|

Report

from

Europe, the UK

and

Russia

No change in depressed market conditions

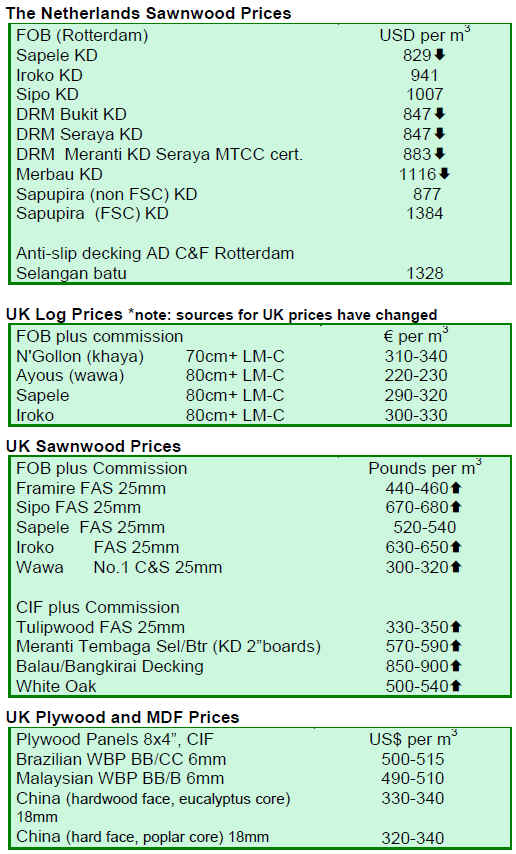

There is little change in the European market for tropical

sawn lumber. There is still very little forward demand for

sapele, the main commodity species, as large importers in

the UK and the Benelux countries continue to off-load

stocks at below replacement value. Due to very slim

margins, there is very limited incentive for importers to

engage in trade in this species �C as one major UK importer

commented recently ��I haven��t made any money on sapele

in over a year��. He noted that the same could be said of

sipo, although a few other lower volume species have been

performing a little better, for example iroko and framire.

Confidence has been obliterated throughout a large swathe

of the European hardwood importing trade. This combined

with continuing lack of access to credit and insurance

cover has meant that the focus is still on reducing stocks �C

despite the clear evidence that supply further down the

pipeline has been greatly reduced.

There is however a feeling that prices are now very close

to the floor, if not already there. A frequent comment by

European agents is that with the so little buying for so

long, forward prices could rise quite dramatically in the

second half of the year if importers do at last turn their

attention to replenishing their depleted stocks.

Market perspectives from Ecobuild: Tropical

hardwoods left on the bench while others score

The Ecobuild event held in Earl��s Court, London, from 3-5

March reaffirmed that environmental issues are likely to

play a key role in the UK construction sector despite the

economic recession. This year��s show featured 800

suppliers from across Europe, a very impressive increase

on last year��s 500 exhibitors given the current climate.

Judging from the crowds, the show is likely to have

achieved the organizers�� pre-show estimate of over 30,000

visitors, breaking last year��s record of 26,000.

High levels of interest in the show reflects both the strong

focus on sustainability and green issues that now pervades

the UK architectural and design professions together with

a host of recent UK government initiatives aimed at

boosting green performance in the construction sector.

Behind many of these initiatives lies rising concern for

energy efficiency as the UK �C like all other EU countries -

struggles to reduce carbon emissions in line with

international Kyoto commitments. Conformance to the UK

government��s Code for Sustainable Homes (CSH) became

mandatory for all UK housing developments in May 2008.

CSH sets minimum standards for energy efficiency and

provides UK homebuyers with information about the

environmental impact of their new home.

The timber industry was strongly represented,

participation being boosted by the Timber Works pavilion,

an area dedicated to first-time exhibitors and supported by

various UK timber trade associations. The clear message

coming across from the timber sector was that increased

use of timber can make a major contribution to sustainable

construction. A huge range of highly technically advanced

wood products and wood-based construction techniques

were on show, driving home the message that timber is the

material best placed to meet the challenges of 21st century

construction �C that is combining rapid and cost effective

building methods, lasting technical performance and

beautiful structures with unbeatable environmental

credentials.

One particular highlight was the Eco house, a family home

built in wood to very high energy and environmental

standards in the space of only one week in 2008 during a

live edition of Grand Designs, a hugely popular UK prime

time TV show. Other highlights were ZedFactory��s timber

frame Zero Carbon House; KLH��s Carbon Neutral

Construction method comprising a honey-comb of solid

timber panels recently used for construction of a 9-storey

apartment block in London in the space of only 29 weeks;

and JELD-WEN��s launch of DreamVu, the UK��s first

volume made timber window to achieve a U-value of 0.7-

1.0W/m²K.

