Overview of global wood pellet markets:

historic and future demand

Written by William

Strauss, FutureMetrics

The past few years have been challenging for wood pellet producers

and pellet production project developers. A temporary plateau in

demand growth for new co-firing or full conversion power plant

projects in the industrial pellet market has led to an excess of

production capacity. A series of warm winters in Europe compounded

by low fossil fuel prices have depressed demand for pellets and new

pellet stoves and boilers in the heating pellet markets. What will

the future bring to the wood pellet markets? This article will try

to answer that question.

Wood pellet markets comprise two primary sectors: industrial wood

pellets that are used as a substitute for coal in power plants, and

premium pellets used in pellet stoves and pellet boilers for

heating.

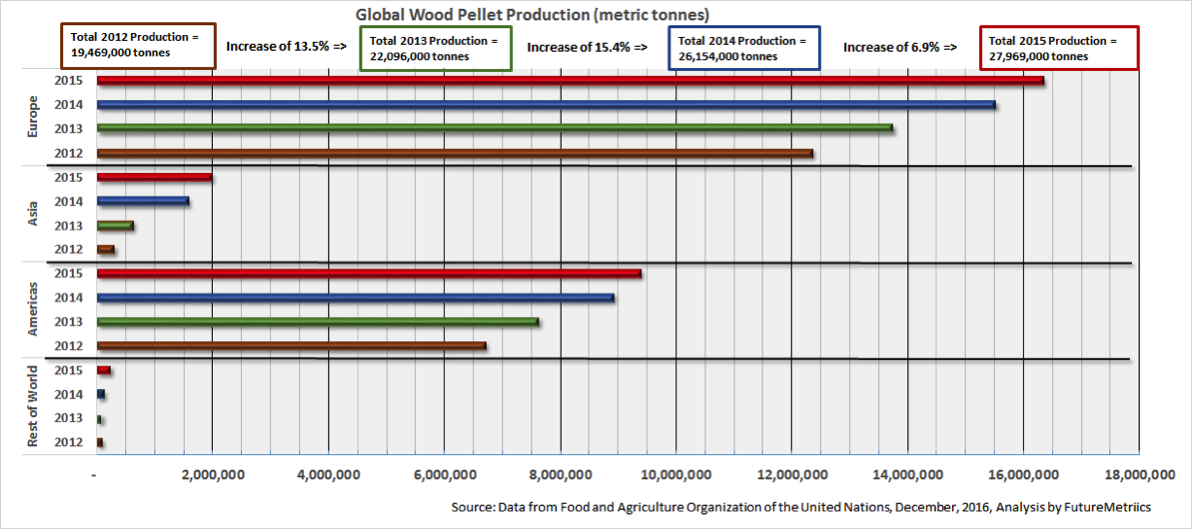

Global wood pellet markets, both the heating and industrial sectors,

have had significant growth in the past decade. Growth rates over

the most recent four years of data has been about 10 per cent

annually; from about 19.5 million metric tonnes in 2012 to about 28

million metric tonnes in 2015.

Industrial wood pellet markets

The industrial wood pellet market is expected to grow significantly.

The chart below shows the historical actual demand and forecast

potential demand for the industrial wood pellet markets. Current

(2016) aggregate demand for industrial pellets is estimated to be

about 13.8 million metrics tonnes per year. That is the equivalent

of a large bulk carrier ship carrying 40,000 tonnes about every day.

.

Future demand in the U.K. and E.U. is expected to plateau by 2020. However major growth is expected in Japan, and Korea in the 2020s. Canada has the potential to experience increasing demand for industrial pellets. That is due to decarbonization policies from the Canadian federal government and specific policies in provinces such as Alberta. FutureMetrics has two recent presentations with details on the forecasts for Canada and Japan. The presentation on the Canadian markets with a specific focus on Alberta is HERE. The presentation about the Japanese markets is

Over the 15 years from 2010 to 2025,

the average annual increase in demand for industrial wood pellets is

expected to be about 2.7 million metric tonnes per year.

