|

Report

from

Europe, the UK

and

Russia

EU economies under stress

Economic news coverage in Europe in recent weeks has

highlighted the challenges faced by Greece as it struggles

to finance its huge debts. The problems in Greece are

particularly worrying because of the threat posed to the

credibility of the euro-zone’s financial system of which

Greece forms a part.

During February, European leaders signed an agreement

supporting Greece which they had hoped would draw a

line under the issue. But no sooner had the ink dried on the

agreement, more bad news arrived in the form of figures

indicating that GDP in the 16-country currency zone rose

by just 0.1% in the three months to the end of December

compared with the previous quarter.

The only reason for any improvement in GDP at the end of

last year was largely down to France, where an increase in

consumer spending lifted the economy by 0.6%. France’s

large and reasonably self-contained economy has been

relatively less exposed to the global financial and

property-market crises.

France also bucked the downward trend partly because its

government plays a dominant role in the economy. French

public spending rose by 0.7% in the fourth quarter, after

similar increases in the previous two quarters.

Nevertheless, the budget deficit in France was still a hefty

8% of GDP in 2010, placing strict limits on the public

sector’s ability to support the economy in the absence of

stronger private consumption.

Elsewhere in Europe, GDP during the last quarter of 2009

was either flat―as in Germany―or falling, as in the UK,

Italy and Spain. A key problem throughout Europe is that

consumers are not spending enough. In the euro-zone, this

problem is compounded by the strong currency which

makes it difficult for manufacturers to boost sales in other

parts of the world.

Weak export growth is a particular problem in Germany

where manufacturers tend to be more heavily dependent

on export markets but at least Germany has stronger

domestic consumption than most other European

countries. German consumers were thriftier during the

boom years and are now less indebted. Nevertheless, cold

winter weather could have pushed Germany back into

recession during the first quarter of 2010.

Prospects for improved consumption are very weak in

other European countries. Spain was once a rich source of

internal euro-area demand but its consumers are now

weighed down by debts accumulated during a long

housing boom.

Recent data from the UK indicates that January’s cold

weather had an adverse impact on consumption,

particularly in the timber and wood products markets.

Both supply and demand in the housing market came

almost to a standstill, while retail sales of furniture and

DIY materials took a hit as snowed-in consumers put off

shopping for non-essentials.

In the UK there are at least some signs of rising

confidence in future market prospects. Some 29% of

British furniture makers polled by the Confederation of

British Industry in January expected the volume of new

orders to increase over the coming three months, although

6% expect output to fall. 12% of furniture makers are

more confident about the business outlook than they were

three months ago; in October 2009 the figure was -7%.

Confidence among wood and wood product producers,

apart from furniture manufacturers, was sharply higher

than in the autumn, when 32% of firms said they were less

optimistic than in the previous quarter; the corresponding

figure on optimism now stands at +14%.

Speculative purchasing of hardwoods

The generally poor economic forecast has been reflected

in commentary from European hardwood lumber

importers in recent days. While most reckon the worst of

the downturn could be over, they are still forecasting

tough trading conditions until at least the end of this year.

Analysts report that short supplies, lengthening lead times

and rising prices in all the major hardwood producing

regions have encouraged some speculative purchasing of

hardwood lumber by a few of the larger importers.

The bigger importers, with access to finance, have been

building stock levels and now find themselves in a

reasonably strong position, particularly as they can offer

mixed loads for quick delivery to the smaller distributors.

On the other hand, some of the larger traders and

importers are also suffering severely from their relatively

high overheads and are looking for ways to cut these, for

example by reducing staff in their sales networks.

