|

Report

from

North America

Tropical sawnwood imports down in January

Total US sawn hardwood imports increased from 57,396

cu.m in December to 62,602 cu.m in January, the increase

was mainly due to higher imports of temperate species.

Tropical sawnwood imports were 17,299 cu.m in January,

down 10% from December.

Imports from most tropical sawnwood suppliers declined

in January, with the exception of Congo/Brazzaville

(1,287 cu.m), Ghana (729 cu.m), Indonesia (720 cu.m) and

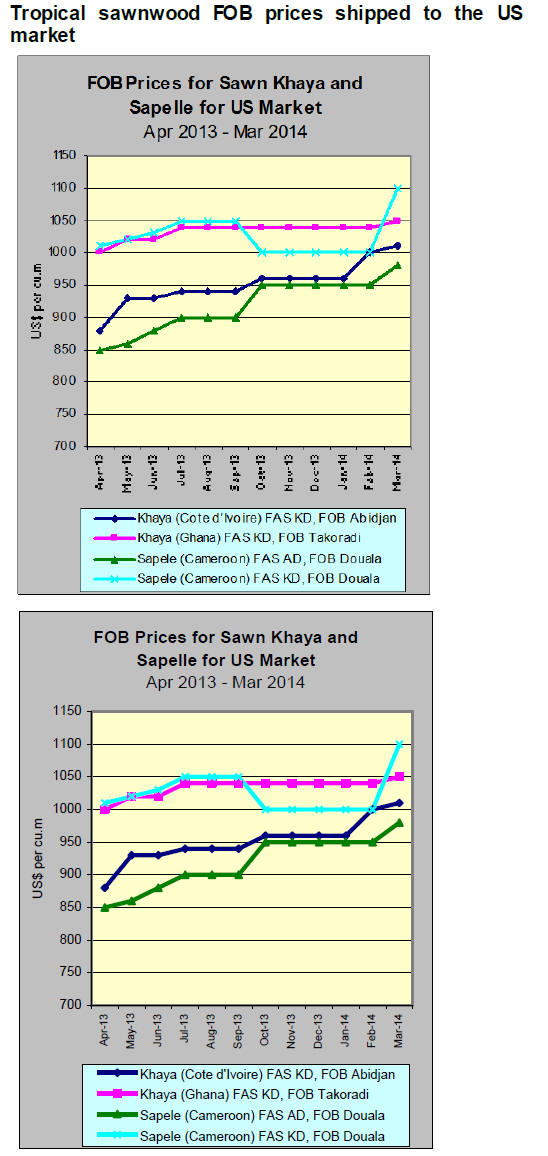

Peru (420 cu.m). Imports from Cameroon fell by 19% to

1,960 cu.m in January, with sapelli accounting for 1,355

cu.m. 834 cu.m of sapelli sawnwood were imported from

Congo/Brazzaville.

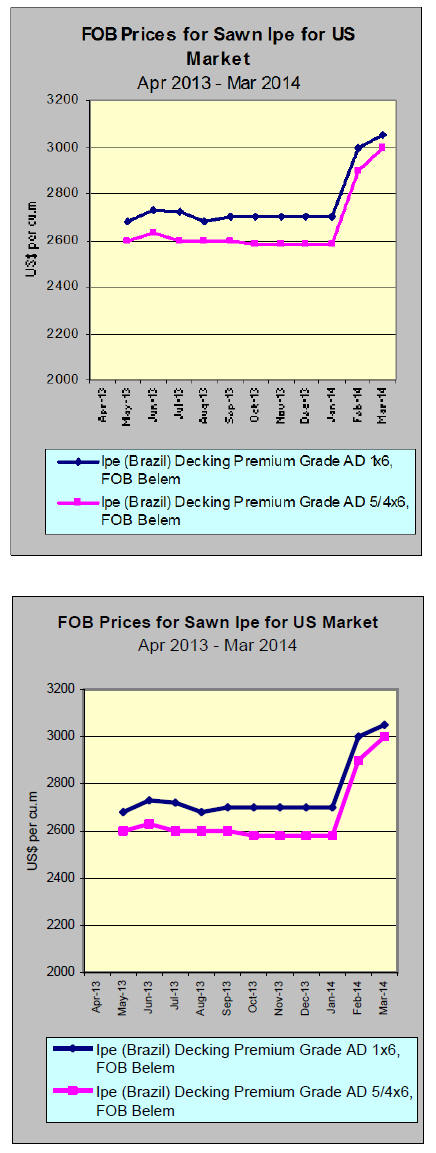

January shipments from Brazil were 3,170cu.m, down

12% from December. Ipe imports from Brazil recovered

slightly compared to the end of last year (especially

September to November) and reached 2,535 cu.m in

January.