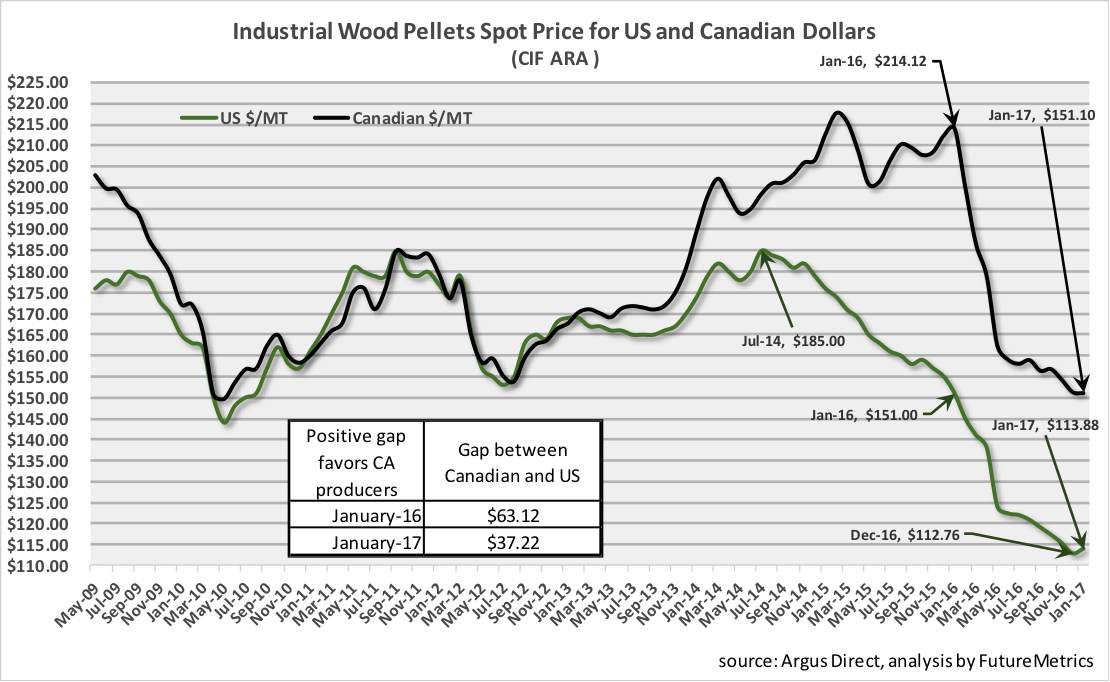

Presently, there are too many pellets chasing too few buyers. The

buildup of production capacity based on demand forecasts from a few

years ago has resulted in a current state of excess supply in the

industrial wood pellet sector. As a result, spot market prices for

industrial wood pellets have hit historical lows.

The industrial pellet oversupply is

compounded by increased production in eastern Europe and decreased

demand for heating pellets in Europe due to above average

temperatures the last three winters. But with several large power

stations – Lynemouth and MGT in the U.K. and Langerlo in Belgium –

coming online in 2018, the oversupply will be soaked up by the new

demand. Drax’s unit 1 will be full-firing (from 85 per cent

co-firing) very soon, adding about 330,000 tonnes per year of

increased demand. As of early January 2017 it is still unclear if

the Dutch markets will begin co-firing. If they do, new industrial

pellet demand could increase by an additional 3.5 million tonnes per

year.

That new demand, combined with growth in the Japan and South Korea,

will soak up the current excess capacity and is expected to bring

CIF ARA (cost, insurance and freight in the

Amsterdam-Rotterdam-Antwerp area) spot prices back into line with

the long-term averages.

