|

Report from

Europe

Signs of revival in European wooden furniture

manufacturing

The recession in Europe has created many challenges for

the European wood furniture sector. However the sector

remains globally significant as a driver of design and

production innovation.

There are also signs that the international competitiveness

of the European furniture sector is improving.

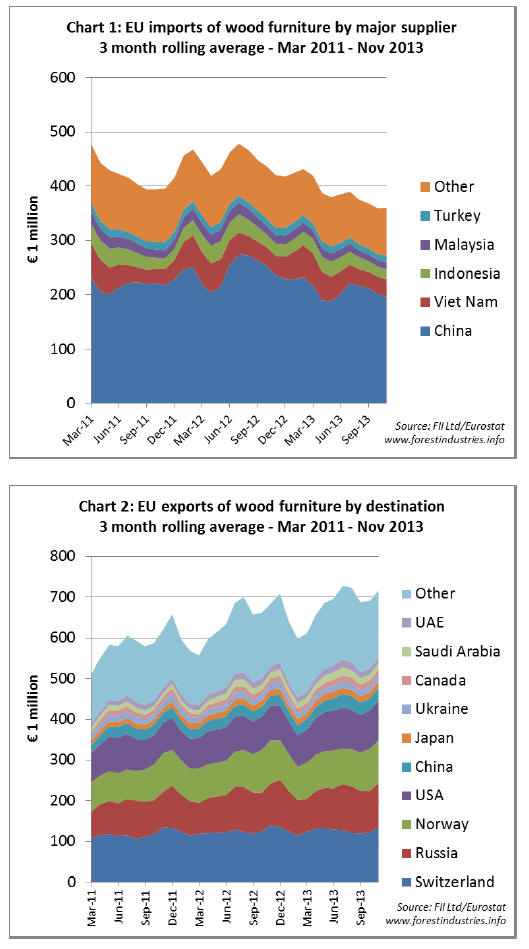

The charts below suggest a significant change in Europe‟s

position in the global market for wood furniture. Chart 1

shows the 3 month rolling average value of EU imports

between the start of 2011 and November 2013.

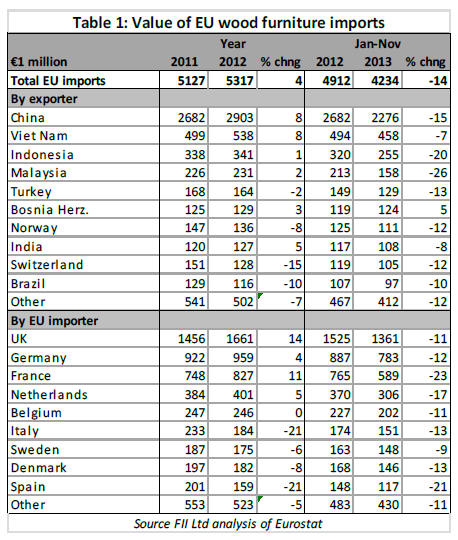

Chart 2 below shows equivalent data on EU exports during

the same period.

The moving average is used to smooth out short-term

fluctuations, which are strongly influenced by factors like

vacations or shipping delays, so that the longer-term trend

becomes clearer.

EU imports of wood furniture have been falling over the

last 3 years (Chart 1) while exports have been rising

(Chart 2).

At the start of 2011, EU net trade in wood furniture was

close to zero, with both imports and exports averaging

close to €500 million per month. However, by the end of

2013, the EU had a trade surplus in wood furniture of

around €350 million per month.

Average monthly imports of wood furniture into the EU

had fallen to €350 million while exports had risen to just

over €700 million per month.

These figures should be put into perspective. EU external

trade in wood furniture is relatively small compared to

total consumption, which is about €50 billion per year (or

€4200 million per month). There is much reliance on

domestic manufacturers.

Only about one quarter of wood furniture consumed in EU

countries ever crosses a national boundary. Total internal

trade in wood furniture between EU countries averages

around €1200 million per month.

Trade statistics and anecdotal reports suggest that the level

of EU consumption and internal trade in wood furniture

have been static at a low level since 2009 when there was

a steep decline during the financial crises.

While external trade forms only a small part of the EU

furniture sector, it is becoming much more relevant to

European furniture manufacturers. During the recession,

manufacturers have become more focused on improving

competitiveness relative to manufacturers in other

countries, particularly China.

