|

1.

CENTRAL/ WEST AFRICA

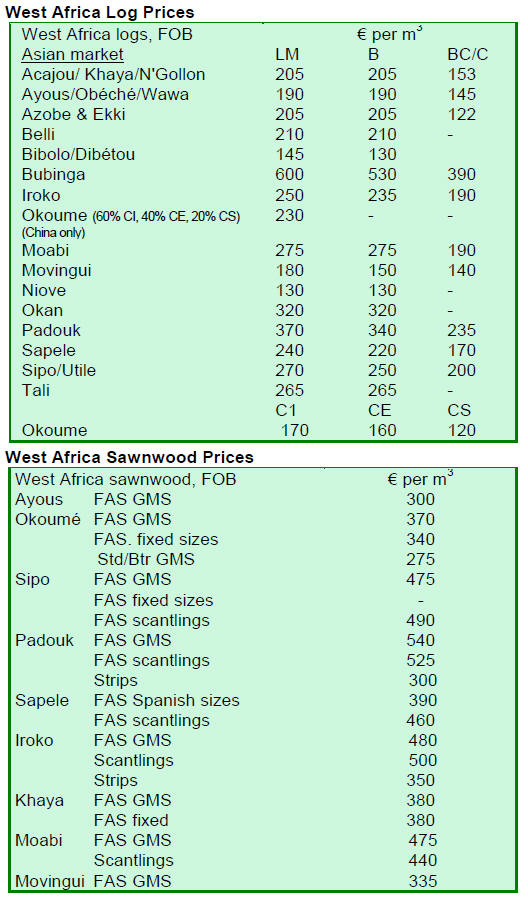

Iroko remains in good demand

The market situation remains unchanged and there are no

reasons to expect any major fluctuations in the near future,

says an analyst. During the past few months price changes

have mostly been driven by increasing demand for

individual species and this fortnight was no exception.

Iroko logs are still in good demand and prices climbed by

another Euro 10 per cu.m from the mid-September level.

However, Iroko sawnwood prices have not yet fully

caught up with the rise in log prices. Over the past two

weeks sawnwood prices moved up by Euro 10 per cu.m

while prices for strips were unchanged at Euro 350 per

cu.m.

Sawmills in the West and Central African region still have

fair numbers of existing contracts to complete for the final

quarter. According to analysts, there is a chance of some

new business opportunities, however, sawmillers are

cautious about the first months of next year and this is

reflected in their lack of willingness to invest to increase

production.

Gabon plans Free Trade Zone

As the log export ban in Gabon is maintained, contractors

have now begun preparations for a Free Trade Zone which

is planned to encourage investment in various industries

including timber processing. There are reports that the log

ban is beginning to impact government revenues and the

business outlook for the many ancillary traders and

suppliers to the logging sector.

Export markets

In Cameroon, Congo Brazzaville and Equatorial Guinea,

log exports are reportedly sufficient to meet the current

market demand, China and India being the main export

destinations. China¡¯s demand for sawnwood is expected to

continue to grow.

The market situation for hardwood sawnwood in the UK

and Continental Europe is dull, but steady. Only iroko and

ayous sawnwood are in demand. Prices for all other

species have remained unchanged through the past two

weeks or more.

As the European winter begins, there is a great deal of

uncertainty over prospects for the building and

construction industries. UK businesses are waiting for the

government¡¯s autumn spending review due to be published

in October. The review is expected to bring cuts in

government expenditure that will affect the construction

industry and is forecast also to restrain the housing market.

2. GHANA

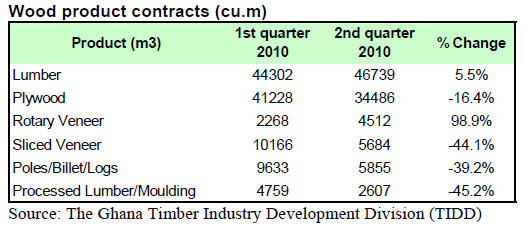

Second quarter wood product contracts fell 10%

Permits for a total contract volume of 105,926 cu.m of

wood products were approved and processed by the TIDD

in Ghana during the second quarter of 2010, down 10.2%

compared to the first quarter of 2010. As in the first

quarter of 2010, there were no recorded applications for

furniture parts exports in the period under review.

