2.

GHANA

GFC in discussions with industry to review timber fees

The Forestry Commission of Ghana (GFC) is consulting

with the timber industry on an upward revision of the

Timber Rights Fee (TRF), also known as the Timber Fee.

This is the annual rent that companies pay for their forest

concessions.

This fee has remained unchanged since 2005 so a

review committee is being set up. This was made known

by Mr. Robert Wilson, The Corporate Manager, Public

Relations of the GFC.

The fee is an annual rent paid by loggers on their timber

concessions and the upward revision that is expected will

generate more revenue for the State for various timber and

forest development projects in the country.

The Office of Administrator of Stool Lands (OASL) and

the GFC are responsible for the management of the

proceeds on behalf of stools / landowners.

While the GFC manages the Forest and collects revenue,

the OASL ensures that the stool /landowners receive their

share in the context of the prevailing laws on

disbursement.

Bank of Ghana considers Chinese Yuan as additional reserve currency

The Bank of Ghana has announced that it will invest in

emerging market securities. For some time there has been

a debate on whether the Chinese currency should be

included because of the growing Chinese investment and

economic cooperation. It now appears that a decision has

been taken by the Bank of Ghana to proceed and include

the Yuan in its portfolio.

Ghana strengthens maritime security capacity

In order to be better equipped to combat piracy and

generally improve maritime security the Ghana navy has

acquired four new Chinese-built patrol ships.

Piracy off the coast of West Africa has been on the rise

and acquisition of these new vessels will enable the Ghana

navy to respond to any maritime threat.

Floods in Accra brings business to a halt

Accra, Ghana¡¯s capital, as wells as some other parts of the

city have been hit by severe flooding following heavy rain.

Media reports talk of the Kwame Nkrumah circular road

being underwater preventing normal business activities.

The floods have caused serious damage to property but, as

yet, there are no reports of damage to wood processing

plants.

3.

MALAYSIA

MTCS rejected for Dutch government procurement

In 2010, the official Dutch government timber

procurement body TPAC judged that the Malaysian

Timber Certification System (MTCS) does not meet the

Dutch procurement criteria for wood.

On 19 October 2011, the Board of Appeal of Stichting

Milieukeur (SMK), an independent panel, rejected the

Malaysian Timber Certification Council¡¯s (MTCC) appeal

against this decision.

The UK Timber Trades Journal suggests that the main

reason for TPAC¡¯s rejection of MTCS is what it claims is

the scheme¡¯s limited recognition of the rights of

indigenous peoples and lack of adequate protection against

the conversion of certified natural forest to other uses,

including plantations.

The SMK appeals panel said MTCC had not provided

substantive arguments in their case. ¡°The result is that the

MTCC Board¡¯s action is on all counts dismissed,¡± it said.

An MTCC spokesperson said it regretted the decision,

which it said undermined the efforts by developing

tropical forest countries like Malaysia to implement timber

certification.

¡°As a voluntary timber certification scheme that has been

developed through a Malaysian multi-stakeholder process,

the MTCS is unfortunately held responsible by SMK for

issues that are inherent to the Malaysian constitutional,

legal and political system,¡± said MTCC chief executive

Chew Lye Teng.

¡°Secondly, the SMK unfortunately chose not to take into

consideration the additional measures to address the TPAC

concerns that have been agreed between MTCC and the

Dutch State secretary Joop Atsma.¡±

¡°Contrary to the SMK ruling, the Danish, British, French

and UK governments and the German municipality of

Hamburg have recognised the MTCS as providing

assurance of sustainable timber,¡± said the MTCC.

The Netherlands is the largest market for Malaysian

timber in the EU. In 2010, Netherlands imported around

100,000 cu.m of hardwood lumber from Malaysia.

The Netherlands accounts for 49% of exports of MTCS

certified timber products.

4.

INDONESIA

Nigeria makes presence felt at Expo

Indonesia

Indonesia attracted around US$351 million in trade

agreements and orders at the 26th Trade Expo Indonesia,

the country¡¯s largest trade exhibition, held from October

19th to October 23rd. Most of the new business was for

furniture products report analysts.