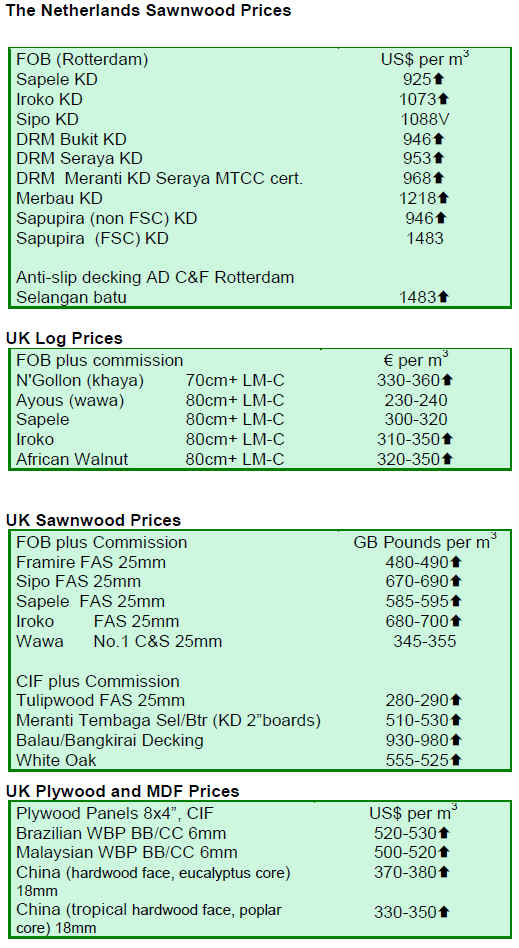

Rising CIF prices for tropical hardwoods

European CIF prices for many tropical hardwoods have

been rising due both to tightening availability and to rising

freight rates. These trends are set to continue. Most mills

are reported as still producing at well below capacity and

lacking raw materials and other resources to quickly

increase supply.

The shipping lines also seem determined to keep pushing

freight rates higher. As a result of this some Asian

shippers are now incorporating freight clauses into their

contracts to avoid the need for new price negotiations.

Some are even considering only quoting on an FOB basis.

Euro CIF prices for sapele, sipo and iroko lumber are now

around 10% higher than at the end of 2009. US$ CIF

Europe prices for the various meranti lumber types and for

bangkirai decking profiles have also experienced around a

10% rise over the same period.

On the other hand, prices for replacing sold out stocks of

African whitewood species like ayous/wawa remain

stable.

Low stock levels in EU

Despite some increased forward buying, hardwood stocks

across Europe remain generally very low. The long lead

times between ordering and despatch has meant that gaps

in stocks have been generally widening.

Lead times for African hardwoods are now up to 6

months, with no guarantee that products will arrive or that

prices will be adhered to. As a result, the intense

competition between importers that dampened prices in

2009 for onward sales of existing landed stock of some

species, notably sapele, is now less aggressive.

Only the low level of manufacturing and consumption in

Europe is preventing lack of supply becoming a more

critical problem.

The fear is that when manufacturing does at last begin to

pick up, the inability of tropical producers to respond

quickly and to deliver more wood to market may

encourage manufacturers to switch to alternative more

readily available products.

Gabon log ban impacts EU plywood market

According to EUWID, the European market for okoume

plywood has been slow during the last two months.

Merchants are reported to be carrying heavy stocks and

enquiry levels are low.

The okoume plywood market, which is focused heavily on

France, with lesser volumes destined for the Netherlands

and southern Europe, has been badly affected by weak

construction activity over the winter months. Nevertheless,

there are expectations that improved spring weather will

improve demand in April and May.

A critical factor affecting both supply and demand of

okoume plywood in recent months has been uncertainty

surrounding Gabon’s log export regulations. According to

EUWID, a surge in buying by European merchants

occurred at the end of 2009 due to expectations that the

log export ban - scheduled originally for 1 January this

year - would lead to supply disruption.

French manufacturers received an upsurge in orders at that

time. Meanwhile, mills in Gabon also reported an increase

in their European customer base. Howeve,r EUWID

reports that the upsurge in demand from European

merchants has tailed away this year.

The announcement that log exports would continue

temporarily was sufficient to reassure merchants that

supplies would not suffer immediate disruption. It remains

to be seen how the European market will react to these

changing circumstances.

