2.

GHANA

Sawnwood dominates export trade

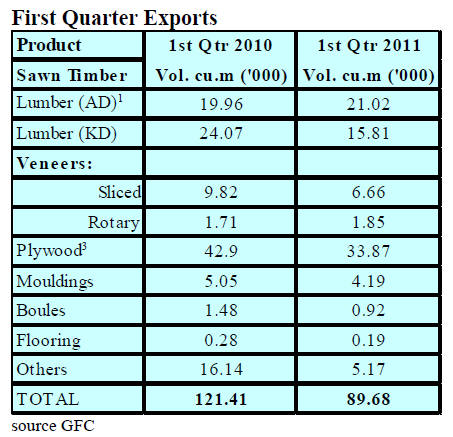

Ghana¡¯s revenue generated from timber and wood export

for first quarter of 2011 dropped 24% to Euro 30.18

million compared to the same period last year. The

corresponding export volume for the period was

89,680cu.m this year compared to 121,410 cu.m last year.

Air and Kiln dried lumber together accounted for 41% of

the total value of wood exports for the quarter, while the

contribution of plywood exports was 38%, 12 other

products contributed the balance of the total exported

value.

A drop in export volumes of kiln dried lumber (-34.3%),

sliced veneer (-32.2%), air and kiln dried boules (-37.8%)

and parquet flooring (-32.1%) has been attributed to the

inadequate domestic supply of logs.

Exports to African countries continue to grow

The ECOWAS market (mainly Nigeria, Senegal, Niger,

Gambia, Mali, Benin, Burkina Faso and Togo) absorbed

86 % of total wood product exports to African countries

and were worth around Euro 13 mil. in the first quarter

2011.

Plywood and air dried lumber (especially of Ofram and

Ceiba) were in high demand and continue to be of interest

to buyers in Nigeria and Niger. Ghana¡¯s exports of wood

products to African countries grew by around 42% in both

value and volume in the first quarter.

Hint of recovery in exports to the US

European markets accounted for 25% of the total value of

exports (Euro 7.56 million) and stood at 19,124 cu.m for

the first quarter of 2011.

Key markets included Italy, France, Germany, the United

Kingdom, Belgium, Spain, Ireland and Holland. The US

accounted for 10% of the value of exports and 4% of the

export volumes, both figures being higher than for the first

quarter 2010.

Markets in Asia such as India, Malaysia, Taiwan P.oC.,

China, Singapore and Thailand together contributed Euro

3.92 million to the total of wood export value in January-

March 2011.

The Middle East countries, notably Saudi Arabia,

Lebanon, United Arab Emirate and Israel together

contributed another Euro 2.55 million.

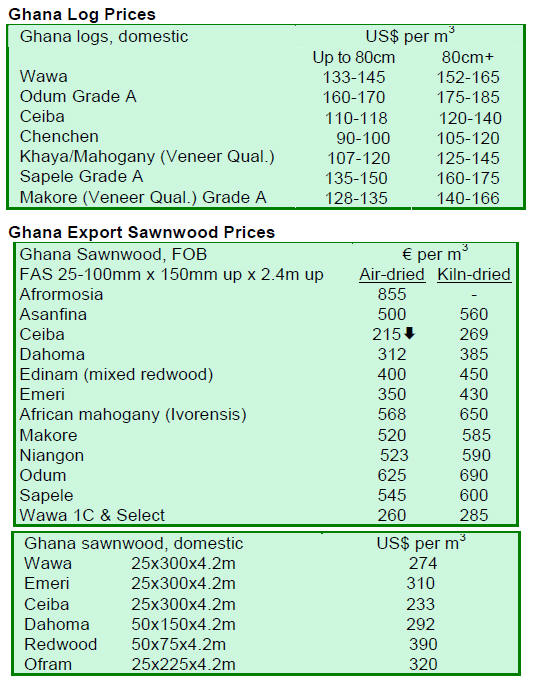

Ghanaian export mills meeting TIDD price guidelines

Sawnwood prices for traditionally exported species such

as Wawa, Mahogany, Sapele, Makore and Odum

improved slightly during the first three months of 2011.

