Japan Wood Products

Prices

Dollar Exchange Rates of

25th August 2014

Japan Yen 104.06

Reports From Japan

ˇˇ

State of the Japanese economy ¨C assessment by BoJ

The Bank of Japan (BoJ) has determined in its latest

assessment that the Japanese economy is on a moderate

recovery track and that consumption is improving after the

huge boom in consumption just prior to the consumption

tax increase.

In the words of the BoJ:

Private consumption shows movements of

picking up, while some weakness remains.

Business investment shows some weak

movements recently, while it is on the increase.

Exports are flat.

Industrial production is in a weak tone with a

reaction after a last-minute rise in demand before

a consumption tax increase.

Corporate profit improvement appears to be

pausing.

Firms' judgment on current business conditions

is cautious, while it shows signs of improvement.

The employment situation is improving steadily.

Consumer prices are rising moderately.

On short-term prospects the BoJ warns that there remains

a downside risk to the economy if the negative impact of

the consumption tax increase continues. The government

has revised down its assessment of short-term factory

output and has indicated that if weakness in the economy

continues it will take action to sustain growth so that its

inflation goal is achieved.

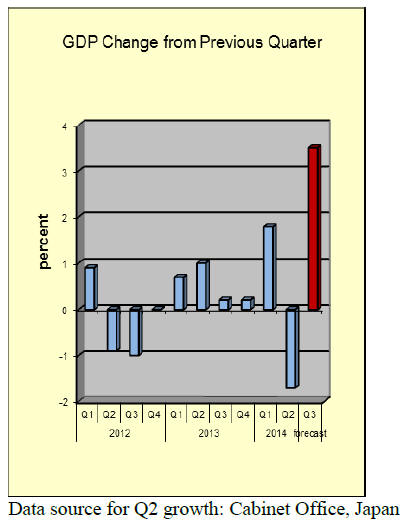

The consensus amongst analysts is the third quarter GDP

growth will be around 3.5%.

Fourth consecutive fall in household spending

Japan's Ministry of Internal Affairs and Communications

has released the results of its survey on household

spending showing an almost 6% decline in July compared

to June. This marks the fourth consecutive decline in

household spending since the consumption tax was raised.

August is vacation time in Japan but reports show a sharp

drop in holiday spending which added to the decline

already being experienced with sales of electronics and

cars.

The July data confirms what the BoJ had deduced, namely

that the effect of the consumption tax rise is taking longer

to dissipate than expected.

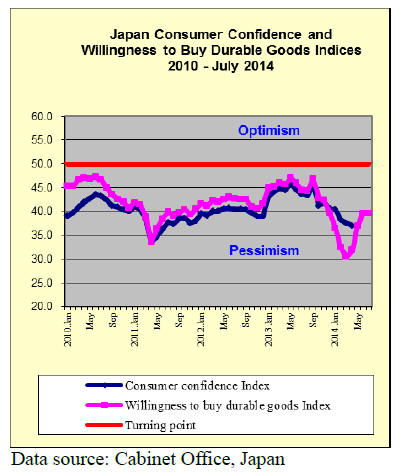

The biggest problem facing consumers is that wages are

not catching up with price rises and this puts a downward

pressure on household spending. The next consumer

confidence survey is expected to show persistent

weakness.

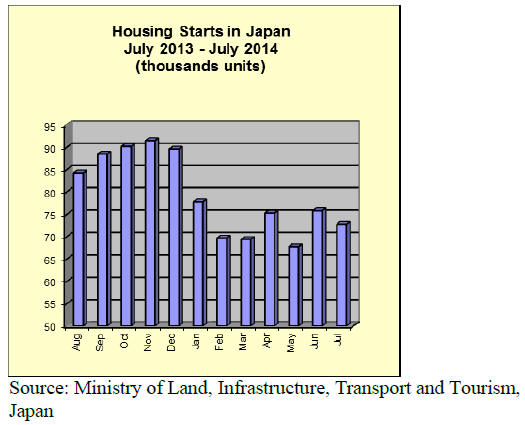

July housing starts reverse course

Japan‟s Ministry of Land, Infrastructure and Transport has

released July housing starts data showing a downturn. A

fall in building activity was anticipated but the extent of

the fall was more than expected.

