|

Report

from

Europe, the UK

and

Russia

European hardwood market still in a slump

Consumption in the European hardwood market continues

to slump on the back of poor economic news and

uncertainty, lack of bank credit and the restrictive policies

of credit insurers.

Despite very low levels of production in Africa, such is the

weakness of international demand that European buyers

report that new orders can still be placed with African

mills at short notice, with delivery times of no more than

two to three months. Prices seem to have hit the floor, the

mills having no margin for further downward movement

and little incentive for reductions now that stocks are at a

low level. However, European importers are generally

vague about forward price levels since so few have made

any significant purchases over recent months.

Stock levels of most African hardwoods remain high in

Europe. Some larger importers are continuing to offload

this stock at below replacement cost so there is little

incentive to enter the forward market. Orders for onward

sale into the European market are generally small, and

importers holding heavy stocks are still willing to offer

sizeable discounts for those willing to take larger volumes.

European forward demand for sapele, both logs and

lumber, has been particularly weak. However consumption

of other species has been a little more active. Such is the

lack of confidence in Europe��s joinery and furniture

manufacturing sectors, that even Gabon��s ban on the

harvesting of douka, ozigo, moabi, and afo from 1 January

2009 has done little to stimulate demand for the remaining

stocks of these species.

The demand for Asian species is no better. Although there

are some reports of increased enquiries since the start of

the year, these have not been translated into significant

new orders. As with Africa products, European importers

seem to have no difficulty obtaining the limited stocks

they require at relatively short notice despite evidence of a

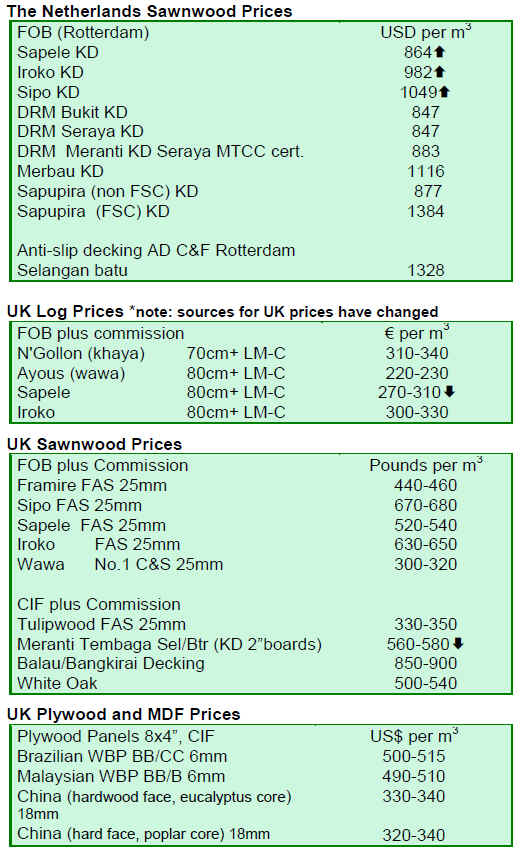

sharp decrease in production levels in South East Asia. US

dollar forward prices for meranti lumber and window

scantlings have weakened again slightly in recent weeks,

although prices for selangan batu/ bangkirai decking

profiles seem now to have stabilized after losing a lot of

ground at the end of last year.

European plywood demand ��terrible��

The opening words of the TTJ��s report on the demand for

plywood in the UK, the largest importer of this commodity

from outside the EU, say it all: ��The state of demand in the

plywood industry is terrible and is getting worse��. TTJ

reckons that for the UK plywood industry, 2009 may be

��the toughest year in its history��.

The dire state of the UK construction sector has meant that

importers and agents find themselves with no orders,

despite efforts to generate demand through cheap offers.

Those carrying stock are desperate to offload in order to

maintain cash flow. But many distributors, faced with an

almost total lack of end user consumption, have cut back

on purchases to such an extent over the last six months

that they hold near zero levels of stock. TTJ quotes one

importer who suggests that he has gone from bringing in

40 containers a month to just two.

It is entirely a buyers market, with clients being very

particular about what they want and the specific (always

small) quantity required. The lack of orders seems to be

affecting all parts of the trade. There has been no pick up

in Brazilian plywood imports despite these being duty

exempt into Europe until the end of April. There are a few

agents that are a little more positive �C one suggesting that

the market should bottom out in April-May, with a bit

more consumption in the spring months balancing the

existing low levels of supply.