There were improvements of between Euro 5and Euro 15

per cu.m over the TIDD approved Guiding Selling Prices

(GSP).

With the exception of lesser used species such as Essa,

Yaya, Bompagya, Duabankye and high density species

(especially Ekki, Danta and Denya) which have been

introduced into the Middle East and Chinese markets

recently, exporters were able to achieve the GSP for

sawnwood.

Export prices of plywood continued to increase during the

quarter under review. Prices improved by between Euro 5

and Euro 20 per cu.m. About 70% of the plywood

contracts for the period have been destined for Nigeria.

Prices of Niangon boules to France fell significantly

during the quarter under review. Prices dropped to Euro

450 per cu.m, the GSP price at the tme was Euro475 per

cu.m. However prices of the same product to Germany

were a little better hovering averaging around Euro 460

per cu.m.

3.

MALAYSIA

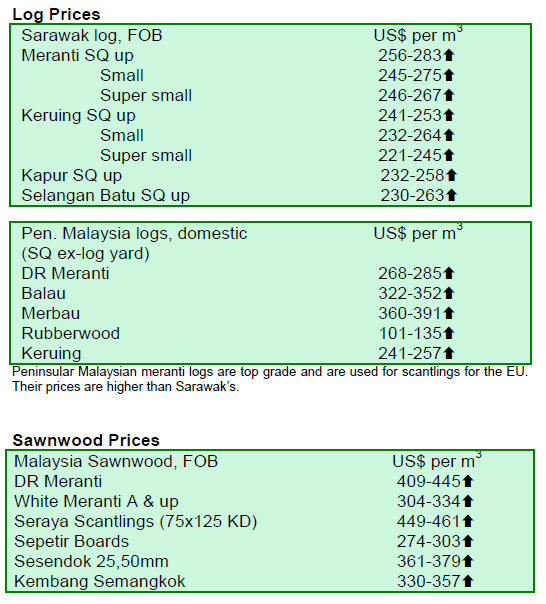

Domestic and export price differentials eroded

Prices of Malaysian timber and timber products continue

to rise sharply due to strong demand and higher fuel prices

which are driving up transportation and production costs.

Price differentials between domestic and export quality

wood products are eroding fast.

This is expected to have a spill-over effect on other

building and construction material in the market. The

increase in construction grade plywood prices is expected

to increase construction cost by 10% to 30% for both

commercial and housing projects.

Logging area reduced in 10th Malaysian Plan

The Malaysian National Land Council has set aside

155,000 ha. of forest to be harvested for timber annually

under the Tenth Malaysian Plan (10MP), a reduction of

15,000 ha. from the previous Ninth Malaysia Plan, which

allowed for 170,000 ha. of forest to be harvested annually.

According to the Malaysian Natural Resources and

Environment Ministry, the annual allowable cut was

adjusted to meet criteria set up to determine proper and

effective forestry management.

The ministry added that up to 2008, Sarawak had 6 million

ha. of forest reserve out of 14.43 million ha. for the entire

country.

However, in terms of forested areas, Sarawak had up to

8.23 million ha. this constituted 66.9% of the state land

area, compared to 4.4 million ha. (56.7%) for Sabah and

5.85 million ha. (44.7%) for Peninsular Malaysia.

New ¡®green¡¯ material for industrial applications

The Malaysian Agricultural Research and Development

Institute (MARDI) has succeeded in developing Kenaf

Polymer Composite (KPC) as a ¡®green¡¯ material for

construction and industrial applications. This came as a

result of intensive research and development over a six

year period.

Kenaf is regarded as a suitable substitute for timber

products as it is a short term fibre crop, thus mitigating the

need to harvest timber for wood-based product

applications. The initial market potential for KPC products

is estimated at RM3 billion annually.

Presently, samples of KPC have been sent to the EU for

further testing and certification of its durability and

properties. KPC is regarded as outstanding reinforcing

filler in thermo-plastic composites when combined with

certain plastic resins.

4.

