Japan Wood Products

Prices

Dollar Exchange Rates of

10th February 2014

Japan Yen 102.27

Reports From Japan

Domestic demand expected to maintain strength

despite tax increase

The Deputy Governor of the Bank of Japan, Kikuo Iwata,

recently presented the Bank‟s view of prospects for the

economy at a meeting with business leaders in Miyazaki

prefecture.

See:

https://www.boj.or.jp/en/announcements/press/koen_2014/

data/ko140206a.pdf

He reiterated the Bank‟s view that aggressive quantitative

easing is the way to support the government‟s efforts to

pull the Japanese economy out of deflation.

He repeated that the aim of the Bank is to achieve a 2

percent year on year increase in the consumer price index

(CPI) and that the Bank will continue with the quantitative

easing as long as necessary to achieve the 2% target. The

Bank of Japan has been steadily increasing the monetary

base, mainly through the purchase of long-term Japanese

government securities.

Looking ahead, the Deputy Governor said “Domestic

demand is likely to maintain firmness and external

demand is expected to increase, albeit moderately”.

Against this backdrop, while the economy will continue to

improve a short term decline can be expected after the

consumption tax increase.

At the monetary policy meeting held last month, the Bank

reviewed its outlook for economic activity and prices

through to the end of fiscal 2015. The median Policy

Board forecasts are for real GDP growth rates to be 2.7%

in fiscal 2013, 1.4% in fiscal 2014, and 1.5% in fiscal

2015.

Efforts to generate inflation are working

Data from Japan‟s Finance Ministry indicates that in

December 2013, inflation accelerated, industrial output

expanded and demand for workers increased which

suggests the current fiscal initiatives of the government are

having a positive effect in the real economy.

Another positive sign was that industrial production rose

in December last year.

The most immediate test of business confidence going

forward into 2014 will come when the annual wage

negotiations are concluded and when the impact of the

April 1 consumption tax increase can be assessed.

If workers cannot secure wage increases then inflation will

eat into family disposable incomes driving down domestic

demand. At the moment Japan's economy is showing

remarkable improvement and a strength not seen for years.

The question is how consumers are going to respond over

the next few months?

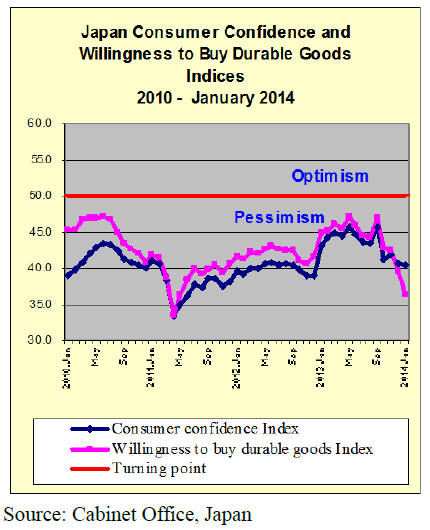

Consumer confidence falls

Japan‟s Cabinet Office has released the results of the

January 2014 Consumer Confidence Survey.

Householder confidence slipped for a second consecutive

month with the consumer index dropping from 40.6in

December to 40.4 in the January survey.

Among the sub-components of the index, the overall

livelihood index fell and the assessment of income growth

potential also fell. The index for consumer willingness to

buy durable goods was down sharply (Dec. 2013, 39.6 to

36.4 in Jan. 2014).

Overall most households surveyed were pessimistic on

three of the four factors assessed: economic well-being,

income growth and purchasing of durable items. Rather

surprisingly, consumers were optimistic on job prospects

an upward trend recorded for three months.