Nigerian businesses led the way with some US$38 million

worth of orders, followed by Malaysia (US$32 million),

the UK (US$26 million) and Belgium with US$20 million.

It was reported that Nigerian businesses were the

biggest

buyers at this trade show accounting for 11% of all

transactions.

Interim statistics show that at 6,391 buyers from 89

countries attended and participated in the exhibition. The

organizers are forecasting final attendance figures of

around 8,300.

Indonesia faces risks from the EU debt crisis and

economic stagnation in the US

The Indonesian Chief Economic Minister has said that he

was still optimistic that the Indonesian economy could

achieve a 6.5% growth in 2011 and may reach 6.7% in

2012, barring any negative global economic impacts.

He added that an IMF report indicated that Asia

continues

to face adverse risks arising from the EU debt crisis and

economic stagnation in the US.

The IMF indicted that economic growth in Asia will

hover

around 6.3% in 2011 and 6.7% in 2012.

Nevertheless, the Indonesia government will continue to

monitor and take pre-emptive measures in the face of any

possible impact from declining world economic growth in

2012, the Minister added.

5. MYANMAR

Myanma Timber Enterprise profile

The Myanma Timber Enterprise (MTE) reports that there

are some 91 state-owned sawmills in Myanmar. Ten of

these mills are producing for export. In addition to the

state-owned mills there are over 450 small and medium

sized sawmills and around 1,200 reprocessing mills.

The SMEs are privately owned wood processing plants

and mainly produce furniture and other semi-finished

products.

In addition, the MTE reports that it has six plywood

mills

and several furniture and moulding plants for the

production of wood products for export.

While there are some modern mills in the country the

MTE points out that many mills need re-tooling with more

advanced processing equipment.

As a result, says the MTE, the current milling

capacity is

well below the annual allowable harvest which means

there are logs available for export.

For more see:

http://www.myanmatimber.com.mm/

6.

INDIA

Domestic log prices firm as

imported log prices climb

With the monsoon rains having receded in most parts of

India log auctions have restarted in Central and Western

depots.

Approximately 3,500 cu.m of teak logs were sold in

South

Gujarat depots recently. Most of these logs were from premonsoon

harvests but, despite these being considered old

logs, prices in rupee were firm as the cost of imported logs

has been rising. In terms of dollars, prices remained at

levels seen in previous auctions of old stock and sales

were brisk.

Prices for non-teak logs have also been rising and

the

market is expected to continue on a firm trend in the

coming months say analysts.

Freshly felled logs have started to arrive at the

log depots

and will be auctioned after the Deepawali holidays.

Signs that Indian manufacturing output is slowing

India¡¯s exports maintained a robust growth rate despite the

prospects of a decline in the months ahead due to

European and American economic problems.

The EU and the US are the biggest markets for India

accounting for about 30% of all shipments.

In the first half of the year exports recorded a 52%

increase to US$160 billion. In contrast, imports have been

falling and only grew by 36% during the same period.

During September 2011 import growth fell 17% compared

to figures for September 2010.

Though there are signs that manufacturing output is

slowing, government sources are hopeful of achieving a

GDP growth rate of around 8.2% for the year.

A new name added to the list of well equipped

furniture manufacturers

Over the years, modern and well equipped furniture

factories have been established in India such as those of

Godrej, Featherlite, Zuari, Wipro, Reliance and Durian.

New names are being added to the list and the latest

is

Coffee Day Group (CCD chain) which is reported to have

made arrangements to import large quantities of tropical

hardwood from the Republic of Guyana.

Raw material will be shipped to Mangalore and used

for

the manufacture of a wide range of furniture at the

company¡¯s Chikmaglur plant.

Presently the company uses Silver Oak, Teak,

Rosewood

and other hardwoods, some of which come from areas

within the company¡¯s coffee estates around Chikmaglur.

These timbers are used for faced plywood and other faced

panel products as well as for furniture.

Discounts on consumer durables attracts hesitant

consumers

After several months of depressed retail sales in the run up

to the Deepawali holidays, sales of consumer durables

have picked up say analysts.

Reports suggest that furniture and other showrooms

are

busy but have had to offer big discounts to stimulate

demand.

