Japan

Wood Products Prices

Dollar Exchange Rates of 25th

July

2019

Japan Yen 108.67

Reports From Japan

ˇˇ

Consumption tax likely to go ahead as

planned

The Japanese economy is less likely to dip into recession

when the consumption tax is increased in October say

analysts after assessing recent retail sales and the pace of

housing sales, neither of which are showing signs of pretax

rise panic buying.

In an effort to avoid any shock to the economy the

Japanese government plans a range of measures to offset

any negative effects of the tax hike on household spending

including tax breaks on car purchases and homes and

rebates for those making cashless payments. The planned

2% rise in tax will not apply to most food stuff.

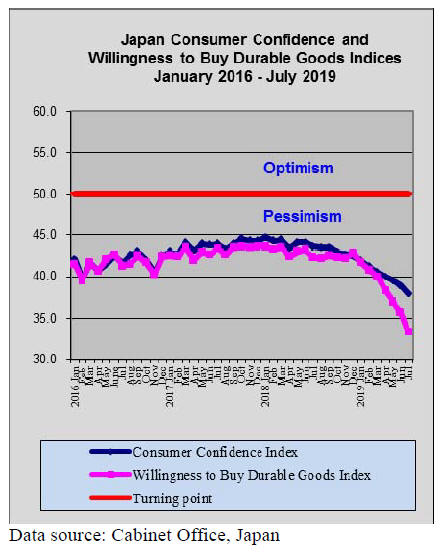

Some observers note that the Japanese economy is more

vulnerable now than it was when the tax was raised before

and that already households are very pessimistic (see

falling consumer sentiment data) so the possible impact on

spending, especially for durable goods such as furniture,

should not be underestimated. Household purchases of

durable goods have fallen to the lowest level since April

2014 when the tax rate went up last time.

Would more leisure time boost spending by young

workers?

In an economic assessment earlier this year the Japanese

government reported that the economy was in one of the

longest periods of expansion for almost 70 years being

driven by new job creation and rising wages, however, a

recently released review makes no mention of this

focusing on the uncertainties in international economic

policies, in particular the US/China trade conflict and

Britain's exit from the European Union.

With respect to the consumption tax rise, which is

almost

certain to go ahead in October this year, the review says

there is a danger that household spending, a pillar of the

Japanese economy, could falter even further.

The review notes that spending by younger workers

remains especially weak and that efforts should be made to

reduce long working hours to create more leisure time

which could encourage spending.

Exports impacted by slow-down in China

Data from JapanˇŻs Ministry of Finance is showing that

June exports were down almost 7% year on year, the

seventh monthly decline. Exports to China, JapanˇŻs

biggest trading partner, fell just over 10% in June the

fourth consecutive monthly year on year decline.

Falling exports, along with falling factory output, is

undermining capital expenditure. Policymakers are

pinning their hopes on a rise in domestic consumption but,

against the backdrop of a looming tax hike, this seems

optimistic.

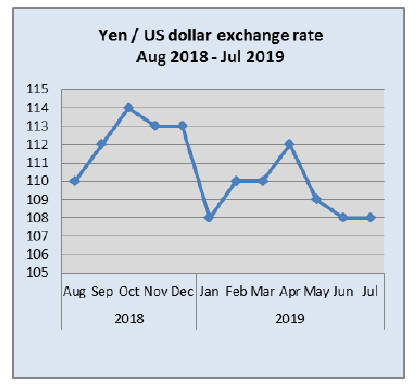

Officials from the Bank of Japan have reiterated that they

remain ready to expand monetary easing if the economy

falters. The impact of such easing would be a weakening

of the yen from its current 108 exchange rate against the

dollar. Just 4 months ago the yen was 112 to the dollar.

Any weakening of the yen would be a boost to exports.

Good use for abandoned homes

It is probably not widely known but the poverty rate

among single mothers in Japan is the highest of all 34

OECD countries. A local non-profit organisation ˇ®Little

OnesˇŻ is helping to address the poverty and discrimination

faced by single mothers and at the same time help address

the problem of abandoned houses in Japan.

The approach by the NPO is simple, it acquires an

abandoned house, undertakes renovation and offers it to

single mothers who face considerable discrimination when

it comes to finding rented accommodation.

Since 2013, ˇ®Little OnesˇŻ has housed more than 200 single

mothers using this approach, turning problematic

abandoned houses into much-needed homes for a

vulnerable group of women and children.

The NPO has gained international recognition for its work

and was awarded top honours at the World Habitat

Awards.