Analysts say this was because of the fact that the main

furniture export company, Scanstyle Mim Limited, has

been concentrating on the domestic market.

Export levels of all major wood products decreased in

volume during the second quarter, except sawnwood and

rotary veneer which picked up by 5.5% and 99%

respectively in comparison to the previous quarter.

Exports of Plywood, poles/billets/logs, sliced veneer and

processed lumber/mouldings fell by 16%, 39%, 44% and

45% respectively compared to the first quarter of 2010.

Sawnwood continued to be the leading export product

accounting for 44% of the total export volume in the

second quarter of 2010.

The regional offices in Kumasi, Accra and Sunyani

accounted for 40%, 1.6% and 12% respectively of the total

export permits issued during the second quarter.

Sales to the Middle East, China and North African countries improve

The falling Euro exchange rate against the US dollar

during the second quarter of 2010 boosted timber exports

from Ghana to the Middle East, China and North African

countries. Ghana¡¯s timber exports are priced in Euro while

contracts made with the aforementioned countries are

quoted in US dollars.

The medium to heavy density species including dahoma,

danta, edinam and denya have been difficult to sell in

European markets, however, markets in the Middle East,

China and North African countries have shown increased

interest in these species.

Due to the booming plywood market in the West African

region, more and more processing mills in Ghana focused

on production of plywood instead of sliced and rotary

veneer for export. As a result, production of veneer for

export has been low since 2009, however, the second

quarter contracts showed improved sales for rotary veneer.

Generally, the contract prices met the Guiding Selling

Prices (GSP) set by the TIDD. The average market prices

for BB/CC quality plywood in the West African region

were 5% to 10% higher than the GSP in the second quarter

of 2010. Prices of mahogany sawnwood for the US market

improved significantly from a price average of US$798

per cu.m in the first quarter to US$830 per cu.m in the

second quarter of 2010.

3.

MALAYSIA

Concerns over expansion of the Red List

A recently published study by the International Union for

Conservation of Nature (IUCN) reports that over one-fifth

of the world's plants are under threat of extinction. The

IUCN study suggests that three species; keruing, meranti

and kapur from three different genera Dipterocarpus,

Shorea and Dryobalanops may also be threatened. The

species are not on the IUCN Red List yet as they need to

undergo a lengthy verification process. For more

information: http://www.iucnredlist.org/news/srli-plantspress-

release

The Sarawak Timber Association (STA) stated that

inclusion of these three major commercial tree species into

the IUCN Red List of Threatened Species would severely

impact Sarawak¡¯s timber trade. These three species

account for up to 62% of total log and 24% of sawnwood

exports from Sarawak respectively. In the period from

January to August this year, Sarawak exported 2.71

million cu.m of logs worth RM1.32 billion, compared to

3.78 million cu.m and RM1.79 billion for the entire 2009.

Web based marketing tools for furniture markets

Prices of Malaysian wood and timber products continue to

climb as the US dollar depreciates against the Malaysian

Ringgit. The situation has been beneficial for Malaysian

importers of veneers and other raw materials for the

domestic furniture industry, but at the same time,

Malaysian furniture exporters are facing difficulties in the

international market.

As a result of the appreciating Ringgit coupled with ocean

freight rate increases, exporters of Malaysian furniture are

facing stiff competition, not only from Chinese furniture

manufacturers but also from US based furniture

manufacturers. Some furniture manufacturers in Malaysia

say that their advantage of low-cost manufacturing has

been lost due to the lowest Ringgit to US dollar exchange

rate in 13 years.

In addition, the Malaysian Ringgit has also strengthened

against the Euro having the effect of making Malaysian

furniture exports more expensive in the US market

compared to the exports from Europe.

American department stores such as Macy¡¯s, Sears and

Wal-Mart are collaborating with some US based

manufacturers to market both home and office furniture

through the internet lowering the marketing and retailing

costs. This is an advantage that most Malaysian furniture

manufacturers have been unable to tap.

