|

Report

from

Europe

First step to ban illegal timber trade

On 4th May 2010, the European Parliament��s Environment Committee adopted a draft recommendation for a second reading to ban trade of illegally logged timber.

The paper included adoption of prohibition on trading illegally harvested timber and timber products, extension of traceability requirements throughout the supply chain and minimum standards for penalties. These key issues were disregarded by the Council during the first Council��s reading last year.

The European Parliament and Council have now started negotiations to formulate a consensus text before the Parliament��s plenary vote scheduled for July.

Just-in-time becoming the norm in the UK

The TTJ��s recent hardwood market report highlights the extent to which the UK has shifted away from speculative purchasing towards just-in-time ordering. The shift has become more obvious during the recession.

Hardwood traders have been acting as ��the customer��s stock-holder�� as manufacturers and merchants have responded to tight credit and uncertainty over future consumption by reducing their own stocks. The TTJ speculates that this effect is long term and today��s just-in-time approach may be the new norm, especially with smaller companies.

The market conditions for sawn hardwood in the UK have improved slightly in the second quarter of the year and there is a cause for cautious optimism. Although the new-build construction market is still very slow, sales for repair, maintenance and improvement (RMI) have been improving.

However, the improvement in demand could be temporary. According to the TTJ, the recent market uptick is probably partly due to a ��catch-up after the appalling winter��. Demand from the public sector may also have been boosted as many government organisations were getting to the end of budget periods and were rushing to spend money allocations.

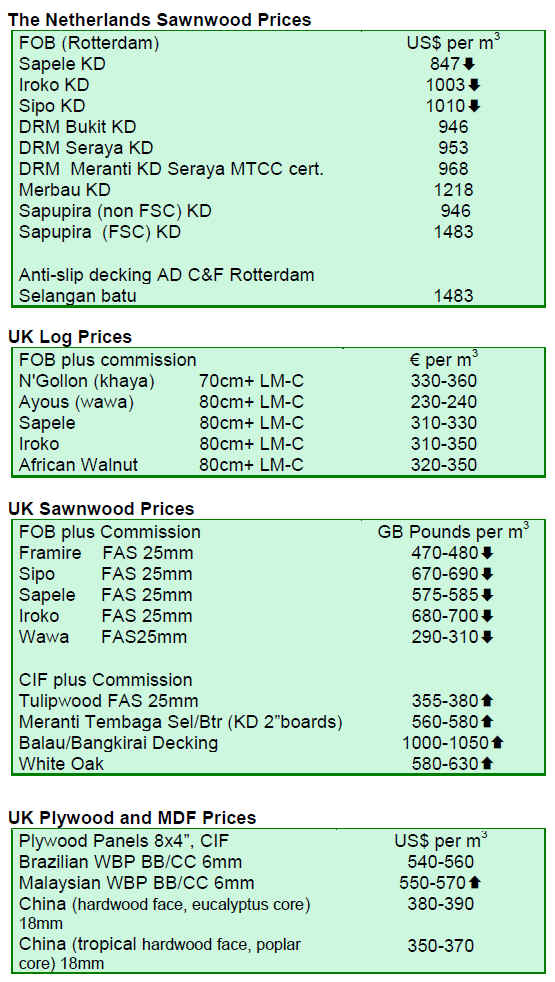

Although sapele remains the dominant tropical hardwood in the UK, short supply, particularly in 63mm, is boosting sales of alternatives such as sipo and boss��. Demand for framire and iroko is steady, while demand for ipe and bangkirai decking has risen with improving spring weather. Meranti, however, is losing out to beech and yellow poplar/tulipwood in paint-grade applications.

Despite slow consumption, concerns are mounting about the supply side of the equation. Lead times for tropical hardwood species are now very lengthy, extending into the last quarter of this year for African species. Even for American hardwood species, which buyers have been accustomed to receive within a couple of weeks, lead times may extend to 2 months. American shippers are tending to offer available supplies to their most reliable long-term customers first.

UK CIF prices quoted in GBP for most hardwood species have risen significantly over recent weeks. The TTJ suggests that while some UK distributors are still selling stock at well below the replacement cost, the price rises from the supply side are beginning to move up the distribution chain as grounded stocks run increasingly thin.