For more see:

https://translate.google.com/translate?hl=en&sl=ja&u=https://w

ww.npolittleones.com/&prev=search

and

https://www.world-habitat.org/world-habitat-awards/winnersand-

finalists/affordable-safe-housing-single-mothers/

Import update

Introducing the Japan Furniture Association (JFA)

Although Japan is regarded as being an economic and

technological power and a country with rich traditions and

culture, it is little known that it is also one of the top

furniture producers in the world with an annual shipment

value of yen 1,400 billion generated by approximately

10,000 furniture manufacturers.

In recent years, Japanese furniture has begun to appear in

international furniture trade shows, such as those in Milan

and Cologne. The JFA writes ˇ°Japanese furniture is a

reflection of Japan's distinctive culture and environment

the designs are fresh and stylish and offer the chance for

customers to create new living styles.

The Japan Furniture Association (JFA) pursues a wide

range of activities aimed at promoting exports of Japanese

furniture including surveys of overseas market trends and

coordination between Japanese furniture manufacturers

and foreign sources of raw materials.

To balance its furniture import promotion activities, the

Association continues to study and propose export

promotion measures for the domestic industryˇ±.

SEE:

http://www.jfa-kagu.jp/en_export.html

Opportunities for EU companies in the Japanese

furniture market

A recent report from the EU-Japan business centre

focusses on the Japanese furniture and home fashion

market, including key industry players, current market

trends and future direction of the market.

The report offers a critical discussion of distribution

channels on the Japanese market ideas on new ways to

rethink strategy and market entry into the Japanese

furniture and interior market.

See: https://www.eubusinessinjapan.eu/sites/default/files/2018-

04-the_japanese_furniture_and_home_fashion_market-glisbyeubij.

pdf

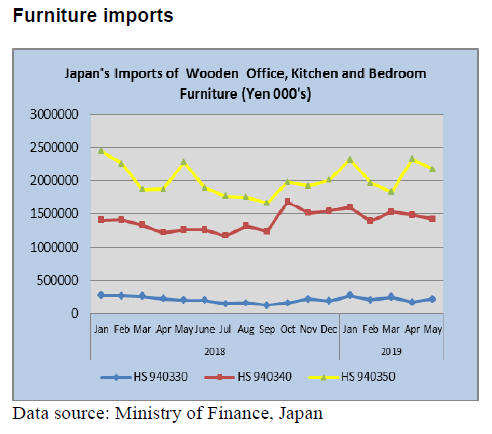

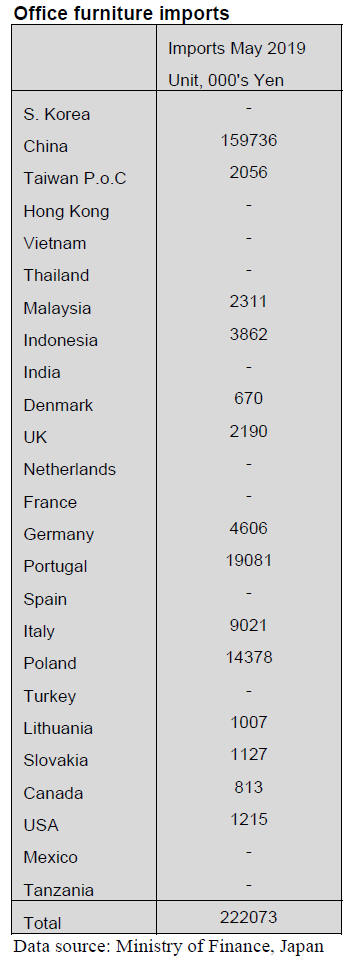

Office furniture imports (HS 940330)

Year on year, the value of May imports of wooden office

furniture rose 10% after the 25% decline in April and

month on month May imports rose over 30% compared to

the previous month.

The value of May shipments from China jumped 30% and

China accounted for over 70% of all wooden office

furniture imports to Japan in May. Exporters in Portugal

re-enter the Japanese market saw a sharp rise in shipments.

Portugal accounted for 8.5% of JapanˇŻs wooden office

furniture imports in May. The other major supplier in May

was Poland which contributed a further 6% to total import

values.

