|

Report

from Europe

and the UK

EC and Vietnam establish FLEGT Technical Working Group

The Vietnamese Ministry of Agriculture and Rural

Development and the European Commission (EC)

have agreed to establish a bilateral Technical Working

Group on Forest Law Enforcement Governance and Trade

(FLEGT). The aim of the working group is to jointly

investigate the options of combating illegal logging and

related trade and the possibility of negotiating a FLEGT

Voluntary Partnership Agreement between Vietnam

and the European Union. Vietnam is a major exporter of

processed timber products to the EU and has recently been

criticized for importing illegally harvested timber

to supply its booming furniture sector. With legislative

initiatives against the trade in illegal timber products being

developed in the US, the EU and other consumer

markets, the Vietnamese industry is seeking ways to

maintain and expand its market position by guaranteeing

the legality and sustainability of its timber products. The

European Union has recently completed negotiations for a

FLEGT Voluntary Partnership Agreement with Ghana and

is currently negotiating such agreements with Malaysia,

Indonesia, The Congo and Cameroon.

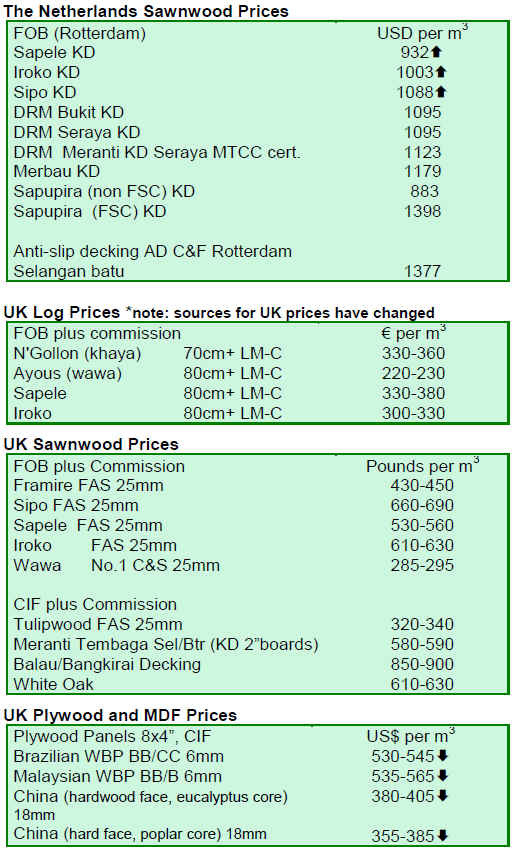

UK plywood market faces uncertainty

European CIF prices for hardwood plywood are down

across the board against a background of weak

consumption and uncertainty over prospects for 2009.

Prices are highly volatile �C as one UK plywood importer

notes: ��while I can tell you a price today it will be

completely different next week. All I can say is that it��s

entirely a buyers market. There are numerous cheap offers

out there and we can just take our pick��. Generally falling

CIF prices into the EU are also partly indicative of falling

freight rates from most regions in response to declining

fuel costs and the reduction in the overall level of global

trade.

For Brazilian suppliers to the EU, although there has been

some pick up in inquiries amongst importers seeking to

benefit from the duty free quota, most importers are still

holding back on large orders. Widespread speculation that

prices might drop further in the New Year is only adding

to importers reluctance to place orders now. EU buying of

plywood from Brazil is now concentrated on only a few

large shippers. Many smaller Brazilian shippers formerly

engaged in the trade are no longer active as they lack

access to sufficient capital to finance raw material and

other costs.

Meanwhile, European CIF USD prices for Chinese

poplar/bintangor plywood are now around 10% down on

prices prevailing in October. The failure of demand for

Chinese plywood in the EU and US has contributed to the

closure of numerous smaller Chinese plywood mills in

recent months.

Indonesian plywood shippers are now offering goods to

the European market at a level of around INDO96 +30 to

INDO96 +32. Efforts by Indonesian shippers to increase

prices to European buyers over the summer were

unsuccessful in the face of weak market conditions.

While Malaysian mills are struggling to find orders, there

is feeling that they are better placed to weather the storm

than their competitors in China and Brazil. This reflects

their recent concerted efforts to diversify their product

range and to offer a wider range of services such as FSC

and MTCC certification. Nevertheless, there is some

expectation in the EU that prices for Malaysian plywood

will fall again in the New Year.

UK importers suggest that existing landed stocks of

hardwood plywood are reasonably high for the time of

year and are likely to be sufficient to cover anticipated

levels of demand at least until February and March 2009.