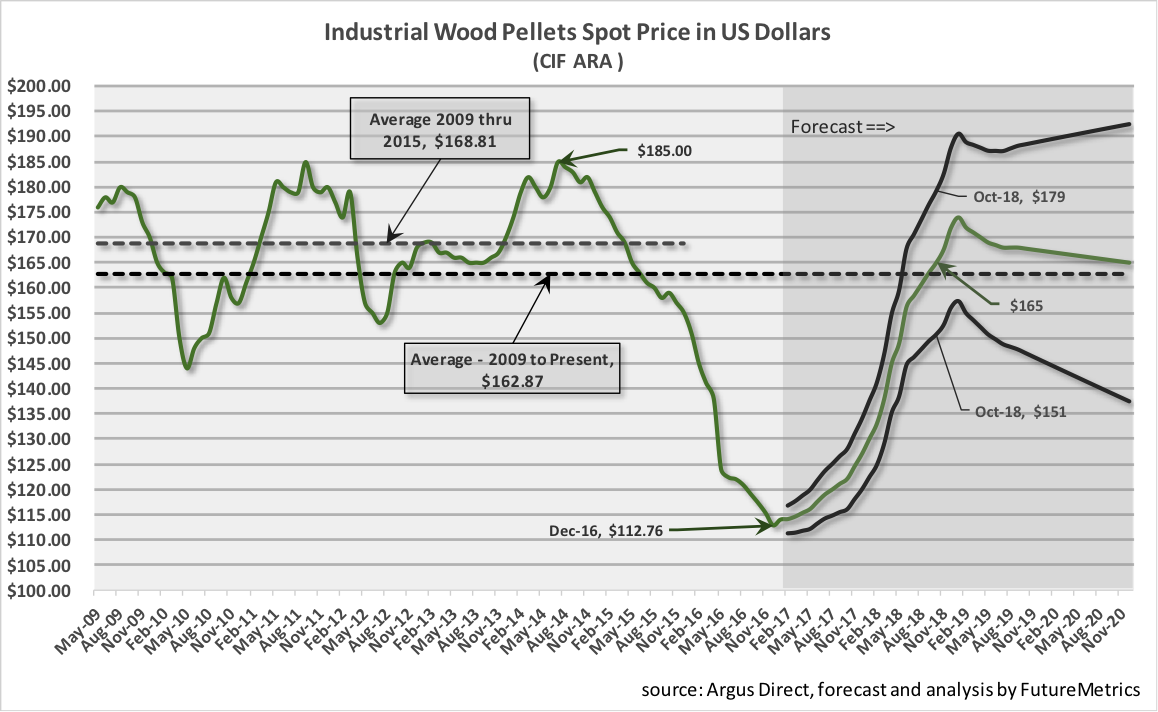

The forecast assumes that the

supply/demand disequilibrium that currently exists is corrected

after several large pellet-consuming projects described above come

on line. The forecast also assumes that production capacity will not

exceed demand and that the heating markets absorb normal quantities

(i.e., normal winter temperatures).

China?

There is major uncertainty regarding the Chinese markets for pellet

fuel both in terms of potential demand and in terms of how much

pellet fuel could be produced domestically. On one hand, they have

very limited forest resources for producing wood pellets. On the

other hand, they have almost unlimited agricultural wastes that

could be made into pellet fuel.

Using ag-waste for pellet fuel has many challenges. The big issue is

that ag-wastes are high in abrasive silica and corrosive chlorine.

Both are highly problematic for utility pulverized coal boilers. At

low co-firing levels, those issues might be diluted to a level that

is acceptable. But at higher co-firing rates non-purpose built

boilers that are not designed for ag-wastes cannot use ag-pellet

fuel.