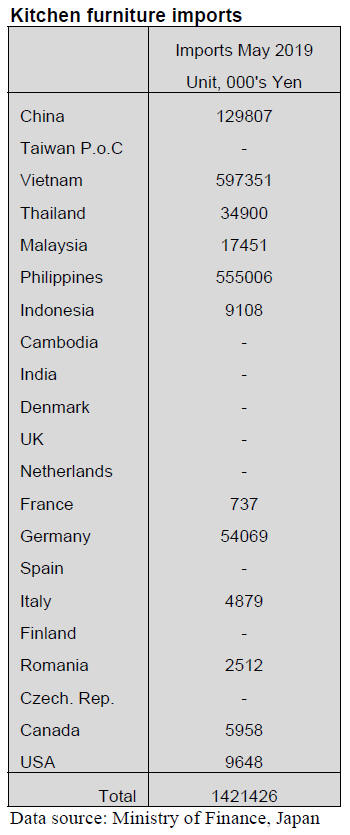

Kitchen furniture imports (HS 940340)

Year on year the value of May imports of wooden kitchen

furniture rose 13% adding to the over 20% rise seen in

April, however, 2019 May imports were barely different

from the previous month.

Shippers in Vietnam and the Philippines maintain their

grip on the Japanese market for imported wooden kitchen

furniture and in May Vietnam edged out the Philippines

accounting for 42% of the value of imports compared to

the 39% share captured by shippers in the Philippines.

Exporters in China consistently command third place in

the ranking of JapanˇŻs imports of wooden kitchen furniture

suppliers and in May accounted for almost 10% of

imports. The top three shippers consistently account for

around 80% of the value of JapanˇŻs wooden kitchen

furniture imports.

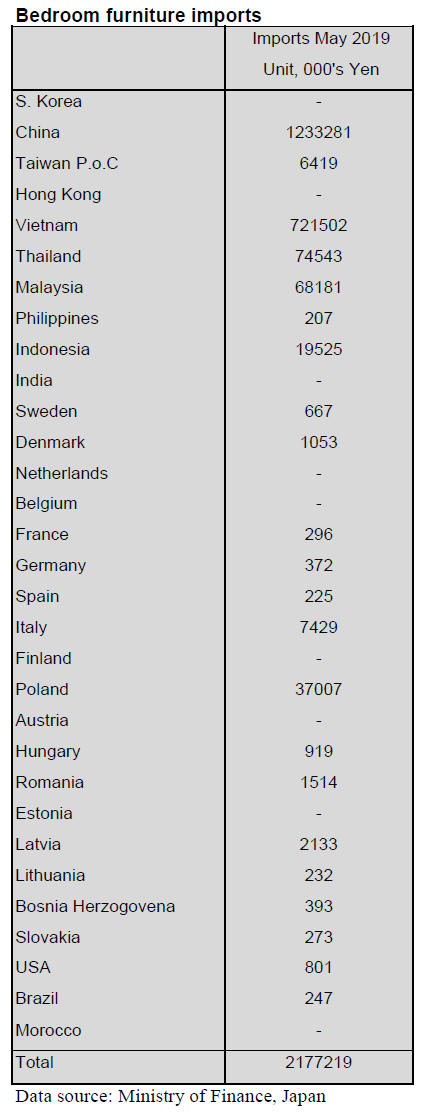

Bedroom furniture imports (HS 940350)

While it appeared the steady decline in wooden bedroom

furniture imports had been arrested in April when there

was a slight rise imports in May slipped back into negative

territory dropping 4% year on year and by 6% month on

month.

China and Vietnam accounted for 90% of JapanˇŻs

wooden

bedroom furniture in May. Shipments from China were

about the same as in April but May shipments from

Vietnam dropped almost 20%. Of the balance 20% of

imports Thailand, Malaysia and Poland accounted for

about 3% each of May imports to Japan.

Trade news from the Japan Lumber Reports (JLR)

The Japan Lumber Reports (JLR), a subscription trade

journal published every two weeks in English, is

generously allowing the ITTO Tropical Timber Market

Report to reproduce news on the Japanese market

precisely as it appears in the JLR.

For the JLR report please see:

http://www.nmokuzai.

com/modules/general/index.php?id=7

Forestry white paper

The government disclosed 2018 forestry white paper in

June. In chapter 1 special edition of theme of manpower.

It is critical issue to secure enough man power for forest

industry. In last December and January this year,

questionnaires are sent to young students and trainees and

received 378 responses.

Desired jobs are 30.9% of forest and forestry and 9.8% of

wood industry. The most important factor in selecting job

is job satisfaction (74.5%), wage and bonus (69.2%) and

working hours and vacation (62.2%).

For the question what was the largest issue when acquiring

the job, the most concern is condition of treatment or

working condition.