7. BRAZIL

September exports drop across the board

In September, exports of wood products (except pulp and

paper) fell 4.7% in value compared to levels in September

2010, that is from US$206.4 million to US$196.8 million.

Pine sawnwood exports declined 11.5% in value in

September compared to the same month in 2010, dropping

from US$14.8 million to US$13.1 million. In terms of

volume, exports dropped 13.0%, from 64,700 cu.m to

56,300 cu.m over the same period.

Exports of tropical sawnwood also fell in volume

and

value, from 51,300 cu.m in September 2010 to 39,400

cu.m in September 2011 and from US$23.8 million to

US$21.5 million, over the same period. This performance

corresponds to a 9.7% drop in value and 23% drop in

export volumes.

Pine and tropical plywood export performance

disappointing

Pine plywood exports declined 15% in value in September

this year compared to levels in September 2010, from

US$24.8 million to US$21.1 million. Export volumes

were down 20% over the same period, from 67,500 cu.m

to 53,900 cu.m.

Similarly, exports of tropical plywood crashed from

8,300

cu.m in September 2010 to just 6,000 cu.m in September

2011, representing a 28% drop. In terms of value, the

decline was in the order of a 25% from US$4.8 million to

US$3.6 million.

The bad news continues with declines in wooden

furniture exports

Wooden furniture exports which fell from US 49.2 million

in September 2010 to US$41.6 million in September this

year representing a 15.4% decline in exports during the

period.

Timber industry urging Mato Grosso State

government to reconsider tax increase

Representatives from the Mato Grosso Center of Wood

Producers and Exporters (CIPEM) are discussing with the

Mato Grosso State government the increase in the Fiscal

Unit Standard (the index that updates the taxes charged by

the Brazilian States). A recent decision by the State

increased the rate to 31.5%.

This tax adjustment, says CIPEM, is having a

negative

impact on the timber sector as it has pushed up the cost of

wood raw materials.

The Fiscal Unit Standard, which was R$36.03 went up

to

R$46.83 which means that prior to the change the state

government used to collect 7.4% as a forest products

transport document services fee, today under the new

rules, the rate collected has risen to 11%.

CIPEM contacted the Mato Grosso State Secretariat

of

Environment (SEMA) to negotiate a reduction in the tax

rate on services.

Furniture industry benefits from BNDES credit line

The Brazilian Development Bank (BNDES) reported that

in the past 12 months around 500,000 transactions were

made through the BNDES Card worth R$ 7.2 billion. In

the same period, retailers and furniture manufactures made

27,000 transactions (5.4% of total) worth R$308.8 million

(4.2%).

The BNDES card is a credit line launched in 2003,

designed especially for micro, small and medium-sized

enterprises.

This credit line is pre-approved for companies with

gross

annual revenues of up to R$ 90 million. The credit limit is

R$1 million through the Bank of Brazil, Banrisul,

Bradesco, Caixa Economica Federal and Ita¨² Bank.

Repayment terms are up to 48 months and the interest rate

charged is 0.97% per month.

Purchases of raw material from distant States

driving

up production costs in Mato Grosso

Log harvests in the state of Mato Grosso totaled 1,045

million tons in the period January to September this year

and of this volume around 6% were utilised for the

production of wood products for export.

In addition to the raw materials provided from

State

resources, some sectors of the timber industry in Mato

Grosso have been purchasing wood products from other

regions of Brazil.

Most of these raw materials come from mills in Mato

Grosso do Sul, Parana and Sao Paulo States where

plantation timbers are used for OSB and MDF production.

The Furniture Industry Union of Mato Grosso

(Sindim¨®vel) has said that the purchase of raw materials

from other States for furniture manufacturing began due to

the difficulty in securing raw materials locally but this is

resulting in increased costs of production.

Delays in the release of imported Brazilian

furniture by

Argentinean authorities hampering trade

Furniture exporters in Brazil are complaining that delays

by Argentinean authorities in releasing from Customs the

imports from Brazil are hampering trade. Exports from

Brazil to Argentina from January to September fell 18%

compared to levels in the same period in 2010.