The strongest hardwood presence was the American

Hardwood Export Council (AHEC) with a large stand

featuring a new pavilion in tulipwood designed by a

leading UK architect. The pavilion demonstrates the

beauty and versatility of this abundant American species.

AHEC has been working with Osmose, a UK based

preservative treatment company to extend utility of the

species to external applications.

Other materials closing the green gap on timber

While timber maintains a strong reputation as the green

material of choice, the Ecobuild show also emphasized

that other material sectors are intent on closing the gap and

are now scoring green points.

The plastics industry highlighted the recent achievement

of an A-rating for uPVC windows in the Building

Research Establishment (BRE) Green Guide, now a key

reference for green procurement in the UK construction

sector as it is integrated into the CSH. The A-rating means

that uPVC windows are now regarded by BRE as just as

environmentally-friendly as wood windows. BRE justified

the A-rating at an Ecobuild side-event, pointing to the

efforts of the plastics industry to recycle a higher

proportion of windows at the end of their life-cycle.

However, participants at the event also noted that it is

difficult to judge the objectivity of BRE��s rating as their

methodology lacks transparency and the baseline data is

not publicly available.

BRE were also playing a leading role at Ecobuild to prop

up the dubious environmental claims of the UK aggregates

industry �C which like the plastics industry has set its sights

on undermining timber��s lead on sustainability issues. The

UK aggregates industry promoted itself at Ecobuild as ��the

Responsible Source��, a claim largely dependent on their

anticipated conformance to a new BRE ��Responsible

Sourcing Standard��. The process to develop the BRE

standard, which was chaired by Tarmac �C a large UK

aggregates supplier - was rushed through despite stiff

opposition from the timber sector to fit with the

procurement timeline for the London 2012 Olympics

(which requires that all materials be ��responsibly

sourced��). The BRE standard is now being used by the

aggregates sector as a tool to neutralize the wood

industry��s sustainable source message.

Tropical hardwoods must be FSC certified

Ecobuild��s message to the tropical hardwood sector was

��if you want to participate in this market, make sure you

are FSC-certified �C and even then watch your back��. This

is well illustrated by the Wood Window Alliance which

led the UK wood window sector marketing drive at the

show. The wood window sector should be strong

marketing territory for tropical hardwood, these being the

only wood products able to perform well in exterior

applications without the need for fossil-fuel intensive

chemical or heat treatments. But the message from the

Wood Window Alliance was a negative one. Rather than

seeking to defend the use of tropical wood, the Alliance��s

approach was to deny their continuing role in the UK

industry.

The Alliance��s ��Specifiers Guide to Timber Windows��,

which featured at Ecobuild suggests that ��tropical

deforestation is a major contributor to CO2 emissions and

global warming�� without bothering to qualify this with any

statement about the distinction between forest conversion

and sustainable tropical forest management. This error is

then compounded in the Guide with the inaccurate

observation that ��timber from tropical forests is rarely, if

ever, used by UK wood window manufacturers�� �C a fact

easy to disprove by a short conversation with any one of

many wood window manufacturers at Ecobuild who

confirmed their continuing use of sapele, meranti and a

range of FSC certified tropical hardwoods.

Many window companies participating in the show �C

which included just about all the major UK manufacturers

- did confirm that that they now require independent

certification, preferably FSC, of all their wood supplies.

They have been driven to this by the UK government��s

commitment to ensure that all their wood is ��legal and

sustainable�� and by internal management issues which

mean that if you supply certified wood to one major

customer and certified raw material is sufficiently

available, it is simpler to switch over to 100% certified

production.

Many window manufacturers noted that while they still

supply small volumes of sapele and meranti product, they

have also made a concerted effort to transfer to nontropical

substitutes that are more readily available FSC

certified. These substitutes included plantation grown

eucalyptus from South America and South Africa, and a

range of heat-treated softwood products from Scandinavia

and New Zealand. While the latter are still available only

in relatively small quantities, prices are competitive

against tropical hardwoods, particularly as all are provided

FSC certified as standard. Their performance is also

extremely strong �C one manufacturer noted that he is

willing to offer a 50-year guarantee for his heat-treated

softwood product, compared with a 40 year guarantee for

his tropical hardwood products.

Heat-treated pine products were also providing tropical

hardwoods a run for their money in other sectors. The

number of companies offering these products as

alternatives to tropical decking, flooring, cladding, and

other components is mushrooming. All the major UK

hardwood importers are now diversifying into these

products. Examples of heat treated branded products

include Lignia and Lunawood.