For the first time in the White Paper, this issue contains

income of forest workers to show that the working

condition, particularly wage is the largest concern. Others

are trend of number of forest workers and what type of

workers are the most demanded. In other chapter, the most

recent issue of wood product export like cedar fence for

the U.S. market and use of wood for non-residential

buildings.

On wood biomass materials, cellulose nanofiber is now

largely used. For energy use of biomass, consumption of

fuel wood is increasing and utilization of left-over fiber in

the wood increased to 19% in 2016 from 9% in 2014.

Demand projection meeting

The Forestry Agency held the first wood demand

projection meeting for fiscal year 2019 on June 25.

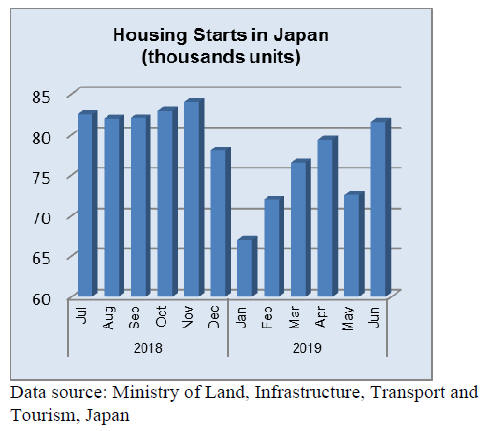

Housing starts forecast by 13 private think tanks are

912,000 units in average, about 40,000 units less than

2018. The last forecast in March was 920,000 so 8,000

units less in six months.

Wood products demand during July and December this

year would be less than the same period of last year.

Demand of imported products like lumber, plywood, logs

and laminated lumber would be all less than the same

period of last year.

Meantime, the supply of domestic logs and softwood

plywood would be up so some items may be over

supplied. Think tanks commented that reaction of

consumption tax increase in October this year to 10%

would be much smaller than the increase of last time from

5% to 8%.

Supply of domestic logs for lumber in the third

quarter

would be 5.8% more than last year but the particular

demand for 2x4 lumber, which was active last year, would

be less this year.

Supply of domestic softwood logs would increase by

11.5% for the third quarter because new plywood mills

start up and increase by 4% in the fourth quarter but the

demand for softwood plywood would peak in the third

quarter and decline in the fourth quarter.

North American logs and lumber for the second half of

this year are available with much lower prices this year but

with uncertain future demand with withdrawal of one large

Douglas fir lumber mill, both demand and supply would

remain low like last year or lower.

Import of North American lumber would be 1,896 M

cbms, 8.2% less than 2018. Both imported and domestic

structural laminated lumber and European lumber would

be the same as last year or less. Russian log import would

largely decrease due to export duty increase and total

arrival is estimated about only 91,000 cbms, 28.3% less

than 2018 while lumber import would be the same as last

year despite high prices.

On radiate pine logs and lumber, demand for crating has

been sluggish because of trade war between China and the

U.S.A. Domestic log export for the first four months of

this year was 13.4% more than 2018 and lumber export

was also up by 10.5%.

Forestland purchases by foreign capital

The Ministry of Agriculture, Forestry and Fisheries

disclosed result of the investigation on forestland purchase

by foreign capitals in 2018. Total purchase was thirty of

373 hectares. In this three cases of purchase of 260

hectares by the American capital with purpose of solar

power generation. The purchase of the same purpose is

reported in 2017 for 90 hectares. The investigation has

been done since 2006 and trend is gradual increase year

after year. Between 2006 and 2018, total purchase is 223

cases with 2,076 hectares.

The investigation is made through each prefectures based

on purchase report required by the Forestry law.

Purchasers are nonresident foreign corporation or private.

By the area of the purchase, Hokkaido is the top with 178

cases of 1,577 hectares. Others are well known resort areas

like Hakone and Karuizawa with the purpose of building

summer house or investment. There are only three cases

with large purchase over 100 hectares.

In 2009, some corporation registered at British Virgin

Island purchased 292 hectares in Hokkaido for the purpose

of grazing field then 163 hectares were purchased by Hong

Kong corporation for the purpose of development or

investment in 2013.

There is another one with 125 hectares for the purpose of

developing summer house property.

In 2018, 118 hectares and 140 hectares in Hyogo

prefecture were purchased by the American corporation

for the purpose of building solar power generation facility.

This is new with different purpose. Total of forestland

purchase by the foreign capitals is 6,787 hectares, which is

0.03% of total forestland of 25 million hectares in Japan.

