|

Report

from

Europe

EU imports of tropical sawnwood main low but consistent

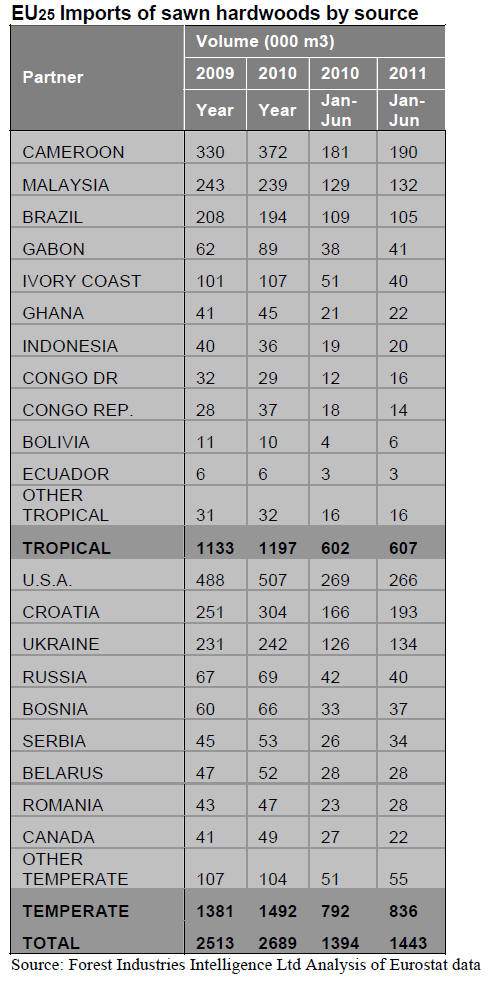

The following table shows imports of hardwood

sawnwood into the EU-25 group of countries from January

to June 2011.

Overall, imports are up only slightly compared to the same

period in 2010, with most of the growth in imports of

temperate hardwood, particularly from the countries of the

former Yugoslavia.

These countries are capable of supplying high quality oak,

a timber which has consolidated its hugely dominant

position in the European market this year.

During the first six months of 2011, EU imports of tropical

hardwood were very similar in volume terms and 5% up in

(euro) value terms compared to the same period the

previous year.

EU imports from Cameroon, Gabon, Ghana, the

Democratic Republic of Congo and Bolivia have

recovered quite robustly this year.

However these gains have been offset by a decline in

imports from Ivory Coast, Congo Republic and Brazil.

Imports from Malaysia have remained static compared to

the previous year.

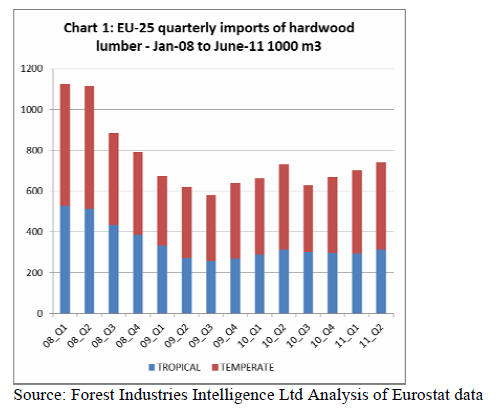

The following graphic shows quarterly trends in EU

imports of hardwood sawnwood during the last 3 years.

Total hardwood sawnwood imports rose consistently in the

12 months before June 2011, although they still remain

well below levels prevailing before the economic crises.

Most of the gains over this period have been in temperate

hardwoods, of which quarterly imports increased from

327,000 m3 to 427,000 m3.

In the year to June 2011, tropical hardwood imports

remained flat at around 300,000 m3 each quarter.

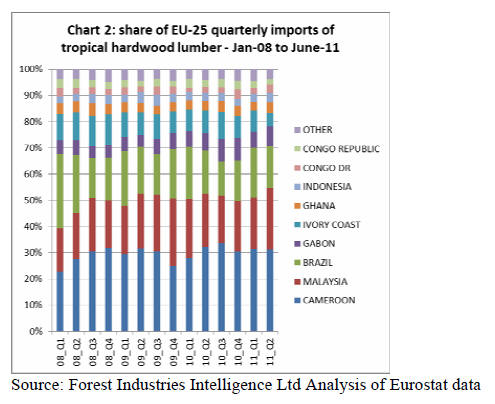

Cameroon consolidates position as dominant supplier to the EU

How the share of different countries in total tropical

hardwood imports has varied since the start of 2008 is

shown in the following graphic.