July 2014 housing starts were just 86% of those in July

2013.

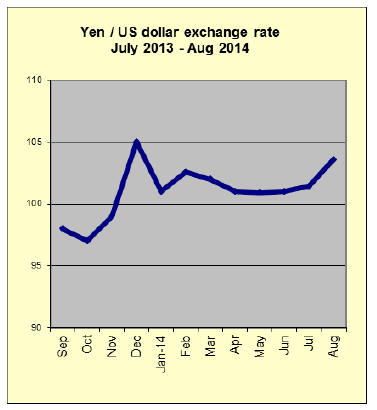

Yen moves above 103 to the US dollar

The Japanese yen:dollar exchange rate altered

significantly towards the end of August as funds were

withdrawn from the „safe haven‟ Japan as tensions eased

in Ukraine and Iraq.

A yen:dollar exchange rate of over yen 103 to the dollar is

higher than what the BoJ appears to be targeting so if the

yen weakens further the BoJ may intervene.

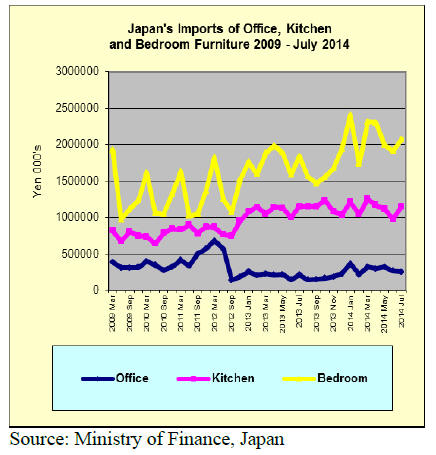

Trends in office, kitchen and bedroom furniture

imports

Japan‟s office, kitchen and bedroom furniture imports

from 2009 to the end of July 2014 are shown below.

Japan‟s imports of bedroom furniture increased in July

reversing the downward trend for the past two months.

Demand for imported kitchen furniture has improved

slightly but was capped by the weak housing starts.

Imports of office furniture have settled back into the

steady and unchanged levels seen before the peak just

before the consumption tax increase in April this year.

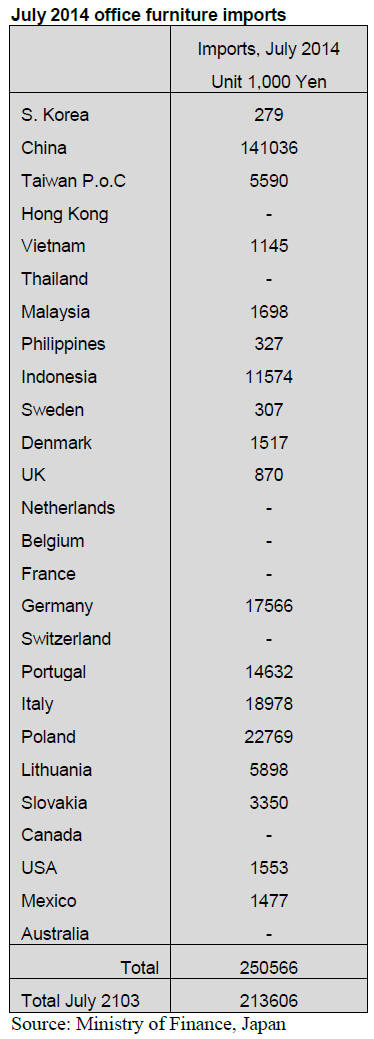

Office furniture imports (HS 9403.30)

Japan‟s July 2014 imports of office furniture were up 17%

compared to levels in July 2013. China remains the major

supplier (56%) with the bulk of the balance being supplier

from the EU, notably Poland, Italy Germany and Portugal.