INDONESIA

More transparency on forest

clearing moratorium

The 2 year moratorium on primary forest clearing and

logging provided guidance to the plantation, energy and

construction industries concerning green house gas

emissions, while offering various forms of exemptions and

concessions. The moratorium outlines the following:

• The moratorium mandates ministers and

government officials to suspend the processing of

all permits for logging and forest conversion

purposes, including those for timber and palm oil,

in primary forests and peatlands in the following

government categories: conservation forest,

protected forest and production forest. Permits

however, are allowed for secondary forests,

which have been affected by human and

commercial activities.

• It will be enforced over two years and is open for

extension. Its implementation will be overseen by

a task force on Reducing Emissions from

Deforestation and Forest Degradation (REDD).

• It covers up to 64.2 million ha. of primary forest

and more than 30 million ha. of peatlands. No

compensation will be offered under the

moratorium to firms unable to expand in these

areas, although the government has allocated

another 35 million ha. of "degraded forest" for

commercial development.

The moratorium provides the following

exemptions:

• Firms with existing permits or have approval in

principle from the forestry minister for permits to

log and convert forest.

• Extension of existing permits.

• Projects to develop geothermal and other power

plants, oil and gas fields, sugar and rice

plantations.

• Ecosystem restoration

• The government will regularly update a map of

its forests in a bid to correct overlapping permits

in the sector. The map will be published to help

investors clarify which forest areas are still on

offer and which are not.

5.

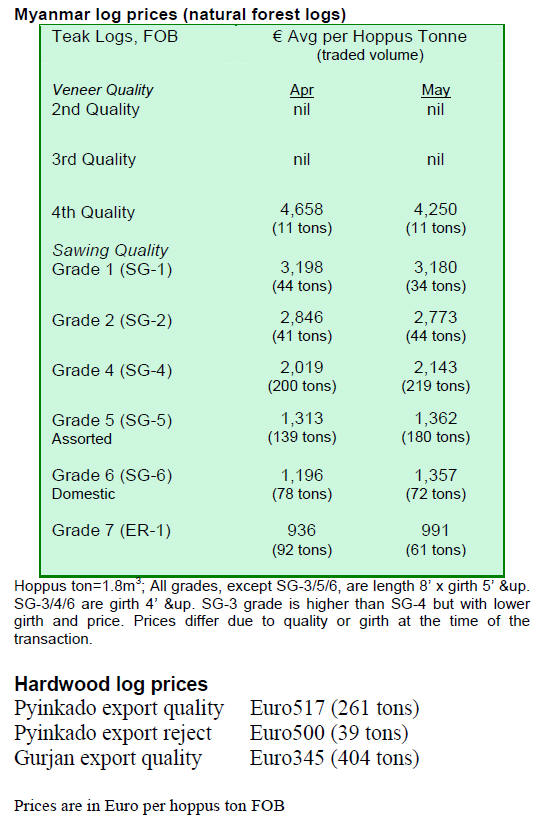

MYANMAR

monsoon strands logs in the forest

Myanmar¡¯s annual monsoon usually begins around the last

week of May or early June but this year the rains started in

April which caught loggers by surprise and they had to

leave a huge quantity of logs in the forest as conditions did

not permit transportation.

The drop in supply of logs triggered an upward swing in

log prices in Yangon and also resulted in some short

shipping.

Importers in Bangladesh steady buyers of Gurjan

Hardwood buyers report that while Gurjan prices are on

the rise the prices of Pyinkado are rather soft as trading is

slow.

The reason for the good Gurjan market is said to be

because of active purchases by buyers for the markets in

China and Bangladesh. Importers in Bangladesh have

always been steady buyers and the logs are used mainly

for sawnwood production.

Will firm April prices be sustained?

The market outlook for teak and other hardwoods has

picked up, one analyst said. It could be seen in the April

hardwood tender sales that export quality Pyinkado

fetched US$ 716 (cf. MTE list price US$ 642 to 678).

Export rejection quality Pyinkado fetched US$ 694 (cf.

MTE list price US$ 578).

Export quality Gurjan (Kanyin) logs fetched US$ 445

(cf.

MTE list price from US$ 375 to 390) Demand for Teak,

especially Sawing Grade 7 (ER1) is very strong but this

quality log is in short supply so demand is expected to

remain high.

