Japan Wood Products

Prices

Dollar Exchange Rates of

26th March 2014

Japan Yen 102.05

Reports From Japan

ˇˇ

JapanˇŻs 2014 budget heavy on state spending

The 2014 budget has just been adopted in Japan and

incorporates massive government spending which may be

as high as US$936 billion. The extra high budget involves

more resources for social security, defense and public

works much of which is aimed at softening the blow of the

upcoming tax increase.

Considerable faith is being placed in fiscal stimulus

measures to strengthen the economy but the Japan Times,

the prominent English language newspaper, is urging

caution saying ¨Dthe tax h ike , co mb ined with higher

pension premiums and reduced social benefits could cost

households yen 7.5 trillion (appro x. US$74 b illion)ˇ¬.

Japanese consumers are also being hit by rising costs of

imported goods because of the weakening yen, all of

which could drive down consumer spending. Household

spending in Japan accounts for over 50% of GDP so lower

consumer spending will affect the whole economy.

For a summary of the 2014 budget see:

http://www.mof.go.jp/english/budget/budget/fy2014/01.pdf

Retail sales boom

Japanese consumers have been on a spending spree ahead

of the 1 April increase in the consumption tax. Retailers in

the country report record sales of electrical goods and the

auto market has jumped around 30% over the past months.

However the retailers are well aware the good times will

come to an end after the tax hike and are planning sales

campaigns to try and keep sales afloat.

Foreign cash flies from Japan

Data from Japan's finance ministry showed foreign

investors sold around US$11 billion in the second half of

March, the biggest movement of cash since 2005 as a

reaction to worries that Japan's economy is faltering.

Analysts say the delays in implement ing essential reforms

to spur growth are yet to be enacted which is further

undermining confidence in the government strategy.

While the Japanese media have been quick to report the

wage increases recently agreed by the large corporations

many small and medium sized companies could not offer

workers an increase in basic wages. The government is

expected to respond to any slowing in the economy with

another fiscal stimulus package in mid year.

See:

http://www.mof.go.jp/international_policy/reference/itn_tr

ansactions_in_securities/week.pdf

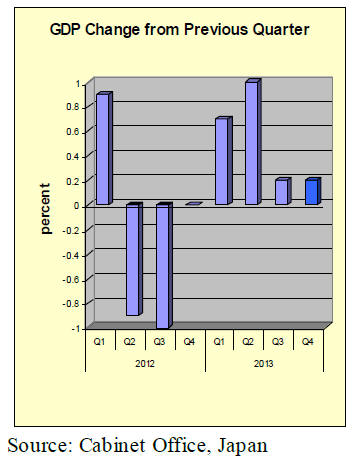

First quarter GDP figures will be available in April and are

expected to show a significant improvement because of

the increase in consumer spending in advance of the

consumption tax increase.

Quantitative and qualitative monetary easing explained

In a speech at the International Centre for the Study of

East Asian Development on 24 March, Kikuo Iwata, the

Deputy Governor of the Bank of Japan (BoJ) spoke on the

Bank of Japanˇ®s philosophy behind its quantitative and

qualitative monetary easing (QQE) policy.

The BoJ introduced QQE in April 2013 to achieve the

price stability target of 2 percent in terms of the year -onyear

rate of change in the Consumer price Index (CPI)

with a t ime frame of about two years.

The full speech can be seen at:

https://www.boj.or.jp/en/announcements/press/koen_2014/

ko140324a.htm/

Iwata e xpla ined: ¨DQQE consists of two pillars. The BoJ

has made a clear commitment that it "will achieve the

price stability target of 2 percent at the earliest possible

time, with a time horizon of about two years."

The second pillar is to engage in actions that embody the

commitment specified in the first pillar. As exemplified by

the phrase "quantitative and qualitative monetary easing,"

those actions are to increase the "quantity" of the BoJˇ®s

balance sheet and change the "quality" of its asset

purchases.

An increase in quantity requires massively increasing the

amount of money the BoJ directly supplies to the financial

system -- this is called "the monetary base" -- at an annual

pace of about 60-70 trillion yen.

Measures to increase the monetary base are mainly

through the purchases of Japanese government bonds

(JGBs), and the BoJ will purchase JGBs so that their

outstanding amount will increase at an annual pace of

about 50 trillion yen.

A change in quality requires purchasing assets with a

higher risk profile. Among the JGBs, the BoJ has started

purchasing those with longer remaining maturit ies. In

addition, it has increased the amounts of purchases in

exchange-traded funds (ETFs) and Japan real estate

investment trusts (J-REITs) in order to reduce risk

premiums on assets.

