|

Report

from Europe

and the UK

European economic confidence severely dented by

banking crisis

Widely reported measures by the UK government to bailout

failing banks have quelled the worst fears of European

investors and depositors of an imminent and disastrous

economic collapse. Steps have been taken to inject a

massive amount of state money into leading retail banks

and significantly reduce interest rates by several central

banks, including the euro area��s European Central Bank.

Nevertheless, economic confidence in Europe has taken a

severe beating over recent weeks, as evidenced by

weakening currencies and forecasts that Europe may be

facing its worst recession since the early 1990s.

In the UK, the scale of the bank rescue plan has been

particularly dramatic, the government having pledged

GBP400 billion to guarantee that no UK bank fails.

However the very need for such drastic measures seems

only to have underlined how bad things have become. By

putting its full weight behind the banks, the government

has signaled its determination to avoid a worst-case

outcome. But confidence has been shaken to the core,

while concerns are now being raised over the severe fiscal

risks associated with such a large input of public money.

The government is now deeply in debt, leaving no room

for increased public sector spending to tide the economy

over the bad times and holding out the prospect of tax

increases which will further dampen private sector

spending.

UK confidence was ebbing even before the real scale of

the banking sector crises became clear in early October

2007. Business surveys of purchasing managers for both

manufacturing and the services sector touched record lows

in September. Construction is wilting as homebuilders put

projects on hold and lay off workers. As much of the UK��s

recent growth had been driven by the City, and based on a

financial model whose defects have now been brutally

exposed, expectations are that the nation��s economy will

be particularly hard hit. The UK economy now seems

certain to have entered a recession during the second half

of 2008. This has led to a rapid fall in the value of sterling

against other currencies.

Economic conditions in other European countries are less

dire, but still the outlook is not good. Due to relatively

tight regulation of the banking sector and relatively strong

retail banking networks, France has had to bail out just one

bank, Dexia, a small Franco-Belgian lender. This was

intended merely as a precautionary, confidence-boosting

measure. Nor have the French been on a huge credit binge.

The household savings rate remains high. Nevertheless

third-quarter GDP figures are likely to show that the

French economy is already in recession and the IMF

forecasts growth of just 0.2% in 2009.

Germany��s bank rescue package is backed by a state

guarantee of EUR400 billion with the aim of ensuring that

no ��system-relevant�� bank will fail and no depositor will

lose money. Nevertheless, indications are that Germany

will not avoid a slowdown. The IMF expects no growth at

all next year. Germany has sounder public finances, less

indebted enterprises and more competitive wages than

others. Yet it is more dependent on exports, so will be hit

harder by a global slowdown.

Italy��s banks have not been so exposed to the global crises

as those in other parts of Europe partly because, as the

nation��s Finance Minister recently admitted to parliament,

they are ��less advanced and sophisticated��. The

government is still forecasting GDP growth of 0.5% in

2009 but this is now a minority view. The employers��

federation, Confindustria, expects the economy to shrink

by 0.2% this year and 0.5% next.

Spain��s banks lack liquidity but none has needed rescuing

thanks to the Bank of Spain��s tight regulation and the

prudence of Spanish bankers. But Spain is worse off than

many others on the broader economic front. The banking

crises has further undermined confidence already reeling

from the effects of a burst housing bubble. The IMF now

expects the economy to shrink by 0.2% next year and

unemployment is rising.

Tropical hardwood sawnwood markets take a hit

Judging by the comments of European agents and

importers, the effects of the banking crises on demand for

sawn hardwood have been immediate and fairly dramatic.

One major supplier to the UK notes that ��our sales of sawn

hardwood were doing reasonably well until the first week

of October 2008 when the panic over the stability of the

banks came to a head. Demand picked up a little the week

following the announcement of the bank bail-outs, but it

has gone quiet again now��.

Overall consumption of hardwood sawn lumber in the UK

has taken a hit from the rapid decline in new residential

construction. This has particularly affected demand in the

mass production joinery and window manufacturing

sector. This in turn has fed through into particularly weak

demand for commodity tropical hardwood species

including sapele and meranti.

