|

Report

from

North America

Renovation and remodelling to be the main drivers of

moulding demand in 2011

Renovation and remodelling of existing homes is so far the

main driver of moulding demand in 2011, producers

learned at a meeting of the Moulding and Millwork

Producers Association earlier this year. At the meeting the

following market trends were identified, as reported by the

Door & Window Manufacturer Magazine:

Retail outlets dominate the distribution of moulding and

millwork products. Retail sales account for 65% while

35% of products sell through professional dealers and

direct industry sales. As a result, the Big Box home

improvement stores have a strong influence on the market.

Since 2008 retail and professional dealers have

consolidated and more than 1,200 retail outlets have been

closed by just three of the US’ largest building material

suppliers.

Residential renovation and remodelling is expected to

remain the main driver of moulding and millwork

consumption in the near future as the US housing stock is

aging and new house construction remains at very low

levels.

Finger-jointed mouldings account for over half of the US

market, followed by MDF. Solid wood moulding has an

estimated market share of just 6%. The market for MDF

mouldings is expected to increase through 2012, mainly at

the expense of pine mouldings as prices for pine raw

materials are increasing.

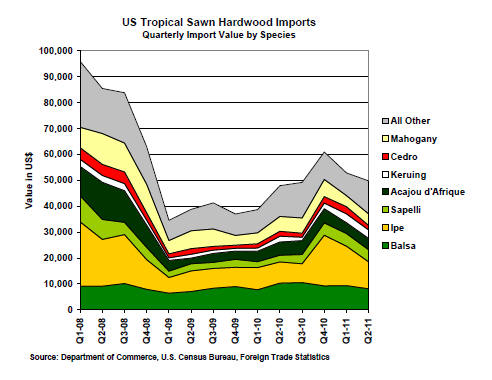

Second quarter decline in sawn tropical hardwood imports

The value of US imports of sawn tropical hardwood

continued to decline in the second quarter of 2011 after

gaining substantially in 2010. The value of year-to-date

imports is still significantly higher than in 2010 (+19%).

In terms of volume there was a 7% gain in year-to-date

imports.

The difference between the rates of change in the value

and volume of imports is largely due to the US dollar

weakening in 2011.

US imports of sawn tropical hardwood were US$49.8

million in the second quarter of 2011, down from US$52.8

million in the first quarter. Among the species that gained

the most year-to-date are virola (+105%), sapelli (+96%),

keruing (+91%) and ipe (+54%).

Year-to-date import values of the following species

declined from the previous year: teak (-29%), mahogany (-

12%), acajou d’Afrique (-7%) and balsa (-3%).

On a monthly basis, the volume of June sawn tropical

hardwood imports increased from May by 18% to 17,912

cu.m.

Imports of balsa were 3,049 cu.m. (-17% year-to-date), ipe

1,668 cu.m. (+35% year-to-date), keruing 1,659 cu.m.

(+80% year-to-date), acajou d’Afrique 2,059 cu.m. (-21%

year-to-date), mahogany 1,004 cu.m. (-16% year-to-date),

and virola 2,184 cu.m. (+114% year-to-date).

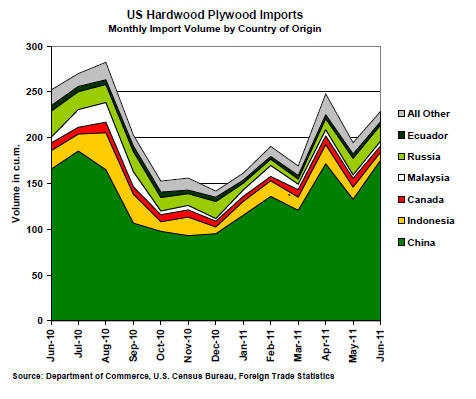

China main beneficiary from increased US hardwood

plywood imports

US hardwood plywood imports increased by 18% to

228,740 cu.m. in June. Year-to-date plywood imports

grew by 8% with China as the main beneficiary.

Imports from China were 175,312 cu.m. (+36% year-todate),

accounting for 77% of total US hardwood plywood

imports in June.

Imports from Indonesia were 8,995 cu.m. (-30% year-todate),

from Malaysia 5,505 cu.m. (-56% year-to-date) and

from Ecuador 3,401 cu.m. (-12%).

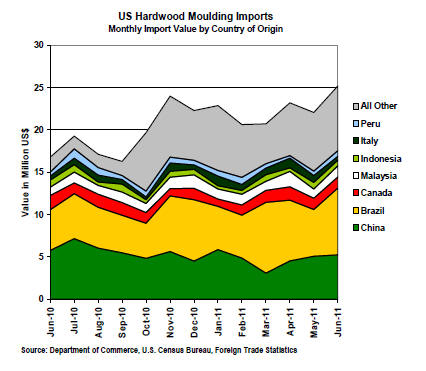

Growth in hardwood moulding imports from Brazil

US imports of hardwood mouldings have increased after a

brief decline in May. The value of imports was US$20.0

million in June, up 17% from the previous month.

Brazilian shipments account for 37% of year-to-date

imports compared to 27% from China. In June, Brazil

shipped hardwood mouldings worth US$7.9 million to the

US (+59% year-to-date) while imports from China were

US$5.2 million (+1% year-to-date) and from Malaysia

US$1.3 million (+50% year-to-date).

Malaysia largest supplier of hardwood flooring

US hardwood flooring imports rose by 29% to US$2.4

million in June, up 61% compared to the same period in

2010. Malaysia was the largest supplier of hardwood

flooring imports at US$637,000 (+109% year-to-date).

China exported hardwood flooring valued at US$564,000

(+49% year-to-date). Imports from Brazil were

US$217,000 (+23% year-to-date) and from Indonesia

US$110,000 (+143% year-to-date).

Related News:

|