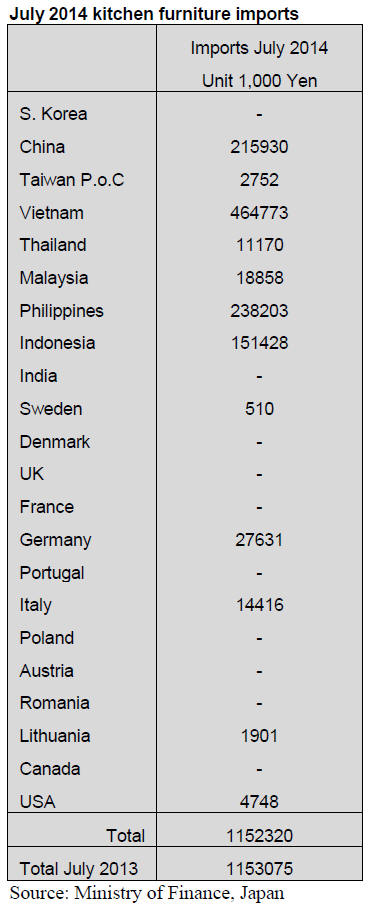

Kitchen furniture imports (HS 9403.40)

The top suppliers of kitchen furniture to Japan in July

continued to be Vietnam (40%), Philippines (21%) and

China (18%) which together supplied almost 80% of all

kitchen furniture imports in July.

The other major suppliers were all in SE Asia, Thailand,

Malaysia, Philippines and Indonesia with the last two

being the major suppliers in the region.

Year on year, July 2014 imports of kitchen furniture

barely changed from 2013.

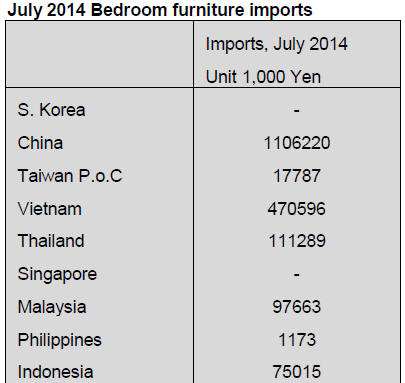

Bedroom furniture imports (HS 9403.50)

Year on year Japan‟s imports of bedroom furniture were

13% up on levels in July 2013 and were also higher than

in June this year.

China, Vietnam and Thailand dominated bedroom

furniture imports in July as they have since the beginning

of the year. Other major suppliers include Malaysia,

Poland and Romania.

Trade news from the Japan Lumber Reports (JLR)

The Japan Lumber Reports (JLR), a subscription trade

journal published every two weeks in English, is

generously allowing the ITTO Tropical Timber Market

Report to extract and reproduce news on the Japanese

market.

For the JLR report please see:

http://www.nmokuzai.

com/modules/general/index.php?id=7

Revision of JAS rules on 2x4 lumber

The Ministry of Agriculture, Forestry and Fisheries drew

up revised JAS rules on 2x4 lumber. The main change is

to classify domestic cedar, cypress and larch to reflect

physical characteristics and strength of domestic species

properly since the original rule was made based on North

American lumber.

Domestic species have been classified and adapted same

as North American lumber standard. As more domestic

species have been used for 2x4 construction, it becomes

necessary to have own rules fordomestic species to

evaluate the characteristic correctly.

There are accumulated data on domestic species, which is

another background for the revision. Restriction on ring

count is also revised. In the past, the rule is that core wood

does not have enough strength so that wood with more

than 6 mm ring count is automatically graded as the lowest

grade but now domestic cedar, cypress, larch, Southern

yellow pine are excluded from the ring count restriction to

evaluate original performance properly.

There will be a new rule on MSR vertical edge glued

lumber, which allows utilization of short lumber for

sawmills.

South Sea(tropical) logs

South Sea log export prices continue firm with low log

production. Weather in Sarawak, Malaysia has been dry

and water level of rivers is low, which makes log towing

difficult. In particular, log supply in Tanjung Manis,

where majority of logs come by rivers, is tight.

India‟s purchase has been very aggressive after Myanmar

banned log export. India is now buying Sarawak low grade

logs for plywood mills. This pushes log export prices up.

Currently, meranti low grade prices are about $270 per

cbm FOB. The demand in India is brisk and with their

currency Rupee getting strong so export log prices seem to

stay up high by India‟s robust demand.

Log prices for Japan, which needs quality logs and

selected logs, are pushed up by strong log prices for India.

Current meranti regular log prices are US$280-295 per

cbm FOB. Small meranti prices are US$245-260 and super

small meranti prices are about US$230.

In PNG and Solomon Islands, log supply decreased by

prolonging rain so that the prices remain firm.

