|

Report

from

Europe, the UK

and

Russia

Short term EU market prospects very poor

Short term prospects for the European hardwood sector

appear very poor. Hardwood consumption has been hit by

serious economic disruption resulting from the bursting of

the property bubble and associated credit crunch. This has

created a vicious downward spiral as lack of credit to

businesses and individuals is now causing severe cash

flow problems and reducing economic activity further,

contributing to rising levels of unemployment, higher debt

default rates, and further falls in consumer spending.

Media reports highlighting these problems are helping to

reinforce and deepen negative sentiment. It should be said,

however, that the world keeps turning; there is economic

activity; and wood is being consumed. Although the

market is extremely competitive, those with the right stock

at the right price are finding buyers.

But there is no disputing that these are extremely tough

times for hardwood traders in the EU. According to many

importers �C whether of logs, lumber or plywood �C these

are the worst trading conditions they have ever

experienced. Many suggest that there was particularly

abrupt deterioration in market conditions with the banking

crises that emerged in early October.

At present it is too early to say with any degree of

certainty how much demand has been lost since the onset

of the economic crisis or will be lost and for how long.

Some large European importers report that they have

bought hardly anything for forward shipment for six

months. Generally cash flow is extremely tight and efforts

are still being made to reduce inventory. This in turn is

feeding through into even lower prices for landed stock.

At some point stocks will reach a level where it becomes

essential for buyers to move into the forward market, but

most reports suggest that stage has yet to be reached.

Giving accurate price indications in such market

conditions �C where the major focus is on reducing existing

grounded stock levels and there is very little forward

buying �C is extremely difficult. Forward prices are

generally being quoted across a wide range. All that can be

said with any degree of accuracy is that there are cheap

offers around on many standard items. These are coming

from those shippers most desperate for cash flow and that

have been slower to react to changing market conditions

by reining in production levels.

Statistics show deep declines in EU imports of

hardwood products

Unfortunately the reports of an abrupt downturn in EU

demand during the last quarter of 2008 cannot yet be

tested with reference to trade statistics. The most recently

available comprehensive EU import statistics are only

available until the end of the third quarter of 2008. These

show that while the hardwood trade in some European

countries was holding up reasonably well to the end of

September 2008, trading conditions in others has been in

steep decline all year.

The following charts show the volume of hardwood

primary and secondary wood products (logs, rough sawn

timber, veneer and plywood) imported from developing

countries by the EU-25 group of countries (i.e. all EU

countries excepting new members Romania and Bulgaria).

The data is for quarterly imports beginning in the first

quarter of 2007 and ending in the third quarter of 2008.

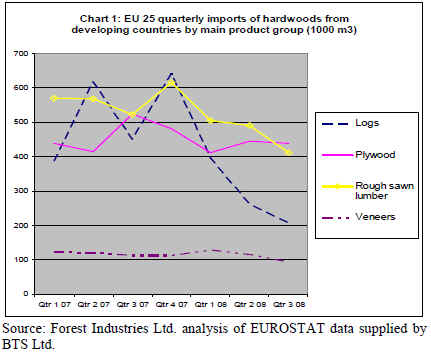

Chart 1, which breaks the data down by product group,

highlights that EU imports of hardwood logs from

developing countries declined dramatically from the start

of 2008 onwards, while imports of hardwood sawn

lumber, veneer and plywood were also sliding downwards,

although at a slower pace.

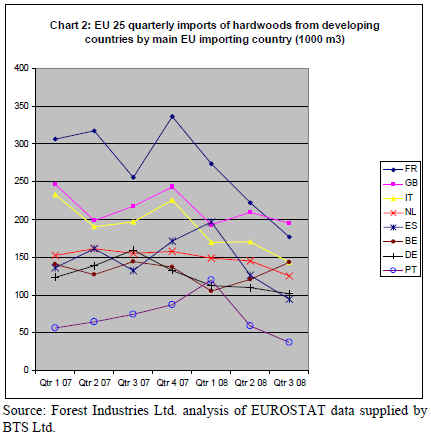

Chart 2 shows that the biggest decline in EU imports of

hardwood products from developing countries in the first

nine months of 2008 was recorded by France which has

seen a significant fall in the volume of log imports,

particularly from Africa. It also shows that Italian imports

have been on a downward trend at least since the start of

2007, a sign of longer term economic problems in that

country. Meanwhile imports into Spain and Portugal were

rising strongly throughout 2007, but fell dramatically from

the start of 2008 onwards with the bursting of Spain��s

housing bubble. Anecdotal reports indicate this trend

continued and intensified in the fourth quarter of 2008.

Spanish wood importers suggest that overall hardwood

sales in 2008 may be down as much as 30% to 40%

compared to the previous year. The German and Dutch

markets were characterized by a steady slide in imports

from around the third quarter of 2007 onwards.