The flooring products on show highlighted the continuing

strength of the fashion for oak �C a fashion that the

manufacturers are building on and extending by offering

oak products in huge diversity of finishes and stains. They

are responding to a fashion for darker colors not so much

by procuring tropical hardwoods, but rather by steaming or

staining oak to a color that is almost black. This trend is so

entrenched that one European flooring supplier at the

show said his company is now sourcing product

manufactured from German oak in Indonesia.

Mounting competition from non-wood substitutes

Furthermore competition from other non-wood sectors is

mounting. The plastics industry seemed to have

particularly set it sights on the tropical hardwood sector,

developing look-alike products for exterior applications,

such as garden furniture and boarding. A company called

Ecogenic was promoting a new product manufactured

entirely from recycled plastic that would replace tropical

hardwood plywood in non-structural exterior applications

(notably hoardings). Two plants each capable of churning

out 400,000 panels of the new product each year will be

set up in the UK during 2009.

Particularly worrying for the tropical sector, is that these

competitors seemed to be playing to a receptive audience.

There was a strong feeling amongst architects, designers

and specifiers, that the key environmental issue at present

is the ��carbon footprint��. This was linked to a preference

for any product ��locally produced�� and not perceived to be

transported over long distances. It also contributed to a

strong aversion to tropical hardwoods amongst many

people contacted at the show. There was a simplistic

assumption that tropical hardwoods are closely associated

with deforestation and therefore linked to increased

emissions.

There seemed to be nobody at the show willing to explain

the inherently strong environmental credentials of

sustainably produced tropical hardwoods. Even those

marketing FSC certified tropical hardwoods appeared

determined to muddy the message. The headline

marketing message of one flooring supplier specializing in

FSC certified products was ��Did you know that the UK is

the second largest importer of illegally felled timber in the

EU��.

People like tropical hardwoods �C they just don��t know it

There were a few crumbs of comfort for the tropical wood

sector at Eco-build if you were willing to look hard

enough. JELD-WEN, the UK��s largest joinery supplier by

a significant margin, was displaying some high quality

Malaysian-manufactured windows and doors. The JELDWEN

representatives, when asked, were very ready to

comment on their Malaysian suppliers�� reliability and

quality. The only problem was that the doors, while

backed by a meranti engineered wood product, were faced

with American cherry, while the meranti window frames

were painted clear white. It seems that, as things stand,

many UK buyers are happy to exploit the superior

technical attributes of tropical hardwoods, just as long as

they remain hidden.

European Parliament pass verdict on illegal logging legislation

Moves to introduce new legislation into the EU that would

require forest products operators to take steps to minimize

the threat of illegal wood entering supply chains are at a

critical phase. The European Parliament Committees

responsible for the considering and amending the draft

legislation before voting by a full plenary session of

Parliament, due on 23 April, have just passed their verdict,

proposing substantial amendments.

One view of the amendments proposed by the

Parliamentary Committees was expressed by WWF and

Greenpeace, who immediately welcomed the move,

suggesting the amendments represent a significant

strengthening of the original proposal. Greenpeace said

that the proposed changes would ��make the timber

industry accountable and set up an effective system to

control the legal origin of wood��. Many of the

amendments originated from Caroline Lucas, MEP and

leader of the EU��s Green Party, so it is perhaps not so

surprising that green campaigning groups are so

supportive.

But according to another view, the Parliamentary

Committees were poorly advised, failed to grasp the

underlying concept behind the original proposal, and as a

result missed a real opportunity to implement more

rational improvements. The amendments proposed by the

Committees effectively turn a fairly moderate proposal to

extend the practice of due diligence amongst operators that

��first place�� timber on the EU market into a system of

rigorous state control over the entire European wood

supply chain.

The Parliament��s amended text proposes that the central

objective of the EC��s original proposed legislation be

changed so that all forest products operators in the EU

would be placed under an obligation to prove the legality

of the wood they deal in. The intent of the original

proposal �C that extra requirements for traceability and

certification would only be required where there is a high

risk of illegal wood entering supply chains �C would be

lost. The Parliament��s amended text might be costly to

implement and require an army of technically qualified

chain of custody personnel that is currently absent. The

suggested measures may also be regarded as poorly

targeted - wasting time and resources on tracking wood

from all areas when it might be better to focus on a limited

number of high risk supply chains.

Whether or not the draft legislation is eventually adopted,

and the form it finally takes, remains to be seen. The

legislation is being considered under the EU��s convoluted

��co-decision�� procedures. These require that the legislation

must be agreed both by the European Parliament (directly

elected by the EU population) and the Council of

Ministers (representing the EU Member State

governments). It is usual practice under this procedure for

the Parliament to propose a long ��shopping list�� of desired

outcomes, which is then adapted into a more realistic

compromise framework following input from the Council

of Ministers �C the members of which actually have to take

responsibility for implementing the legislation.

��

|