In Japan, log market continues depressed by reactionary

demand drop after the consumption tax hike in April.

Accordingly, the market has no room to accept higher

FOB prices but supply side has been tight in log supply

since last February even after rainy season was over in

June when log prices slacken normally but this year is

different with log prices staying up high. If this high level

continues through summer then rainy season starts in fall,

further increase of log prices is possible as log supply

decreases again in rainy season.

Plywood

Domestic softwood plywood market is weakly holding.

The demand slowed down since May after the

consumption tax increase. Shipment from plywood mills

dropped and the inventories started increasing.

Because of this, all the softwood plywood mills started

curtailing the production since late June and this time they

are all making the same pace orderly to stop decline of the

market. The market reacted favorably to this action and

the trading has been normal without any confusion until

middle August.

However, the production curtailment actually started in

July and June statistics did not reflect this move.

The Ministry of Agriculture, Forestry and Fisheries

disclosed June statistics. The production of softwood

plywood was 231,500 cbms, 3.7% more than June last

year and 4.4% more than May while the shipment was

178,700 cbms, 18.9% less and 0.1% less. The inventories

were 212,000 cbms, 33.6% more than May so the

inventories finally reached about 0.9 month for the

production.

Current market prices of 12 mm 3x6 panel in Tokyo

region are yen 940-950 per sheet delivered, 10 yen down

from July.

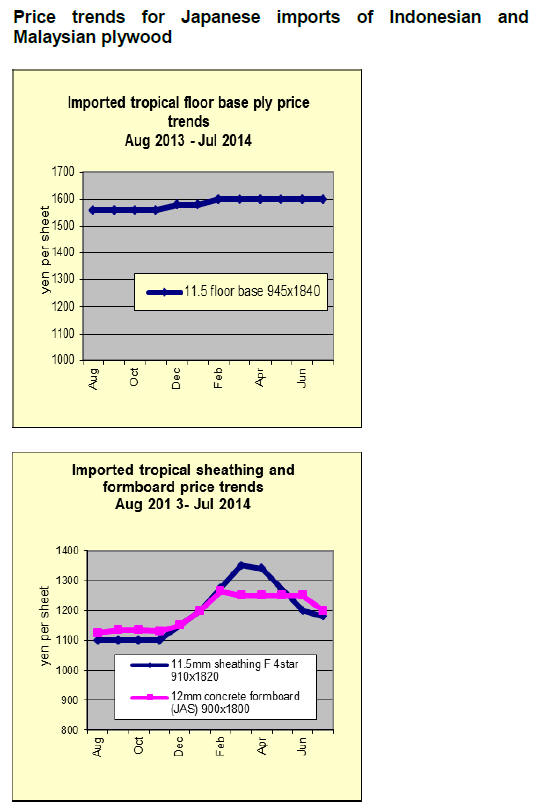

Imported plywood market is bottoming. Since late May,

the market started slackening with slow

demand but with continuous higher export prices by the

suppliers, the importers finally started stop under selling

since late July and asking higher prices and wholesalers

and dealers have started making procurement with bottom

feeling.

Nevertheless, the demand has not really recovered and

with ample port inventories, the importers struggle to pass

higher prices. Current market of 3x6 JAS concrete forming

panel for coating is yen 1,300-1,340 per sheet delivered,

unchanged from July.

Import of North American logs for the first half of 2014

According to the summary the tallying organizations made

up, total import of North American logs were 1,789,000

cbms, 4.3% more than the same period of last year.

Logs for sawmills in major Douglas fir ports like Kure,

Matsunaga and Kashima decreased considerably by mills‟

slower production but log arrivals increased for the ports

like Ishinomaki and Sakai Minato where plywood mills

are so increase of logs for plywood mills offset decrease of

logs for sawmills.

Volume for top three port of Kure, Kashima and

Matsunaga where Chugoku Lumber and other major

Douglas fir sawmills like Toa decreased and total of three

ports was 852,000 cbms, 13.6% drop and share of three

ports in total import was 47.6%, 7.6 points down from the

same period of last year. Another port of Matsuyama

where another large Douglas fir sawmill, Tsurui Sangyo

islocated, showed 19% decline as well.

|