Interestingly, both the UK and Belgian hardwood markets

were performing reasonably well until the end of

September 2008, but anecdotal reports indicate an abrupt

change of sentiment from October onwards.

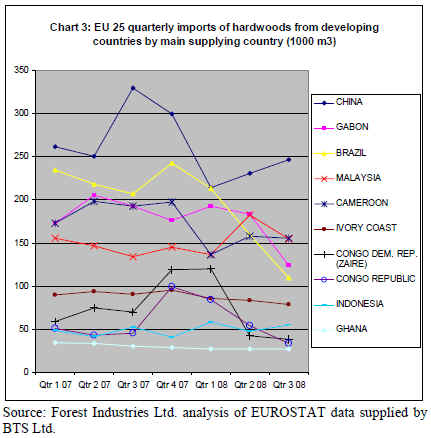

Chart 3, which shows data by major supplying country,

indicates that EU hardwood imports from Brazil have

declined very dramatically, with third quarter imports in

2008 being only around 50% of imports in 2007. Imports

of hardwood from China �C which mainly consist of

plywood destined for the UK �C have been extremely

volatile, which is not particularly unusual in the

commodity plywood sector. EU hardwood imports from

China in 2008 have been lower than in 2007, but on a

quarterly basis were tending to recover during the first 9

months of the year. This reflects particularly low levels of

EU plywood imports from China in the first quarter of

2008 owing to uncertainty over possible introduction of

anti-dumping duties on Chinese manufacturers.

The fortunes of African countries supplying the EU have

varied widely over the last 12 months. Imports from

Gabon �C much of which are destined for France �C fell

rapidly in 2008. EU imports from the Democratic

Republic of Congo rose strongly at the end of 2008 and

into the first quarter of 2008, but then fell dramatically

thereafter. Imports from Cameroon, Cote d��Ivoire and

Ghana have generally remained more stable, showing only

a steady decline during the first three quarters of 2008.

Meanwhile EU hardwood imports from Malaysia actually

strengthened during 2008 and imports from Indonesia,

although still a shadow of their former size, also showed

some recovery. Both countries were benefiting from

mounting plywood supply problems amongst their major

competitors in China.

Putin signs resolution on Russian timber export duties

Prime Minister Vladimir Putin signed Resolution 982 on

24 December 2008, which set export fees at 25% from 1

January 2009 to 1 January 2010 on certain pine species

and birch with a diameter not less than 15 cm. The export

fees for oak, beech and ash are reported to be EUR100 for

per m³. The 80% export fees on major roundwood types is

effectively postponed as a result of the resolution (see also

TTMR 13:22).

German demand for African wood products worsen

In a recent report on German demand for African

hardwood, the trade journal EUWID notes that demand

worsened significantly in the closing weeks of 2008. Some

African exporters were cutting prices to German buyers in

an effort to obtain supply contracts but without much

success. EUWID noted that ��indications of actual prices

are rather vague as many importers simply have not placed

any new orders in Africa��. As a result, EUWID reported

that price quotes for standard lumber items are ranging

very widely. For example, FOB prices for FAS air dried

sapele lumber in random lengths are quoted in the range

EUR400/m³ to EUR500/m³ (down from EUR500-600/m³

at the end of September 2008). Equivalent prices for sipo

are quoted at EUR500/m³ to EUR650/m³ (down from

EUR650-EUR700 at the end of September 2008). EUWID

note that prices quoted for logs by African shippers to

German importers seem to be more stable but low levels

of actual purchasing make any meaningful assessment of

real market prices difficult.

No sign of light in UK plywood market

��Desperation to clear stock heightens competition�� - the

headline of the UK Timber Trade Journal��s most recent

report on the UK plywood market gives an idea of the

scale of the challenges currently facing the sector. Writing

in mid December, TTJ noted that ��in many cases

customers�� cheque books were locked away several weeks

ago and have not reappeared. It has become almost

impossible for plywood importers to quote a price that

would encourage a purchaser to buy ahead of the

Christmas period��. At that time, UK importers were offloading

stock as fast as possible, putting strong downward

pressure on landed stock prices. TTJ reported that offers of

Chinese plywood ��at very low levels��, supported in part by

the Chinese government��s decision to raise tax rebates on

plywood and other panels from 5% to 9% in an effort to

support export sales, had yet to have any impact on UK

purchasing decisions. Some of the UK��s largest importers

of Chinese plywood are believed already to be sitting on

several month��s stock and some of those that have placed

forward orders have been requesting delays to shipment

and even attempting to renegotiate contracts. TTJ notes

that prices for Malaysian plywood on offer to UK buyers

have also weakened on the back of the generally negative

market sentiment.