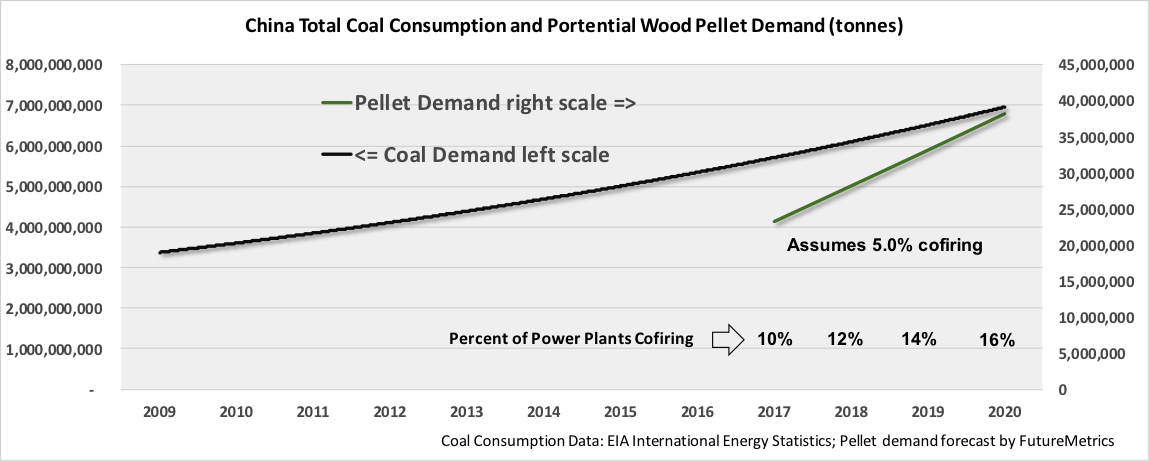

The 2016 to 2020 five-year plan has explicit support for pellets. If

China were to embrace co-firing of wood pellets, even at modest

ratios, the internal demand would be very large. The chart below

shows that at a five per cent co-firing rate, in 2020 if only 16 per

cent of China’s coal power plants are co-firing, demand would be

almost 40 million tonnes per year.

What will happen in China over the

next few years with respect to wood pellet demand is very uncertain.

If that market opens up to foreign imports of wood pellets, it will

not only be massive, but depending on their requirements for

sustainability (or not) it could be disruptive.

Heating wood pellet markets

The heating pellet sector has grown steadily in the past decade.

Unlike the industrial pellet sector which is policy driven, the

heating pellet markets are primarily driven by the comparative costs

of heating fuels. Pellets have historically been the lowest cost

fuel for heating in most regions. Low crude oil prices and therefore

low heating oil and propane prices have recently challenged pellets’

