it is not

surprising that house building activity has increased.

House prices in India are almost back to levels prior to the

economic slowdown in 2008/9. This is translating into

firming prices for wood and wood products in India and in

countries where India is buying logs.

Custom duties in India¡¯s budget

In the budget presented on 26th February, 2% has been

added to Central Excise. This means that all wood panel

products will attract a 10% counterveiling duty, making

them approximately 2.5% more expensive (inclusive of

surcharges). In the case of logs and sawn timber the duties

remain the same, a disappointment for importers who were

looking for a reduction.

Expanding forest cover.

As announced in the State of The Forests 2009 report, the

net forest cover in India has expanded.

The states reporting increased forest cover are: Himachal

Pradesh, Arunachal Pradesh, Jammu and Kashmir, Sikkim

Mizoram, Manipur Nagaland, Tripura Jharkhand, Orissa

and Uttara khand. On the other hand, Assam, Andhra

Pradesh and Chhattisgarh have reported declines in their

forest area.

The losses of cover can be due to mining sector

operations. The good thing is that there is a growing

awareness of the importance of increasing the ¡®green¡¯

cover.

Investment in downstream production

There is great potential for expanded panel product

manufacturing in India but the main problem is the

scarcity of wood raw materials.

Under these circumstances, making composite panels

using agricultural waste combined with wood chips is

gaining momentum.

Several production lines have been set up for

manufacturing agro-composite MDF and particleboard.

One such unit has been established in Gujarat by Rushil

D¨¦cor Limited using cotton stalks and wood.

Another factory has been built in Ankleshwar also in

Gujarat, producing particleboard from a bagasse and wood

mix. One more unit by Paralam Global Pvt Ltd is nearing

completion at Nagpur Maharashtra using a similar mix of

raw materials. Shivdhan Boards Pvt.Ltd. of Maharashtra is

producing particleboard using a mix of bagasse, sawmill

waste and small sized logs.

A few more plants are reportedly being planning and/ or

executed to meet the growing demand for these panels as

the base material for further lamination with paper /

veneers/ PVC foils etc, for which there is a large market in

India.

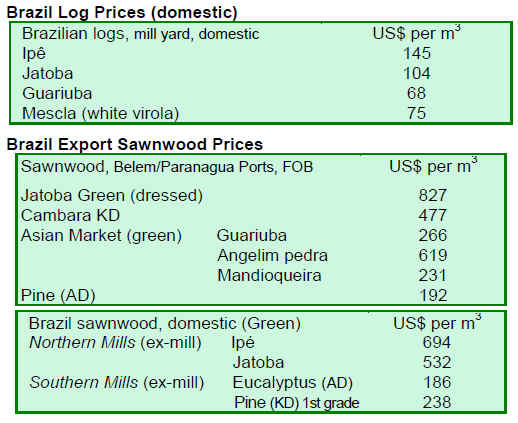

7. BRAZIL

¡®Ghost¡¯ timber companies in Par¨¢

The regional office of the Brazilian Institute of

Environment and Natural Resources (IBAMA) in Par¨¢ has

identified over 150 ¡®ghost¡¯ companies trading timber and

other forest products. This number is quoted in the interim

report of the so-called ¡°ghostbusters¡± operation, which

tracks the forest product flow in the state.

The ¡®ghost¡¯ companies identified by IBAMA are reported

to have provided false management plans and forest

control documents to support the purchase of and trade in

illegal timber. The receipts presented to inspectors were

from non-existent companies. In some cases, the plate

numbers of vehicles reportedly used for the transport of

forest products were those of regular passenger cars and

motorcycles, not timber trucks.

Through the ¡®ghost¡¯ companies, illegal timber could be

disguised as that coming from approved logging areas

with approved management plans. IBAMA is prosecuting

the offenders.

The Promadeira Fair

The seventh Promadeira Fair will take place in August this

year in Sinop, 500 km from Cuiaba. The region is

considered the largest timber manufacturing cluster in the

State.

This cluster of wood product industries apparently

provides some 40.000 direct and 120,000 indirect jobs.

The raw materials for the various industries come from

around 2.6 million hectares of sustainably managed forest.

There are plans to increase this to 6 million hectares.

In addition to the traditional international business

promotion activities of technical visits and product

exhibition, the up coming Fair will feature innovations

such as a display of a mini-forest with a demonstration of

sustainable forest management techniques.

Native tree seedlings will be distributed and there will be a

video presentation on "Standing Forest: the management is

possible," produced by the Timber Industry Association of

Northern Mato Grosso (Sindusmad) in partnership with

the Center for Wood Producers and Exporters of Mato

Grosso (CIPEM). This focuses on sustainable forest

management practices.

Falling exports from Northern Mato Grosso

Exports from the Alta Floresta tropical timber cluster fell

39% in January 2010 compared with the same period last

year according to the Ministry of Development, Industry

and Foreign Trade (MIDIC). Exports fell from US$

645,000 in January 2009 to US$595,700 in January this

year.

The major product traded was tropical timber

(US$568,400) but sales were down 38% compared to

January 2009.

The main importers were Spain, (accounting for US$

223,700, or 37.5% of the total export), followed by

Canada (US$155,100), the United States (US$ 142,200),

Belgium (US$ 47,300) and India which imported just

US$27,300 worth of wood products from the region.