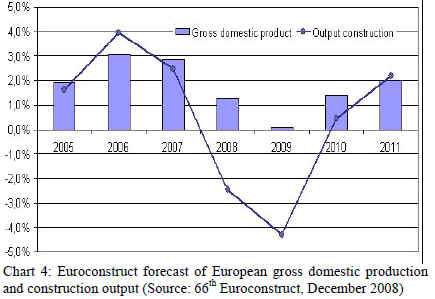

European construction holds out for prospect of longterm

growth

Given that the European construction sector is estimated to

account directly for around 70% of all European

consumption of wood products, future activity in this

sector to a large extent holds the key to future market

demand. A comprehensive forecast of future trends was

one outcome of the EUROCONSTRUCT Conference

which brought together 180 experts in early December.

This suggests that, despite the short-term gloom, there are

reasons to be optimistic about medium and long-term

prospects.

According to EUROCONSTRUCT, the construction

market in Europe is worth nearly 1,650 billion (thousand

million) euros, a figure which exceeds the entire GDP of

Italy. While much of the news surrounding European

construction in recent times has focused on the rapid

deterioration of residential construction in several western

European markets �C notably in Spain, the UK and Ireland

�C EUROCONSTRUCT highlight that this is only part of

the story.

EUROCONSTRUCT emphasize the huge variations in

construction sector activity that exist throughout Europe.

For example, Eastern European markets (Poland, Czech

Republic, Slovakia, Hungary) differ greatly from the

market of the Western countries. In the West, residential

covers nearly 50% of the market, while in the countries of

the East, civil engineering and non-residential construction

are more important. The average budget spent per capita in

construction in Western Europe is still three or four times

more than the spending made in the Eastern countries.

Nevertheless, according to the EUROCONSTRUCT

forecasts, Eastern Europe will be the focus for

construction sector growth in the short to medium-term.

EUROCONSTRUCT note that no European country will

be spared by the economic crisis, even in the construction

field. Construction output is falling or remains at best

positive in Western Europe for the 2008-2009 period.

Ireland and Spain are, in this respect, the countries most

affected by the crisis. These two countries excepted,

participants at the conference predicted growth of 0.2% for

2010 and nearly 1.5% in 2011.

In Eastern Europe, EUROCONSTRUCT forecast that

construction will continue to grow in 2009 but less

markedly than in previous years. Despite the global

economic crises, Poland is still going through a good

period thanks to work starting on large infrastructure

projects. What's more, from 2010, growth is expected to

be more sustained for all the Eastern countries.

EUROCONSTRUCT��s general analysis of the sector for

2009 shows that, until recently, it was above all residential

that was experiencing difficult times. Although nonresidential

escaped this negative trend for a while, it

appears that it is now caught in the storm. This trend will

also affect the civil engineering segment, which will see a

reduction in growth though most often without going into

the red. Again however, forecasts in this field are less

alarming for Eastern Europe.

The figures for renovation throughout Europe are expected

to follow a downward trend in 2009 but on a smaller scale

than the other segments of the sector. This is good news

for hardwood given that renovation projects often use a

relatively higher proportion of real hardwood products

compared to softwoods and other materials than new build

projects.

EUROCONSTRUCT are also optimistic about longer term

prospects, forecasting recovery in the sector from 2010

onwards. The rate of recovery will however vary widely

by construction segment. The first to get its head above

water should be civil engineering, closely followed by

renovation. On the other hand, no improvement in new

construction is expected until at least 2011.

EUROCONSTRUCT also note that the economic crisis is

not the only challenge currently faced by the European

construction industry. Other key factors affecting the

sector will be a forecast rise in demand for single family

homes and a general ageing in the European population.

And overshadowing all this is the strong and intensifying

political focus on combating global warming which is

expected to have huge repercussions on all the

construction segments.

Speakers at the Conference were unanimous in the view

that sustainable construction is an opportunity waiting to

be seized. The issue of global warming highlights the need

for infrastructure developments that can better withstand

climate fluctuations, for superior energy performance, and

for wider use of materials that sequester carbon.

EUROCONSTRUCT point out that in order to meet EU

targets for reduced greenhouse gas emissions over the next

half century, a large proportion of Europe��s existing

housing stock will have to be either renovated or replaced

to ensure they meet much higher insulation levels.

The medium and long-term opportunities implied by the

EUROCONSTRUCT forecasts for increased consumption

of wood, which is the most energy efficient building

material available, are obvious.

More information about the economic situation and course

of European construction can be obtained from two reports

(��Summary Report�� and the ��Country Report��) published

by EUROCONSTRUCT. These can be ordered them from

the organizer of the EUROCONSTRUCT conference

(info@aquiec.be).

|