With consumption static in domestic markets, European

furniture companies are seeking to increase sales in other

parts of the world.

This more outward looking strategy seems to be working

for EU manufacturers. Exports of wood furniture are

rising, particularly to Russia, North America, China, and

the Middle East.

The rise in exports is being led by manufacturers in Italy,

Germany and Poland (see Table 1). Meanwhile EU

imports of wood furniture have been falling, a trend which

strengthened in 2013 and affected all the main external

suppliers including China, Viet Nam, Indonesia, Malaysia

and Turkey (see Table 2).

Overall these trends suggest a revival in the relative global

competitiveness of European wood furniture

manufacturers over the last 3 years.

Strong global influence of large EU furniture

manufacturers

The latest edition of World Furniture

(www.worldfurnitureonline.com), the quarterly journal of

the Italian furniture industry research association CSIL,

includes an overview of production trends in the European

furniture sector.

CSIL note that profits have declined and the total value of

European furniture production has been static for a decade

(or even decreased in some countries). However CSIL also

highlight the strong global influence of Europe.s largest

furniture companies.

Following the recent rapid growth in emerging markets,

particularly China, the EU now accounts for one quarter of

the world.s furniture production and consumption. EU

share of world furniture production has contracted over the

last decade so that the total value of production in the EU

in 2012 was no more than ten years previously.

Total EU furniture sector turnover in 2012 was ��100

billion, just over the peak of 2008. European furniture

industry profits after tax and net income have reduced by a

cumulative 30% over the last 5 years.

However these trends are partly offset by a rise in

furniture production in plants operated by European

companies in other parts of the world. European furniture

companies continue to play a leading role in the

international market.

Europe is home to 84 of the world.s Top 200 furniture

manufacturers. These companies are mainly located (in

order of importance), in Germany, Italy, Sweden, France,

the UK, Poland, Finland, the Netherlands, Austria,

Denmark, Lithuania, Spain and Romania.

Although in terms of numbers, around 85% of European

furniture companies are micro enterprises with less than

10 employees, the leading European companies are very

large.

The 100 largest companies in Europe have a total turnover

of ��20 billion and average of ��150 million. Together these

100 companies account for around 20% of the EU

furniture sector turnover. Their productive presence now

includes numerous plants outside the EU, notably in

China, Russia, Ukraine, Belarus and USA.

Europe's large furniture companies have adopted various

strategies to improve competitive during the European

financial crises.

These include downsizing (with plant closures and layoffs),

increasing production efficiency, increased sourcing

from Asia, strong investment in existing and new retailing

formats (including in emerging markets) and a strong

focus on brand development.

As a result, despite the recession in domestic markets,

European manufacturers have retained their global

leadership in furniture design and production innovation.

European furniture manufacturers go east

CSIL report that around 80% of EU furniture production

value in 2012 was in Western Europe (EU15 group of

countries). This is down from around 90% a decade ago.

However, these figures omit the rising value of production

by Western European companies in plants outside the

region.

Weak European consumption has meant that Western

European companies now focus heavily on expansion of

exports to fast growing emerging markets.

Germany has the best performing furniture sector and

recently overtook Italy as the largest European furniture

producer (in terms of value).

Germany now ranks as the world's third largest furniture

producer after China and the United States. It is also the

second largest exporter after China. According to Eurostat

data, Germany is host to over 9,000 furniture

manufacturing companies.

The furniture sector in Italy, comprising 20,000 mainly

small furniture companies, is more fragmented than in

Germany. These companies are concentrated in several

regional clusters in Italy.

The performance of these clusters has varied widely in

recent years depending on product specialisation and their

diversity of export markets.

Rapid production growth in Poland

Production value in the EU13 group of Eastern European

countries increased 50% between 2002 and 2012. This

region now accounts for 20% of total EU production

value. Production growth has been particularly rapid in

Poland, Romania, Lithuania and Slovakia.

Furniture production in this region has always been more

export-oriented than in Western Europe. By combining

relatively cheap labour with proximity to European

customers, furniture production in these countries has

risen alongside the on-going process of EU eastern

expansion and market integration.

Poland is by far the leading furniture exporter in Eastern

Europe with over ��6 billion in 2012. Exports accounted

for as much as 79% of Poland.s production value in 2012.