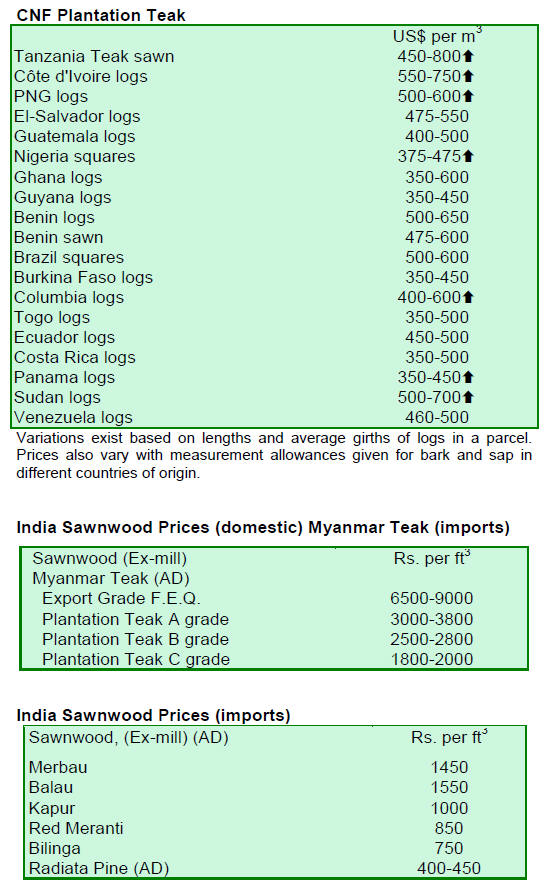

6. INDIA

India sets high export target

As the flow of exports from India improves, the

government of India has set an export target of US$500

billion for 2013-14, almost doubling the US$246 billion

achieved during 2010-11.

The current export policies, diversification of

markets and

technological advances have helped the government

project such an optimistic future. Processed wood product

exporters have also been quite active and expect to

contribute to enhancing the export performance.

Log sales brisk and prices firm

In Western India, the current schedule of log auctions,

which began on the 22nd of May in forest depots in north

and south Gujarat, will continue until the 5th of June.

Thereafter auctions will begin in forest depots of central

Gujarat notably the Vyara, Rajpipala and Tapti regions.

These auctions will run until the third week of

June.

Approximately 6,500 cubic metres of Teak and about

4,200 cubic metres of other hardwoods put up for sales are

of newly harvested logs, sales are expected to be brisk and

prices firm.

Optimism in building sector driving demand

Sales of teak and hardwoods in forest depots of Central

India for example Madhya Pradesh have also seen active

bidding. Reports indicate that approximately 20,000 cubic

metres have been sold and that newly harvested logs,

felled in the current season, continue to arrive.

There is a positive attitude in the Indian building

and

construction sectors and this is driving demand for locally

grown hardwoods as well as Teak. Prices secured in the

central as well as in the western forest depots tend to be

similar as the final market is the same. At present teak

prices per cubic foot Hoppus are as below:

Shipbuilding quality Teak logs Rs.2100~2300

First quality Teak Saw-logs Rs.1700~2000

Long length high girth Teak logs Rs.1500~1800

Average Sawmill quality15ft & up Rs.1000~1200

¡° ¡° 12ft & up Rs.900~1000

¡° ¡° 8ft - 10ft Rs.800~ 900

7. BRAZIL

Exports of tropical sawnwood and

plywood fall

In April the value of exports of timber products (except

pulp and paper) declined 5% to US$ 191 million compared

to the level of US$ 201 million in April 2010.

Pine sawnwood exports dropped 2.2% in value in

April

compared to the level in the same month of 2010, from

US$ 13.5 million to US$ 13.2 million. In term of volume,

April 2011 exports were down 9.3% from 62,400 cu.m in

April 2010 to 56,600 cu.m in April this year.

Exports of tropical sawnwood fell both in volume

and in

value, from 46,500 cu.m in April 2010 to 33,700 cu.m in

April 2011 and from US$ 22.7 million to US$ 17 million

in the same period. This corresponds to a 25% decline in

value and a 28% decline in volume.