For the complete data see:

http://www.esri.cao.go.jp/en/stat/shouhi/shouhi-e.html

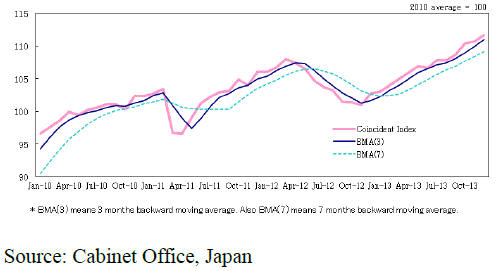

Japan composite index improves

The key indicators of the current state of the Japanese

economy released by the Japanese Cabinet Office all

improved in December and moved to the highest level in

more than five years. Companies have increased output

and are beginning to offer more jobs as they see profits

improve.

The index of coincident indicators comprising industrial

output, retail sales and new job offers, climbed 1.0 point

from the previous month to 111.7, up for the fourth

straight month (100 = base line 2010). The December

results are the best since 2008, prior to the global financial

collapse.

The index of leading indicators, which offers a window on

developments over the next few months also improved in

December, moving up to 112.1 driven by more confidence

in the private sector.

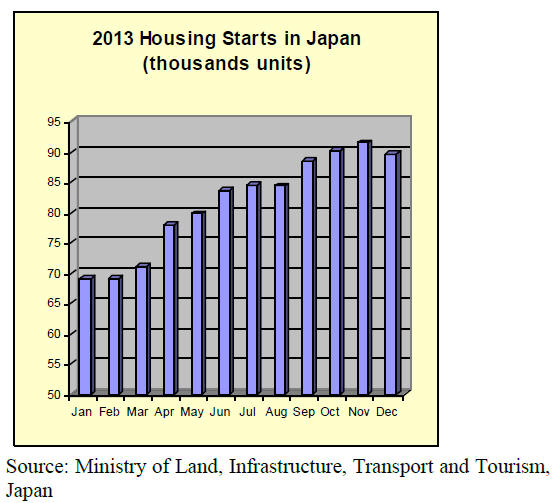

Impressive growth in housing starts

According to a report released today by the Ministry of

Land, Infrastructure, Transport and Tourism Japan‟s 2013

housing starts were up 11% from 2012 a record pace of

increase not seen since the mid 1990‟s.

Housing starts in December were 89,600 down from the

91,500 in November but some 18% higher than in

December 2012. The decline in December is the result of

the slow-down in construction because of the weather,

especially in the northern prefectures and because of the

end of year holidays.

Japan‟s housing starts rose for a 16th consecutive month in

December 2013, the longest consistent improvement since

1994.

While consumer optimism is growing much of the

increase in housing starts is in response to the planned

increase in consumption tax due to take effect in April this

year. Analysts expect housing starts to peak in March and

then fall back as the new tax regime comes into effect.

Overall housing starts in Japan in 2013 were 1.06 million

units slightly above earlier forecasts.

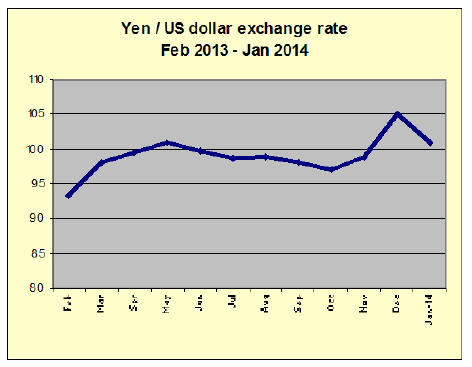

Yen exchange rate reacts to emerging economy

difficulties

Forecasts are for the yen to stabilise at around yen 100-

110 to the US dollar throughout 2014 but the mixed

signals from the US Federal Reserve and the instability of

emerging market currencies will tend to strengthen the yen

higher. In mid February 2014 the yen was trading at

around 101 to the dollar.

The economic problems in emerging economies are

undermining the weak yen policy of the Japanese

government and Central Bank. If demand in emerging

markets weakens significantly there will be a direct and

negative impact on Japanese exports.

Around half of Japan‟s exports go to emerging markets

including China (20%) which rises to almost 30% if Hong

Kong and Taiwan P.o.C markets are included. Any decline

in imports from these and other emerging markets would

seriously undermine the efforts of the Japanese

government beat deflation.

