|

Report

from

Europe

Economy improves but no signs yet of rising tropical

hardwood demand

Across the EU, signs are emerging of a gradual

improvement in economic conditions and confidence.

Fears of a euro currency collapse have receded into the

background and the political situation seems more stable

in Southern Europe.

GDP growth resumed from the second quarter of 2013 in

several European countries, notably the UK and Germany.

Construction sector activity has also improved

significantly in the UK and Germany from the start of the

summer onwards.

However, there is little sign yet of these positive

developments filtering through into the European market

for tropical hardwood. After a slow start to the year and

subdued buying in summer, the EU market for tropical

sawn hardwood has continued weak into the autumn

months.

There was a brief increase in orders from European

importers during September immediately after the summer

lull to replenish depleted stocks. However, general lack of

confidence and limited availability of credit meant that

very few importers have been willing to speculate and to

build stock holdings in anticipation of stronger future

demand.

The slow pace of tropical hardwood imports into Europe

has been almost universal this year with nearly every EU

Member State recording a significant downturn in imports.

With consumption so limited for so long, the number of

tropical suppliers engaged in the European market has

declined. This means that even when demand improves �C

as it has recently in the case of sawn sapele �C supply soon

becomes a problem.

In addition to slow consumption and limited supply,

imports this year have been hampered by legality concerns

following introduction of the EU Timber Regulation

(EUTR) in March 2013 and by mounting competition

from a range of wood and non-wood substitutes.

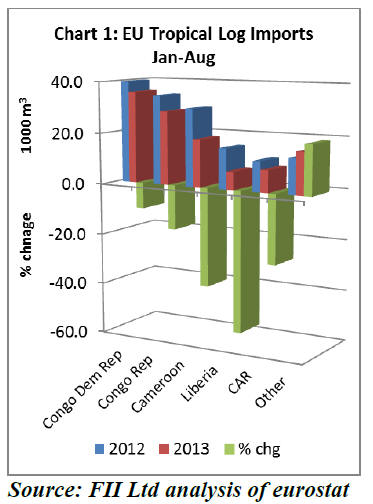

EU imports of tropical hardwood logs down 21%

In the first 8 months of 2013, EU imports of tropical

hardwood logs were 114,000 m3, down 21% compared to

the same period in 2012.

Imports of this commodity into France, the main

destination, were down 11% at 62,000 m3. Imports from

all the leading supply countries declined, including Congo

(Kinshasa), Congo (Brazzaville), Cameroon, Central

African Republic, and Liberia (Chart 1).

The decline is due to the combined effects of weak

European demand, supply constraints and regulatory

uncertainty. Political unrest has restricted log availability

from Central African Republic in 2013.

The Liberian government placed a freeze on all logging

activities in January this year, including on the exportation

of logs from the country.

In May this year, the Forest Stewardship Council (FSC)

terminated its relationship with decorative veneer and

hardwood timber producer Danzer Group following a

complaint from an environmental group. This has further

undermined European demand for products manufactured

from Congolese logs.

Meanwhile, encouraged by the EUTR, environmental

groups have focused heavily on finding discrepancies in

the legal documentation for log exports from the Congo

basin.

A shipment of Congolese wenge logs is currently being

held in custody by the German authorities as they

deliberate over alleged irregularities in the certificates of

origin filed for the shipment.

The competent Congolese Ministry has intervened to state

that the legal documentation is correct. A final decision is

now awaited from the German authorities over whether

the shipment will be confiscated and a fine imposed.

Irrespective of the outcome, the dispute has added to the

already high level of uncertainty in the EU tropical

hardwood log trade.

Tropical sawn hardwood imports unlikely to exceed

900,000 m3 in 2013

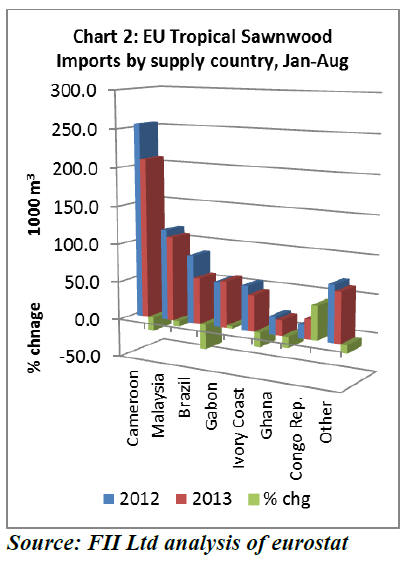

EU imports of tropical sawn hardwood in the first 8

months of 2013 were 597,000 m3, 14% down on the same

period in 2012 (Chart 2).

After falling below 1 million m3 for the first time since

records began in 2012, it is unlikely that EU imports of

sawn tropical hardwood will exceed 900,000 m3 in 2013

and they may be as low 850,000 m3.

EU imports of tropical sawn hardwood during the first

eight months of this year fell particularly heavily from

Cameroon, at 209,800 m3 down 18% compared to the

same period in 2012. Imports also fell sharply from Brazil

(down 32% at 60,000 m3) and Ivory Coast (down 19% at

47,000 m3).

After a rapid fall between 2011 and 2012, the pace of

decline in imports from Malaysia has slowed slightly this

year. Imports of Malaysian sawn hardwood were down 7%

at 109,900 m3 during the first 8 months of 2013.

In contrast, both Gabon and the Congo (Brazzaville)

recorded rising sales of sawn hardwood in the EU during

the first 8 months of this year. EU imports from Gabon

increased 3% year-on-year to 60,200 m3, while imports

from Congo (Brazzaville) were up 44% year-on-year at

25,700 m3.

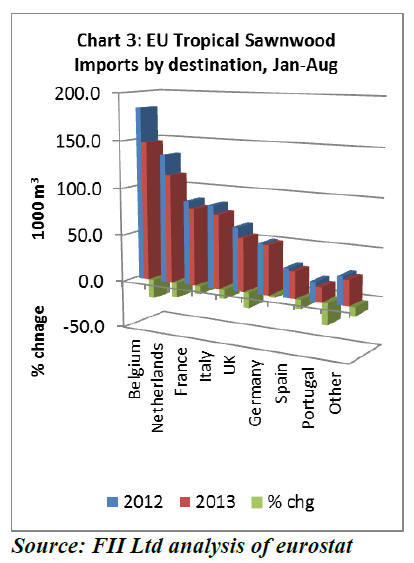

Imports of sawn tropical hardwood declined into all the

major EU markets during the first 8 months of 2013 (Chart

3).

Imports fell particularly heavily into Belgium (down 20%

compared to the same period in 2013), the Netherlands (-

16%), and the UK (-16%).

Imports into France and Italy declined sharply in 2012 and

have continued to slide in 2013, but at a slower pace. In

the first 8 months of 2013, imports were 81,100 m3 into

France and 77,800 m3 into Italy, respectively 9% and 10%

down on the same period the previous year.

Germany is the only large market where imports have

remained relatively stable this year, reaching 51,600 m3 in

the first 8 months, only 2% down on the same period in

2012.

Limited supply of sawn sapele

Falling EU imports during 2013 are only partly due to

weak demand. Limited supply of sawn sapele is now

beginning to have a significant impact on the level of

imports.

Lead times for sapele are becoming very lengthy with

orders placed now not being offered for delivery until

April next year at the earliest. This is resulting in sharply

rising prices both on an FOB basis and for landed stock in

the EU.

A number of factors are being blamed for lack of supply,

including increased diversion of trade to China and the US

and the fact that African mills have not returned to precrises

capacity.

In addition, a representative of one large EU distributor

with operations in Africa suggests that less sapele is

available in the new concession areas now being allocated

for harvesting. The reasons for this are unclear.

Supply is less of an issue and prices have been more stable

for most other major African commercial species.

Iroko prices on offer to European buyers have changed

little in recent months, although there is speculation that

this might change with rising demand, particularly in the

US and Ireland.

Expectations that Ivory Coast framire would be subject to

widespread boycott in the UK market as a result of EUTR

compliance concerns have not materialised. Although a

few former buyers are no longer engaged in the trade,

others have approved some Ivory Coast suppliers in line

with their due diligence requirements.

Those suppliers are now reaping the rewards of rising

European demand for their products, particularly in the

UK.

The low prices for framire offered by some Ivory Coast

exporters during the spring and summer months to

stimulate demand are no longer available.

Less direct competition between sapele and meranti

In the past, there was strong direct competition in the

European market between African sapele and South East

Asian meranti, so much so that prices changes in one

species would quickly impact on demand and prices in the

other.

However this relationship seems to have broken down

during the recession. The European market has become

increasingly accustomed to and oriented towards African

sapele.

In the formerly large Dutch window sector, Malaysian

meranti used to have a strong edge over African sapele

due to quicker turnaround times and tight adherence to

Dutch quality and size specifications.

However this market has been devastated in recent years

due to the recession and zealous adherence to FSC

certification standards by public authorities.

The result is that prices for meranti lumber on offer to

European buyers have remained weak and unresponsive to

the rise in prices for African sapele.

Another change is that Malaysian meranti is no longer

readily available at short notice to European buyers.

As the world‟s demand for tropical hardwood has shifted

away from Europe towards other markets, notably in Asia

and the Middle East, very few Malaysian sawmills now

maintain stocks of meranti lumber in European

specifications. Instead of waiting a few weeks for products

to arrive after ordering, turnaround times now extend to

several months.

Weak demand for hardwood for marine defence and

decking

European demand for heavy-duty species such as South

American greenheart and African ekki has been very weak

this year.

This is due both to the long-term decline in local

government funding during the recession and continuing

efforts by government authorities to substitute tropical

hardwood for other species and products with lower costs

upfront and which are perceived to have a smaller

environmental footprint.

The market for tropical decking timbers in Europe during

the 2013 summer season proved to be very slow, with

some reports suggesting demand down 20% or more

compared to the previous year.

Weather conditions in Europe were quite good this year

and there was a reasonable level of activity in the decking

sector as a whole. The decking market in the UK was

particularly good, boosted by rising business confidence

and better weather over the summer months.

However tropical hardwood has suffered a further loss of

share in the decking sector this year both to other wood

species and to Wood Plastic Composites.

Amongst tropical hardwoods, Asian bangkirai has suffered

more from substitution than South American alternatives

such as a cumaru and ipe. Orders of bangkirai for the next

spring season, usually placed in the autumn of the

preceding year, are expected to be delayed and low again

this year.

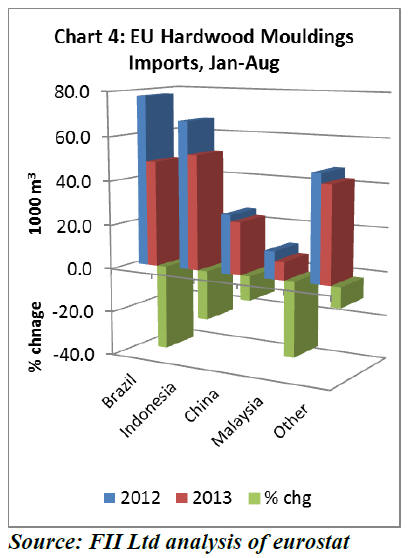

EU imports of hardwood mouldings decline 24%

In previous years, some of the decline in EU imports of

sawn tropical hardwood has been offset by rising imports

of hardwood mouldings and engineered wood products

from tropical countries. However this year, imports of

these products have also fallen sharply (Chart 4).

EU imports of hardwood mouldings, most of which derive

from developing countries, were 175,400 m3 in the first 8

months of 2013. That is 24% less than the same period in

2012.

Imports from Brazil fell particularly heavily, down 38% at

47,900 m3. Imports also fell from Indonesia (-22% at

52,100 m3), China (-11% at 23,700 m3) and Malaysia (-

34% at 8,200 m3).

Some of the decline in EU imports of hardwood

mouldings may be due to declining competitiveness

relative to EU domestic production.

For example, Brazil‟s hardwood industry continues to

suffer from high and rising labour and other business

costs, while China‟s labour costs have risen rapidly in

recent years. Hardwoods are also coming under intense

competitive pressure in the mouldings sector from pine

and MDF.

However, there are isolated reports of some tropical

hardwood products regaining market share in the

moulding sector at the expense of temperate hardwoods.

For example, in recent years American tulipwood made

significant inroads into the European market for painted

mouldings.

However this year there are reports of Ghanaian wawa

retaking share as the price of American tulipwood is

rising.

During 2013, lack of log supply and rising US and

international demand has led to a significant increase in

prices across the full range of American hardwood species.

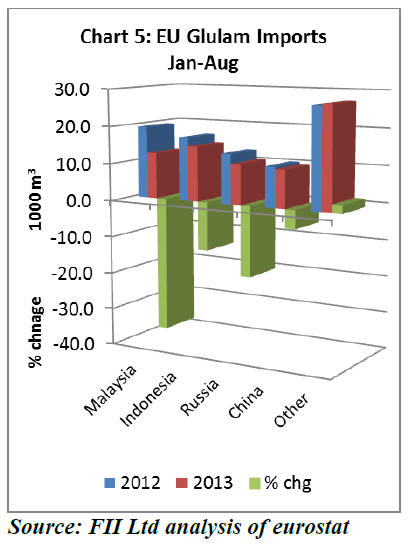

14% fall in EU imports of window scantlings

Weak construction sector activity during 2013 has led to

further declines in EU glulam imports (Chart 5). EU

imports of this product, which consist primarily of

scantlings for the window sector, were 75,800 m3 in the

first 8 months of 2013, 14% less than the same period the

previous year.

EU imports of scantlings from Malaysia were 12,300 m3

during this period, down 36% year-on-year. Imports from

Indonesia were 14,800 m3 between January and August

2013, a 15% decline.

Short-term prospects for meranti window scantling in the

EU market seem poor. Despite limited buying this year,

importers‟ inventories have run ahead of demand in recent

weeks.

Prices in Europe have been falling and exporters in Asia

are also coming under intense pressure to reduce FOB

prices.

However, longer term prospects appear more promising.

More building permits are now being issued in Germany,

the leading European market, and there is rising

confidence in the German construction sector.

The UK construction sector is also rebounding more

strongly than expected this year. The UK has not been a

significant market for tropical hardwood glulam in the

past, but interest in engineered scantlings is now rising

with introduction of tougher quality and energy-efficiency

standards for wood windows.

These factors, together with limited supply of sapele, the

leading African wood used in European joinery, might

lead to improving European demand for meranti window

scantlings during 2014.

��

|