Poland is also increasingly influential in the global

furniture industry. In 2012, it was the world.s 7th largest

manufacturer (up from 12th in 2002) and the 4th largest

exporter (up from 5th in 2002) after China, Germany and

Italy. As in Italy, production in Poland is highly

fragmented.

There are almost 24,000 furniture manufacturers in the

country mainly concentrated in the Wielkopolskie,

Mazowieckie and Malopolskie regions.

Romania is the second largest furniture producer in the

EU13 group of countries, although production of ��1.5

billion in 2012 was only a quarter of that in Poland.

Furniture production in Romania expanded at an average

annual rate of 6.3% between 2002 and 2012. Exports

account for 88% of production and have driven this rapid

growth.

The Czech Republic is the third largest producer of

furniture in the EU13, with production value of ��1.4

billion in 2012. The country has around 500 producers,

mostly locally owned with lower levels of foreign

investment than in other parts of the region.

Lithuania is now the fourth largest furniture manufacturer

in Eastern Europe, with production value rising by 400%

between 2002 and 2012, notably due to large investments

by the Swedish giant Ikea.

Ikea reports strong market growth in China, Russia

and US

The 2013 financial report for the Ikea Group, the world's

largest furniture retailer, provides insights into the outlook

for the international furniture sector.

In the financial year 2013 (to 31st August 2013), Ikea's

sales increased 3.1% to ��27.9 billion and profit also

increased by 3.1% to ��3.3 billion. Market conditions

continued to improve, reports the retailer, with strong

growth in China, Russia and the US.

Ikea reports that "Consumer spending is improving in

many countries. While the challenging economic situation

may not be over, there are positive signs. Important

consumer markets such as the US are coming back and

Europe in general is starting to recover.

Even some of the challenging markets in Southern Europe

are showing good signs of activity.�� The Ikea Group

claims to have gained market share in almost all markets.

The largest markets were Germany, the US, France,

Russia and Sweden. Ikea, which specialises in large

volume sales of low priced furniture, suggests "this

indicates that value for money is increasingly important".

The Ikea Group has an ambitious growth agenda, aiming

for ��50billion in sales by 2020. It states that the large

emerging markets are important sources of future growth.

In FY13, the Ikea Group opened two more stores in China

. another step in expansion in the Chinese market. Ikea's

long-term focus is to "keep developing better products at

lower prices, improving the shopping experience and

becoming more accessible to our customers, for example

through an improved service offer, e-commerce and

continued expansion".

European furniture shows highlight continuing strong

fashion for oak

A recent report from the American Hardwood Export

Council (AHEC) reviews fashion trends based on visits to

European furniture shows. AHEC note that there are three

high profile furniture shows in Europe. The imm show in

Cologne, Germany and Maison Objet in Paris take place in

January, while the Salone del Mobile is held in Milan,

Italy in April.

All attract an international audience both in terms of

visitors and exhibitors. However, exhibitors often have to

choose between the Cologne and Paris as they are held

within only a few weeks of each other.

The Cologne fair is more traditional and is of particular

focus for companies selling into the German market and

other Central and Northern EU countries. But as with all

the big European shows there are always plenty of visitors

from outside Europe.

Based on their visit to imm Cologne, AHEC suggest

contemporary design furniture has a much greater

representation than in the past. Traditional and

reproduction furniture is shown but does not dominate.

The exhibition is a platform for leading brands and

individual designers targeting the higher end of the

market. As a result, quality materials are used.

There was a lot of real wood on display, often in

combination with other materials.

It is hard to quantify, but AHEC suggest that real wood

was more prominent than in previous years and there were

fewer paper foil and vinyl finishes. This suggests the

higher end of the European furniture sector is still an

important source of demand for hardwood.

According to AHEC, contrasting colours is a very obvious

trend at the moment, and many manufacturers are using

the natural tones of wood to contrast with bright colours.

White with wood also seemed a particular theme for many

brands this year.

The vast majority of the wood was temperate hardwood;

there were relatively small amounts of tropical hardwood

or softwood species on show.

The dominant species was oak, but ash was also common,

a little beech and quite a lot of walnut, most of which was

American. AHEC report that the trend for a natural rustic

look has grown in recent years. It is now common to see

leading brands offering expensive designer collections

with ��character�� solid oak.

