Sharply rising prices with extremely

lively global demand for building materials. All timber products are

currently following this development. Above all, the export markets

in China and the USA lead to shortages of availability and rising

prices in Europe.

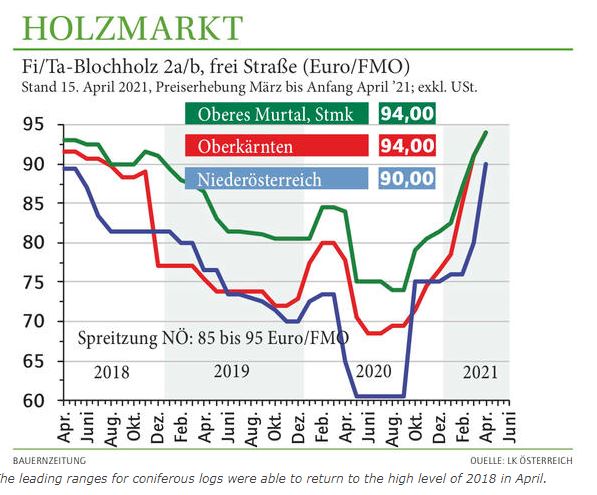

Due to the booming wood markets, the needle saw log prices in

Austria have meanwhile reached the level before the beetle-related

oversupply. However, the supply lags behind the increasing demand.

The timber harvest in autumn 2020 was slowed down due to the price

level at the time. Accordingly, the Austrian sawmills are currently

receptive. Provided that there are no weather-related restrictions,

the wood provided will be removed quickly.

Leading range spruce A / C, 2b

mostly over 90 euros / FMO

While the leading range Fichte A / C, 2b is usually paid over 90

euros per FMO throughout Austria, the price level in the damaging

regions of the Waldviertel and Mühlviertel is not understandably

lower. Inferior qualities are also following the upward trend, but

the gap to the leading range is unusually large. Individual premiums

are granted for late uses. Contracts are currently more likely to be

concluded with a short term and a price differentiation between A /

B and C quality is increasingly being used again. When comparing

offers, therefore, the type of case must be taken into account more

strongly again, the quality assessment at the sawmill should be

meticulously checked.

Larch is still in high demand, and prices have increased somewhat

regionally.

Relaxation even with

industrial wood

Despite the regional oversupply due to old damaged wood, the

situation on the coniferous roundwood market is gradually easing, at

least in terms of quantity. The prices are stable at a below average

level. A slightly reduced amount of sawmill by-products and waste

paper have regionally led to faster removal and increased quantities

of pulpwood taken over. The purchase of grinding wood relaxes mainly

through export. For red beech fiber wood there is normal volume

demand at stable prices.

Lively demand for energy wood

With the exception of Upper Carinthia, in the southernmost federal

state there is a noticeable increase in demand for energy wood, even

for small to medium-sized biomass plants. Larger heating plants

underpin their stronger demand with slightly rising prices. In the

other federal states, it is difficult to market energy wood apart

from existing delivery profiles.

Bark beetles require further

attention

Despite a relatively cool April, the bark beetle monitoring delivers

the first catch figures. Appropriate attention must be paid to the

processing of infested beetle trees from the previous year and catch

material.

All prices quoted relate to business transactions in the period from

March to the beginning of April 2021 and are net prices to which

sales tax is to be added. The following tax rates apply to the sale

of wood to entrepreneurs: with sales tax flat rate for all

assortments 13%, with regular taxation for energy wood / firewood

13% and for round wood 20%.

Source: LK Austria

market report as of April 15, 2021