|

Report

from

Europe, the UK

and

Russia

Economic indicators show deteriorating trend

Economic problems continue to mount in Europe. The

UK, Spain and Ireland were hit hard early on by the

collapse of their respective property markets. The UK��s

economy, with its heavy dependence on financial services,

has also suffered more profoundly than other economies

from the crises in the banking sector. Now contagion has

set in and conditions are deteriorating rapidly throughout

the EU.

Germany, France and Italy, the euro area��s three biggest

economies, have experienced a rapid decline in industrial

production in recent months as the strong euro and

weakening global demand has hit exports hard. Germany��s

industrial output fell at annualized rate of 15.1% in the

three months to November compared with the previous

three months; in France it fell by 14.5% and in Italy by

19.5%. Domestic consumption is also being squeezed

throughout the euro zone. Although the area��s consumers

have relatively high savings and low debt by rich-world

standards, they are becoming more nervous as

unemployment is rising. Consumer confidence in the eurozone

has sunk to a record low �C falling particularly

dramatically in Spain and Ireland.

Policy makers are trying desperately to avert the crises, so

far with little success. The Bank of England has reduced

interest rates to 0.5%, their lowest ever. The European

Central Bank (ECB) cut its key rate by 50 basis points to

2% on January 15th. Fiscal policy is being loosened

aggressively in a few countries, leaving the UK in

particular with a huge budget deficit.

Signs are that the European economy will remain

depressed for at least the rest of 2009, with tentative hopes

of a recovery in 2010. In January 2009, the Economist

Intelligence Unit forecast that euro area GDP would

contract by 2% in 2009 - a substantial downgrade from

December��s forecast of minus 1.2%. Much of this is due to

the deteriorating outlook for Germany, which is likely to

contract by more than 2% in 2009. Prospects in the UK

may be even worse, the IMF forecasting that the nation��s

economy might contract by 2.9% in 2009.

Until only a few months ago, reports indicated that Eastern

Europe might escape the worst impacts of the global

downturn. But economic conditions in the Baltic States

have a taken a serious turn for the worse. This has raised

concerns that the downturn might spread into other parts

of Eastern Europe. Industrial production in November

2008 in Latvia, Estonia and Lithuania fell respectively by

14%, 17.5% and 7%. In mid January, the IMF and other

foreign lenders had to step in to bail-out Latvia��s economy

imposing tough austerity measures as a condition of the

rescue package. Attention is now focusing on Poland, the

biggest regional economy, which until recently seemed

fairly safe. Industrial production in the country has nosedived

in recent weeks. The central bank has cut interest

rates sharply in response but it is too early to say whether

this will halt the slide.

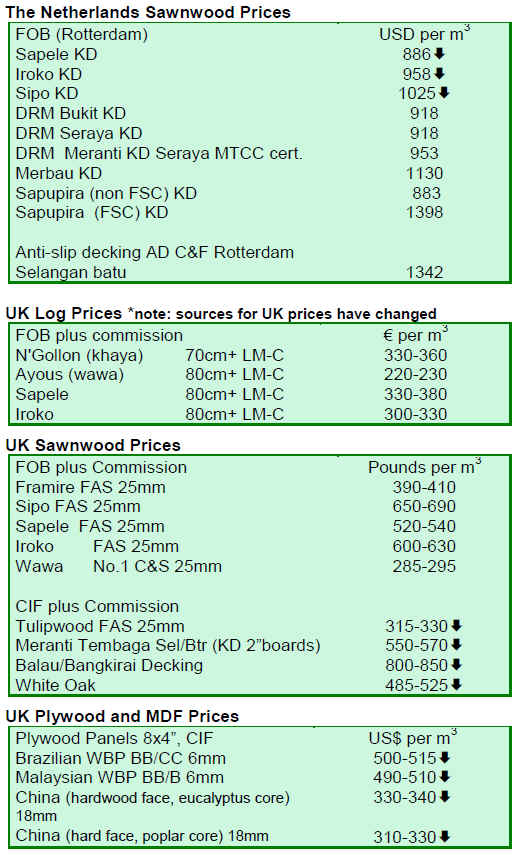

Sawn lumber market in the doldrums

Overall the European market for tropical hardwood sawn

lumber remains extremely depressed. There is very little

forward purchasing as importers focus on offloading

existing landed stock at a time when consumption has

slumped and prices are weakening. Agents report only a

slight pick-up in orders during the week immediately

following the end of the Christmas vacation, but these

tailed away very quickly in the following weeks.