Cameroon is now well established as the largest single

supplier of tropical sawnwood to Europe, consistently

contributing around 30% of all imports. Malaysia’s share

has been fluctuating but generally increasing and

consistently accounts for around 20% of EU tropical wood

supply.

Brazil’s share has been decreasing in the EU as more

wood is now being diverted to Brazil’s domestic market.

However, Brazil continues to account for around 15% of

total European tropical sawnwood supply and the country

remains an important supplier to the exterior decking

market.

Political problems have led to Ivory Coast progressively

losing share in the European market, from around 10% to

5% in the 12 months to June 2011.

Gabon’s share of the European tropical sawnwood market

has been rising and now stands at around 7% following

inward investment in wood processing and the country’s

ban on log exports.

Little prospects for any significant upturn in EU demand

Prospects for any significant improvement in European

demand for tropical wood during the last quarter of 2011

and in 2012 seem slim say analysts.

Demand for both African and South East Asian hardwood

sawnwood has barely picked up any pace since the

summer slowdown. Meanwhile economic uncertainty is

once again mounting across the continent.

The market for African sawn timber in Europe is

characterised by cautious buying for main commercial

species despite relatively low stocks for the time of year.

This is due to a combination of economic uncertainty,

continuing tight credit conditions, and nervousness about

long lead times when buyers are increasingly demanding

quick deliveries. Only a very limited number of importers

are in a position to speculate on the purchase of larger

volumes to hold in stock.

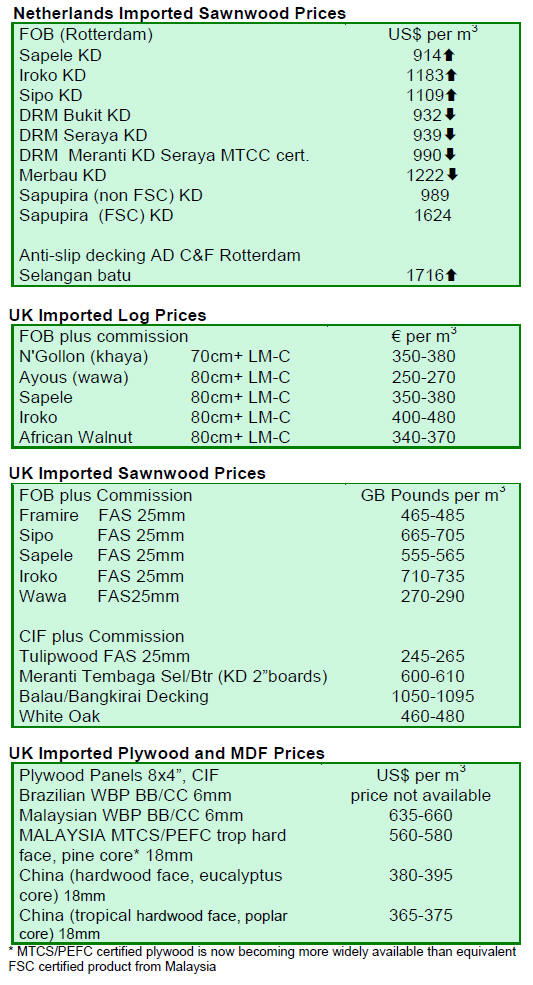

FOB prices for African sawn timber remain broadly stable,

with slow consumption balanced by limited supply.

However, market conditions vary according to species and

specification. There are reports of significant divergence

between markets for air dried and kiln dried African sapele

sawnwood in Europe.

While stocks air dried sawnwood is readily available on

the ground in Europe and prices are quite low, prices for

kiln dried are rising due to shortages of kiln space.

Meanwhile lead times for kiln dried material imported

from Africa are very lengthy.

UK importers report that framire/idigbo is now much

easier to source from Ivory Coast than earlier in the year.