When we (the BoJ) decided to introduce the QQE last

April and used the expression -a new phase of monetary

easing both in terms of quantity and quality -. The BoJ has

been pursuing monetary easing in exactly that manner, at

an unprecedented scale.ˇ¬

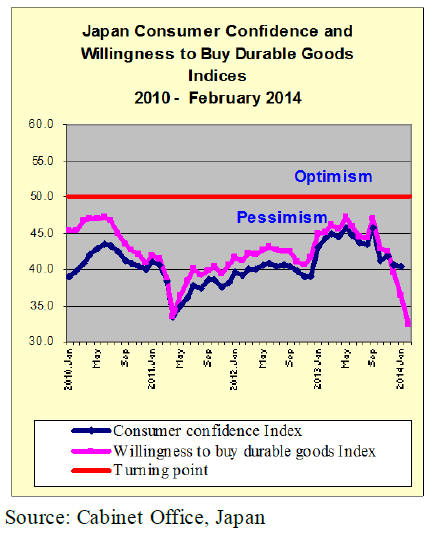

Sharp fall in consumer confidence due to impending

tax hike

Japanˇ®s Cabinet Office has released the results of the

February 2014 showing the consumer confidence index

fell to 38.3 in February, the third month of decline and the

lowest it has been since September 2011.

The latest Consumer Confidence Survey was carried out in

15 February and showed more Japanese householders

were even more pessimistic than in January.

In a strange statistical twist consumer confidence was

sharply below the level forecast by many analysts and at

the same t ime retail sales have been booming as purchases

are made in advance of the consumption tax increase.

It is likely to be several months until the confidence index

in the survey is undisturbed by such one-off events. The

results of the March survey will be available in mid April.

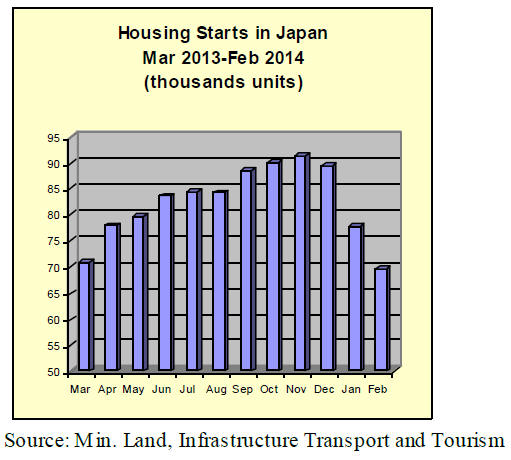

Japan housing starts fall sharply

After rising 12.3% in the last quarter of 2013 the latest

figures fro m Japanˇ®s Ministry of Land, In frastructure and

Transport shows that first quarter 2014 housing starts

growth fell to 1% year on year and are down 10.4% from

January. Although a decline in starts was expected the

February results are well below the 4.9% growth analysts

had forecast.

House builders in Japan are bracing for lean times after the

consumption tax is increased and as a new fuel surcharge

will be levied from mid April. The pace at which the 50

major building contractors have been securing orders fell

in February extending the decline seen in January.

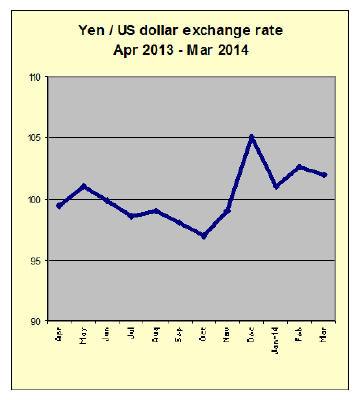

Yen:dollar March roller coaster

In early March the yen strengthened against the US dollar

rising to almost 100 as the yen became a haven currency

on concerns over US Russia relations .

However, within days the dollar s trengthened against the

yen as traders shrugged off worries over slowing growth in

China and the tensions over Russia's annexation of

Crimea. By the end of the month the yen/dollar exchange

rate was 103 to the US dollar.

Interest rates in the US are set to rise as early as 2015, if

not before and recent confirmation of this by the US

Federal Reserve boosted the dollar.

When US interest rates increase the yen, euro and

Canadian dollar are likely to be among the biggest losers

as these countries will not be in a position to raise interest

rates at the same time or at the same speed which is likely

to result in further weakness for the yen.

South Sea (tropical) logs

Weather in Sarawak has been unstable. After heavy rain

stopped, came dry weather with sun shine and some rivers

are drying up. In particular, Tanjung Manis is heavily

affected by this weather and log production is

considerably dropping so the buyers are sending their

ships to Baram and Bintulu to fill up ships.

Since production at Tanjung Manis takes about a half of

export logs, other ports are not able to fill up a gap. Thus, total volume

is

declining. Facing this shortage, India is sending their ships

to PNG and Solomon Islands.

