|

Report

from

North America

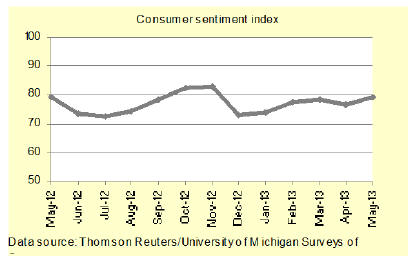

Consumers more positive about economy

Consumer confidence in the US economy went up in May,

according to the Thomson Reuters/University of Michigan

consumer sentiment index. Higher home prices and rising

stock market prices supported the more positive outlook.

Consumers plan to buy more than any other time since

2007. Households of all income levels were more

confident in the economy, but the largest gain was in highincome

households (incomes above $80,000).

Growth in manufacturing of wood products, furniture

Economic activity in the US manufacturing sector

declined in May for the first time since November 2012,

according to the Institute of Supply Management. On a

positive note, the wood product and furniture

manufacturing industries reported growth in May.

Unemployment remained essentially unchanged in April

and May. Unemployment was 7.6% in May, according to

the US Bureau of Labor Statistics.

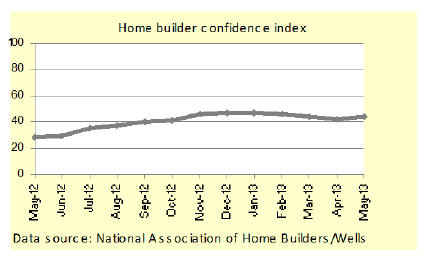

Growing demand for new homes

Builder confidence in newly built single-family homes

improved in May, according to the National Association of

Home Builders.

Higher building material costs and the lack of skilled

workers in some regions remain a challenge for builders.

However, more Americans are looking to buy a house,

while the supply of homes for sale is tight.

New home construction strongest in the Midwest

US housing starts fell to 853,000 in April at a seasonally

adjusted annual rate, down by 16.5% from the previous

month. The decline was almost entirely in multi-family

homes. The share of single-family homes in total starts

was 72%, up from just 60% in March.

The number of building permits issued passed the onemillion

mark in April. 1.02 million permits were issued, at

a seasonally adjusted annual rate, up 14.3% from March.

The number of permits issued is usually an indicator of

future building activity.

The Midwest saw the strongest increase in housing starts

(+10.9%) and building permits (+22.3%). The Northeast

posted declines in both housing starts (-12.8%) and

building permits (-2.0%).

Home prices up

Sales of existing homes increased by 0.6% in April. The

supply of homes for sale increased, but it remains lower

than what is considered a balanced market between sellers

and buyers.

Home prices increased from March to April. The largest

gains were in cities in the West (Sacramento, Las Vegas,

San Francisco), according to the Zillow Home Value

Index.

Canadian housing starts declined in April

Canada’s housing starts declined to 176,000 in April, at a

seasonally adjusted annual rate. The value of residential

building permits issued is up, but the Canada Housing and

Mortgage Corporation does not expect a reversal of the

downward trend in construction.

The housing market remains robust, based on sales of

existing homes and home prices.

Slow recovery in non-residential construction

Spending on non-residential building construction

increased by 1.0% from March to April (at a seasonally

adjusted rate). Private construction grew by 2.2% in April.

Public construction continued to decline (-3.0%) due to

reduced government spending. Commercial buildings was

the best-performing sector within public construction.

Architectural firms with a commercial/industrial

specialization reported a decline in business conditions in

April, according to the Architecture Billings Index.

The commercial building construction market remains

variable. Institutional architecture firms reported more

steady growth, but the rate of improvement is slow.

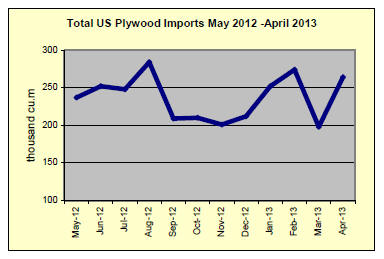

Higher hardwood plywood and furniture imports in

April

US imports of plywood, including imports from China,

recovered in April after a steep drop in March. Furniture

imports also grew, while imports of other processed wood

products were largely stable compared to the previous

month.

Hardwood plywood imports rebounded in April after a

steep drop in March. Total hardwood plywood imports

were 264,715 m³ in April, up 33% from MarMarch. Year-todate

imports are 35% higher than in 2012.

The recovery in total imports was due to higher imports

from China. China’s shipments increased from 61,058 m³

in March to 170,984 in April (+33% on a year-to-date

basis).

Imports from Indonesia fell to 31,322 m³ in April, but

year-to-date imports remain 99% above 2012. Imports

from Malaysia also decreased from March to 9,046 m³ in

April (+23% year-to-date).

Shipments from Ecuador fell to 11,871 m³ (+422% yearto-

date), but Ecuador remains the third-largest supplier of

hardwood plywood so far in 2013, after China and

Indonesia.

