|

Report

from

Europe

European plywood market undergoing rapid

change

The European plywood market is changing rapidly.

Since the start of a recession in 2008, the market has

become less willing to pay premium prices for tropical

hardwood plywood. Instead it has opted for plywood

manufactured from alternative hardwood species.

The emergence of China as a major supplier of large

volumes of hardwood plywood at competitive prices

played an important role to drive this change. Now the

market looks set to alter again.

This time the main driver is likely to be the EU Timber

Regulation (EUTR), to be enforced from March 2013.

The EUTR will require that EU importers have access

to documents demonstrating negligible risk of any

wood product coming from an illegal source.

This will present challenges for suppliers of wood

products that rely on long and complex supply chains -

such as many Chinese plywood manufacturers.

Switch from tropical to temperate plywood

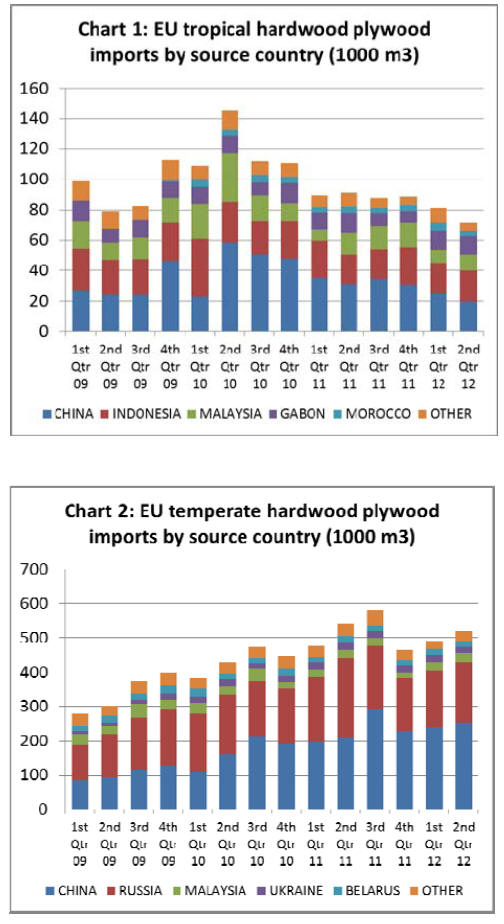

EU imports of tropical hardwood plywood have been

falling since the middle of 2010 (Chart 1). Between

January and June 2012, the EU imported 153,000 cu.m

of tropical hardwood plywood, 15% less than the same

period in 2011.

In the first half of 2012, tropical hardwood plywood

imports into the EU fell 33% from China (to 45,000

cu.m), 8% from Indonesia (to 40,000 cu.m) and 9%

from Malaysia (to 20,000 cu.m).

European domestic manufacturing of tropical

hardwood plywood �C using imported African okoume

logs - has also fallen dramatically and is now

negligible. This follows implementation of a ban on

exports of okoume logs by Gabon in May 2010.

In contrast, EU imports of temperate hardwood

plywood increased dramatically between 2009 and

2011 (Chart 2).

In the first 6 months of 2012, imports were 1.01

million cu.m, little changed from the same period in

2012. Imports from China were up 21% at 493,000

cu.m, while imports from Russia were down 18% at

344,000 cu.m.

The recent switch from tropical hardwood to temperate

hardwood plywood in the EU market is the result of

various factors. These include relatively high and

volatile prices associated with tropical hardwood

plywood and lack of availability. These trends became

strongly apparent following the tsunami in Japan in

March 2011 which led to a large volume of tropical

hardwood plywood being diverted to reconstruction

work in Japan.

EU plywood imports from Indonesia were particularly

affected by shipment delays and large fluctuations in

container rates during this period.

Meanwhile China��s ability to competitively produce

okoum�� plywood for the EU market has been impaired

due to imposition of anti-dumping duties on EU

imports of this product from China since 2004. The

duty levels imposed range from 6.5 % to 23.5 % for

four Chinese producers and 66.7 % for all other

producers.

However, availability of poplar and eucalyptus

plywood from China has increased rapidly. These

products have become increasingly important in

international plywood supply.

Although not offering equivalent durability, strength

and quality as tropical hardwood plywood products,

prices for Chinese hardwood plywood products are

extremely competitive (see table). The EU market has

increasingly accepted these products for a wide range

of utility applications requiring a lower level of

technical performance.

There is speculation that tropical hardwood plywood

from Indonesia and Malaysia may reclaim some

market share in the EU market during 2013. This is

partly because supply has improved over the last 12

months.

Prices for South East Asian plywood remained more

consistent and have been less volatile than in the past.

In addition, moves to develop comprehensive legality

verification systems in these countries are expected to

boost competitiveness following implementation of

EUTR.

A notable trend in the EU hardwood plywood market

during 2011 was replacement of Indonesian film-faced

plywood with cheaper Russian birch plywood

products. However availability of Russian birch

plywood declined in 2012 as manufacturers struggled

to source adequate volumes of good quality logs.

This led to a particularly sharp fall in availability of

high quality 5x10ft Russian birch plywood. This

situation is expected to ease in January and February

2013 with the onset of large scale winter felling in

Russia.

Slow plywood consumption in recent months

The market for plywood in the EU during the last

quarter of 2012 has been very challenging. Weak

construction sector activity meant that plywood

consumption was very slow. However production costs

for plywood manufacturers continued to rise. But with

supply generally in excess of demand, it is very

difficult to raise prices. Margins in the trade have been

declining.

Some Chinese suppliers of plywood to the EU are

seeking price increases of 2-3% to compensate for

rising production costs and strengthening of the yuan

against the US dollar. But these efforts have proved

unsuccessful so far.