In this situation, log prices are firming. Sarawak meranti

regular prices are US$285-295 per cbm FOB, US$5-10

higher than February. Small meranti is about US$250 and

super small is about US$230. They are also US$5-10 up.

Heavy rain continues in PNG so log production is slow.

China started buying aggressively after some pause during

Chinese New Yea rˇ®s days

Log prices are going up and particularly low grade log

prices are up by about US$20. Ships have to wait for logs

so it takes longer to finish up. There is no sign of weather

improvement. Weather is totally different from Sarawak.

January plywood supply

Total plywood supply in January was 599,900 cbms,

11.4% more than January last year and 12.3% more than

December. This is the highest monthly supply in last

twelve months.

Volume of imported plywood exceeded 360,000 cbms,

which pushed total volume up. Inventories of domestic

softwood plywood dropped below 100,000 cbms.

Imported plywood volume was 366,500 cbms, 12.9%

more than January last year and 25.5% more than

December, which is the largest monthly arrival since June

2011. In

particular, plywood from Malaysia was 158 M cbms, 6.6%

more and 31.1% more, 36 M cbms more than December.

The volume from Indonesia and China also increased by

10-20,000 cbms.

Domestic plywood production in January was 233,300

cbms, 9.2% more and 3.6% less. In this, softwood

plywood was 217,900 cbms, 11.6% more and 3.8% less.

The shipment was 246 M cbms, 9.3% and 6.2% more.

The manufacturers shipped out their inventories so that the

inventories were down to 93,200 cbms, about 23,000 cbms

less than December.

In general, operations of major precutting plants have

been slowing down but orders from large house builders

continue busy.

Plywood manufacturers think that the demand would slow

down after consumption tax hike in April but considering

forecast of housing starts this year, the demand should stay

relatively stable through the year.

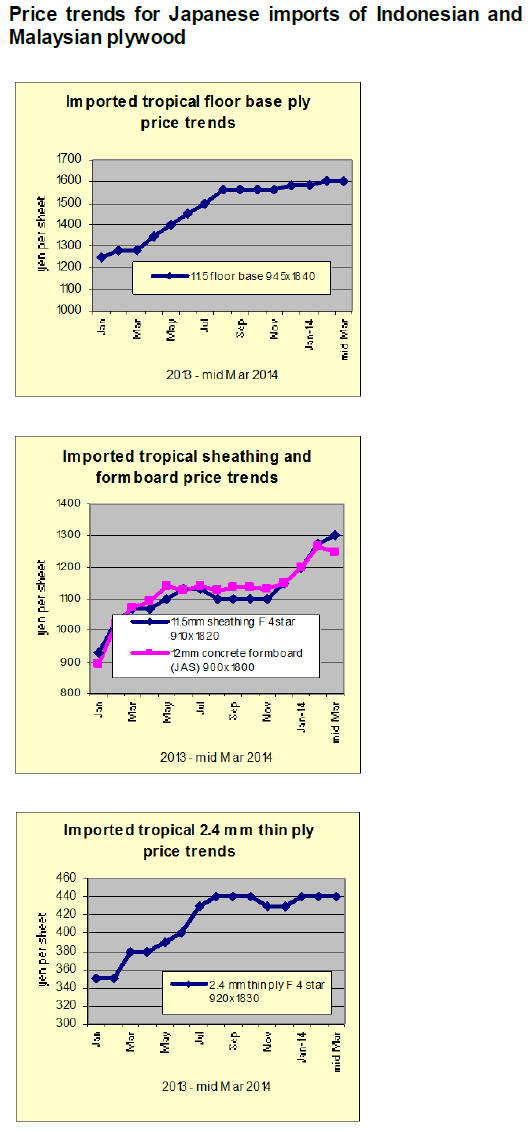

South Sea (tropical) hardwood plywood market

Market of South Sea hardwood plywood soared since last

December with declining inventories and higher offer

prices by the suppliers for future shipments but excitement

simmered down in February and speculative purchases are

over in fear of price drop in March by dumping sales for

book closing. The market is quiet right now.

The suppliers suffer production delay by log shortage

since last December so that arrivals in February and March

would be down. The importers push the suppliers to make

quicker shipments.

In Japan, January arrivals were 360,000 cbms but the

importers felt scarcity with declining on-hand inventories.

Because of delayed shipments, contract balances are

increasing so the importers were not able to buy future in

February.

Meanwhile, the suppliers try to reduce accepting orders in

fear of higher log prices in future. In price negotiations in

late February, the suppliers proposed slight increase but

because of stronger exchange rate, yen cost remains

almost unchanged.