January imports of keruing fell a huge 35% from the

previous month. Malaysian shipments were 984 cu.m in

January, while Indonesia exported 177 cu.m to the US in

January.

Imports of most other species also declined, except

mahogany (2,059 cu.m, +12%), meranti (601 cu.m,

+32%), teak (701 cu.m, +84%) and aningre (106 cu.m,

+26%).

Canada imported less from Brazil in January

Canadian imports of tropical sawn hardwood were

US$2.09 million in January, down 16% from December.

However, imports were 9% higher than in January 2013.

The largest drop was in imports from Brazil, which fell by

59% to US$409,594 in January. Imports from Indonesia

increased to US$168,280 (+14%), while there were no

imports from Malaysia in January.

The value of sapelli sawnwood imports by Canada

doubled from the previous month to US$408,353 in

January. Imports of mahogany were worth US$28,159 and

imports of virola, imbuia and balsa were worth a

combined US$336,820.

US importers say ipe supplies are very t ight this year.

Global demand is rising, while supplies of ipe are limited.

This year the rainy season has been longer than usual,

essentially shutting down the flow of ipe from Brazil.

Slightly improved demand in Europe is adding pressure on

supplies and prices.

More manufacturers offering ‘tropical’ look-alike but

non-wood decking

The market share of non-wood materials for residential

decks has grown dramat ically in the last decade. The

materials substituting for wood include wood plastic

composite, PVC and composites capped with a polymer

shell.

Non-wood decking products are popular in northern US

and along the west coast, with market shares approaching

50% in some areas in 2013. In the Southeast wood remains

the most popular decking material, with approximately 80-

90% of all decks are built in wood.

The leading manufacturers of non-wood decking are

increasingly offering products that are made to look like

tropical wood species, perhaps in an effort to gain a larger

market share in the US South.

Home owners in the Southeast prefer dark, tropical colours

in decking according to market information by TREX, the

largest manufacturer of composite decking. Tropical wood

colours and patterns are also popular in Southwestern US,

where composite decking is more established.

Several producers of composite and PVC decking have

introduced tropical look-alike product lines in 2014, such

as AZEK Building Products who announced in March

three ‗tropical‘ colours.

TimberTech (owned by the same company as AZEK)

emulates the look of ipe in its latest tropical collect ion of

capped composite decking. Advanced Environmental

Recycling Technologies (AERT) offers capped composite

decking in the colours ‗Ipe‘ and ‗Bra zilian chestnut‘.

The colour and name choices reflect the popularity of ipe

in the US decking market, and the use of non-wood

decking the US South may increase in part because of

limited ipe supplies from Brazil.

While the construction and renovation market has not yet

fully recovered from the recession, demand for decking

materials is likely to grow substantially in the coming

years. Demand for tropical species is likely to outstrip

supply and drive up prices which will provide market

opportunities for composite decking manufacturers.

Siding market study predicts good demand growth

Siding demand is mainly driven by new home construction

since almost every house and multi-family building in the

US has siding (exterior cladding). In 2013, however, repair

and renovation were the leading markets for siding

because new home construction was still at relatively low

levels.

Freedonia published a siding market study in March

(Freedonia Study 3144) that forecasts an annual growth of

7% in siding demand in the next five years.

Freedonia expects a strong rebound in US housing starts

and in the construction of hotels, resorts, offices and

commercial buildings, which will support demand for

siding.

Non-wood materials have dominated the siding market for

many years now. Wood siding had a market share of less

than 10% in 2013. Vinyl is the leading material with 27%

of the market in 2013, but other materials (brick, stone and

concrete) are expected to gain market share in the next

five years at the expense of vinyl.

|