Jetro survey of Japanese firms overseas

Between September 13 and October 23 2013, the Japan

External Trade Organization (JETRO) conducted its latest

survey on the business operations of Japanese-affiliated

firms in the five countries in Africa where JETRO offices

are located (South Africa, Egypt, Kenya, Nigeria and Cote

d'Ivoire.

More than half the Japanese companies surveyed forecast

an upturn in business with Africa and 60% of companies

surveyed expect to expand sales in African markets.

However respondents noted “the business environment in

Africa remains harsh with political and social instability,

employment and infrastructure being the main issues of

concern.

Interestingly most respondents located overseas cited

insufficient understanding by and poor communication

with corporate headquarters as the greatest problem.

For more information please see:

https://www.jetro.go.jp/en/news/announcement/20140206

116-news

Workforce reform- more foreign workers to come

The Japanese government is making it easier for the

private sector to recruit foreign workers for highly-skilled

positions and as trainees a move which, say analysts, will

help offset the shrinking domestic workforce and will

support expansion of the economy.

This move comes on the heels of a decision to encourage

and support expansion of the female workforce. To

encourage qualified and skilled mothers to return to work

the government is strengthening the child care system and

is setting voluntary targets for female worker employment

by companies.

The domestic workforce in Japan is shrinking as the

country has the most rapidly aging society in the world,

with a quarter of the population already over 65.

Expansion of the foreign workforce and getting more

women employed or re-employed is important for easing

labour shortages and increasing tax revenues.

Trade news from the Japan Lumber Reports (JLR)

The Japan Lumber Reports (JLR), a subscription trade

journal published every two weeks in English, is

generously allowing the ITTO Tropical Timber Market

Report to extract and reproduce news on the Japanese

market.

For the JLR report please see:

http://www.nmokuzai.

com/modules/general/index.php?id=7

North American log import in 2013

Total import of North American logs in 2013 was

3,415,440 cbms, 14.4% more than 2012. Demand for

North American logs increased by both lumber and

plywood for busy housing starts.

Also the supply of North American lumber did not cope

with expanding demand in Japan so that the demand

shifted to domestic products. The cost of North American

lumber climbed due to weakening yen.

Lumber shipment by Chugoku Lumber, the largest

Douglas fir lumber manufacturer in Japan in 2013 was

1,440 M cbms, 19% higher than 2012, which verifies

aggressive log demand.

Domestic wood products market in Tokyo region

Market prices of domestic lumber in Tokyo region

continue climbing. All the sawmills are running full to

catch up orders but the demand is expanding much larger

than the supply capacity so the supply shortage seems to

continue for some time.

However, there are some changes by users to shift to

imported products after the prices of domestic lumber

soared so much then log inventories by sawmills are ample

now so that the market feels the prices are peaking and the

concern is how long the market holds high prices.

The prices of KD cedar 120 mm post (special grade)

leaped to 65,000-67,000 yen per cbm, 10,000 yen up from

early December, of KD cypress sill jumped up to 90,000-

95,000 yen, 20,000 yen up, of KD cedar stud climbed to

65,000 yen. The prices are up by about 40% to 50%

compared to last summer.

Wood demand projections from Forestry Agency

The Forestry Agency held meeting for wood products

demand projection in December last year. It drew up

demand projection for the first quarter and second quarters

of this year. According to this, the first quarter would stay

without much change but the second quarter would drop

related to the end of rush orders in late last year.

Projections of domestic logs for lumber production in the

first quarter are 3,090,000 cbms, 4.1% more than the first

quarter last year then for the second quarter are 3,040,000

cbms, 2.4% less. Logs for plywood for the first quarter are

740,000 cbms, 2.9% more then the second quarter are

750,000 cbms, 5.2% less.

Total for the first quarter is up by 3.9% then for the second

quarter is down by 2.9%.

Imported logs for the 1st quarter are 1,105,000 cbms, 1.2%

down then for the 2nd quarter are 1,095,000 cbms, 14.6%

down. Imported lumber for the 1st quarter is 1,695,000

cbms, 1.4% down then for the 2nd quarter is 1,800,000

cbms, 14.8% down.