Consumption is very subdued due to the weak

construction sector. This problem is compounded by the

UK��s credit insurance industry which seems to have

decided that the whole of the wood panels industry is high

risk due to its perceived dependence on the construction

sector. Many importers, distributors and merchants are

having their credit insurance withdrawn making suppliers

less reluctant to deal with them.

The usual rush in the EU to place forward orders for

plywood immediately after Christmas is not expected this

year. Importers are likely to hold off new purchases for as

long as possible as many expect further price declines in

the first quarter of 2009.

Analysts report on the depressed EU hardwood market

The US trade journal Hardwood Review Global provides a

flavor of current depressed market conditions for

hardwoods within the EU. In their November issue, the

reporters note: ��one major exporter said that hardwood

demand in every European market �C from the United

Kingdom to Scandinavia to Germany to the Mediterranean

�C has been hurt by the economic downturn. European

buyers were purchasing only enough lumber to fill gaps in

inventory, and most were shopping around to get the best

specifications for the lowest prices��. Hardwood Review

Global go on to note that Italy��s export-oriented furniture

industry is suffering severely in the economic downturn,

while the poor housing market has had a particularly

profound impact on the Spanish and Portuguese door and

window manufacturing sectors. Belgian importers are

reporting that their purchases are down 40% compared to

last year.

In France, commentators reckon that the hardwood trade is

currently running at 15-20% of last year's level, a

contraction common to just about all end use sectors. Only

renovation and flooring are still performing anywhere

close to their usual levels. Due to reasonably good imports

in the first half of the year, French commentators suggest

overall import levels for 2008 will not be far short of 2007

but expectations are for a poor year in 2009.

The UK is in the grip of a downturn led by the popping of

the housing bubble. Rapid weakening in the sterling

exchange rate in recent weeks has also meant apparent

price rises for hardwood imports providing another

disincentive, if any were needed, to enter the forward

market.

EU veneer market shows downward trend

According to the German trade journal EUWID, some

central European sliced veneer suppliers are reporting falls

in sales of 30% to 40% compared to the same period last

year. Sales to western European markets have been weak

all year. Until the summer months, veneer suppliers

reported reasonably stable sales figures to Scandinavia and

parts of Eastern Europe. However, the downward market

trend now affects all European markets without exception.

Demand is weak in all sectors linked to the building

industry, particularly door manufacturing. The furniture

sector has also slowed dramatically in recent months. High

value sectors �C including bespoke fitting, ship, aircraft and

car manufacturing �C were stable during the first half of the

year, but have since gone into decline.

Europe��s sliced veneer producers are responding to the

downturn with a reduction in output. EUWID estimates

that current utilization capacity at veneer mills in the

region may be as low as 30-50%. Despite the cut in

production veneer sales prices remain under pressure.

Under such conditions, procurement of veneer logs has

been severely curtailed, particularly of dollar denominated

stock from the US which has tended to rise in price in

European markets due to the strengthening dollar rate.

European hardwood manufacturers move away from tropical wood

The 25th issue of EUWID��s Holz Special, which provides

a thorough analysis of European market conditions across

several product sectors, notably OSB and flooring, notes

that a number of European parquet flooring producers are

planning on stopping processing tropical timber in the near

future. According to EUWID, MeisterWerke became the

first major Central European parquet manufacturer to

announce plans to remove all tropical timber products

from its lines by the start of 2009. The Austrian firm

Weitzer Parkett followed suit in October. Although the

main reason cited for these measures is increasing concern

for sustainability issues, other factors are also seen as

important. These include the comparatively high costs of

tropical hardwood and the high capital commitment

required in order to source these species, factors which

have become more critical during the current economic

crises.

According to EUWID, European parquet producers are

finding it very hard to generate new orders for their

products and many have now built up large unsold

inventories of finished goods. Producers of three-ply and

multi-ply parquet that have pushed ahead with capacity

development in recent times have been particularly hard

hit. EUWID suggest that overall parquet production levels

in the EU may fall by between 12% and 18% in 2008

compared to 2007.

The Environmental Investigation Agency (EIA) has turned

up the heat on European parquet flooring manufacturers��

using tropical hardwoods with publication of their ��Buyer

Beware�� report in October 2008. The report was based on

interviews undertaken by EIA researchers posing as

customers during September 2008. The inquiry considered

whether retailers of merbau flooring on sale in the UK

could prove that it originated from legal sources and

whether adequate information was available to consumers.

According to EIA, while in the first instance retailers were

often quick to make strong environmental claims about

their merbau flooring products, on further investigation

these claims could often not be substantiated. Drawing on

their analysis, EIA called on the UK government ��to put in

place measures to outlaw the sale of wood products and

timber derived from illegal logging��.

��

|