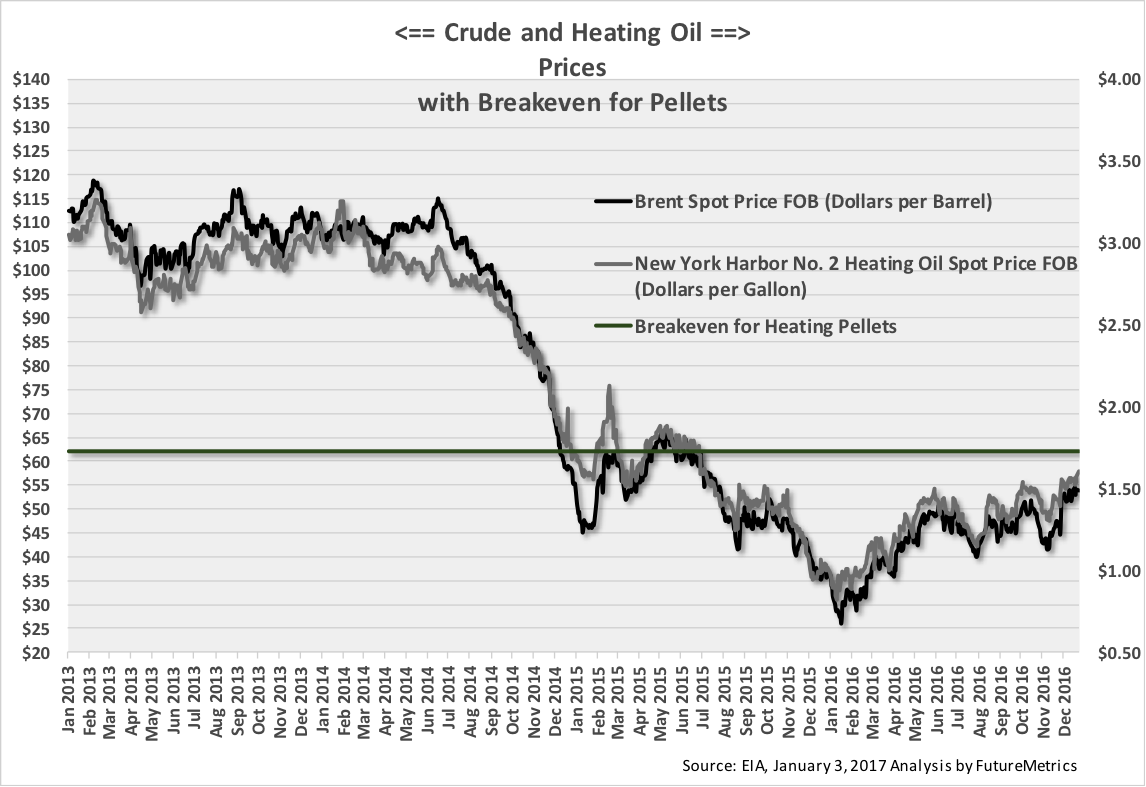

position as the lowest cost heating fuel. The chart below shows the

recent price history of crude oil and heating oil and further shows

that at about $62.50 per barrel, heating oil prices will be about at

breakeven with wood pellets for the equivalent energy (assuming $245

per ton pellet price). Retail heating oil prices are at least $0.50

per gallon higher than the NY harbor spot price shown in the chart.

In some jurisdictions retail heating oil prices are nearly

$1.00/gallon higher than the NY harbor prices.

If recent trends in crude oil prices

continue, pellets will soon again be the lowest cost heating fuel.