Drop of both logs and lumber for the 2nd quarter is larger

than the 1st but this is due to large volume for the 2nd

quarter last year and the volume of logs remain unchanged

from the 1st quarter and lumber volume actually increases

for the 2nd quarter.

As to North American lumber, import of the 1st quarter

would increase by 2.2% because of declining inventories

but the 2nd quarter would drop by 10.6% by declining

demand.

European lumber, which inventory is high, would drop by

7.4% in the 1st quarter and by 21.2% in the 2nd quarter.

Radiata pine logs and lumber would increase as export

cargoes would grow.

Both domestic and imported structural laminated lumber

would increase for the 1st quarter with 535,000 cbms,

7.9% up then drop in the 2nd quarter with 540,000 cbms,

7.9% down.

Domestic plywood would increase for both 1st and 2nd

quarter by 9.0% and 2.3% but the imports would decrease

so total would be 1,570,000 cbms for the 1st quarter (1.1%

down) and 1,590,000 cbms for the 2nd quarter (5.6%

down).

Forecast of the seasonally adjusted annual housing starts

are 997,000 units for the 4th quarter 2013, 925,000 units

for the 1st quarter and 859,000 units for the 2nd quarter.

European lumber market

Market of redwood laminated beam and whitewood post

has been tightening after the inventories of imported

products are dropping by active operations by precutting

plants so that now the orders are coming to domestic

laminated lumber manufacturers. With brisk orders, the

plants are so busy that deliveries take more than a month.

The manufacturers are aggressively seeking to increase the

prices but at the same time, they are afraid of demand slow

down after the first quarter.

Radiata pine logs and lumber

Crating lumber market is tightening after Orvis, the largest

radiate pine lumber manufacturer, announced to close its

Himeji mill in April.

Lumber buyers place orders to multiple suppliers so that it

is much larger than actual demand. Also lumber buyers

want to procure before the consumption tax is increased in

April.

Radiata pine sawmills carry order balance for about a

month then competing domestic larch and cedar plants

also have order files of more than two weeks so the supply

is tight.

The market prices are firming after both New Zealand logs

and Chilean lumber export prices are up. New Zealand A

sort log prices for January shipment were $5 per cbm C&F

up and further increase is likely.

Chilean lumber suppliers proposed higher prices and the

negotiations had tough going but final settlement was $5-

10 up for February shipment.

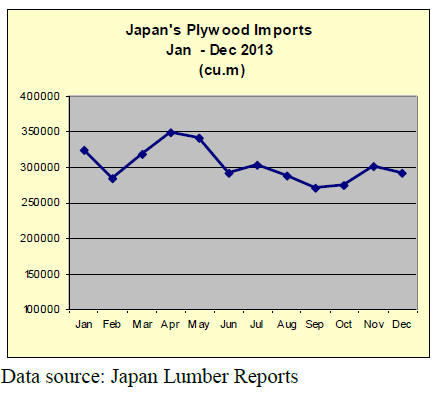

Plywood

Supply of domestic softwood plywood continues tight.

Orders by precutting plants are brisk as their February

orders are all filled up.

Meantime, plywood manufacturers produced 226,500

cbms in December, 12% more than December last year

despite shorter operating days then the shipment was high

at 226,600 cbms, 7.4% more.

The inventories were 119,000 cbms, 2.3% less than

November, the lowest in 2013.

The market prices are 980-1,000 yen per sheet delivered

on 12 mm 3x6, 20 yen up from November, 1,450 yen on 9

mm 3x10 long panel and 1,950 yen on 24 mm 3x6 thick

panel. Both are flat.

Market of imported plywood continues firm with tight

supply. Both 3x6 JAS concrete forming for coating and 9

and 12 mm structural panel are particularly tight. Future

seems high due to higher export FOB prices by the

suppliers and weakening

yen so that wholesalers are aggressively procuring what‟s

available now.