However, most large UK importers are now less inclined

to purchase from Ivory Coast due to continuing difficulties

of obtaining credible documentation to demonstrate

legality at source.

This is becoming more of an issue as importers are

tightening up due diligence systems in preparation for

enforcement of the EU Timber Regulation from March

2013.

European landed stocks of iroko are reported to be quite

low at present. However there are also reports of

weakening prices for onward sales in Europe, implying

only slow consumption.

There is now relatively limited availability of sawn

sawnwood in the range of close-grained and fine-textured

timber species such as padouk, doussie , and bubinga

formerly cut in Europe from Gabonese logs.

FOB prices of sawn sawnwood for these species is now

around 20% up compared with the start of 2011.

European purchases of Indonesian bangkirai decking have

remained slow due to weakening of the euro against the

dollar and limited availability with strong demand in East

Asia and Australasia relatively firm prices.

These factors have encouraged more importers to look

again at Brazilian supplies of decking species such as

massaranduba and angelim pedra.

While Malaysian meranti sawnwood in popular European

specifications is available for immediate shipment,

demand has been so slack recently that some shippers have

eased prices in US dollar terms. However, this trend may

be short-lived as log prices are expected to rise again in

South East Asia.

Modified wood divides opinion

Long lead times for tropical hardwoods, combined with

the preference of stockists to work with low inventory

levels to reduce financial and perceived environmental

risks, continue to encourage some European importers to

search for substitutes to tropical hardwoods.

The European modified wood industry was out in force

again at the recent Timber Expo show in the UK, with

some major importers reporting their expectation to

gradually phase out tropical woods in favour of these

alternatives.

On the other hand, there are indications that the modified

wood industry has a way to go before this expectation is

realised.

At Timber Expo in Coventry there were a few specialist

importers willing to make the case for tropical wood over

modified wood.

One importer of hardwood decking said that modified

wood could not yet compete with the technical qualities of

the best tropical hardwoods. He suggested that poor

application of the thermal treatment process in particular

created a very dry product which would then absorb water

and discolour and degrade.

The UK’s TTJ also recently reported the difficulties

experienced by Indurite, a well-known modified wood

brand, to build market share in Europe.

Indurite noted that current modified wood prices mean that

it is still hard to find clients willing to switch away from

established products such as tropical hardwood coming

from South America. Prices for modified wood are tending

to rise on the back of increased energy and material costs.

Growing fears of double-dip recession in Europe

A recent poll of 70 economists by the news agency

Reuters suggests a growing chance the euro-zone economy

will slip back into recession as fears rise that the debt

crisis will escalate, financial markets slump further and a

global slowdown knock growth.

The poll undertaken in early October 2011 suggests a 40%

chance of a return to recession, up from a 30% in a poll

taken just a month earlier and a mere one-in-five in

August.

Reuters comment that “leading indicators point to weaker

economic conditions. Sentiment surveys have deteriorated

across key sectors of the euro zone economy, against a

backdrop of unusually high uncertainty and financial

market tensions,"

The Reuters poll aligns with the October 2011 Regional

Economic Outlook for Europe by the IMF which forecasts

that growth for all of Europe will slow from 2.3% in 2011

to 1.8% in 2012.

Economic indicators have weakened particularly

dramatically in Southern Europe, including in sectors of

considerable relevance to hardwood demand.

For example, the latest medium-term forecasts published

by the Italian construction industry association ANCE in

July 2011 suggest that construction sector investment will

decrease by 4% in 2011 (this compares to a decline of

2.4% forecast at the beginning of 2011).

Similarly, the latest data from the Spanish Government

office (Fomento) indicates that activity in Spain’s

devastated construction sector is sliding further into the

red. Planning approvals in the first seven months of 2011

(50,209) were 13% down on the same period in 2010.

A new report by ICD Research published in September

2011 concludes that growth in the Spanish construction

sector will remain extremely slow at around 1% per

annum at least until 2015.

However the economic news is not all bad. German

consumption figures have been good in recent months.

Building activity in Germany has risen well this year.

German furniture sector sales have also been increasing,

up 7.3% in the first half of 2011.

Interior door manufacturers are reporting brisk orders.

German flooring manufacturers are expecting sales growth

of between 5% and 15% for 2011 as a whole.

Related News:

|