Okoume plywood, imported both from Gabon and

manufactured in France from imported logs, has been a

standard reference product on the French market for many

years. It remains popular at the high end of the French and

Dutch markets, valued for its consistent quality and its

adaptability to a wide range of end-uses.

However, it has also been losing market share mainly

because of the introduction of much cheaper alternative

plywood (notably from China) and other panel products.

Because of declining consumption and a big reduction in

European okoume manufacturing capacity in recent years,

the significance of Gabon’s log export ban to the European

market is considerably less now than it would have been

only a few years ago. The volume of okoume plywood

manufactured in Europe is estimated to have declined

from around 300,000 m3 a decade ago to only 95,000 m3

in 2008.

Meanwhile, mills in Gabon have not yet made much

headway to penetrate the European plywood market,

volumes rising from only around 20,000m3 in 2003 to

45,000m3 in 2008 (with much of this volume destined for

Italy rather than France).

To date much more progress has been made by Gabon to

develop European export markets for sawn lumber.

European imports of sawn lumber from Gabon increased

from 20,000m3 in 2003 to 94,000 m3 in 2008.

With the large mainly French-owned plywood

manufacturers in Gabon pushing product onto the

European market, there is every prospect of Gabon

becoming a more significant plywood supplier to the

European market in the future. But there will be

significant hurdles to overcome of which the development

of sufficient processing capacity in Gabon will only be the

first.

Other hurdles include the need to ensure that product

manufactured in Gabon meets tough quality and

environmental standards, that products of consistent

quality and price are available promptly, and that

marketing efforts are stepped up to counter the mounting

threat from alternative materials.

Wageningen report on certification

The Wageningen University and Research Centre

(Wageningen UR) in the Netherlands has just published a

paper assessing the progress made by FSC to certify

natural tropical forest and the impact on forestry practices.

The report says that there are now 10.9 million hectares of

FSC certified forest in tropical regions of which 74% are

managed natural forests. There are 119 FSC certified

FMU, most located in the Americas. About 28% of the

certified area is in Bolivia, 16% in Brazil, and another

22% is distributed over 16 different countries. FSC

certification has expanded more rapidly in privately owned

FMUs than in community or state-owned FMUs.

The report notes that stronger incentives are needed to

increase the total area of certified tropical forest,

particularly for local communities or indigenous groups.

The results indicate strongly that forest management

certification improves the working standards of FMU in

the tropics, with about 98% of problems raised in

Corrective Action Requests by certification bodies solved

within the first five years of certification.

The full report is available at: http://www.illegallogging.

info/uploads/March10Assessingtheprogressforest

mgtintropics.pdf

Draft versions of EU “Due Diligence” Legislation now available

As noted in a previous report (ITTO MIS Volume 15

Number 3), the EU Council reached final agreement on its

amendments to the draft ‘due diligence’ regulation on 29

January. The Council and the European Parliament, which

passed its own amendments to the original proposal last

year, will now attempt to reach agreement on the final

version of the regulation.

he text of the Council resolution is now available at:

http://www.illegallogging.

info/uploads/st05885re04.en10.pdf

Parliament's proposed amendments can be accessed at:

http://www.illegallogging.

info/uploads/EPDDamendmentsA601152009EN1.

pdf

TAlso, a website monitoring progress of the legislation can

be viewed at:

http://www.europarl.europa.eu/oeil/file.jsp?id=5704232&

noticeType=null&language=en

Overview of EU Voluntary Partnership Agreements

with tropical countries

The European environmental group FERN has published a

Forest Watch Special Report offering a brief overview of

VPAs and an update on the status of negotiations with

Ghana, Republic of Congo, Cameroon, Malaysia, Central

African Republic, Liberia, Indonesia, Gabon and Vietnam.

This may be accessed at:

http://www.illegal-logging.info/uploads/VPAupdate.pdf

|