The prices seem to continue edging up without support by

actual demand. Market prices are hard to pin point as there

is gap between importers‟ asking prices and wholesalers‟

desirable prices. Concrete forming JAS 3x6 panel prices

are 1,250 yen per sheet delivered, 50-70 yen up from

December. 12 mm structural panel prices are 1,320 yen,

70-90 yen up. 3x6 JAS concrete forming panel for coating

is 1,350 yen, 50 yen up.

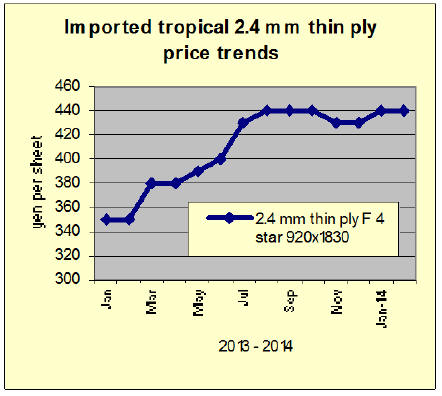

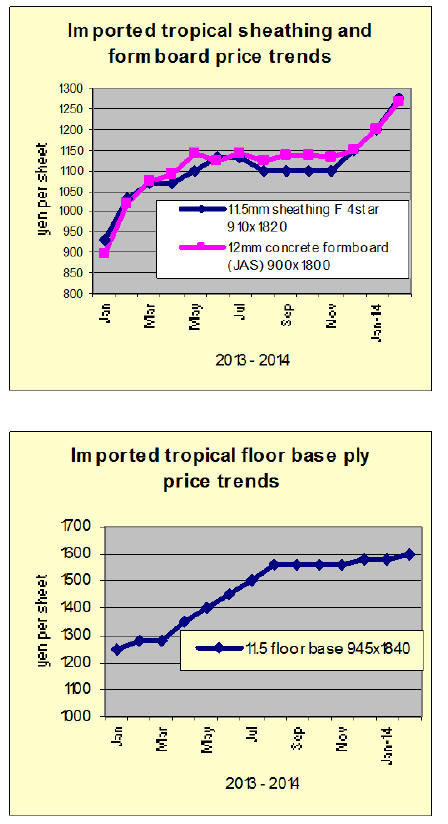

Price trends for Japanese imports of Indonesian and

Malaysian plywood

Certified wood for the 202 Olympics

Two major forest certification organizations, FSC, PEFC

and the Japanese own organization, SGEC (Sustainable

Green Ecosystem Council) have started activities to

promote using certified wood for the Olympic Games held

in Tokyo in 2020.

This is the first such joint activities by three corporations.

Three corporations had several meetings since last fall and

came up with the request to use forest certified wood for

athletic and related facilities of the Olympic and submit

the request to administrative organizations.

Vancouver winter Olympic in 2010 was the first Olympic

to use certified wood then in London Olympic games in

2012, for the request to use sustainable wood and paper for

consumption by organizing committee, FSC and PEFC

were selected. Consequently total of 12,500 cubic meters

of wood was used for various facilities and almost 100%

was certified wood.