Due to the extremely low level of forward sales, it remains

very difficult to obtain consistent and accurate price

information. There are a lot of very cheap offers around

but still buyers are not being tempted. Overall the feeling

is that landed stocks have been whittled down over recent

months with so little forward buying. But the serious lack

of confidence in levels of consumption this year -

combined with the widely held perception that prices will

remain weak and availability relatively prompt - is

deterring any move to build stocks.

This situation seems to apply across the board to the full

range of species, although the problems are most obvious

in the larger volume species. The market for African

sapele is particularly depressed as some large European

importers are selling on to manufacturers and other buyers

at well below replacement prices in their efforts to offload

excess stocks. Similarly USD CIF Northern Europe prices

for white oak �C such a staple of the European furniture and

joinery sectors �C are reported to have fallen by 30% in the

last eight weeks. Malaysian meranti USD CIF Northern

Europe prices have plummeted due to weak consumption

and efforts by Malaysian shippers to generate cash flow in

advance of the Chinese New Year.

Freight rates from the Far East into Europe have also

fallen by around 50% since early December �C a

particularly visible sign of the abrupt decline in European

trade volumes over the last three months.

Plywood trade stagnates

European plywood importers have greatly reduced

forward purchases and remain focused on stock

consolidation. There is much inter-importer trade,

particularly in the UK due to the weakness of GBP

sterling. With the currency so weak it makes sense for UK

importers to buy existing landed stock that was bought

forward by other importers in the middle of last year when

GBP sterling was stronger. There is very unlikely to be

any significant upturn in forward buying until sterling

recovers some of the ground it has lost to other currencies,

particularly the US dollar.

One large UK plywood importer interviewed in late

January notes ��our sales levels in the UK are around a

third less than the same time last year. Plywood is being

consumed and there will come a time when we need to

restock and buy more on a forward basis. However we are

not in that position yet, nor are we likely to be for several

months��. This same importer noted that his company may

be performing better than many competitors due to its

ability to supply more specialist products such as large

panels and marine plywood which are in relatively short

supply. It is those importers that rely more heavily on

large volume commodity products that are really

struggling.

This importer also notes that they are now buying little or

no Chinese plywood with a poplar core. This is due both

to continuing quality concerns and the fact that prices for

Chinese hardwood-throughout plywood have come down

to such an extent that the price of lower-quality poplar

core product is much less attractive.

Another significant impact of the downturn has been to

narrow the price differential between FSC and PEFC

certified and uncertified plywood products on offer to

European importers. As the overall market has contracted,

the relative availability of certified material has increased

and shippers have responded by reducing their certified

prices in an effort to maintain their market share. Those

shippers with access to material from certified forests are

aggressively marketing their products emphasizing that

they can provide environmentally certified product at little

or no price premium.

Although end user demand for FSC and PEFC labeled

plywood remains restricted in the UK, importers suggest

that more enquiries for these products are coming in,

particularly from the public sector. The UK authorities

seem now to be imposing more effectively the central

government procurement policy favoring ��verified legal

and sustainable�� timber. At the same time, the public

sector is becoming a relatively more important market as

private sector construction has declined. For this reason,

together with other factors such as ease of stock control,

brand protection and rising availability of certified product

at little or no premium, more UK plywood importers are

taking a strategic decision to shift over to sourcing 100%

FSC or PEFC labeled product.