Despite the long lead times, the weakness of the GBP against other international currencies in recent weeks has been a further disincentive to UK buyers to enter the forward market. By mid May, the economic problems in Greece and uncertainties over the outcome of the UK election were contributing to particularly high levels of uncertainty in foreign exchange markets.

At present, the GBP is strengthening slowly against the euro, but both the euro and the GBP are weakening rapidly against the US dollar. For the UK buyer, this means that CIF prices for tropical hardwood products from the Far East (quoted in dollars) have increased dramatically, while prices for African hardwoods (quoted in euros) have eased slightly.

Newly elected UK government commits to Lacey-style legislation

The agreement reached between the Conservative and Liberal parties to form a coalition government following the UK Prime Ministerial election on 6th May includes a commitment to impose ��Measures to make the import or possession of illegal timber a criminal offence��.

The implication is that the UK is now committed to the introduction of legislation similar to the US Lacey Act which will provide an added incentive to UK wood product importers to avoid any wood at risk of being derived from an illegal source. This law is now very likely to be introduced in the UK irrespective of the outcome of current EU deliberations on proposed legislation that would place mandatory requirements on all European wood importers to introduce ��due diligence�� systems.

The commitment to Lacey-style legislation by the newly elected coalition government comes alongside a wide range of other environmental commitments. Particularly there are attempts to a low carbon economy, which suggest there will be market interest in green building and sustainable materials.

EC forecasts only a very gradual recovery

Based on a comprehensive review of economic conditions across the EU, the European Commission issued its Spring 2010 forecast on 5th May. The report concludes that recovery is underway in the EU, albeit a gradual one.

Continent-wide GDP started to grow again in the third quarter of 2009, up by 0.3% compared to the same period in 2008 ending the longest and deepest recession in the EU's history.

Looking ahead, the report suggests that EU is likely to benefit from a stronger-than-expected turnaround in the global economy, particularly in Asia, which has improved financial-market conditions and should assist Europe��s export growth. The recovery has been firm, especially in the manufacturing sector.

On the other hand, several issues are expected to restrain domestic demand for years to come. These include: the downsizing of the construction sector which is still ongoing in a number of Member States; weak private consumption growth as disposable income is held back by weak wage and employment growth; heightened risk aversion that will weigh on private investment; higher financing costs for firms and households; and government deficits which have tripled in total across the EU in recent years and which will greatly restrict potential for further public spending.

Optimism following successful Milan furniture show

The Milan Saloni 2010 furniture show during the 6 day period from 14th April proved to be a huge success, both in terms of numbers of visitors and exhibitors. The signs are that European furniture designers and manufacturers remain confident about their long-term future despite the economic downturn.

While the show itself seems to have risen above the challenges of the economic downturn, it was clear from the displays that designers and manufacturers are being forced to adapt to the changed economic landscape. This year companies introduced far fewer new products than usual and made them less technically ambitious. The show reflected a new situation in which furniture buyers are much more careful and want products whose value matches the pricetag. Also increasing concern for sustainable consumption was reinforced from the last year.

The emphasis on sustainability and simplicity was essentially good news for wood. The vast majority of the wood on display at the show was in temperate hardwood. A leading advocate for wood at this and previous Milan shows was the Italian manufacturer Riva.

Tropical wood under pressure in the outdoor furniture segment

Design trends apparent in Milan were generally working less well for tropical wood. The fashion towards combining furniture for indoor and outdoor use �C first identified at last year��s show �C has intensified. Unfortunately this seems to be associated with a significant shift to materials considered lighter-weight than tropical wood.

In fact all of the buzz in the outdoor furniture sector in Milan was around non-wood products, claimed to be environmentally friendly because they have been made locally and therefore reducing the need for exotic imports.

At least the show revealed new possibilities for the marketing of tropical hardwoods to the European furniture sector. The show indicated growing interest in design references from outside Europe, including from South East Asia and Africa. Furthermore many furniture designers are very keen to exploit the narrative associated with the materials they use, particularly where there is a strong sustainability message. With appropriate packaging and communication, the extraordinary back-story associated with the sustainable management of tropical hardwoods could be a major selling point amongst European designers in the future.

Related News:

��

|