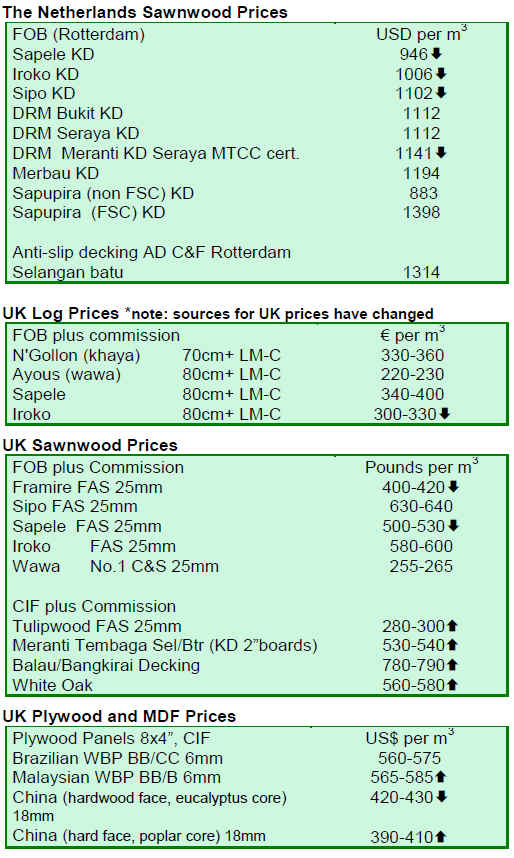

FOB prices for sapele quoted to UK importers have

remained soft in recent weeks. However agents suggest

that these prices may have hit a floor as margins amongst

African exporters are already extremely tight and

production levels have been sharply curtailed. Much

reduced forward purchasing of sapele during 2008 also

means that UK grounded stocks are now low and there are

gaps in some areas. In the credit crunch, the pressure to

buy little and often has intensified.

Meanwhile weakening of sterling against the dollar has

meant that sterling prices for meranti have been rising and

are now less competitive against sapele. Demand for iroko

in the UK has held up reasonably well, however the

market for framire/idigbo is described by one agent as

��dire��.

To some extent the decline in UK demand from new

residential construction has been offset this year by

continuing consumption in the renovation sector. With

house prices falling and credit tightening, less people are

moving house but they have been spending money on

improvements. The concern now is that increased

nervousness over the banking crises will undermine even

this source of demand while tightening public finances

will reduce demand from public sector projects. For

example, due to budget cuts in the wake of the credit

crunch, the Olympic Delivery Authority for the London

2012 Olympics has already been forced to cut the number

of housing units in the Athletes Olympic Village from

3,500 to 2,800.

Demand in the Benelux countries also remains very

subdued. One agent in the region suggested that importers

are still carrying very high stocks of standard items. For

example, sales of tropical hardwood decking fell well

short of expectations this year and stocks remain very high

at a time of year when they should be low. This will

inevitably feed through into much reduced orders for the

spring 2009 season. Given the current stock position and

the obvious desire in the current market situation to avoid

holding excess stock, this agent was told by one of his

leading buyers not to expect any new orders for at least

three months.

Reports are coming through of slow sales of hardwood to

the Italian furniture and flooring sectors. Many Italian

furniture and flooring factories are now only operating

three or four days per week and several have closed

permanently. This reflects both declining domestic

consumption and intense competition in export markets as

manufacturers from all regions are now chasing declining

orders. Hardwood orders from Spanish and Portuguese

manufacturers have also been declining, with the signs of

particular stress in the Spanish door industry.

European plywood importers fail to step up

purchasing

The credit crunch and economic slowdown has meant that

European plywood importers are very reluctant to commit

to purchasing in any volume while stock holdings are seen

more and more as a liability. However there may be a few

opportunities to find buyers before the year is out.

According to a plywood trader quoted in the UK��s TTJ

��the biggest factor in the UK and European markets at the

moment is fear��.Stock reduction is running ahead of

demand reduction and, as we run into autumn and winter,

we will see some shortages. The trade has still got some

buying to do before the New Year��.

European imports of Chinese plywood have been

declining due to recent consolidation of the Chinese

plywood sector, combined with rising costs of raw

material, labor and energy, and the downturn in European

consumption. The same TTJ article notes that despite

recent consolidation in the Chinese plywood

manufacturing sector, UK buyers continue to receive huge

numbers of offers of plywood from mills in China. This

suggests that there is still excess supply in the pipeline, a

fact also reflected in a slight softening in prices for

poplar/bintangor plywood from China. In addition to slow

consumption, reluctance amongst many European

importers to buy Chinese plywood reflects continuing

concerns over variable quality of product.

Meanwhile, there are signs that the price differential

between Malaysian and Indonesian tropical hardwood

plywood on offer to EU importers is narrowing. A

relatively high price for Indonesian plywood in recent

times has meant that Malaysia has been the main

beneficiary of partial shift away from Chinese plywood in

the EU market. However, according to the German trade

journal EUWID, prices for 4X8ft BB/CC grade Indonesian

plywood for shipment in October/November 2008 stand at

Indo96 +32% to +34%, a decline from Indo96 +37% at the

end of August. Meanwhile, over the same period

Malaysian prices have risen from Indo96 +19% to +20%

to Indo96 +24% to 25%. The price gap for European

importers is expected to narrow further next year when EU

import duties on Indonesian plywood are due to be

lowered from 7% to 3.5%, equivalent to the duty currently

imposed on Malaysian plywood.