EU garden furniture sector provides opportunities for

tropical timber suppliers

The garden furniture sector remains a major source of

demand for tropical hardwood products in the EU. Data on

the size of the sector in the various European countries is

not readily available, but anecdotal reports indicate that

Germany, France, Italy and the UK and the four largest

consumers of garden furniture products roughly in order of

importance. The market picture is complicated by the fact

that a significant proportion of the Top Quality Grade A

Teak imported into the Italian market is not used for

garden furniture but rather as decking for the luxury boat

building industry.

The European garden furniture sector is unusual for its

relatively high level of interest in environmental

certification. High profile environmental campaigns,

combined with the sector��s obvious dependence on

environmentally sensitive tropical hardwoods and the

relatively large volume of product sold through big name

retailers, have meant a very strong emphasis on certified

product. Many retail buyers in the EU will no longer

directly or indirectly purchase or offer uncertified timber

or wood products. With very few exceptions, FSC is

essentially the only brand of certification recognized in the

sector.

While big-name retailers have become more dominant in

the sector in recent years, there is still quite a high degree

of fragmentation. Huge volumes are sold through

companies like Metro in Germany, Carrefour in France,

B&Q, Homebase, and Tesco in the UK. But significant

volumes also find their way to final consumers through

smaller garden centers and internet firms.

Large retailing companies often buy a significant

proportion of finished products direct from the Far East.

Direct buying normally generates a much higher margin

for a retailer. However there are also risks associated with

buying direct and paying for goods well in advance of

delivery. Therefore a proportion may also be bought from

EU branded companies who can offer stock support in the

EU with a quick repeat order delivery time.

There are a large number of European ��pseudo

manufacturers�� who are now in effect importers and

wholesalers supplementing the large retailers�� supplies and

also acting as a major source of goods supplied to the

smaller garden centers and retailers. Pseudo manufacturers

usually operate by supplying a design to a Chinese or SE

Asian producer who then makes the furniture under the

brand name of the pseudo manufacturer. Occasionally the

factory design is used. Quite often a pseudo manufacturer

acts on behalf of a retail buyer.

There are only a very few garden furniture companies

actually manufacturing products in the EU and most use

materials other than wood. For example Kettler still

produces steel garden furniture in the EU while importing

their wooden furniture from SE Asia.

Teak is generally the preferred species in the garden

furniture sector, although lack of availability of this

species combined with the strong emphasis on ensuring

products are FSC certified has meant the sector now

utilises a wide range of alternatives. Of tropical species

these include iroko, eucalyptus, acacia, balau, meranti,

keruing, shorea, sindana, and couboril. Lack of availability

of FSC certified teak from Myanmar and Indonesia has

contributed in recent times to a shift in sourcing of wood

raw material to other regions, for example from teak

plantations in Central America, Eucalyptus plantations in

South Africa, Acacia plantations from Vietnam and other

SE Asian countries, and couboril from Brazil. In addition a

lot of FSC certified pine from Russia, Northern Europe,

North America and New Zealand is now pressure treated

to extend its life for outdoor use.

Until the start of last year, the EU garden furniture sector

was generally expanding. However in 2008 the wet

summer in north-west Europe undermined demand. The

worldwide economic downturn then severely dented

confidence. Many retailers continue to hold excess stocks

over from the 2008 season and, lacking confidence in a

significant recovery this year, have drastically reduced

forward ordering for the 2009 season.

Another effect of the economic downturn has been to

contribute to growing interest in lower priced products

especially lower grade plantation teak, Acacia and

Eucalyptus. With cost becoming an even bigger driver of

demand in difficult trading times, there is growing concern

amongst manufacturers over the continuing price

differential that exists between FSC certified and

uncertified raw material suitable for garden furniture

manufacture. Concern is particularly pronounced as the

downturn also seems to be encouraging more interest in

relatively cheap non-wood products including no or low

maintenance aluminum, steel and mixed material furniture

mainly from China.

|