The World Trade Organization (WTO) norm for the

release of exports is 60 days but, according to the

Association of Furniture Industries of Rio Grande do Sul

(Movergs), Argentina is exceeding this norm and that

some exported products have not been released by

Argentinean authorities for almost twelve months.

Brazilian currency depreciates slightly against

the US dollar

According to the Brazilian Institute of Geography and

Statistics (IBGE) the National Consumer Price Index

(IPCA) rose 0.53% in September up from the level in

August (0.37%).

The cumulative rate over the past 12 months is now

7.31%

and this is above the government¡¯s goal which is 6.5%.

The average exchange rate for the Real against the US

dollar rate in September was BRL 1.75, while in the same

month of last year was BRL 1.72 signaling a slight

depreciation of the Brazilian currency against the US

dollar.

The Central Bank¡¯s Monetary Policy Committee (Copom)

decided to reduce the Selic rate by 0.50% to 11.5% and

this accelerated the pace of falling interest rates that began

in August. The next Copom meeting is scheduled for late

November.

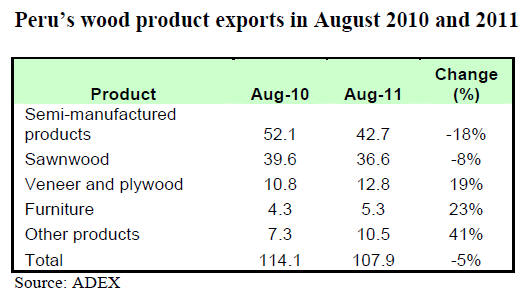

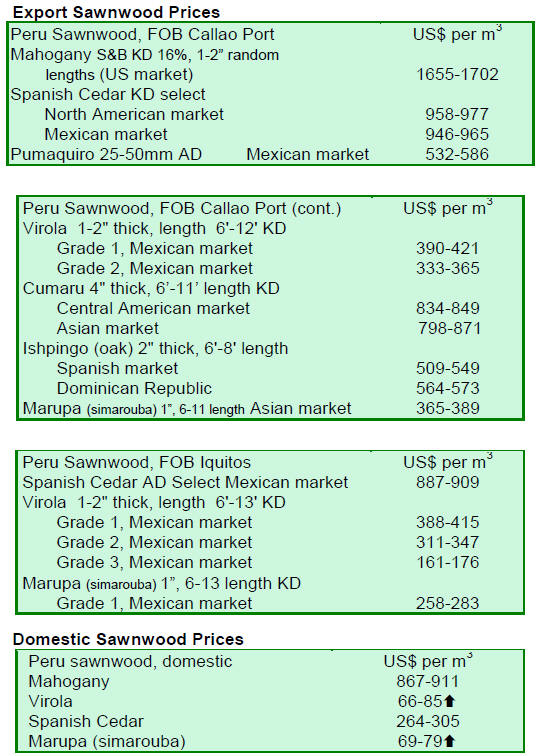

8. PERU

China reduces timber imports from Peru

According to data from the Export Association of Peru

(ADEX), wood product exports between January and

August this year totalled US$108 million FOB compared

to the US$114 million in the same period last year, a

decline of around 5%.

Up until the end of August the three main export

markets

were China, Mexico and the United States and these three

markets accounted for 76% of the wood sector exports.

Among the countries that reduced imports from Peru

were

China and Italy. China¡¯s imports of sawnwood fell

sharply.

Added value products 40% of all wood product

exports from Peru

Semi-manufactured product exports up to August, at US$

42.7 million FOB, represented 40% of the value of all

wood product exports, down from the US$52.1 million in

the same period in 2010.

Sawnwood exports were the second largest and

represented around 35% of all wood product exports.

Exports of sawnwood up to August were US36.6

million

FOB, down 8% when compared to the US$39.6 million

exported in the same period in 2010. The main market for

sawnwood from Peru was Mexico which accounted for

43% of total sawnwood exports.

Mexico the major market for veneer and plywood

Between January and August this year exports of veneer

and plywood were valued at US$12.8 million FOB, up

12%. Some 70% of all veneer and plywood exports from

Peru were destined for Mexico. This year Ecuador has

emerged as a new export market for plywood and veneer

from Peru.