However, Malaysian owned ¡°Laura Ashley¡± is the

exception. The furniture manufacturer operates in 225

stores in the UK and in 233 franchises worldwide.

Improvements made in web marketing boosted company¡¯s

sales through the internet by 63%. Currently, e-market

sales comprise 12% of the company¡¯s total sales of

furniture and home furnishing.

4.

INDONESIA

Indonesia tightens controls to identify

illegally harvested timber

At the beginning of the September, the Indonesian

government strengthened measures to ensure only timber

and timber products with proper documentation proving

legality are exported. Any timber or timber products not

supported by appropriate documentation are immediately

considered as illegally harvested.

Indonesia will apply a system called the Timber Legality

Verification System (SVLK) to track and monitor

industrial forest concessions (HTI), production forest

concessions (HPH) and community plantation forests

(HTR).

The system is said to satisfy European Union legislation

designed to remove illegal wood from European trade.

According to the EU requirements, timber tracking and

due diligence systems are due to be fully effective by 2013.

The Indonesian government commented that they are

committed to the Voluntary Partnership Agreement (VPA)

to be signed with the EU. A technical meeting, planned to

take place by the end of 2010, is to address outstanding

issues before the final agreement is signed. The annexes to

the VPA are expected to be completed by the end of

October 2010.

The VPA requires a specific agency to oversee approval of

licences to export any timber and timber products.

Presently, five institutions including PT Sucofindo, PT

Mutuagung Lestari, PT Mutu Hijau Indonesia, PT TUV

International Indonesia and the Forest Industry

Revitalization Board (BRIK) have been appointed to

verify the legality of timber products for export.

Japan seeks alternatives to overcome rising raw material costs

The Japanese government is considering further

collaboration with the Indonesian Institute of Science

(LIPI) in the area of timber processing. The collaboration

is meant to address the issue of rising raw material prices.

Indonesia is the largest exporter of plywood to the

Japanese market. Japan also imports hardwood roundwood

from other countries which is processed by its downstream

processing industry. Japan has vast domestic forest

resources which it is planning to exploit by legislating for

domestic wood use in the country.

Appreciation of Rupiah eases

Prices of Indonesian timber products remained steady and

largely unchanged as the Indonesian Rupiah depreciated

against the US dollar. Indonesian timber product exporters

earlier expressed their concerns over the continuous

apperception of the Indonesian currency against the US

dollar.

5.

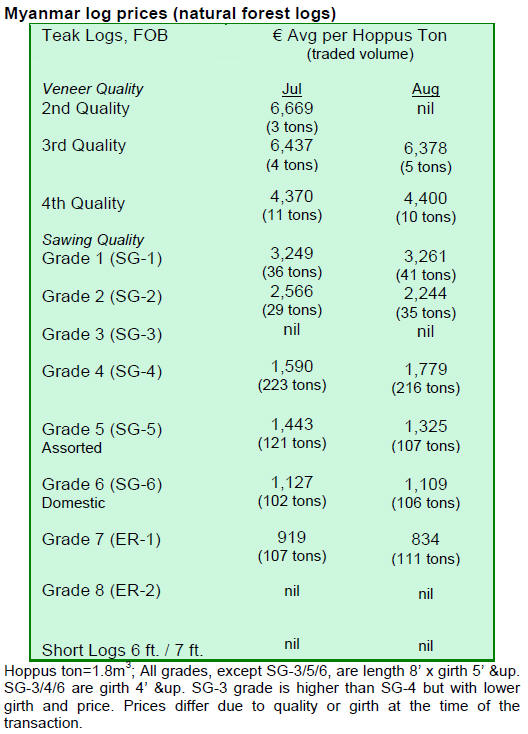

MYANMAR

Domestic

consumption and exports to ASEAN grow

After the economic crisis in 2008/09, timber exports from

Myanmar shifted to some other ASEAN countries and the

Middle East, as the EU countries reduced imports by about

80% compared to the pre-crisis level. U Nay Tun Min,

secretary general of the Timber Merchant Association

(TMA), said this was mainly because buyers from the EU

found their buying power curtailed, while demand from

ASEAN countries like Thailand, Singapore, Vietnam and

Malaysia was strong. However, according to analysts, the

Indian market remains the major export destination for

Myanmar timber with about 70% to 80% share of the total

exports.