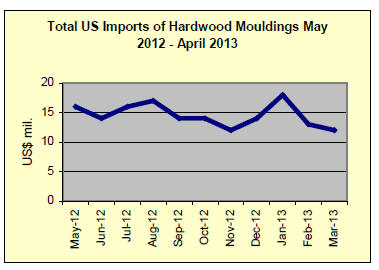

Hardwood moulding

Hardwood moulding imports increased in April following

two months of low import volumes.

The US imported $14.2 million worth of hardwood

moulding (-14% year-to-date). Imports from China

increased to $4.7 million, but year-to-date imports from

China remain 22% below 2012. Hardwood moulding

imports from Brazil decreased to $2.6 million (-28% yearto-

date).

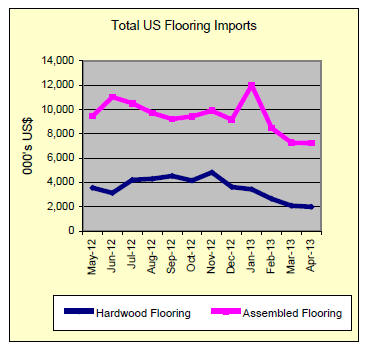

Wood flooring

US imports of assembled flooring panels remained steady

in April at $7.2 million. However, year-to-date imports are

11% lower than in 2012. Imports from China increased

slightly but they remain far below 2012 imports. China’s

shipments were $3.3 million (-25% year-to-date).

Hardwood flooring imports continued to decline and total

imports fell to just under $2.0 million in April. Year-todate

imports are still 20% higher than in 2012. Malaysian

hardwood flooring shipments to the US increased to $0.7

million in April (-35% year-to-date).

Imports from Indonesia were worth $0.5 million (+169%

year-to-date). Imports from China remained below

$200,000 (+36% year-to-date).

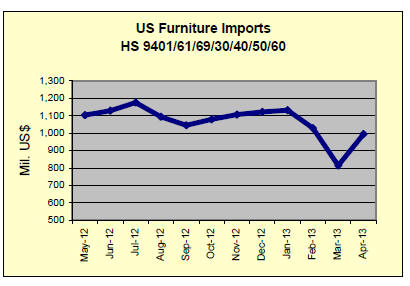

Wooden furniture

US imports of wooden furniture recovered from the

sudden drop in March. April imports were worth $994.5

million (+3% year-to-date).

China’s furniture shipments to the US grew to $456.3

million in April (+3% year-to-date). China’s share in total

imports was 46%, up from 39% in March.

Imports from Vietnam were $147.6 million in April (+7%

year-to-date). Mexico’s shipments declined steeply in

March, but they went back up to $45.4 million in April.

March furniture orders were up by 1% year-to-date

compared to 2012, according to a monthly survey of US

furniture manufacturers and distributors (Smith Leonhard

Furniture Insights May 2013). Two-thirds of the

companies surveyed reported higher orders so far in 2013.

Furniture shipments fell by an estimated 3% compared to

March 2012. Year-to-date furniture shipments were only

1% higher than in 2012.

Furniture inventories at distributors and manufacturers

remain relatively high for business conditions. Inventories

declined by 4% in March from the previous month

towards more balanced levels.

Market outlook: Growth in home sales will support

furniture demand

The March data on new furniture orders and shipments

indicates that market conditions are stable. April and May

were more positive for manufacturers and distributors,

according to Smith Leonhard.

The High Point Market furniture show in April was very

successful for most attendees. Improving consumer

confidence and the growth in home sales will contribute to

a stronger demand for furniture.

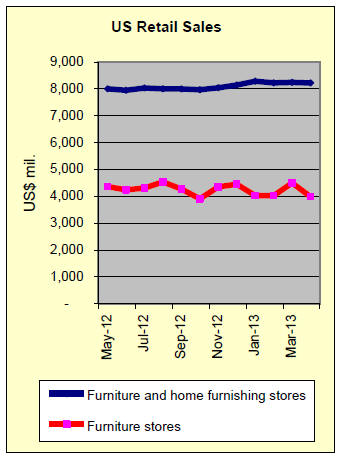

Furniture retail figures disappoint

Retail sales at furniture stores in the US fell by 11% from

March to April, according to the US Census Bureau. April

sales were $3.98 billion, when adjusted for seasonal

patterns and holidays. Furniture sales were only 1% higher

than in April 2012.

Proposed rules for formaldehyde emissions from

composite wood products

The US Environmental Protection Agency (EPA)

published the proposed rules for formaldehyde emissions

from composite wood products on May 29. The rules

apply to hardwood plywood, particleboard, MDF and

finished products containing these materials. Both

imported and domestically produced products must meet

the standards.

The proposed regulation consists of two rules:

The first rule sets the limit how much formaldehyde can

be released. It also includes testing requirements, product

labelling, and documentation and recordkeeping

requirements.

The second rule sets the third-party certification

requirements for composite panel manufacturers. EPArecognized

third-party certifiers will regularly audit

manufacturers, and conduct and verify formaldehyde

emission tests. More information about the proposed rules

is available here:

http://www.epa.gov/oppt/chemtest/formaldehyde/index.ht

ml

The EPA accepts comments about the proposed rules until

August 9, 2013.

|