On the other hand, pine plywood exports increased

7.4%

in value in April 2011 compared to the same month in

2010, from US$29.8 million to US$32 million. The

volume of exports increased 2% from 84,000 cu.m to

85,700 cu.m.

Exports of tropical plywood dropped from 9,600 cu.m

in

April 2010 to 6,500 cu.m in April 2011, representing a

32% fall. In terms of value a 22.2% decrease was

registered.

April was also not a good month for wooden

furniture

exports. Export earnings dropped from US$ 42.4 million

in April 2010 to US$ 40.2 million in April 2011 (-5%).

Furniture exports to Argentina grow

Argentina was the main destination for Brazilian furniture

exports last year. From January to April 2010 exports

totalled US$ 29 million but in the same period this year

exports were up 34% to US$ 40 million.

However, exports to the US and France, the other

two

main importers of Brazilian furniture, have declined so far

this year. Exports to France, the third largest importer of

furniture from Brazil, dropped sharply from US$26

million in January to April 2010 to just US$16 million in

the same period this year, a drop of around 38%.

Overall, Brazilian furniture exports dropped only

marginally from US$ 235 million (January to April 2010)

to US$ 232 million in the same period this year.

Wooden bedroom furniture bucks the trend

According to the Brazilian Association of Furniture

Industries (Abim¨®vel) in the first three months of 2011,

Brazil exported furniture worth US$17.3 million to the

United States. This is some 11.5% lower than that during

the same period in 2010 when exports reached

approximately US$ 19.5 million.

However, Brazilian wooden bedroom furniture is a

favorite in the US market and exports of these items have

been increasing according to the Ministry of Development,

Industry and Foreign Trade (MDIC).

The US/Brazil trade balance in 2010 was in favour

of the

US as the US imported US$ 19 billion but exported US$

27 billion to Brazil. The US is still the key trading partner

for Brazil, not only in the furniture sector but also in the

energy sector.

The trade between the two countries has a long

history and

is of importance and efforts are made so that this shall

remain so in the future.

Economic news

The National Consumer Price Index (IPCA) for April

closed close to the March rate (0.79%). The accumulated

rate for the year to date is 3.23%, 0.58 percent above the

rate of the same period in 2010.

In April the BRL appreciated against the US dollar.

The

Central Bank¡¯s Monetary Policy Committee (Copom)

raised the Selic rate by 0.25 percentage points, to 12% per

year. This move continues the slow down of the rate of

increase in the prime interest rate that began in January

2011, when the rate was raised by just 0.50 percent.

Forest Concession Bidding Process in Para

In Belem, State of Para in the Lower Amazon region more

than 150,000 hectares of public forests were offered for

concession bidding on May 17, 2011. The bidding

committee of the Forestry Development Institute of the

State of Par¨¢ (IDEFLOR) received six proposals for the

available areas.

The forest area put up for bidding is set described

in the

Public Forest Management Law, N¡ã 11.284/2006, and

harvesting in this forest will contribute to the supply of

legal timber. The concession contract requires traceability

of timber production and regular audits and monitoring to

ensure the transparency of legal production.

Moreover, it is hoped that these concessions will

attract

new style of investor since there is a guarantee that

concessionaire can harvest the area in a sustainable

manner and in partnership with communities over a 40

year period. The creation of a Special Bidding Committee

represents a new milestone in forest management in Par¨¢.

"Crisis Cabinet" to combat deforestation

In sharp contrast to the good news given in previous ITTO

market reports, new data shows that the rate of

deforestation in the Amazon has increased again. This data

shows that between August 2010 and April 2011 an area

1,849 sq. km was deforested.

Increases in production of soybeans and corn due to

high

international prices have encouraged producers to clear

more forest also, anticipated changes in the Brazilian

Forest Code are said to be behind the rise in forest

clearance.

The continual delays in the approval of the

Brazilian

Forest Code have had unfortunate consequences. Some

land owners have decided to clear forest land before the

bill on "zero deforestation" is approved in the Brazilian

Congress.

Deforestation in the state of Mato Grosso accounts

for

40% of area registered by the deforestation detection

system. It is reported that the area cleared increased from

505 sq. km to 730 sq.km in a nine month period spanning

2010 and early 2011.