Domestic timber demand for construction and furniture

manufacturing has been increasing during the past few

years. Analysts say that the domestic timber processing

industry, however, is suffering from raw material

shortages and thus log exports need to be cut by 50%.

Domestic demand for timber increased sharply after

Cyclone Nargis hit Myanmar in 2008, and the domestic

timber industry provided low cost materials for the

housing sector and to build fishing boats.

Asian Free Trade Agreements facilitating exports

The ASEAN market is becoming more and more

important for Myanmar timber exports after the

establishment of the ASEAN Free Trade Area (AFTA).

Brunei, Indonesia, Malaysia, Philippines, Singapore and

Thailand reduced import tariffs on all products to 0-5% in

January 2010 to comply with the AFTA agreement.

Countries including Cambodia, Laos, Myanmar and

Vietnam are due, by 2015 to reduce the tariff levels to 0-

5%. At present, all wood and timber product exports from

Myanmar enjoy zero export duties.

In addition, the Generalized System of Preferences (GSP),

a programme effective in Japan and Republic of Korea,

provides zero tariff treatment for some imports from

developing countries including value-added timber

products from Myanmar.

The recent agreement with China, the China-ASEAN Free

Trade Area effective from January 2010, has also proven

to be effective in improving Myanmar timber exports to

China.

6. INDIA

GDP growth sustained

In the second quarter of 2010, India¡¯s GDP continued to

grow, posting the highest growth rate in 30 months.

Between April ¨C June 2010 GDP surged 8.8% compared

to the same period in 2009. Growth in rural India was

2.8% in the second quarter of 2010 against 1.9% last year.

Buoyant economic activity generated more jobs in the

country during the second quarter of 2010 and GDP is

expected to continue growth towards the target level of

10%.

Exports in August were US$16.6 billion, up 23%

compared to August 2009. At this pace of growth, India is

going to meet the export target of US$200 billion set for

2010. August imports in India grew 32% to US$29.7

billion compared to last year.

Growing interest in planting of non-timber species

The monsoon season has been favourable for the tree

planting in India and as a result, over 1 billion trees have

been planted by NGOs so far. Planted species include

bamboo providing raw material for pulp and paper

industry and also for handicraft manufacturing enhancing

the livelihood of the rural population in forest areas. Other

planted tree species for non-timber production include

mangifera, tamarind, Melia azhadirachta, Melia dubia,

Eugenia and Mimusops diospyros.

The trend of planting non-timber species is well supported

with public participation, for example in Ahmedabad

municipality 919,770 trees were planted around the city

area in one day.

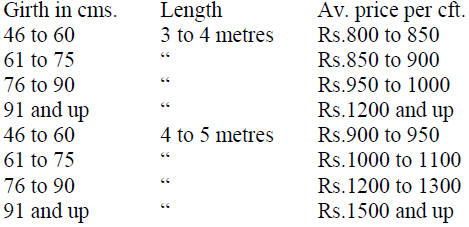

Auction sales in Government Forest depots

At recent log auction sales in Central Indian Government

Forest depots, approximately 19,000 cu.m of teak, 8,600

cu.m of salwood and 7,800 cu.m of mixed hardwood logs

were sold. Demand for domestic teak is improving as

Myanmar teak log imports fall short of demand. However,

due to the monsoon and a quiet period in housing activity,

prices were somewhat lower at Rs.700 for salwood and

Rs.550-600 for mixed hardwoods. The average teak log

prices were as follows:

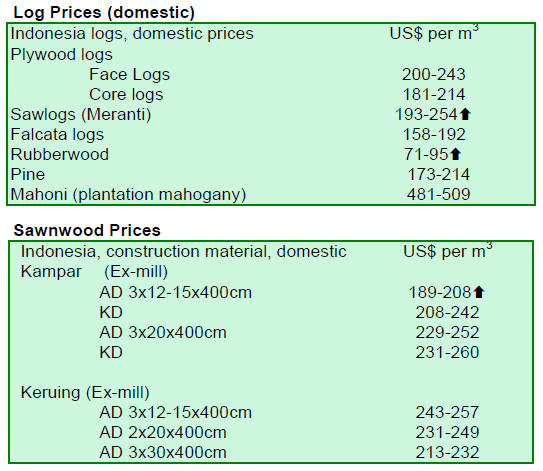

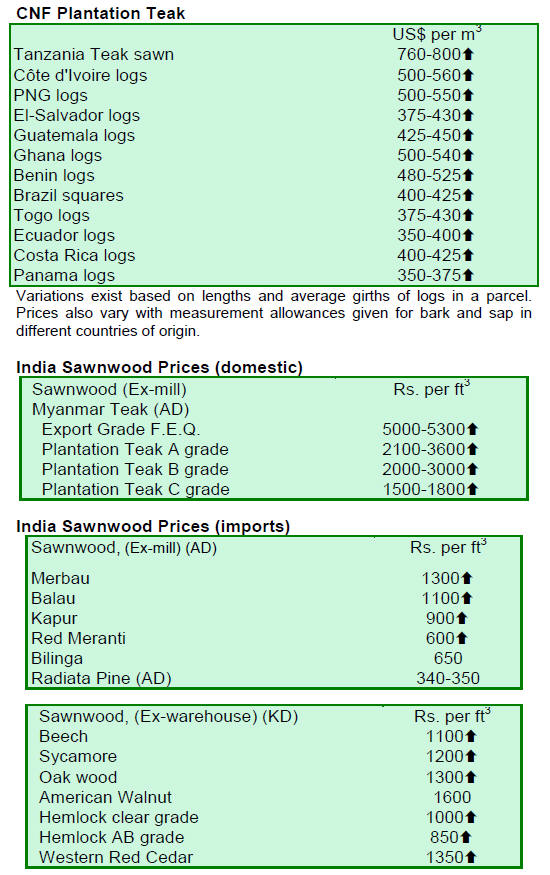

Imported timber and plywood market

CNF timber prices have been increasing due to the

significant rise in ocean freight costs. Especially container

freight rates have surged while break bulk rates are more

flat.

Prices for domestically manufactured marine plywood

have recently been revised due to the higher costs of

labour, chemicals, phenolic resins and timber this is

driving wholesalers to source their plywood from

overseas.

Prices of other grades of locally manufactured plywood

have remained steady, however, analysts expect some

price revisions to come soon.

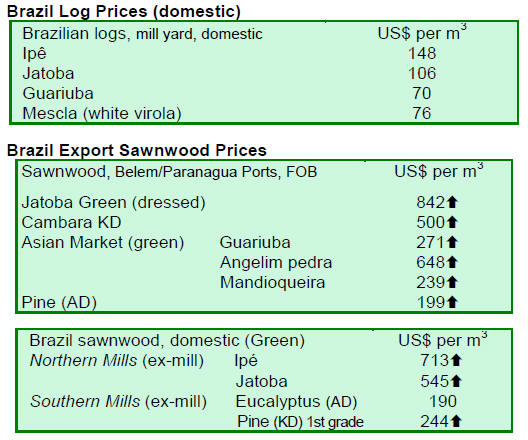

7. BRAZIL

August timber exports

In August 2010, exports of timber products (except pulp

and paper) increased by 22% from US$179 million in

August 2009 to US$217 million.

However, exports of tropical sawnwood decreased in

terms of both volume and value, from 48,400 cu.m in

August 2009 to 42,300 cu.m in August 2010 and from

US$21.3 million to US$19.9 million, representing 12.6%

decline in volume and 6.6% in value.

The recent declines in exports of tropical plywood appear

to have bottomed out as exports increased from 8,800

cu.m in August 2009 to 9,800 cu.m in August 2010, up

11.4%. In value terms, the increase was 10.2%, from

US$4.9 million to US$5.4 million.

Pine sawnwood exports surged 83% in August 2010

compared to the August 2009, from US$7.8 million to

US$14.3 million. In terms of volume, exports rose 47.8%

from 41,800 cu.m to 61,800 cu.m over the period.