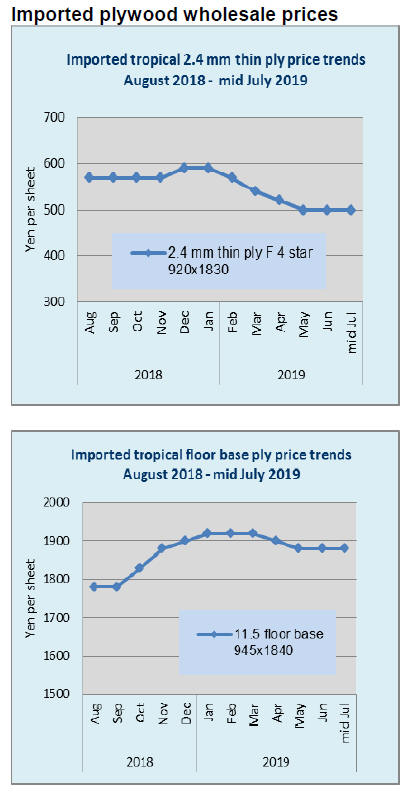

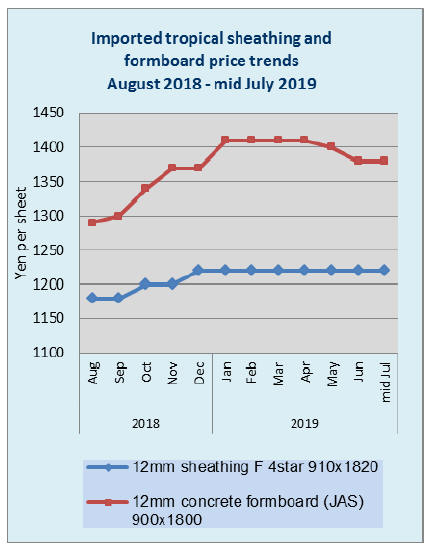

Plywood

There is different move between domestic and imported

plywood market. Movement of domestic softwood

plywood is getting active as precutting plants get busy

with more orders while imported plywood market

continues weak with slow demand despite bottoming

mood.

Orders for precutting plants are increasing and

trading

firms say that plywood orders have been increasing month

after month and some plywood manufacturers have full

orders for month of July.

Because of shortage of trucks, deliveries after 20th of

every month are delaying. Almost all the domestic

plywood manufacturers carry less than two weeksˇŻ

inventory despite full production. They are not able to

increase the production because of man power shortage,

which stops overtime and week end operation. Particularly

thick panel supply is tight.

Major plywood manufacturers in Eastern Japan are asking

higher prices to cover higher cost of logs and trucking.

Market of imported plywood in Tokyo region lacks

vividness. June has more working days than May and

weather was favorable but demand of concrete forming

panels is slow with less number of concrete

condominiums.

The inventories continue declining and there are some

short items but the importers are not able to make future

purchase by sluggish movement in Japan and higher

export prices. The suppliers in Malaysia and Indonesia are

stuck with high cost and are not willing to make sales with

lower sales prices. The importers are attempting to

increase the sales prices in Japan so there are no more

extreme low offers.

Trucking industry

It has been last five years that shortage of truck drivers

became serious problem for wood products industry and it

is getting serious year after year. Number of registered

truck operators is 62,200 in 2016. According to the Japan

Truck Association, labor environment of truck drivers

continues severe. For large truck drivers, annual working

hours are 2,580 and for smaller truck drivers, it is 2,568

hours in 2018.

Average working hours of all the industry are 2,144 so

large truck drivers work 456 hours a year more than other

industry while annual income of large truck drivers is

4,570,000 yen and of smaller trucks is 4,170,000 yen,

which are lower than average of other industry of

4,970,000 yen.

Number of people engaged in truck transportation in 2018

is 1,930,000 in 2018 but 41.5% is over 50 years old while

drivers under 40 years old are 26.9%.Under this

circumstances, trucking industry is trying to improve

working condition.

It is important to make working hours less and to increase

wage to attract younger people so the government is

assisting by changing laws.

In the past, time for cargo loading and unloading or

waiting was a part of trucking cost but these make

working hours longer so now these are charged on top of

trucking cost.

Wood industry is facing difficulty of securing enough

trucks with higher cost. Large laminated lumber

manufacturers are charged 15-20 % higher cost for

trucking. Local manufacturers need to transport lumber to

large consuming market like Tokyo, which force drivers

longer working hours so it may become necessary to have

costly relay point.

|