Exceptionally heavy deforestation was detected

March and

April this year. The total deforestation is reported to have

increased from 103 sq.km in 2010 to 593 sq.km in 2011.

The federal government has established a "Crisis

Cabinet"

to expand operations to combat deforestation. The

Environment Minister and the Science and Technology

Minister announced the strengthening of monitoring

through deployment of new satellites by 2014.

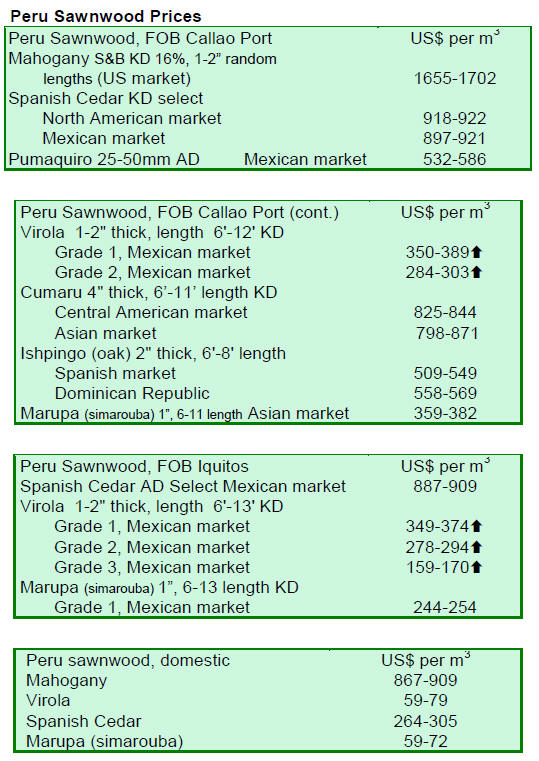

8. PERU

Revised Forest Act ready for

congress

The president of the Agricultural Committee of Congress

reported that, in late May, the Land Commission

submitted a replacement text for the Forest Act so it can

now be debated in the Congress.

A number of regional consultations (17) have been

held

and a national meeting consolidated the proposed

amendments. Representatives of indigenous communities

had demanded a review and discussion of 40 items in the

originally proposed act.

The previous law, Decree Law 1090, Law of Forestry

and

Wildlife, was repealed in December 2010 and a new bill

was approved but this was strongly challenged from many

angles by representatives of the indigenous population

which resulted in the review process.

Reforestation target for 2010 achieved

According to reports from AgroRural the executing

unit

within the Ministry of Agriculture, almost 95% of the

reforestation planned for the period 2007-2010 has been

achieved.

The national plan called for the planting of 230

million

trees, up to mid May this year the total planted was 217.8

million. For the 2010-2011 campaign the goal is to plant

60 million trees and so 47.4 million have been planted

(almost 80% of the target).

9.

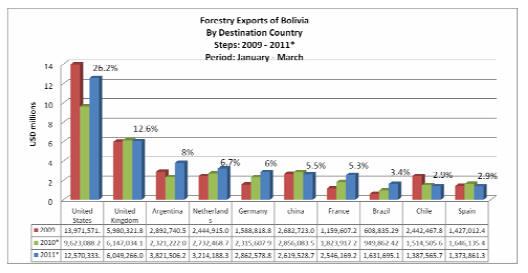

BOLIVIA

Rise in first quarter exports

Exports of timber and non-timber products from Bolivia in

the first quarter increased by 8.7% compared with the

same period last year, rising from US$ 44 million in the

first quarter 2010 to US$48 million in the first quarter of

this year.

Added value goods dominate export trade

The products exported during the year to date are

primarily processed wood products and processed Brazil

nuts.

The wood product exports comprise furniture, doors

and

decking. There is a small trade in primary wood products

such as sawnwood and poles. In the first quarter wood

products accounted for 57% of the total value of exports

the balance being from the export of non-wood products.

Companies in the U.S. continue to be the main

buyers of

Bolivian wood products taking some 26% of exports and

generating US$12.6 million in export earnings for Bolivia.