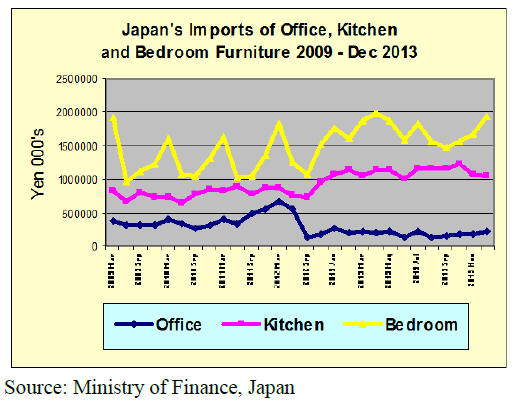

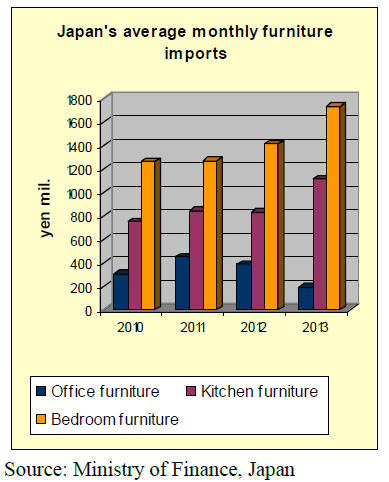

Trends in office, kitchen and bedroom furniture

imports

Japan‟s office kitchen and bedroom furniture imports from

2009 to the end of 2013 are shown below. Imports of

bedroom furniture exhibit a cyclical trend and between

2009 and 2011 monthly imports followed much the same

pattern but overall annual imports did not increase during

this period. However from 2012 bedroom furniture

imports began to increase and the established cycle

changed as monthly imports tended to level out such that

the difference in value between the highs and lows

narrowed.

2012 bedroom furniture imports averaged yen 1,414 mil.

and were up 12% on 2011 levels while imports in 2013

averaged yen 1,727 mil. and expanded 22% compared to

2012.

In contrast to the pattern of bedroom furniture imports in

the case of kitchen furniture imports there has been a

steady rise beginning from 2011. 2012 imports of kitchen

furniture were affected by the weak Japanese economy

much more than imports of bedroom furniture and

monthly imports averaged only yen 750 mil in 2010,

expanding to yen 844 mil. in 2011, yen 832 mil. in 2012

and yen 1112 mil. in 2013.

Despite the 2013 improvement in business sentiment in

Japan and greater investment by the private sector imports

of office furniture weakened considerably from levels in

2011 and 2012.

In 2011 office furniture imports were up 46% on 2010 but

from 2012 imports fell steadily. In 2013 average monthly

imports of office furniture were yen 195 mil. compared to

the high of yen 454 mil. in 2011.

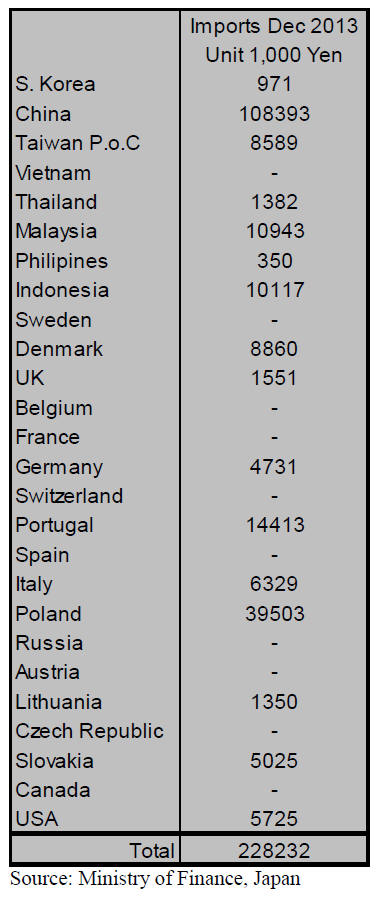

Office furniture imports (HS 9403.30)

In December 2013 Japan‟s imports of office furniture

increased by 23.5% following the 9.5% increase in

November imports. The top supplier remains China which

provided 47.5% of all December imports, marginally

down on the yen 93.3 mil. supplied in November 2013.

The three main suppliers in December, as in previous

months, were China, Poland and Portugal which together

accounted for significantly more of all office furniture

imports in November. Almost all of the increased imports

in December were supplied by these top three suppliers.

For December 2013 Japan‟s imports office furniture from

China were up around 3%, while imports from Poland

almost doubled. Office furniture imports from Malaysia

and Indonesia fell sharply in December as did imports

from Italy.