The value of pine plywood exports jumped 80% in August

2010 compared to the level in August 2009, from US$18

million to US$32 million. Export volumes grew by 31.4%

during the period, from 66,800 cu.m to 87,800 cu.m.

For wooden furniture, the value of exports rose slightly by

1.3% compared to the level in August 2009 to US$48.1

million in August 2010.

Slight increase in timber prices

The average price of timber products in Brazil increased

slightly from the last fortnight period. The prices in the US

dollars increased 0.46% due to a slight appreciation of

Brazilian currency against the US dollar.

Inflation eases

According to the Brazilian Institute of Geography and

Statistics (IBGE), the Consumer Price Index (IPCA) of

August 2010 showed only a slight increase (0.01%) from

July and a 0.04% increase compared to the same month

last year. The IPCA is the official index used by the

Central Bank to monitor inflation and keep it within the

targeted rate of 4.5% with a tolerance of two percentage

points for 2010. The accumulated IPCA for the first eight

months of the year was 3.2%.

The Copom (Economic Policy Committee) kept the prime

interest rate (Selic) at 10.75% per year in August. The

prime interest rate has been lifted three times this year.

In August 2010, the Brazilian currency slightly

appreciated against the US dollar compared to previous

month, the average exchange rate now being at

BRL1.76/US$.

Forest management more profitable than cattle grazing and agriculture

A Study conducted by the Federal Rural University of

Amazonia (UFRA) for the Par¨¢ State Forest Development

Institute (IDEFLOR) shows that forest management is

more profitable than cattle grazing and agriculture in the

Amazon if cattle farmers and agriculturalists comply fully

with the existing environmental and labour laws.

According to the UFRA, each hectare of Amazon

rainforest can generate BRL22.00 from forest management

per year, compared to BRL6.00 from cattle grazing and

BRL14.00 from agriculture. The comparison considered

the costs of complying with environmental and labour

laws. However, without complying with the legislation,

cattle grazing would be more profitable than forest

management.

The study was carried out to offer guidance for forest

concessionaires in Par¨¢ state forests. The local roundwood

timber market was used as a reference to calculate the

value of standing stock to be managed. The average price

of standing timber was estimated at BRL27.20 per cu.m.

Major challenges of timber industry in Par¨¢

The Par¨¢ Timber Exporters Association (AIMEX) recently

made an assessment of the timber sector in Par¨¢ over the

last four years. The assessment was done in advance of the

next governor¡¯s election taking place in October 2010.

AIMEX presented the following main problems faced by

the sector to Par¨¢ state governor candidates:

- Inefficient administration and excessive bureaucracy

of the State Secretary of the Environment (SEMA);

- Lack of efficient licensing of timber-related activities;

- Lack of standardisation of inspection procedures by

IBAMA (Brazilian Institute for Environment and

Renewable Natural Resources);

- Slow adoption of state forest concessions system.

AIMEX acknowledges that the current government had

successes and has shortcomings. The forestry sector¡¯s

main challenge in the coming years is to recover from the

international financial crisis. AIMEX suggested the

following measures to be implemented:

- Establishment of the Forest Management Support

Programme (PAMFLOR) to bring efficiency and

transparency to the forest licensing system;

- Implementation of the Forest Harvest Plan;

- Meeting the goal of 6.5 million cu.m of timber

production in 2010;

- Establishment of standards for industrial inspection

together with IBAMA;

- Building a policy for the forest industry sector with a

specific tax regime to increase timber industry¡¯s

competitiveness;

- Enabling adequate credit lines for the sector;

- Attaching the forestry sector to the major strategy for

economic development.

Brazilian furniture sector imports certified wood from US

Some Brazilian furniture companies have been replacing

tropical veneers and timber with imported certified wood

from the US. Imported species including walnut, ash, oak,

maple, tulip tree have been used by some Brazilian

furniture manufacturers especially when the final product

is exported to the international markets where the use of

certified timber is necessary.

Ready access to certified timber is one of the reasons

Brazilian furniture makers are beginning to import wood

from the US. In addition, the US timber and veneer supply

is constant around the year while in Brazil; the rain season

interrupts or reduces timber supply for furniture

manufacturers.

8.