Buyers in the United Kingdom accounted for a12.6%

share of exports followed by Argentina (8%). The other

significant buyers are in the Netherlands and Germany.

10.

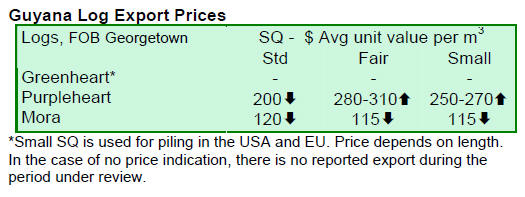

GUYANA

Sawnwood markets resilient

There was no significant export of logs in the period under

review. Even the two main species, Greenheart and

Purpleheart were not exported in any significant

quantities.

However exports of sawnwood made a positive impact

on

the export earnings. Many of Guyana¡¯s species are

exported rough sawn (i.e. undressed) for structural

applications.

These timbers attract good prices and the main

destination

for these durable species is Europe. Dressed sawnwood

continues to be in high demand in the regional Caribbean

market.

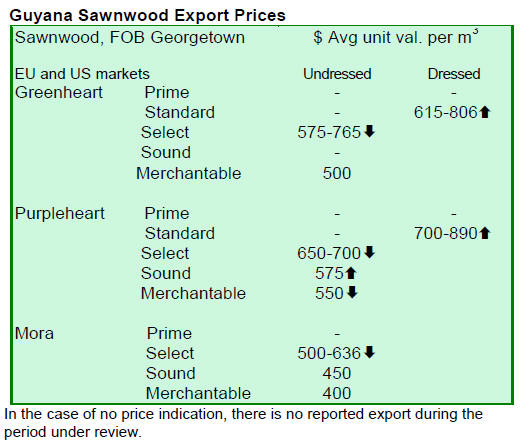

Greenheart and Purpleheart prices firming

Prices for undressed Greenheart (select) sawnwood

dropped at the top end of the price range from US$ 806 to

US$ 765, while prices for undressed Greenheart

(merchantable) remained stable. Prices for dressed

Greenheart moved up from US$ 785 to US$ 806 per cu.m.

Undressed Purpleheart (select) sawnwood secured

good

prices, reaching as high as US$ 700 per cu.m. Undressed

Mora prices slipped slightly from US$ 657 to US$ 636.

However dressed Purpleheart recorded saw a decline

in

prices from US$ 1,302 to US$ 890 for this period as

compared to the previous period.

On the other hand Guyana¡¯s Ipe (Washiba) continues

to be

in high demand in North America fetching good prices.

Roundwood and fuelwood also made notable contributions

towards total export earnings.

The export of products such as doors, spindles,

crafts from

Crabwood and Purpleheart and from non timber forest

products all made a positive contribution to export

earnings.

Opportunities sought in Republic of Congo

Guyanese investors and workers may have an opportunity

in the forest products sector in the Republic of Congo.

Currently work is being undertaken to draft a

Memorandum of Understanding (MOU) to be signed

within the next two to three months between the

governments of Guyana and the Republic of Congo.

In Guyana the Forest Products Development and

Marketing Council (FPDMC) is leading the cooperation

agreement.

This is expected to pave the way for Guyana to

access the

Central Africa ¡°Free Zone¡± for wood products and other

goods as well as services.

Currently, there is no trade between Guyana and

Central

Africa. However, if allowed access to the Free Zone

Guyana could enjoy new markets opportunities with 11

different Central African states.

At the same time the two countries are moving ahead

with

a MOU that focuses mainly on cooperation in the area of

forestry. The Guyana¡¯s FPDMC recognises that the

Congo is very advanced in forest management with

recognized certification and log tracking systems.

The MOU will provide for training for mills in the

Congo

on value added wood products and the development of a

business corridor for Guyanese to build houses and

produce wood products in the Congo.

Additionally, the Congo is encouraging Guyanese

businesses to explore joint venture investments with their

counterparts from the Central Africa state. The Congo

Government has also expressed interest in participating in

such ventures.

With Guyana¡¯s help, the Congolese Government is

moving to embark on a major housing drive to construct

wooden buildings for offices and houses.

Related News:

¡¡