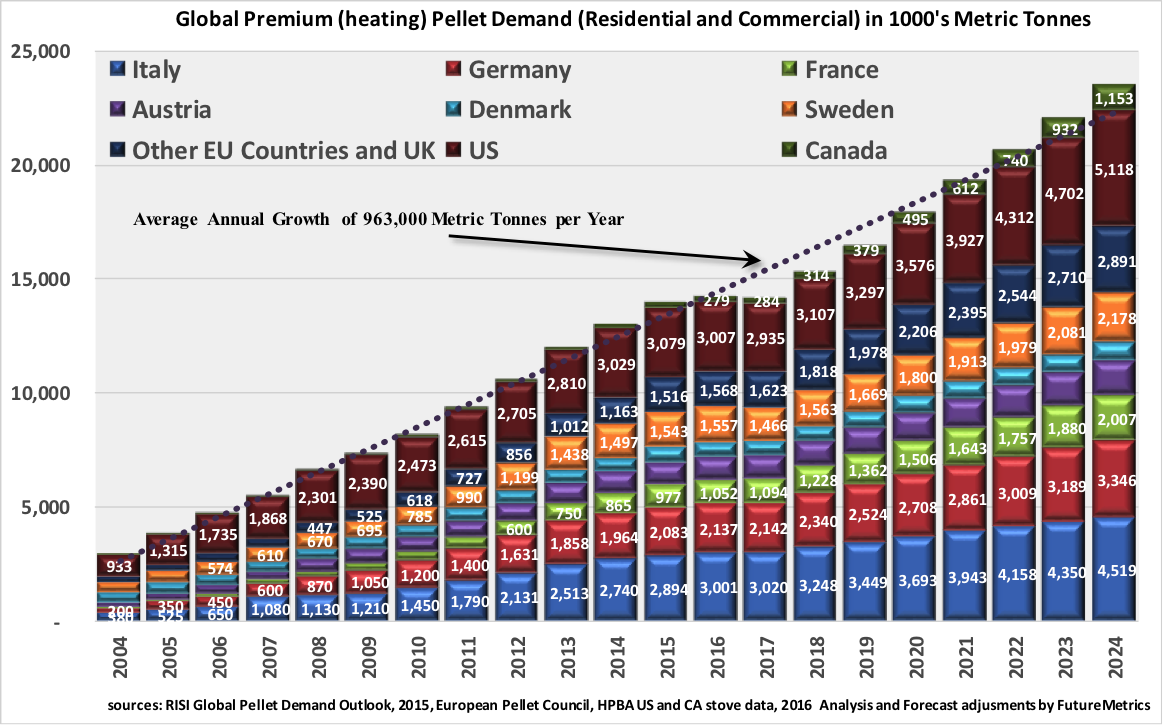

The final chart in this article shows historic and forecast demand

for heating pellets in the major countries that use pellets for

heat. The chart shows the current and expected below trend growth in

the global premium heating markets for 2015-2017. The below-trend

growth is a result of several warmer-than-average winters and low

crude oil and heating oil prices.

Based on expected petroleum prices from 2018 onwards it is likely

that the heating pellet markets will resume their traditional

growth. The heating markets are forecast to have an increase in

demand of about 9.5 million metric tonnes per year from current

levels by 2025.

Conclusion

The fundamentals for significant growth in the heating markets are

sound. The near-term challenge is the cost of alternative heating

fuel.

In most of Europe, where many countries have high taxes on heating

oil, demand is more driven by weather than by oil prices.

In the U.S., heating pellet market growth is highly correlated to

heating oil prices (and to propane prices in the Midwestern states).

The larger the gap between the breakeven price of heating oil versus

pellets the more demand for pellets grows as pellet stove and boiler

sales increase. Weather always will create variation around the mean

annual demand; but higher growth depends on oil prices rising above

about $63 per barrel.

The Canadian heating pellet markets are relatively small. But in a

few provinces, there is potential for significant growth. A

FutureMetrics published a paper on the subject that can be

downloaded

HERE.

The industrial pellet markets are all about carbon emissions and

renewable energy policies.

The E.U. and U.K. markets are expected to plateau in the early

2020s. The industrial wood pellet market needs to look beyond U.K.

and E.U. demand to find growth in the next decade.

The areas in which 2020s and beyond offer significant industrial

pellet demand growth are Japan, Korea, and potentially China.

Japanese policy as it stands today will generate millions of tonnes

per year of new demand; and could generate tens of millions of

tonnes per year.

A press release from

Argus Direct on Jan. 4, 2017 notes that South Korea plans to

increase investment in alternative energy sources by about 25 per

cent to almost 14 trillion won ($11.6 billion) this year. South

Korea is the Asia-Pacific's biggest importer of wood pellets.

According to the Korea Forest Biomass Association, its imports may

climb from 1.5 million tonnes in 2015 to more than 8.5 million

tonnes in 2022.

The U.S. had the potential to generate tens of

millions of tons of pellet demand by 2030 if the Clean Power Plan

had been implemented. Under the Trump administration, the CPP is

expected to be abandoned. There is still a chance that the U.S.

could implement policy that would support the use of pellets in

coal-fired power plants. A recent white paper explains how and can

be downloaded

HERE.

The expectations for the future of wood pellet markets are

optimistic. If our forecasts are correct, more than 30 million

tonnes per year of new demand by 2025 will drive more than $7

billion of investment in new production capacity worldwide.

---------------------------------------------------------------------------------------------------------------------------------------------

William Strauss, PhD, is the president of FutureMetrics. Download

all FutureMetrics presentations, white papers and dashboards online

for free at

www.futuremetrics.com.

Source:

http://www.canadianbiomassmagazine.ca/pellets/growing-demand-for-pellets-6074