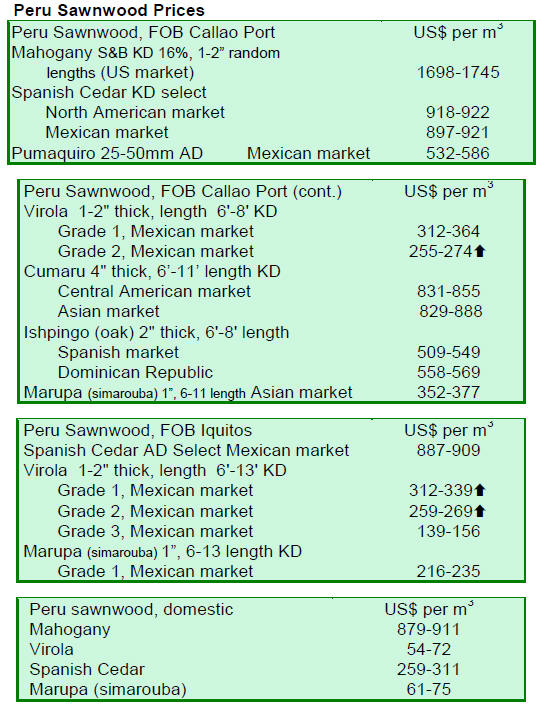

PERU

Sustainable harvest plan for cedar in Peruvian Amazon

In the Peruvian Amazon there are approximately 300,000

cedar trees (Cedrela odorata), which could be exploited

commercially, according to an assessment prepared by the

National Agriculture University of La Molina for the

Ministry of Agriculture and the Environment. According

to the assessment, about 3,000 cedar tree could be

harvested sustainably per year in the Peruvian Amazon.

The assessment complements an earlier study "Evaluation

of commercial stocks and strategy for the sustainable

management of mahogany" by introducing fixed harvest

quota also for cedar. The study also proposes establishing

wood traceability systems, in order to monitor species that

are being harvested and processed for further marketing.

New forestry law to be approved later this year

Wilfredo Panduro, head of the Regional Forest Resource

Management Wildlife Regional Government of Loreto

(formerly INRENA), stated that the draft Forestry Law

was passed back to the Committee preparing the proposal

after comments made in the Congress. Recently, the

committee has been working on collecting more

information and details from the regions to be added to the

next draft.

Environment Minister Antonio Brack said that the new

Forestry and Wildlife law is due to be approved by

Congress in December this year. U.S. representatives have

acknowledged that the Forestry bill in Peru is progressing

well in compliance with the Free Trade Agreement (FTA)

being prepared between the countries. The FTA is almost

completed and the new Forestry and Wildlife law is

needed to finalise the conditions of the agreement. The

rights of indigenous people are still the issue clouding the

bill and its approval in the Congress.

Forest concessions under investigation

Out of the 240 forest concessions in Peru (including

timber, reforestation and ecotourism), between 80 and 100

are under an investigation due to suspected violation of

some regulations, said Omar Guerrero, the deputy director

of Supervision Office of Wood Forest Concessions

(OSINFOR). The infractions that have been found so far

range from bad timber stocking to missing licences or

contracts.

Free Trade Agreement between Peru and Republic of Korea

Peru and Republic of Korea have concluded a Free Trade

Agreement (FTA) which is expected to come into effect in

January 2011.

The total trade between these two countries has been

growing over the past few years totalling US$1.6 billion in

2009. The agreed FTA is said to be a comprehensive pact

involving goods, services and investment opportunities

that will be mutually beneficial.

As a result of the FTA, wood and timber product exports

from Peru to Republic of Korea are anticipated to grow

30%, according to Eric Fischer, chairman of the wood

committee of Peru's Exporters Association.

¡°Korea is a highly industrialised country in this field and

its forest sector provides a wide variety of wood products

that are used for various applications in the construction

sector¡±, Fischer added.