Shipping lines attempted to force through significant

freight rate increases on the Asia-Europe route during

December 2012 in an effort to protect margins

following recent fuel price increases.

However, demand for container space on the route

remained low overall during the Christmas vacation

period and the recent rate increases are now expected

to be short-lived.

One result of low demand for container space is that

European importers are having little difficulty securing

stock. Importers can satisfy their immediate needs for

most plywood products quite easily and lead times

between ordering and delivery of new stock are short.

For example lead times for delivery of Indonesian

plywood to Europe currently average around 5 weeks.

Despite relatively high log prices in Malaysia,

Malaysian shippers of tropical hardwood plywood to

Europe have been reducing prices in recent months in

an effort to maintain market share. But while the price

differential in Europe between comparable Malaysian

and Chinese products has reduced in recent months, it

is still more than 10%.

Uncertainty created by EUTR

In addition to slow consumption, there is much

uncertainty in the EU plywood market concerning the

likely impact of the EU Timber Regulation. In the short

term, EUTR has led to very large bookings of product

from China to arrive prior to the Chinese New Year

festivities in February and just before the EUTR is due

to come into force.

These orders are well in excess of demand anticipated

in the first quarter of 2013. In contrast, forward orders

of both Chinese and tropical plywood for arrival after

the beginning of March 2013 have been very subdued.

The longer term impacts of EUTR are difficult to

predict.

There is still some uncertainty as to how effectively the

law will be enforced.

Many EU Member States have been slow to announce

which government departments will take responsibility

for enforcement and to set out details of monitoring

systems and sanctions.

The European Commission has yet to publish detailed

guidelines for EU importers. This fact, combined with

the high level of plywood import prior to the March

2013 deadline, suggest that it will take time for the full

effects of EUTR to become apparent.

Nevertheless, EUTR may well lead to major changes in

the EU wood products trade over the long term. This is

particularly true of the plywood sector which is

traditionally very dependent on imports from outside

the EU.

It is also a sector which relies heavily on hardwood

species from regions considered high risk of illegal

wood supply, including some tropical countries and

Russia.

EUTR enforcement action in Europe may be weak in

the initial stages. But the personal liability imposed by

the law, and the risk to the reputation of operators that

fail to comply, suggest most importers will take the

new law seriously. It is possible many importers will

become more risk adverse than strictly necessary under

the terms of the EUTR.

Chinese plywood and EUTR

Some large EU importers have been working hard with

their Chinese suppliers to ensure that all plywood

imported from the country complies with EUTR

requirements. However, there is still scepticism in the

EU trade that Chinese manufacturers will be able to

secure robust documentary evidence of legality for

many plywood product lines.

This is due to the complexity of supply chains in

China��s plywood manufacturing sector. It is also due to

lack of reliable systems to demonstrate legal origin in

many countries from which China imports logs for

plywood manufacture.

An article in the UK Timber Trades Journal in

December 2012 quotes a major UK plywood importer.

He suggests that due diligence work in advance of

EUTR has already ruled out 20% of the Chinese

factories with which his company deals. Many more

are expected to be added to the list as the process

proceeds.

Particularly affected will be Chinese plywood

manufactured from tropical species lacking FSC or

PEFC certification.

European importers are already identifying uncertified

wood from Papua New Guinea, the Solomon Islands

and most African nations as high risk.

European imports of uncertified Chinese softwood

plywood products, suspected of containing wood of

Russian origin, are also likely to be scrutinised closely.

Analysts suggest that many EU plywood buyers will be

only sourcing FSC or PEFC certified plywood after

March 2013.

On the other hand, EU importers are likely to be less

concerned about Chinese plywood manufactured using

only plantation-grown poplar and eucalyptus.

Environmental groups are keeping up the pressure and

raising the stakes for European importers engaged in

trade in Chinese plywood. They are sending out strong

signals that wood products from China will be first in

the firing line for EUTR scrutiny.

Malaysian and Indonesian measures to ensure

EUTR compliance

Indirect imports of tropical hardwood plywood via

transit processing countries like China may well suffer

22 ITTO TTM Report 17:1 1 �C 15 January 2013

as a result of EUTR. However, the EUTR may again

favour direct imports of tropical hardwood plywood

from Malaysia and Indonesia. This is because of

simpler supply chains and moves to develop third party

certification.

Indonesia is progressing rapidly towards full

implementation of a Voluntary Partnership Agreement

(VPA) with the EU on illegal logging.

Under the terms of the VPA, all timber products

exported from Indonesia will comply with the

Indonesian mandatory chain of custody certification to

ensure legality of product.

Similarly, a large proportion of Malaysian production

is PEFC-certified. All these measures are expected to

make the EUTR due diligence process for Malaysian

and Indonesian plywood much simpler.

Alternatives to tropical and Chinese hardwood

plywood

The high perceived risks associated with sourcing

plywood from some tropical countries, or countries

with complex supply chains like China, is already

encouraging a search for replacement products. EU

importers have been making more enquiries about

radiata pine and eucalyptus plywood from plantations

in South America.

European panel manufacturers have also been

encouraged to develop new products that may be used

to replace tropical hardwood plywood in external

applications.

For example, the Ireland-based MDF manufacturer

Medite recently won the UK Timber Expo Innovation

award for their ��Tricoya�� MDF panels.

Tricoya utilises the latest advancements in acetylation

technology, which naturally alters the wood��s chemical

structure so that it is not affected by the effects of

water absorption. According to the manufacturer��s

claims, MDF may now be used even in highly exposed

environments.

* The market information above has been generously

provided by the Chinese Forest Products Index Mechanism

(FPI)

��

|