|

Report

from

Europe

European market for tropical wood quiet but stable

The European market for tropical hardwood lumber is

quiet but stable. Uncertainty about future demand has

meant that forward purchasing is being kept to a

minimum.

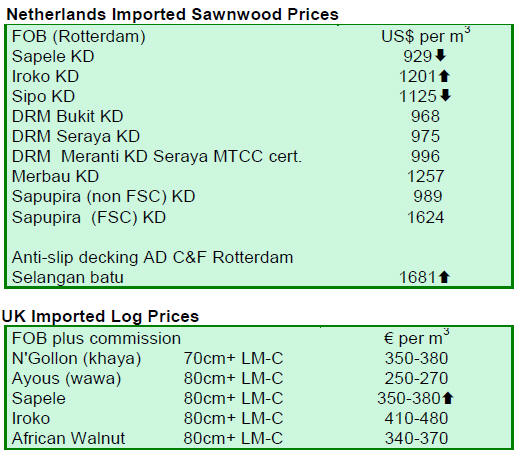

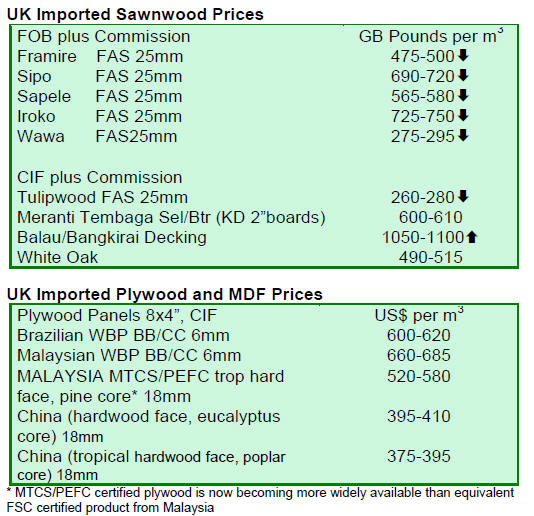

Overall, European stocks of sawnwood of the most

popular species such as meranti, bankirai, sapele, sipo, and

wawa remain at historically low levels. However, with

slow consumption this has not led to reports of significant

supply problems. Orders are being placed to replace stocks

as and when gaps open up.

Long lead times for African sawnwood remain a problem

in the European market. Turnaround times for forward

orders are currently running at around three months for

sapele and significantly longer for other species.

As a result there is heavy reliance on cross trading with

other importers for many species. Accordingly, Meranti

sawnwood, which despite log procurement problems in

Malaysia, is still more readily available at shorter notice

and is gaining a marketing edge.

The supply situation in Ivory Coast still remains difficult

with the result that availability of framire/idigbo and iroko

is restricted. Gabon��s log export ban which has yet to be

offset by sufficient development of domestic sawing

capacity has also resulted in limited supplies of a wide

range of more specialist species such as afzelia/doussie,

izombe, kevazingo/bubinga, and movingui.

Availability of Indonesian bangkirai decking profiles

improved slightly from earlier in the year. However the

existing landed stocks of bangkirai decking are generally

regarded as sufficient to meet relatively subdued demand

in the European market this year. This, combined with

high prices, is deterring any significant upturn in new

orders for bangkirai by European importers.

With only a few exceptions, prices on offer to European

buyers for the leading commercial species �C sapele, sipo,

iroko, framire, and meranti �C have remained relatively

stable in recent weeks.

The most notable exception is bangkirai decking, prices

for which have continued to escalate to levels that

importers say cannot be absorbed in Europe under current

market conditions. There are also reports of firming prices

in the European market for more specialist species

previously cut from logs imported from Gabon.

Consumption and exchange rate concerns dampen

forward business

A key factor discouraging speculative timber purchasing

by European importers is the high level of uncertainty over

future consumption levels and exchange rates trends.

Having started the year at around €1.28/USD, the euro

strengthened considerably to reach €1.48/USD in early

May. Since then the euro has lost only some of this

strength, falling to €1.38/USD by 10 July.

The strength of the euro has been maintained over recent

months by relatively high interest rates set by the

European Central Bank (ECB), by solid economic

performance in parts of north central Europe, particularly

Germany, and by Chinese investors�� efforts to diversify

out of dollars in favour of euro assets.

However, concerns continue to mount over contagion

from the sovereign debt crises in Greece. Furthermore, in

the last few days ECB President Jean-Claude Trichet

observed that economic activity in the Eurozone appears

to be slowing.

Trichet��s statement is backed by disappointing Italian

industrial production numbers as well as German trade

figures which show that Europe��s largest economy is

becoming increasingly dependent on imports of finished

goods.

These factors have encouraged some analysts to predict

more substantial weakening of the euro against the dollar

and other international currencies over coming weeks.

From the perspective of the European hardwood industry,

weakening of the euro would have several benefits. It

would help boost competitiveness of Europe��s furniture

manufacturers which have been struggling against the

pressure of imports. While a weaker euro would increase

import prices for raw material, it would also lead to

appreciation in the value of importers existing landed

stocks.

A weaker euro against the dollar also tends to improve the

relative competitiveness of African sawn lumber (typically

invoiced in euros) compared to South East Asian and

Brazilian sawn lumber (typically invoiced in dollars).

ThermoWood sales rebounded strongly in 2010

Production data published by the International

ThermoWood Association (ITWA) based in Finland gives

an insight into the recent development of Europe��s thermal

treatment business.

Members of the Association are those companies using the

ThermoWood method developed in Finland and which

have the legal right to use the word ThermoWood onproduct

and in their marketing material.