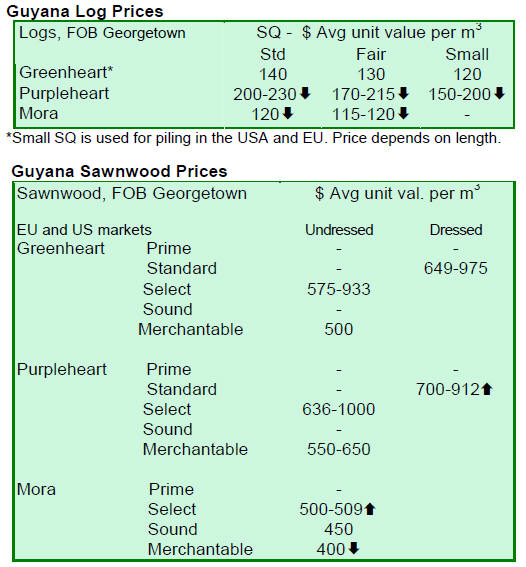

9. GUYANA

Log prices down ¨C sawnwood up

For the period under review, greenheart log prices

remained unchanged while purpleheart and mora log

prices were down.

For sawnwood, undressed greenheart (select) prices

jumped from US$785 per cu.m to US$933 per cu.m over

the period under review. However, the exported volumes

were small.

Similarly, undressed purpleheart (select) gained from

US$750 per cu.m to US$1000 per cu.m while mora

sawnwood prices were steady. Dressed greenheart and

purpleheart both reached higher price averages at US$975

per cu.m and US$912 per cu.m respectively.

During the period under review, baromalli plywood prices

were steady for BB/CC and down for utility category.

Guyana¡¯s washiba (ipe) continues to be in demand

attracting a price average of US$1,600 per cu.m for this

fortnight period.

Roundwood and splitwood contributed to the total export

earnings with favourable average prices the major

destination being the Caribbean market.

For the period under review, exports of value-added

products gained. The major product categories were doors

and windows made from amarante/purpleheart. Also,

NTFP¡¯s and mouldings contributed to the total export

earnings.

Guyana log export policy

Guyana Log Export Policy having a specific focus on

enhancing domestic value-added forest product production

and utilisation of lesser known species came into effect in

January 2009. The policy introduces higher export

commission rates on key log species used for value-added

production in Guyana. Before the imposition of higher

export commission rates, the rate was 2% on all logs. The

current regulation recognises three groups with different

treatments applied since January 2009.

The first group of species were imposed with a 7% export

commission rate effective from January 2009, 10% from

January 2010, and subjected to 12% from January 2011 up

to December 2011. This group includes the following log

species: purpleheart, red cedar, letterwood, bulletwood,

cow wood, tatabu, kabukalli, shibadan, tauroniro, washiba,

hububalli, tonka bean, darina, greenheart, and brown

silverballi.

The second group of species were imposed with a 7%

export commission rate from January 2009 and 10% from

January 2010 up to December 2011. The group includes:

itikiboroballi, determa, wamara, hakia, mora, dukali, keriti

silverballi, wallaba, fukadi, and futui.

The third group exposed to the higher export commission

rates include squares 20.3 cm X 20.3 cm and greater (or 8¡±

X 8¡± and greater). This applies to the following species:

purpleheart, red cedar, letterwood, kabukalli, shibadan,

washiba, hububalli and tonka bean.

According to interim reports, the implementation of

Guyana log export policy has proved to be so far

successful. The main value-added timber species showed

a 40% decrease in log export volume in 2009 and a 25%

decrease in the first half of 2010 compared to the same

period in 2009. Among the main species that have shown

significant decline in log exports are greenheart,

purpleheart, kabukalli and washiba. However, production

volumes of these logs have been maintained implying

higher domestic processing.

Exports of value-added forest products, especially dressed

sawnwood for construction, have increased for washiba,

kabukalli and shibadan as a result of the policy

implementation. The Guyana Forestry Commission (GFC)

has been working to encourage the forest sector to take

steps to further develop timber processing. The GFC

expects that two currently implemented ITTO projects on

Kiln Drying and Forest Industry Development will boost

this effort.

According to the GFC, a comprehensive assessment and

recommendations on the current log export policy will be

published in 2011. In this review, performance of the

current policy, other international examples, and plans for

Guyana¡¯s forest sector will be taken under consideration.

Related News:

|