This oak contains grain and colour variations and even

sometimes knots. Most of the character oak was from

Europe. European producers are favouring European oak

because they can source short dimensions and low grades

more cheaply than white oak from the USA. For the

cleaner more consistent look, manufacturers use mostly

veneered panels for the surfaces but solid for legs, rails

and chairs.

AHEC also note that at Cologne there was quite a lot of

bent wood being used in the contemporary chair design

especially ash which lends itself to this application, but

also beech and some oak. One new trend this year was the

use of heat treated hardwoods - European and North

American - for outdoor furniture.

According to AHEC many of the wood trends apparent in

Cologne were reinforced at Maison Objet in Paris. At this

show, oak was by far the dominant wood material for both

furniture and flooring. Flooring manufacturers exhibited

oak in hundreds of different finishes and colours. Furniture

and interior fittings in pale oak were very popular and

often contrasted with other materials such as fabrics or

metals in bright colours.

The Paris show also highlighted the continued fashion for

„streamline‟ designs �C tables with very thin legs and backs

and tables with wafer-thin tops. For higher end products,

many manufacturers were using American walnut which

remains very popular for luxury goods. Many companies

at the show reported that their production is now based in

China, Vietnam, Poland and Romania.

Chinese products increase market share in the UK

The new Statistics Digest issued by the UK Furniture

Industry Research Association (FIRA) at the end of 2013

suggests a small recovery for furniture manufacturing in

the UK.

However the sector continues to suffer from loss of market

share to Chinese product in the domestic market and poor

export market performance. The report indicates that the

UK furniture sector manufactured £6.5 billion of product

in 2012.

The significance of imported furniture is reflected by the

fact that, at between £4.3 and £4.5 billion, it comprises

40% of the home market. UK furniture exports, however,

have remained relatively static for many years, and

struggle to reach £1 billion each year.

There were 6131 furniture manufacturers in the UK in

2012. This number has changed little in recent years. The

industry is dominated by micro-businesses and SMEs,

with only 260 companies (4%) operating at turnovers in

excess of £5 million in 2012. 83% of companies turned

over less than £1 million.

A high proportion of UK furniture companies are

extremely small. 58% have annual turnover of less than

£250,000. Furniture manufacturing is quite evenly spread

around the UK, although there is a higher concentration in

London and the South-east which together account for

24% of all UK furniture manufacturers.

Total imports of furniture into the UK decreased from £4.5

billion in 2010 to £4.3 billion in 2011 but then increased

again to £4.5 billion in 2012. The largest external supplier

was China which accounted for 33% of import value in

2012.

Other major suppliers are Italy, accounting for 10% of

import value in 2012, and Germany which supplied 9%.

UK furniture exports increased from £754 million in 2009,

to £993m in 2011, but 2012 saw a reverse in this trend,

with exports falling slightly to £946 million.

The UK has traditionally targeted its exports at the

Republic of Ireland and the USA and this continued to be

the case in 2012 (16% and 13% respectively).

Trade with leading European nations such as Germany,

France, the Netherlands and Belgium was the other main

source of income from exports.

The Statistics Digest also explores trends in the wider UK

economy. Key points include:

Total consumer expenditure in the UK increased

by just over 2% between 2009 and 2012 to over

£920 billion.

Total lending to consumers in the UK has been

increasing slowly. Between 2009 and 2012, total

lending increased by £23 billion to £1475

billion.

However total "unsecured" lending (i.e.

excluding mortgages) of £210 billion in 2012 was

much lower than its peak of £238 billion in

September 2008.

There was a slight upward trend in UK housing

starts between 2008 and 2011 followed by a

slight downturn in 2012. Preliminary indications

are that housing starts increased again in 2013.

While the total number of UK property

transactions gradually increased over the 2009 to

2012 period (by 9%), there was a significant rise

of over 5% between 2011 and 2012. Preliminary

data suggests the rising trend continued in 2013.

FIRA conclude, based on their statistical analysis and

other anecdotal evidence, that furniture consumption in the

UK is recovering slowly.

Consumers are becoming willing to borrow and spend

more money, and housing starts and transactions are up.

However the market remains well below the pre-2008

level and is unlikely to grow rapidly.

* The market information above has been generously provided by the

Chinese Forest Products Index Mechanism (FPI)

|