The ThermoWood method greatly enhances the durability

and stability of softwoods and temperate hardwoods so

that they are capable of competing with tropical

hardwoods in certain end-use sectors including decking,

window frames, cladding and external doors. Of 13 ITWA

members, 10 are based in Finland and one each in

Sweden, Japan and Turkey.

According to ITWA, ThermoWood sales increased

continually between 2003 and 2008 to reach 79,000 cu.m

in 2008 before the onset of recession which led to a

decline in sales to 74,000 m3 in 2009 (see chart).

However sales rebounded strongly in 2010 to reach an all

time high of 92,000 cu.m. Around 91% of ThermoWood

production was based on pine and spruce in 2010, with

birch, aspen and ash accounting for much of the rest. Last

year, 87% of all Thermowood produced was sold inside

the EU.

Membership of ITWA does not include companies using

the expanding range of alternative heat and chemical

treatments to ThermoWood. A recent analysis by the

German trade journal EUWID identified a total of 30

companies across Europe operating various treatment

plants of this type with capacity of around 300,000 cu.m.

On this basis, members of the ITWA probably account for

between 30 and 40% of total capacity across Europe.

Other countries with significant capacity include Germany

(about 13% of total European capacity), Netherlands

(12%), and Estonia (8%). Other countries with treatment

plants include France, Croatia, Austria, and Switzerland.

European countries to negotiate a legally binding

forest agreement

European Ministers agreed to begin negotiations on a

legally binding agreement (LBA) for sustainable

management of Europe's forests. The announcement came

at the Ministerial Conference on the Protection of Forests

in Europe (or Forest Europe) held in Oslo, Norway from

14-16 June 2011.

The agreement would require all European countries to

develop and ensure implementation of a national

sustainable forest programme. This would integrate

climate adaptation and mitigation strategies with broader

sustainability goals such as biodiversity conservation and

rural development. Ministers also agreed at the meeting to

cut the rate of biodiversity loss within forest habitats by

half, and to take steps to eliminate illegal logging.

According to media reports, there was no universal

support for adopting an LBA amongst European countries.

Sweden's Rural Affairs Minister Eskil Erlandsson told the

conference that while he supported the concept of

sustainable forest management, he favoured a voluntary

approach rather than an LBA. "I do not believe in common

legislation for forests across the pan-European region.

Put simply, one size does not fit all," he said. "We need to

recognise the different geo-climatic and socio-economic

conditions. Therefore, my conclusion is that the voluntary

track is the best way of supporting the development and

implementation of sustainable forest management."

However, he said he signed the declaration in order for

negotiations to begin.

As background for the Forest Europe meeting, and to

provide a starting point for negotiation of an LBA, the UN

Economic Commission for Europe (UNECE), the UN

Food and Agriculture Organization (FAO) and Forest

Europe collaborated to produce "State of Europe's Forests

2011: Status and Trends in Sustainable Forest

Management in Europe". The report is based on detailed

information provided by countries.

The main findings of the report include that:

• forests cover one billion hectares in Europe, 80%

of which are in the Russian Federation; European

forests cover 45% of total land area, or 32% if

Russia is excluded;

• European forests are expanding at a rate of 0.8

million hectares every year and remove the

equivalent of about 10% of European greenhouse

gas (GHG) emissions; there is a high degree of

fragmentation with around 30 million private

owners;

• most Europeans think that their forests are

shrinking;

• the sector provides four million jobs and accounts

for 1% of the region��s GDP;

and

• most countries have explicit objectives on forestrelated

carbon.

Authors of the report developed a draft method to assess

European forests�� sustainability, which while not yet peerreviewed,

identifies a number of threats and challenges,

including:

• landscape fragmentation;

• a shrinking and aging workforce;

• negative net revenues of several forest

enterprises;

and

• mobilizing enough wood for energy while

reconciling biodiversity values and the needs of

the traditional wood sectors.

The report is available at:

http://www.foresteurope.org/?module=Files;action=File.g

etFile;ID=1630

New guide to legal and sustainable forest and trade initiatives

A new guide to global initiatives designed to promote

legal and sustainable timber production and trade has been

published by Tropenbos International with support from

the Ministry of Economic Affairs, Agriculture and

Innovation of the Netherlands.

The guide describes a total of 127 government, privatesector

and NGO initiatives towards enhancing

understanding and support for the exchange of views and

proposals on efforts to advance forest governance and

encourage legal and sustainable forest industries and trade.

The guide suggests that "the range of initiatives reflects

the increasing commitment from a large variety of

stakeholders who are willing to address illegality in the

forest sector �� substantial momentum has been created".

While recognising the benefits from such a diversity of

initiatives, the guide also points to the dangers: "the

growing number... of initiatives....may make

communication, cooperation and coordination challenging.

Initiatives should avoid duplication and ensure consistency

in issues such as transparency, inclusiveness, market

pricing, equality, synergies and effectiveness, both in

policy development and in implementation."

It also notes that there are gaps in the frameworks and that

"still, some countries and regions either have limited or no

initiatives".

The guide recommends that "various areas should be

further explored for their potential to expand the scope and

effectiveness of efforts to halt illegal timber production

and trade.

Examples include timber procurement initiatives and

codes of conduct by the public and private sector,

incorporating effective forest governance and promotion

of legal and sustainable timber production and trade in

bilateral cooperation initiatives".

The guide is available at:

http://illegallogging.

info/uploads/enhancingtradelegallytimberweb.pdf

Related News:

��

|