|

Report

from

Europe

Europe offers little prospect of improved hardwood plywood demand

European consumption of tropical hardwood plywood

remained at low levels during the third quarter and there

now seems little prospect of any significant upturn in

forward buying before the end of the year.

The significant UK market for tropical hardwood plywood

is becoming increasingly oriented towards break bulk

shipments from China at a time when consumption is

limited and buying is more price focused. Despite

continuing concerns about quality, fitness for purpose and

environmental credentials, Chinese plywood is being

favoured in the UK because it offers a 20-30% price

advantage compared to Malaysian plywood, the principal

competitor.

After significant arrivals of Chinese product in recent

months and with construction sector activity still slow and

facing an uncertain future, forward buying of hardwood

plywood in the UK has been limited in September. A

particular concern for the future of the UK market is the

government Comprehensive Spending Review due to be

published in October which may well demand very

significant cutbacks in public sector spending on

construction and renovation activity.

European imports of hardwood plywood from Indonesia

are now restricted to high value specifications, with much

of the volume destined for continental Europe rather than

the UK. Rising prices for birch plywood from Russia over

recent months, a result of the forest fires that raged

through the country this summer, have helped boost

demand for film-faced Indonesian plywood in Europe.

European imports of hardwood plywood from Brazil,

formerly a major supplier, are currently running at

negligible levels. Brazilian hardwood plywood exports to

the whole of Europe averaged little more than 2000 cu.m

per month in the first half of 2010.

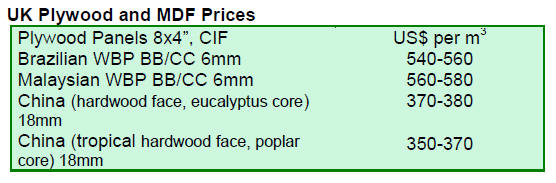

CIF Europe prices for Chinese hardwood plywood edged

higher over recent months in response to rising raw

material and labour costs in China and strengthening of the

Yuan on international exchange markets. Although there

are reports of a downturn in Chinese production in recent

weeks due to poor weather conditions, European agents

and importers report that supplies are sufficient to meet

continuing low levels of European consumption.

Anticipated increases in Chinese FOB prices may be offset

by slightly lower freight rates in coming weeks.

Meanwhile CIF Europe prices for Malaysian and

Indonesian hardwood plywood have remained broadly

steady in recent months, with a slight rising tendency

reported for some grades such as film-faced Indonesian

product. No significant supply problems are reported and

products are currently available for reasonably prompt

shipment.

Consumption of okoume plywood in the main European

markets of France, Netherlands, Italy and Spain, remains

very sluggish. This business has become increasingly

difficult during the course of 2010 with, on the one hand,

margins squeezed by rising raw material costs due to the

Gabon log export ban and, on the other, mounting

competitive pressure from lower priced alternatives such

as poplar combi plywood.

European demand for African sawnwood still subdued

European forward orders for African tropical sawnwood

have remained subdued during the third quarter. An

improvement in the Euro-Dollar exchange rate, which

decreased the competitiveness of African hardwoods

relative to Asian alternatives, reinforced the usual

slowdown over the summer vacation period. There is still

little sign of any significant improvement in orders at the

end of September. Many European importers continue to

reduce their stock holdings of African sawnwood in the

face of sluggish consumption and on-going supply

difficulties.

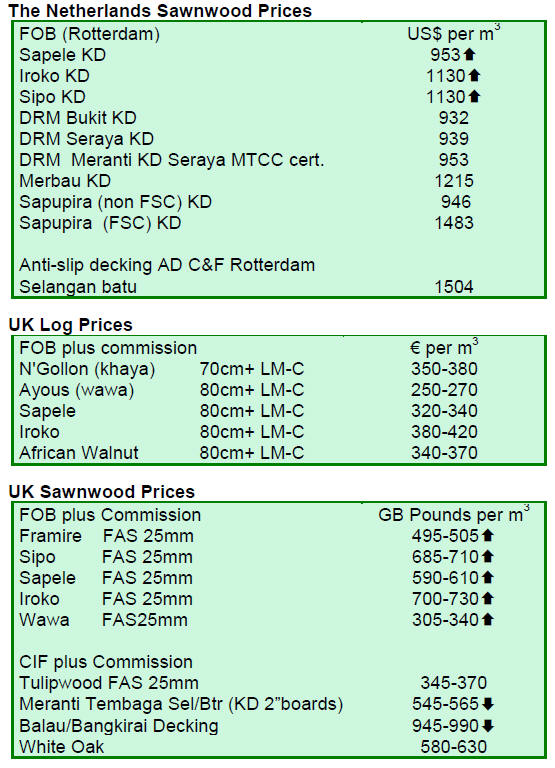

Following CIF Europe price rises for African hardwood

sawnwood in the first half of 2010, prices have remained

broadly stable over recent months. However, there are

some signals that the rise in prices for sapele sawnwood,

probably the most significant tropical joinery species

traded in Europe, may resume during the last quarter of the

year. This reflects low stocks both in Europe and in the

African supply pipeline which has resulted in long lead

times. New forward orders of sapele sawnwood are

unlikely now to be shipped prior to Christmas.

European demand for sipo sawnwood is currently very

subdued and FOB prices are stable. Demand for iroko

sawnwood is a little more buoyant which, against a

background of very limited availability, is encouraging

some exporters to push for higher prices.

The Gabon log export ban has led to a decrease in

availability of sawnwood of more special African species

such as padouk, ovangkol, and bubinga in the European

market. Significant volumes of these species were

formerly cut from Gabonese logs in European mills. These

species are likely to remain in limited supply until such

time as African mills respond by increasing levels of

processing for the relevant European niche markets.

In contrast to the situation with African sawnwood, there

are reports that weakening of the US dollar against the

Euro during the third quarter, combined with rising prices

for sapele sawnwood and low landed stock levels

encouraged a pick-up in European forward orders of

Malaysian meranti sawnwood during the third quarter.

Related News:

|