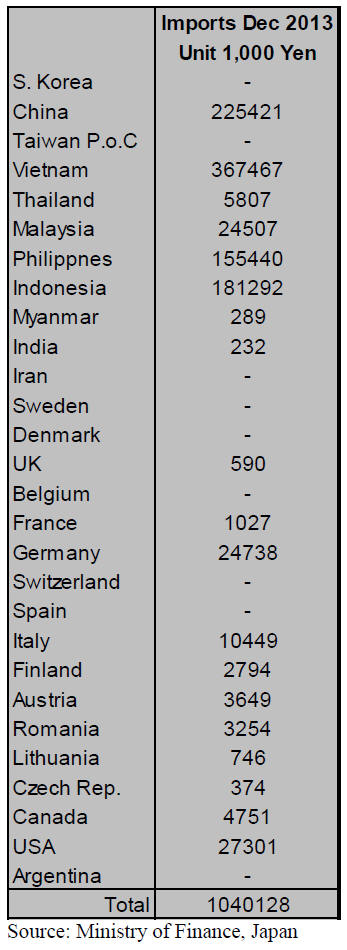

Kitchen furniture imports (HS 9403.40)

In order of value of imports Vietnam, China Indonesia and

Philippines continued to provide the bulk (89%) of kitchen

furniture imported by Japan according to figures from

Japan‟s Ministry of Finance. December 2013 kitchen

furniture imports, at yen 1,040 mil. were down slightly on

November imports. Asian suppliers provided 89% of

Japan‟s kitchen furniture imports in December 2013.

Vietnam maintained its position as the number one

supplier of kitchen furniture by a significant margin

supplying 35% (39% in November 2013) of Japan‟s

kitchen furniture imports.

The other main suppliers were China (21.5%) Indonesia

(17.4%) and Philippines (15%). Imports of Kitchen

furniture from Vietnam in December fell by around 12%

and imports from Indonesia and Philippines also declined.

In contrast, imports from China grew 27%.

Of the non-Asian suppliers Germany replaced Italy as the

number one supplier in December but December imports

were below that in November.

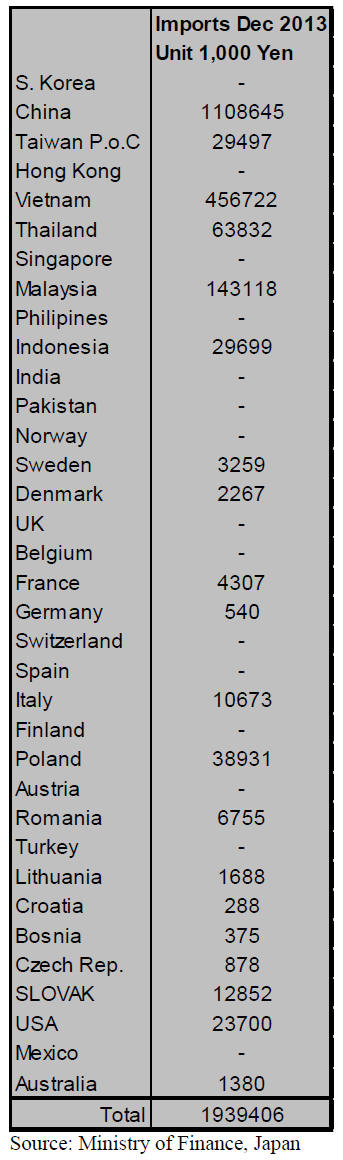

Bedroom furniture (HS 9403.50)

Japan‟s imports of bedroom furniture have steadily

increased throughout 2013 as can be seen from the annual

growth figures illustrated above.

December 2013 imports of bedroom furniture were a

record yen 1,939 mil. up almost 16% on levels in

November. Once again China topped the table of bedroom

furniture suppliers to Japan, providing some 57% of all

bedroom furniture.

Together, China, Vietnam and Malaysia accounted for

most (88%) of all bedroom furniture imports. The rise in

overall imports of this item was largely due to increased

supplies from the top three suppliers.

The other main suppliers were Poland, yen 39.9 mil.;

Indonesia, yen 29.7 mil.; USA, yen 23.7 mil.; followed by

Slovakia and Italy at just over yen 10 mil. each.

|