European window sector shows a few bright spots

The German trade journal EUWID comments that

��German window scantling manufacturers and major

importers still have a relatively optimistic view of the

future. In Central Europe demand for window scantlings is

said to be generally satisfactory, especially for high quality

and heavier assortments. Prospects for the rest of the year

are considered to be relatively positive for Central

European countries: here recently announced state

economic stimuli packages are expected to stimulate

demand for energy-saving renovation work on windows.

However no improvement is in sight in the UK, Ireland,

Spain, or Eastern Europe��.

European traders push for verified legal products in Indonesia

At the end of March, European timber trade

representatives visited Indonesia to discuss the need for

independently audited wood products to meet new

international market demands. A group of timber trade

representatives led by the UK Timber Trade Federation

met timber industry leaders from Indonesia to discuss how

new timber trade regulations and policies are toughening

up demand for verified legal and certified timber.

Asian exporters face new challenges in meeting

international market requirements; US and EU legislation,

and public and private sector purchasing policies are now

combining to make independently audited legal and

sustainable timber a requirement for continued access to

those markets.

Over 100 Indonesian timber and furniture producers

attended a national trade forum in Kemayoran, Jakarta to

hear how international markets for timber are changing.

The US government��s amendment of the Lacey Act has

now made it illegal to import illegal timber into the US.

The EU is currently finalizing its ��due diligence��

legislation that will require all EU importers to assess their

timber sources and eliminate illegal timber from their

supply chains. Both are responses to Indonesian

government calls for international legislation to eliminate

the trade in illegal timber.

This demand is now being pushed by new EU Green

Procurement Guidelines and EU Member State

governments�� timber procurement policies that dictate

buying decisions for at least 20% of the EU market. More

importantly, buyers are paying a small premium for such

timber. In addition, delegates heard that negotiations for a

new EU-Indonesia timber licensing agreement (the

Voluntary Partnership Agreement) are likely to continue

with the objective of concluding the deal by July 2009.

Once agreed, the scheme would guarantee the legality of

all Indonesian timber exports and would have important

market implications for Indonesian producers.

Responding to this matter, Ambar Cahyono, Asmindo

Chairman said, ��Asmindo supports all forms of

cooperation, certification and legalization, [which] is why

Asmindo is very concerned about public forest

certification to fulfill market demand. It is hoped that it

will give a certain value that is profitable and production

value to the organization��s members to make a

breakthrough into the international furniture market��.

Rachel Butler, UK TTF explains: ��The TTF is on the

industry��s side; we want a sustainable timber trade

because we believe in timber and we are committed to

supporting our suppliers to meet the changing

requirements in the EU and UK��.

European timber buyers have heard the good news that

Indonesian industry is well placed to meet this challenge.

Independent auditing of current timber harvesting under

various private sector schemes meets requirements for

legality in most sensitive international markets. Once the

new national scheme requirements are known,

modifications in business practice for those companies

currently operating legal verification schemes should be

minimal. For further information contact Rachel Butler of

TTF (rbutler@ttf.co.uk).

FAO comment on economic crisis and wood sector

The State of the World��s Forests 2009 report issued by

FAO in Rome earlier this month comments on the possible

long-term impact of the on-going economic crisis on the

world��s forests and wood sector.

FAO note that the collapse of the housing sector in

western countries has reduced demand for a wide array of

wood and wood products, leading to mill closures and

unemployment. New investments are slowing as a result,

affecting all wood industries. The demand for

environmental services has also changed as a result of

reduced ability and willingness to pay for such services.

Carbon prices have remained highly volatile. Future

climate change arrangements may face challenges as

countries give priority to tackling the economic crisis.

FAO are concerned that this might have negative impacts

on forest resources through, for example ��reduced

investment in sustainable forest management and a rise in

illegal logging as the decline in the formal economic

sector opens opportunities for expansion of the informal

sector. Land dependence, which had been easing, could

increase, raising the risk of agricultural expansion into

forests, deforestation and reversal of previous forest

gains��.

But there could also be positive impacts: ��reduced wood

demand could lessen pressure on forests, while conversion

of forest for large scale cultivation of commercial crops

such as oil-palm, soybeans and rubber could slow as their

prices fall��. The forest sector could benefit from the

pursuit of a ��green path�� to development �C through

building up of natural resource capital (e.g. through

afforestation and reforestation and increased investments

in sustainable forest management), generation of rural

employment and active promotion of wood in green

building practices and renewable energy. Certainly, this

change of path will require fundamental institutional

changes, but the crisis may bring about greater willingness

to accept and implement long-overdue reforms��.

The report is available at:

http://www.fao.org/docrep/011/i0350e/i0350e00.htm

��

|