Furniture and furniture parts exports post hefty

gains

in a gloomy market

Furniture and furniture parts exports were worth US$5.3

million FOB up 23% on the performance in the same

period last year. The main markets for these products

were the US and Italy.

9.

GUYANA

Timber enterprises benefit

from commissioning of new kiln

With the recent commissioning of a new wood-drying kiln

at least 32 enterprises in Linden in Guyana¡¯s Region 10

are expected to benefit.

This kiln drying plant was funded by the

International

Tropical Timber Organisation. One of the enterprises in

the Region 10 Forestry Group responsible for managing

the facility said it will be open to all the 32 Forestry Group

members in Region 10 as well as other companies.

This investment could pave the way for the further

development of the wood processing sector in the Linden

area.

The Government of Guyana is working to diversify

employment opportunities for the people in Linden and

wood processing is one of the sectors identified as new

economic activities.

The Guyana Forestry Commission, along with the

Forest

Products Development and Marketing Council of Guyana,

has been promoting kiln drying as an essential element in

the development of downstream processing.

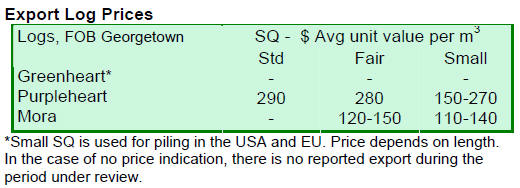

Purpleheart log exports earn valuable foreign

exchange

During the period under review no Greenheart logs were

exported. However the export of Purpleheart logs made a

contribution to overall export earnings. Purpleheart

Standard sawmill quality log prices increased compared to

levels reported earlier.

In contrast, Purpleheart Fair and Small sawmill

quality log

prices remained unchanged. Mora logs were exported and

Standard sawmill quality logs were at the same price

levels as previously reported.

On the other hand Fair and Small sawmill quality

Mora

logs were in good demand and prices remain firm.

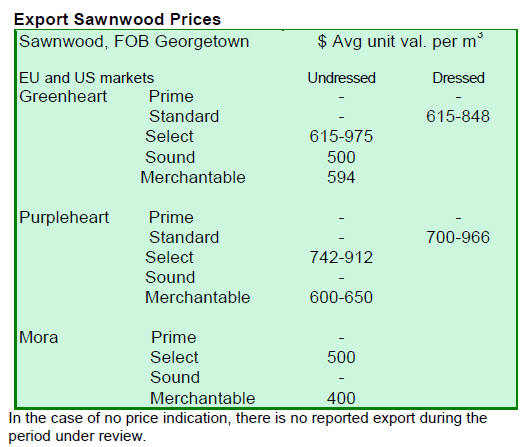

Market demand for Guyana¡¯s sawnwood sustained

Exports of sawnwood made a notable contribution to total

export earnings for this period. Undressed Greenheart

(select) prices were maintained.

There were some price increases for Undressed

Greenheart

Sound and Merchantable qualities and prices were

generally favourable.

Prices for Undressed Purpleheart Select quality

fell in the

period under review from US$1,050 to US$912 per cubic

metre. However Undressed Purpleheart (merchantable

quality) received better prices with its top-end prices

moving to US$650 per cubic metre.

Undressed Mora (Select and Merchantable qualities)

sawnwood prices remained unchanged on the export

market in comparison to previously reported levels.

Dressed Greenheart sawnwood prices experienced a

dip

from US$933 to US$848 per cubic metre, while Dressed

Purpleheart sawnwood enjoyed attractive prices on the

export market rising from US$912 to US$996 per cubic

metre.

Plywood prices improve in the Caribbean markets

Baromalli plywood was exported in BB/CC quality and

secured favourable prices as high as US$708 per cubic

metre in the main market for this product, the Caribbean.

Roundwood products secure firm prices

Other roundwood products such as piles and posts

attracted good prices on the export market. The top-end

price for piles wasUS$464 per cubic metre. Posts also

achieved favourable export prices as much as US$735 per

cubic metre.

Related News: