|

Report

from

Europe

Uncertainty in European market for Chinese plywood

European demand for hardwood plywood manufactured in

China has been patchy during the second half of 2013.

Various issues have contributed to uncertainty in this

market during the period. Freight rates have been very

volatile.

In August, China imposed a 6% VAT requirement on both

the costs incurred from ex-mill to FOB and on prepaid

freight. Wet weather in some parts of China during the

autumn months led to delays in eucalyptus and poplar

logging. This in turn contributed extra transport costs for

mills forced to source logs from a larger area. The wet

weather also meant longer veneer drying times,

contributing to delays in shipments of finished plywood.

The market has also continued to be affected by increased

concern for legality verification following EUTR

enforcement. European importers are concentrating

purchases on the larger Chinese mills better able to

provide legality documentation.

Efforts to replace tropical hardwood veneers from regions

perceived to be high risk on illegal logging have

continued. This is changing the mix of products now being

delivered to the European market. There has been a

gradual rise in European demand for dyed reconstituted

poplar-faced plywood despite some concerns about the

quality of glues, the durability and difficulty of achieving

a smooth finish with these products.

Those European buyers willing to pay more for a higher

quality alternative have been sourcing Chinese plywood

faced with an FSC or PEFC certified sapele or meranti

veneer and a non-certified poplar or eucalyptus core.

Overall supply of Chinese hardwood plywood grades for

the EU market has been quite well balanced with demand

in recent months. Total production has been reduced due

to log supply problems and in anticipation of slow demand

over the European winter months.

During the autumn, Chinese mills were requesting that

orders be placed well in advance of the Chinese New Year

holiday season in January. By early December, many mills

had already fully committed their production for the preholiday

period.

Monitoring price trends for Chinese hardwood plywood is

now complicated by the diversity of certified and

uncertified products being sold into the EU market

following implementation of EUTR.

However, overall FOB prices have tended to firm on the

back of reduced production and higher veneer and other

costs in China in recent months combined with consistent

ordering in the run-up to the holiday season. Some mills

are compromising on the quality of veneers and glues in

an effort to maintain stable prices.

Availability of Chinese plywood to European buyers is

expected to become more restricted and prices to firm

during the first quarter of 2014. This is due to the

combined effects of limited log supply and the Chinese

New Year holiday.

There is also likely to be increased diversion of product to

the United States following the US government��s decision

on 5 November to dismiss the on-going anti-dumping case

against Chinese plywood. As a result, previously

announced anti-dumping and countervailing duties of

73.04% on US imports of Chinese plywood which were

due to come into effect in November have not been

imposed.

Volatile freight rates encourages EC anti-trust probe

into shipping lines on Asian routes

Fluctuating freight rates have contributed to very volatile

CIF prices for Chinese plywood delivered into Europe. For

example, freight rates on the Shanghai-Rotterdam route

fell from US$2,800/40ft container in early September to as

low as US$1300/40ft container by the end of October �C a

decline equivalent to about US$30 per cu.m of delivered

plywood.

In November, shipping lines tried to force rates for a 40-

foot container back up to US$2700, but these prices were

short lived and rates had fallen back to US$2000 by mid-

December.

The freight rate volatility stems partly from the practice of

the large container shipping firms operating on the Asia-

Europe route to announce major price hikes on a regular

basis.

These announcements have been made roughly

simultaneously four times in the past year, most recently at

the start of December. On each occasion, the larger firms

have been undercut immediately by smaller container

companies and the price hikes have failed to stick.

The European Commission, citing concerns that some of

the larger firms may be informing each other in advance of

their price intentions and thus impeding competition on

Asia-Europe routes, launched formal anti-trust

proceedings against 14 shipping lines on 22 November

2013.

Revision of EU GSP to impact veneer and plywood

market

Amendments to the EU's Generalized System of

Preference (GSP) scheme are impacting on the EU's

market for veneer and plywood. Certain developing

counties outside of the EU needing economic assistance

are permitted reduced rates of duty under the GSP scheme.

For customs declarations after 1 January 2014, eightyseven

of these countries will no longer benefit from GSP

status.

Of particular significance for the veneer and plywood

trade, Malaysia, Gabon and Russia will lose their GSP

status on 1 January 2014.

EU import duties for both plywood and veneer products

from these countries will then increase from 3.5% to 7%.

Cameroon, Ghana and Ivory Coast will also lose their GSP

status in January 2014, but these countries have other trade

arrangements in place. Brazil will also lose its GSP status

although this will not change anything in the case of wood

products because it was already specifically excluded after

having achieved a sustained significant volume of trade to

the EU.

Countries retaining their GSP status under the reformed

scheme include Congo DRC, Liberia and Myanmar. China

also retains its GSP status but, as with Brazil, this

specifically excludes timber products under Chapter 44, so

effectively no change.

EU tropical plywood imports down 4% in first nine

months of 2013

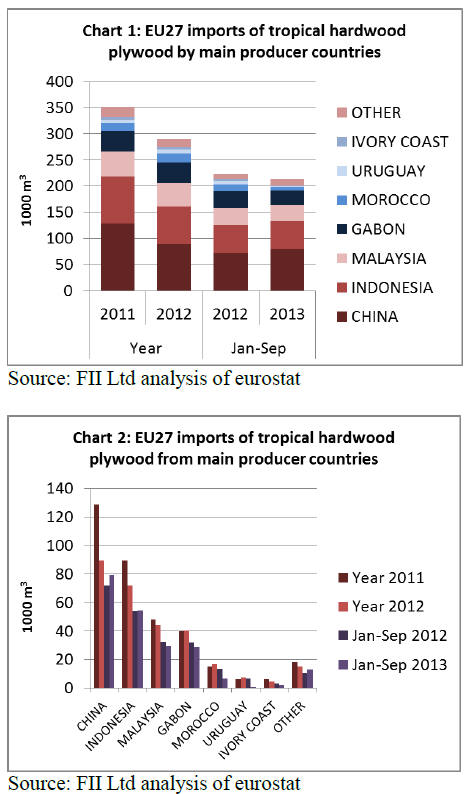

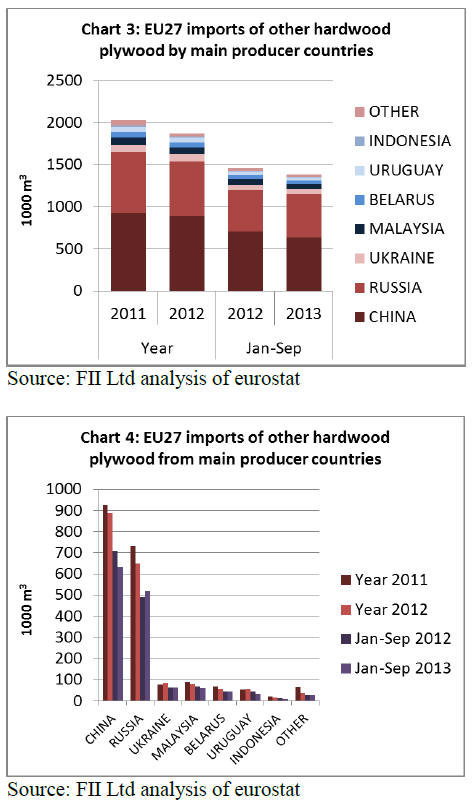

EU imports of tropical hardwood plywood in the first nine

months of 2013 were 214,100 cu.m, 4.2% less than the

same period in 2012 (Chart 1). During the period, imports

increased from China by 10% to 79,000 cu.m and

remained stable from Indonesia at 54,000 cu.m.

However imports of tropical hardwood plywood fell by

8.4% to 29,700 cu.m from Malaysia, and by 9.2% to

28,900 cu.m from Gabon (Chart 2). Imports of tropical

hardwood plywood have been rising into Belgium, the UK

and France this year, but declining into the Netherlands,

Italy and Germany.

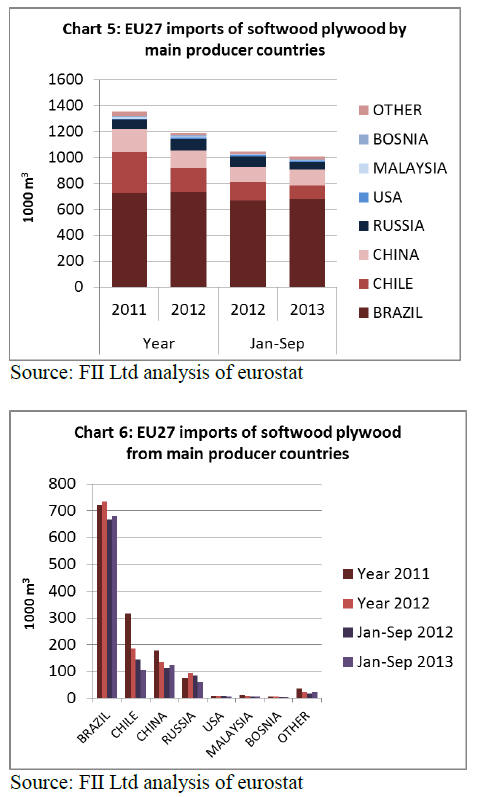

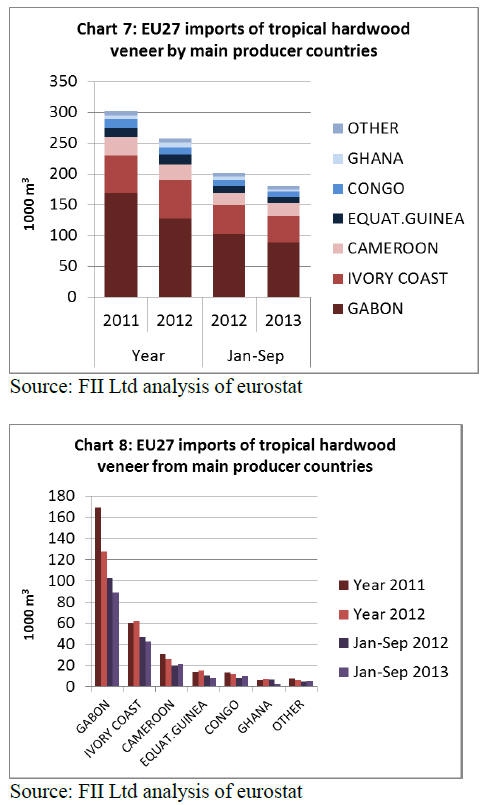

EU imports of plywood faced with other (non-tropical)

hardwoods have also been declining this year. Imports of

this commodity were 1.39 million cu.m in the first 9

months of 2013, 5.1% down on the same period in 2012

(Chart 3).

Imports from China during the January to September 2013

period were 632,600 cu.m, 10.8% less than in the first nine

months of 2012.

This decline was partly offset by a 5.3% rise in imports

from Russia to 517,000 cu.m (Chart 4). A slight rise in

imports by Germany, Poland, Italy and France was

insufficient to offset a decline in imports by the UK and

Belgium.

Slight upturn in European demand for Malaysian

plywood

While imports of Malaysian plywood into the EU declined

during the first nine months of 2013, recent reports

suggest a slight upturn in demand in the last quarter of the

year.

This is particularly true of the UK, Germany and Belgium.

Demand in the Netherlands and France has remained slow.

The short-term increase in demand has contributed to

lengthening delivery times for Malaysian plywood into

Europe. As for Chinese plywood, volatile container rates

have led to significant variations in CIF prices for

Malaysian plywood delivered to Europe in recent months.

However FOB prices have remained quite stable.

Prices for Malaysian plywood are typically up to one third

higher than prices for Chinese substitutes. However, there

is rising interest from importers seeking products

guaranteed to meet European technical performance

standards.

Enforcement of the EU Construction Products Regulation

(CPR) from 1 July 2013 means that CE-Marking

demonstrating conformance to the EN13986 standard is

now mandatory for all plywood used in structural

applications in the EU.

Importers have also been keen to beat the rise in import

duties on Malaysian plywood following the change in GSP

status on 1 January 2014.

European market for okoume plywood still very slow

Expectations that orders for okoume plywood

manufactured in Gabon might pick up in the second half

of 2013 in advance of the rise in import duties from 1

January 2014 have not been realised.

Demand for okoume plywood in Europe remains very

weak with slow buying in both the French and Dutch

construction sector.

There has also been little or no recovery in demand for

okoume plywood from the Italian boat manufacturing

sector this year. Margins in the European okoume

plywood manufacturing sector are extremely thin. In the

face of slow demand, French manufacturers have been

unable to raise selling prices.

Despite low demand, delivery times for okoume plywood

into the EU market have been increasing due to log supply

and transport problems in Gabon over the summer months

and a significant reduction in production both in Europe

and Gabon.

This is particularly true of FSC certified products for

which there is slightly firmer demand since

implementation of the EU Timber Regulation in March

2013.

Robust demand for Russian birch plywood

EU imports of Russian birch plywood have been higher

during 2013 than in 2012. This is despite widespread

reports of supply shortages due to limited log supply in

Russia and rising demand in Russia��s domestic market and

in Turkey, Asia, and in the Middle East.

This in turn has led to long lead times on new orders and

delays to existing orders. Delivery periods for rough

plywood now extend up to 2-3 months.

However availability of Russian film and mesh faced birch

plywood is better and delivery times are shorter. Russia's

exclusion from the EU's GSP on 1 January 2014 has

encouraged some increased buying in the last quarter of

2014 in anticipation of the rise in import duties.

China and Brazil increase share of EU softwood

plywood imports

EU imports of softwood plywood were 1.01 million cu.m

in the first 9 months of 2013, 3.6% down on the same

period in 2012 (Chart 5).

Imports from Brazil during the January to September 2013

period were 680,100 cu.m, 1.8% more than during the first

nine months of 2012.

Imports of softwood plywood from China also increased

during this period, by 10.2% to 123,100 cu.m. However,

imports from Chile declined by over 27% to 104,200 cu.m

(Chart 6).

A rise in softwood plywood imports by Germany, the UK,

and Belgium was insufficient to offset a larger decline in

imports by Italy, Denmark and the Netherlands.

Prices for Brazilian elliotis pine plywood on offer to EU

importers have risen $10-15/cu.m in recent months,

mainly in response to good demand in Brazil and US,

Mexican and Caribbean markets and to rising freight costs.

Flooding in southern Brazil during September led to a

short-term increase in delivery times during the autumn

months.

Higher prices also led to reduced orders from some

European importers concerned about the difficulty of

passing on increased prices to customers at a time when

European consumption is still quite slow.

Nevertheless, there are reports of reasonable European

forward orders for delivery in January under the 2014

quota.

TTJ reports firm plywood demand in the UK

The UK Timber Trade Journal��s latest plywood market

report for the UK suggests that demand in the country is

now �Dfirm�� and product from most sources is attracting

stable to rising prices.

Forward ordering is patchy, but consumption is reasonable

and there is rising optimism about the future. Most

importers are still mainly topping up stock, but more

regular monthly orders are now coming through. UK

importers expect that total sales in 2013 will be slightly

better than in 2012.

EU tropical hardwood veneer imports down 10%

EU imports of hardwood veneer have been declining this

year. Imports of tropical hardwood veneer in the first nine

months of 2013 were 180,800 cu.m, 10.2% less than the

same period in 2012 (Chart 7).