EU releases its proposed illegal logging legislation

On 17 October the European Commission finally

published its long anticipated proposal to introduce new

legislation designed to minimize the risk of illegal wood

entering the EU market. As noted in the previous ITTO

Tropical Timber Market Report (TTMR 13:19), the

proposal is that individual operators engaged in the trade

and production of wood products in the EU would be

required to implement a ��due diligence�� management

system to reduce the risk of any illegal wood entering their

supply chains.

A significant change from earlier drafts of the proposal is

that it would apply only to operators who place timber and

timber products ��for the first time on the Community

market��. There has been some confusion amongst

European trade organizations of precisely which operators

would be captured by this definition (some interpreting it

to include European forest owners). However, an EC

official made clear the intent of this definition at the

International Timber Trade Federation meeting hosted by

the EC-funded Timber Trade Action Plan in Geneva on 27

October. The EC official noted that the measure was

directed specifically at EU-based importers and primary

processors (e.g. sawmills, plywood mills, panel products

mills, pulp mills).

The scope of the products covered by the proposed

legislation is extremely wide, covering all products

included in the existing FLEGT Action Plan (logs, sawn,

plywood, and veneers) together with:

• Pulp and paper of Chapters 47 and 48 of the

Combined Nomenclature, with the exception of

bamboo-based and recovered (waste and scrap)

products;

• Wooden furniture of CN code 9403 30, 9403 40,

9403 50 00, 9403 60 and 9403 90 30;

• Prefabricated buildings of CN code 9406 00 20;

• Fuel wood, in logs, in billets, in twigs, in faggots

or in similar forms; wood in chips or particles;

sawdust and wood waste and scrap, whether or

not agglomerated in logs, briquettes, pellets or

similar forms of CN code 4401;

• Builders�� joinery and carpentry of wood,

including cellular wood panels, assembled

flooring panels, shingles and shakes, wood

(including strips and friezes for parquet flooring,

not assembled) continuously shaped (tongued,

grooved, rebated, chamfered, V-jointed, beaded,

moulded, rounded or the like) along any of its

edges, ends or faces, whether or not planed,

sanded or end-jointed of CN code 4418;

• Particle board, oriented strand board (OSB) and

similar board of wood whether or not

agglomerated with resins or other organic binding

substances of CN code 4410;

• Fiberboard of wood or other ligneous materials,

whether or not bonded with resins or other

organic substances of CN code 4411;

• Densified wood, in blocks, plates, strips or profile

shapes of CN code 4413 00 00;

• Wooden frames for paintings, photographs,

mirrors or similar objects of CN code 4414 00;

• Packing cases, boxes, crates, drums and similar

packings, of wood; cable-drums of wood; pallets,

box pallets and other load boards, of wood; pallet

collars of wood; coffins of CN code 4415;

• Casks, barrels, vats, tubs and other coopers��

products and parts thereof, of wood, including

staves of CN code 4416 00 00.

Green groups have already been critical of the proposals

on the grounds that they do not go far enough in defining

procedures for legality verification and in setting out

specific penalties for operators that might be found to be

trading in illegal wood.

On the other hand, the EC has been conscious of the need

to avoid imposing excessive new bureaucratic

requirements on the trade in timber from areas where there

is little risk of illegal logging. After all, even the most

pessimistic assessments suggest that only perhaps 20% of

existing EU wood imports derive from illegal sources

while the level of domestic supply from illegal sources is

likely to be significantly lower. So it makes absolutely no

sense to subsume the existing 80% of legal wood supply in

new systems and procedures �C particularly as this would

only increase the costs of legal operation, providing an

additional perverse incentive to operate illegally and

undermining competitiveness of wood against other less

environmentally beneficial materials.

Hence the new legislative proposal is carefully targeted

focusing specifically on the risk assessment systems of

companies operating at that point in the trading chain

where there is most leverage to take proactive measures.

No new requirements would be imposed on those

suppliers where there is high confidence that there is low

risk of illegal logging. The proposal also has the strong

benefit of building on and integrating with existing

systems of due diligence that have been developed by

trade associations and NGOs in several countries.

The proposal must now be considered by both the

European Parliament and European Council of Ministers.

The earliest conceivable date on which it could come into

force is April 2009. The proposal includes a provision for

the ��due diligence�� requirements to be phased in over a

period of 2 years, so individual operators would have to

demonstrate compliance from April 2011 onwards.

However, there are still many obstacles to full

implementation and it is possible that a European

Parliament vote on the issue cannot be scheduled until

well after the June 2009 parliamentary elections.

A full copy of the proposal is available at:

http://www.illegallogging.info/uploads/flegttimberproposaloct08.pdf

��

|