Par¨¢¡¯s exports recover

The economy of Par¨¢ started to recover in January this

year after eleven months. Now the economy of Par¨¢ is

ranked second amongst the Brazilian States generating a

trade surplus of US$ 550 million.

Exports from Par¨¢¡¯s increased 13% in January 2010

compared to January 2009 from US$578 million to

US$657 million. In contrast to the situation in 2009 when

export declined sharply, there was a turnaround earlier this

year.

Wood product exports increased 19%, which analysts say

is significant given the deep recession in the sector last

year.

While wood product exports from Par¨¢ were just US$ 24

million in January 2009, in January this year they were

almost US$ 29 million.

8.

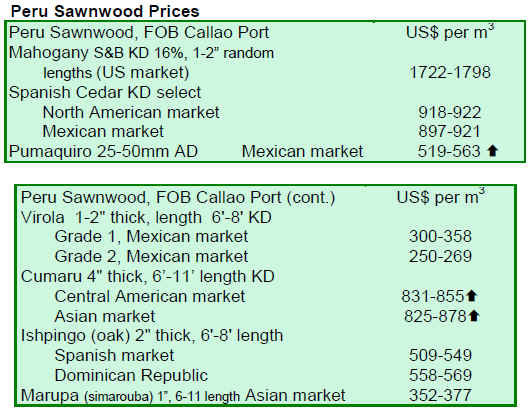

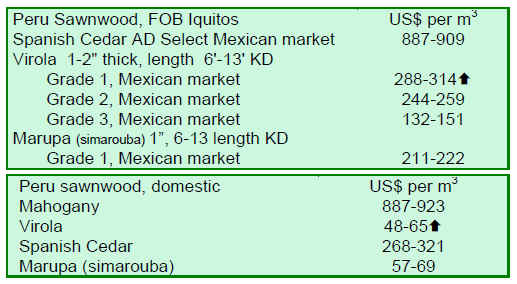

PERU

FTA with EU

Peru¡¯s Minister of Foreign Trade and Tourism, Martin

Perez has reportedly said that while the Peru/EU FTA is

due to be signed in May this year, the agreement would

only become effective in two years time.

This is because there are 27 countries forming the

European Union and the trade agreement must be

approved by legislation in each of these countries.

8.

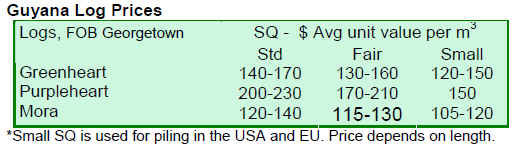

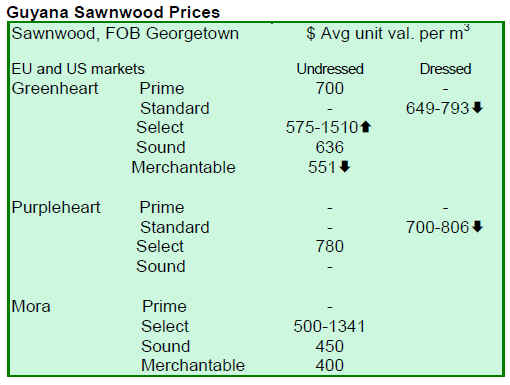

Guyana

Log prices stable, sawnwood prices up

Over the period 16th ¨C 28th Feb, prices for logs were

relatively stable. However Greenheart standard sawmill

quality logs and Purpleheart fair sawmill quality logs

recorded price increases. There were also price

movements for Mora logs.

Sawnwood prices have risen sharply especially for rough

(Undressed) Greenheart select grade. The indications are

that prices have reached an average of US$1,510 per cubic

metre. Prices for rough sawn (Undressed) Mora have also

jumped to as much as US$1,341 per cubic metre, a record

high for the year thus far. Prices for other species such as

rough sawn Red Cedar and Wamara also experienced

favourable price trends over the period reported.

For dressed lumber, both Greenheart and Purpleheart

experienced a decrease in average prices for this fortnight

period.

On the other hand, Baromalli Plywood recorded an

increase in prices for both BB/CC and Utility categories.

The main market for plywood from Guyana is the

Caribbean countries and Suriname which at this point in

time are experiencing a housing boom.

Exports of value added products such as doors, mouldings

and non timber forest products all contributed to export

earnings. The Caribbean remains steadfast as the main

destination for these products from Guyana.

US Forest Service assistance

In January 2010, aid and technical assistance in the

forestry sector was discussed with a team of experts from

the United States Forest Service (USFS).

The USFS team met with representatives of the Guyana

Forestry Commission (GFC) and the Forest Products

Development and Marketing Council (FPDMC)

representatives.

The USFS/ USAID team reportedly proposed a series of

actions in key areas of forestry. In the interest of targeting

sustainable development objectives in the forestry sector,

the proposed actions were derived from broad areas in the

annual work plans of both the GFC and FPDMC.

The topics discussed included Fire Management;

Geographical Information System (GIS); Remote Sensing;

Reduced Emissions from Deforestation and Degradation

Plus (REDD+); and the National Forest Inventory.

Other areas examined for additional technical assistance

comprised testing of lesser used species, capacity building

in the areas of forest product development and marketing

and promotion.

The parties agreed that priority areas for capacity building

should be fire prevention and management, provision of

remote sensing and liaison with other organizations. The

testing of lesser used species for the purpose of making

indoor furniture as well as training in wood technology

and wood anatomy will also be addressed.

|