During the period, imports from Gabon fell 13% to 89,100

cu.m. Imports from Ivory Coast were down 9.5% at

42,700 cu.m. These losses were only partly offset by a rise

in imports from Cameroon, up 7.3% at 21,500 cu.m (Chart

8).

In the first nine months of 2013, imports of tropical

hardwood veneer into France declined 14.9% to 75,100

cu.m. Imports into Spain fell 12.1% to 24,100 cu.m.

However, after a very weak year in 2012, there was a

17.7% rise in imports by Italy in the first nine months of

2013 to 41,100 cu.m.

The decline in EU imports of tropical hardwood veneer is

partly due to weak demand in end-use sectors for

decorative sliced products. Sales to the European door and

furniture manufacturers have been weak all year. There

has also been only slow demand from large interiors

projects, such as hotel, shop and bank refurbishment.

While sales of sliced veneers to board manufacturers and

higher value speciality sectors, such as automobile and

yacht manufacturing have been more stable, these have

been insufficient to offset the decline in the larger

industrial sectors.

In fact rising sales to veneered board manufacturers may

be partly at the expense of direct sales of veneers to

joiners. Prices for sliced veneer are coming under intense

pressure in the European market.

The market situation is little better for rotary tropical

hardwood veneers used for plywood and flooring

manufacturing in Europe. Market conditions in the

European engineered wood flooring sector remain weak

and there is a continuing trend to substitute tropical woods

for alternative materials.

There is also limited demand for veneers in the European

okoume plywood manufacturing sector now that capacity

is much reduced, particularly following the closure of

France-based producer Plysorol in 2012.

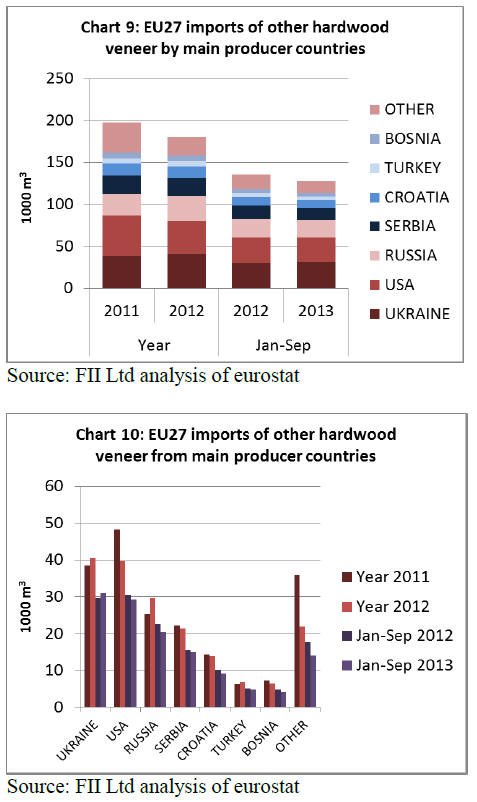

EU imports of temperate hardwood veneer in the first nine

months of 2013 were 127,900 cu.m, 5.9% less than the

same period in 2012 (Chart 9). Due to recent inward

investment, Ukraine is becoming a more important

external supplier of hardwood veneer to the EU.

According to UNECE Timber Committee data, veneer

production in the Ukraine has been rising in recent years

and the country is exporting a wide range of sliced, rotary

and reconstituted (fine-line) veneers into the EU. During

the first nine months of 2013, imports from Ukraine were

31,100 cu.m, 4.7% up on the same period in 2012.

Meanwhile, EU imports of temperate hardwood veneer

fell from the USA by 4.3% to 29,200 cu.m and from

Russia by 9.2% to 20,400 cu.m (Chart 10). Temperate

hardwood veneer imports have been rising into Germany,

Austria and Poland this year, but falling into Italy and

Spain.

|