|

Report

from

Europe

Improvement in economic sentiment in Europe, but conditions very

fragile

Economic sentiment in Europe improved a little during the second quarter

of 2013. Talk of a possible “depression” and euro-collapse has receded

into the background.

Nevertheless overall economic conditions remain fragile and the

construction sector, the major driver of wood demand, is still deep in

negative territory.

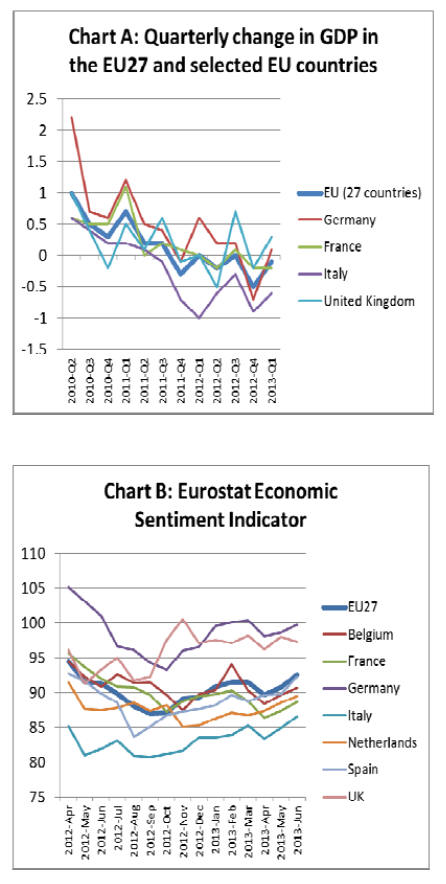

GDP data for the first quarter of 2013 reveals that the EU economy

remained static at the depressed level achieved in the last quarter of

2012.

Slow growth in Germany and UK during the quarter was offset by

continuing decline in France, Italy and other southern European

countries.

Nevertheless, the European Commission was sufficiently encouraged by the

figures to revise upwards their forecast for EU GDP change during 2013

from -0.3% to -0.1%. For 2014, economic activity is now projected to

expand by 1.4% in the EU.

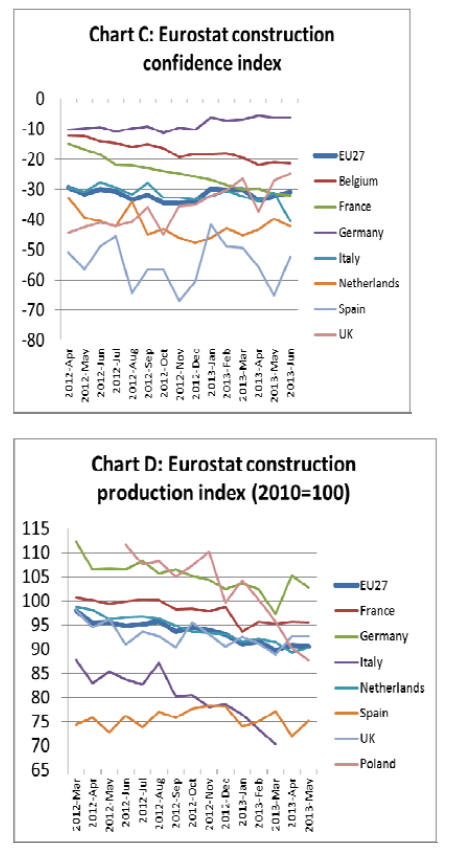

The Economic Sentiment Index (ESI) showed some improvement in the second

quarter of 2013 both for the EU as a whole and for many individual EU

countries (Chart B).

However, the index remains well below 100 in nearly all EU countries.

This means that a majority of those surveyed are still not optimistic

that market conditions will improve in the short term. Germany and the

UK continue to stand out as countries where there is a higher level of

confidence about future prospects.

The Citigroup Eurozone Economic Surprise Index fell very sharply between

the end of February and end of May.

This index tries to capture how well the data is coming in relative to

economic expectations. At the end of February 2013, the index stood at

+70 as most data was exceeding expectations at that time.

However the index fell like a stone to -53.2 at the end of May 2013.

This was due to publication of a relentless series of very poor numbers

across the euro-zone on economic growth, employment, manufacturing,

industrial production, and retail sales.

The CESI improved a little in June 2013. However the index has yet to

establish a meaningful upward trend.

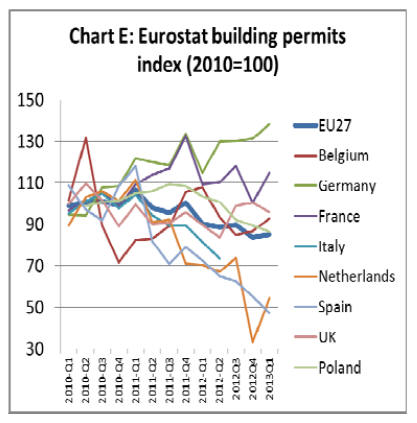

Indicators relating to the construction sector, of most direct relevance

to wood consumption, remain very negative. The Construction Confidence

Index was flat at -30 during the first 6 months of 2013 (Chart C).

This shows that construction professionals are very pessimistic about

the likelihood of an upturn any time soon.

The European Construction Production Index, which measures actual output

in the sector, declined continuously between 2010 and March 2013 and

remained flat at a low level in April and May 2013 (Chart D).

Construction output across the EU in the first 5 months of 2013 was only

90% of the depressed levels registered in 2010.

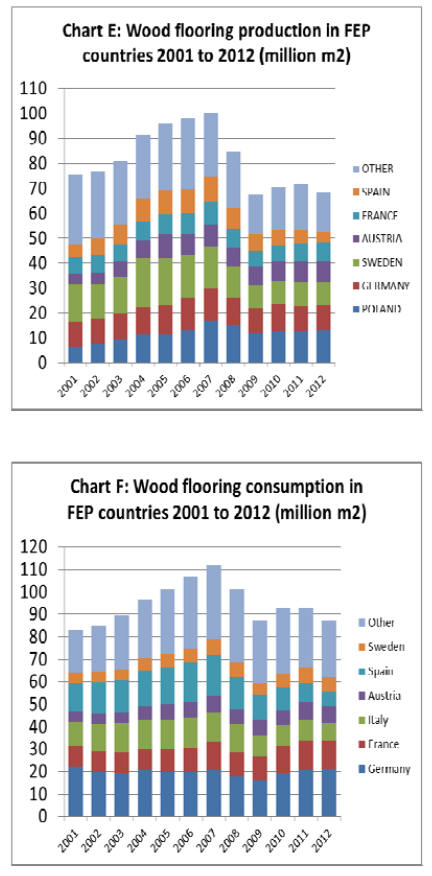

The latest data for the EU Building Permits Index shows there was a very

sharp fall in the number of construction permits issued across the EU in

the last quarter of 2012 and that permits remained at a low level in the

first quarter of 2013 (Chart E).

This strongly reinforces the view that construction activity is likely to

be even weaker during 2013 than in the previous year. Building permits

remain at historically very low levels in Spain, Netherlands, and Italy

and have declined sharply in Poland.

However, building permits have remained robust in Germany and recovered

slightly in France during the first quarter of 2013.

European parquet flooring consumption weakens once more

At their annual meeting in June, the Federation of the European

Parquet Industry (FEP) reported that wood flooring production in FEP

member countries declined in 2012 by 4.7% to 68.3 million m2 (Chart F).

This reversal meant that production in 2012 was no more than in 2009 at

the height of the global financial crises. Production increased a little

in Poland, Germany and Austria last year, but weakened in Sweden,

France, Spain and Italy.

Consumption in FEP member countries followed a similar trend, declining

5.9% to 87.5 million m2 during 2012 (Chart F). Again this was a

turnaround after two years of recovery in 2010 and 2011 and consumption

in 2012 barely exceeded that of 2009.

German and Austrian consumption continued to recover in 2012, but

consumption fell sharply into Spain and Italy and also weakened in

France, Scandinavia and Switzerland.

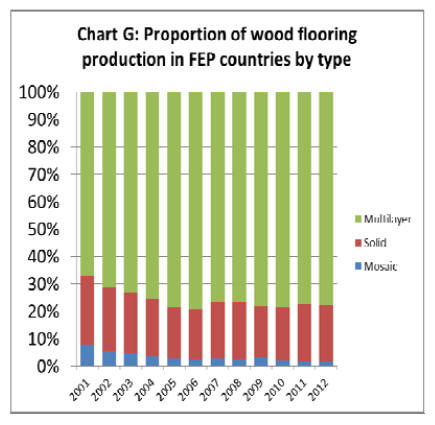

There was little change in the proportion of wood flooring output by

product type between 2011 and 2012 (Chart G).

Multi-layer flooring continued to dominate, accounting for 78% of the

volume of all wood flooring manufactured in FEP member countries during

2012. Solid wood flooring accounted for 21% of production volume and

mosaic flooring for 2% in 2012.

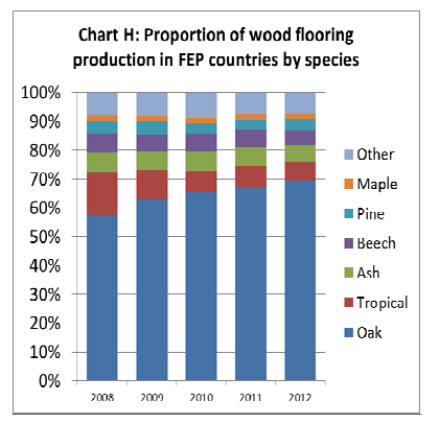

The most obvious trend in species usage during 2012 was a further increase

in oak’s dominance, mainly at the expense of tropical hardwood. In 2012,

oak accounted for 70% of all flooring production in FEP member

countries, up from 58% in 2008. In the last five years, share of

tropical wood has declined from 15% to 6%.

Over the same period, share of temperate species other than oak has

fallen from 28% to 24%. These include ash, beech, pine, and maple in

descending order of importance.

The increasing domination of oak is explained by a combination of:

consumer preference for a species perceived to be full of character and

of “high quality”; the development of a wide range of new staining and

other treatment techniques that have hugely increased the range of looks

that can be achieved with oak; wide availability from domestic and North

America sources; rising prices and declining availability of tropical

hardwoods; and environmental campaigns targeting tropical hardwoods.

European laminated flooring sector suffering from over-capacity and

competition

Europe’s laminated flooring sector, while still dominant in global

terms, has been struggling during the global financial crises.

In addition to declining consumption, the sector has come under intense

competitive pressure from manufacturers in other parts of the world,

particularly China.

The laminate flooring sector is also suffering from overcapacity which

has put considerable pressure on prices. While consumers benefit from

very low prices, retailers now need to shift huge volumes in order to

profit from sales of laminate flooring.

As a result distributors are looking for higher margin products. At

present there’s growing interest in Luxury Vinyl Tiles (LVT) which are

increasingly viewed as offering a better combination of quality, value

and margin.

The European laminate flooring industry is responding, partly through

down-sizing, partly through development of new higher value product

lines, and partly through marketing efforts emphasising the specific

performance and environmental benefits of laminate flooring. The

laminate market has become split between the low-end product selling for

less than euro 10 per square meter and the upscale product that offers

bevelled edges, hand scraping, wire brushing and exotic designs priced

in excess of €20 per square meter.

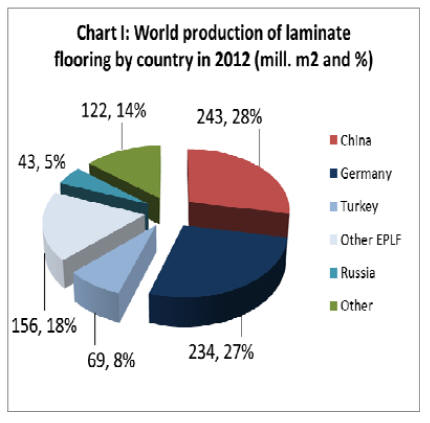

At their annual meeting in June 2013, the Association of European

Producers of Laminate Flooring (EPLF) discussed the global laminate

market noting that, in their estimation, China recently overtook Germany

as the largest single manufacturer of laminate flooring in the world.

EPLF estimate that of total global production of around 870 million m2

in 2012, China contributed 243 million m3 (28%) and Germany 234 million

m2 (27%). However taken together, the 22 member companies of the EPLF

(all located in Europe including Turkey) accounted for 460 million m2 in

2012, 53% of global production (Chart I).

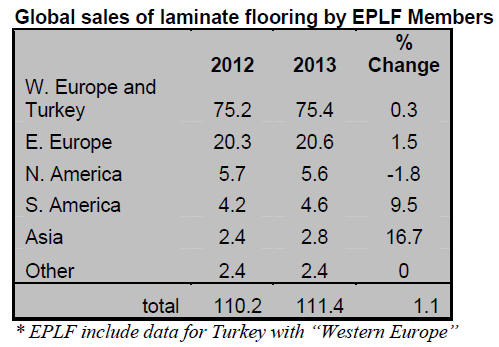

EPLF data shows that sales of laminated flooring by EPLF members fell

sharply during 2011 and 2012 (Table). During these years, low and

declining sales in Europe and North America were only been partially

offset by increased sales to Turkey, Latin America, Asia and Russia.

During the first quarter of 2013, overall global sales by EPLF members

stabilised at the lower level achieved in 2012.

This year sales have continued to decline in Germany, France, the UK,

the Netherlands, Spain, Austria, and the USA. However rising sales in

Sweden, Italy, Latin America and Asia have been just sufficient to

offset weak markets elsewhere.

In 2012, for the first time, EPLF members also provided sales figures by

product thickness. Around 45% of all EPLF laminate flooring sales were

products with a thickness of less than 7.5mm, around 45% were 8mm to 9mm

thick and the remaining 10% had thickness in excess of 10 mm.

Products 8mm to 9mm thick are the biggest sellers in Eastern Europe and

Turkey. In Western Europe, and Germany in particular, customers prefer

products which are thinner than 7.5mm.

European laminate producers complain about Chinese competitors in

Russia

Competition in the laminate flooring market is intense in all

regions. However, EPLF expressed particular concern about competition

from Chinese manufacturers in Russia in a press statement issued after

their June meeting:

“It is with some concern that the EPLF is seeing the Russian laminate

flooring market being flooded with mass produced Chinese goods, which

also do not meet high European standards. There is a risk that these

products will damage the reputation of laminate flooring amongst Russian

customers. The EPLF has therefore decided to initiate a quality campaign

to raise awareness of the high-quality products of European

manufacturers and to distance itself from inferior cheap products”.

The statement goes on to claim that European laminate flooring products

“are environmentally-friendly, high-tech products, manufactured in a

sustainable manner. In other words, they are gentle on resources and

socially responsible. European quality is synonymous with long-lasting

floors, innovative products for enhanced interior comfort, leading

design for versatility and individuality, good value for money and,

importantly, ecologically-sound products which guarantee safety for

customers and their families”.

Mounting challenge from “Luxury Vinyl Tiles”

Laminate flooring is under intensifying competitive pressure from LVT.

Made primarily from polyvinyl chloride resins and plasticizers, LVT is

being heavily promoted as a versatile, relatively low cost but

nevertheless “luxury” product. LVT manufacturers and retailers claim it

offers good cleaning and maintenance, easy installation, good acoustics

and high levels of durability.

It’s also claimed that new decorative films for LVT take advantage of

higher-resolution ‘HD’ printing and other technologies to produce

increasingly realistic wood, stone and tile looks covering a myriad of

designs and textures.

In countering the threat from LVT, the wood laminates industry is

placing considerable emphasis on the relative environmental benefits of

a wood-based flooring product.

European laminates manufacturers now make far-reaching claims that

products are made exclusively from either wood sourced from sustainably

managed domestic forests, or recycled material from the timber industry.

Even the decorative finishes are being printed on certified paper with a

high proportion of recycled material and natural water-based inks. They

are using eco-friendly resins as binder and increasing use of recycled

paper to make packaging.

They claim that laminate flooring manufactured in Europe is low-emission

and far outperforms legal limits for formaldehyde and VOCs (volatile

organic compounds).

To back these claims, European laminate manufacturers are investing in

Environmental Product Declarations (EPDs). Most laminate flooring

manufactured by EPLF members now comes with an EPD prepared in line with

the ISO14025 standard for "Environmental labels and declarations".

Laminate design trends

The “wood look” remains very dominant in the laminate flooring sector

comprising perhaps 80% of all sales. Amongst wood types, the laminates

sector follows the “real wood” sector so far as oak is the preferred

look.

According to EPLF “Oak is always popular with designers. No other

laminate flooring decor offers as many different possibilities as this

expressive domestic timber that has been a dominant mainstream player

over the last few years - and will continue to be so.

Natural, light shades, very rustic textures, subtly altered vintage

looks - oak offers an impressive range of possible designs”.

However, the laminates sector is also trying to differentiate itself

from the “real wood” sector by emphasising its ability to offer a huge

variety of “experimental timber looks”.

Increasingly radical designs are being promoted which combine the grain

of different wood species with unusual and bold colours and other

decorative features. The laminates sector is exploiting its ability to

offer a much wider range of board lengths and widths at competitive

prices than for the real wood product.

There’s also much emphasis in the sector on improving the texture and feel

of laminate flooring to produce a more “authentic” look. This is of

increasing concern to modern architects and consumers and one factor

that continues to give real wood a genuine competitive edge.

* The market information above has been generously provided by the

Chinese Forest Products Index Mechanism (FPI)

|