Buyers in Japan are cautious because of large order

balances and uncertain market after April.

largest LVL plant in Japan

Iida Group Holdings (Tokyo),house builder and real estate

dealer, First Wood (Fukui prefecture), laminate lumber

manufacturer and precutting processor and Kawai Ringyo

(Iwate prefecture), lamina and wood chip manufacturer

will jointly build the largest LVL manufacturing plant in

Aomori prefecture with total investment of about 8.4

billion yen.

Aomori Prefecture has been inviting investment for large

wood processing facilities since 2012. Three groups are

the first one to discuss the location and size of facility.

Size of the facility is LVL production of 60,000 cbms a

year with log consumption of 120,000 cbms.

Total production of LVL in Japan so far is about 70,000

cbms so this facility will be the largest single

manufacturing plant. The plant will be completed in

March 2015.

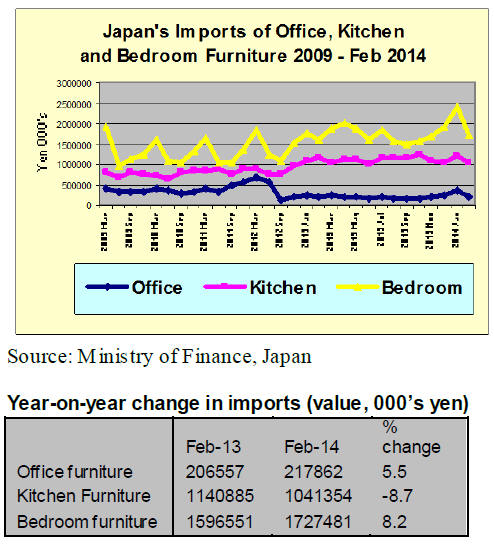

Trends in office, kitchen and bedroom furniture

imports

Japanˇ®s office kitchen and bedroom fu rniture imports fro m

2009 to the end of February 2014 are shown below.

Imports of bedroom furniture exhibited a cyclical trend

between 2009 and 2012.

However, from 2012 bedroom furniture imports began to

increase and have continued upwards since. However,

February bedroom furniture imports fell sharply as

Japanese companies adjusted stocks in anticipation of a

decline in sales after the consumption tax is increased on 1

April.

Similarly, February imports of office and kitchen furniture

fell as businesses brace the fall-out from the tax hike.

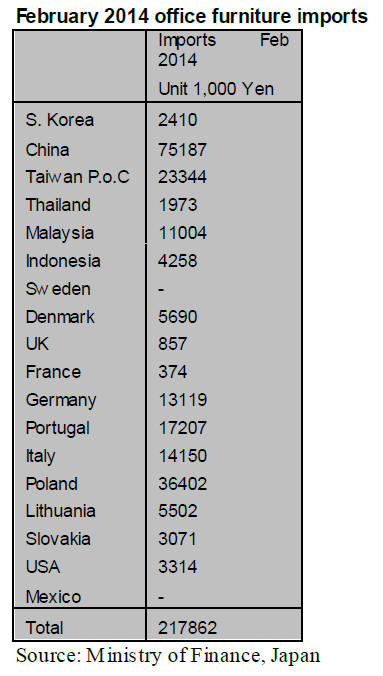

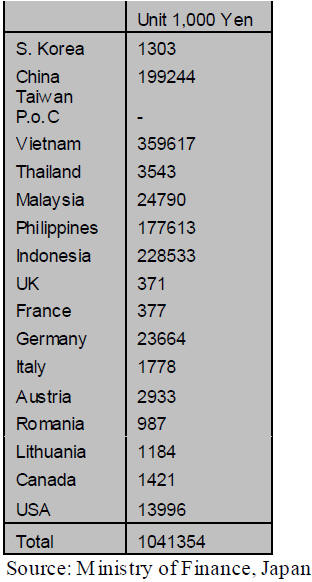

Office furniture imports (HS 9403.30)

February 2014 imports of office furniture into Japan were

up 5.5% year on year but down a massive 40% on January

imports. In February 2014 the biggest losers were China

(down 61%),Indonesia (down 71%), Sweden and

Germany.

The top three suppliers of office furniture in February this

year were China (34.5%), despite the significant decline

compared to January, Poland (17%) and Taiwan P.o.C

(11%). The three top suppliers accounted for 62.5% of all

office furniture imports in February 2014.

EU suppliers of office furniture to Japan accounted for just

6% of all office furniture imports and managed to capture

a greater share of the market in Japan during February.

Kitchen furniture imports (HS 9403.40)

Japanˇ®s February 2014 imports of kitchen furniture were

down 14% compared to levels in January and down 8.7%

compared to levels in February 2013.

The top three suppliers accounted for over 75% of all

kitchen furniture imports by Japan and remain Vietnam,

Indonesia and China.

Of the EU suppliers of kitchen furniture to Japan in

Febraury this year only Germany provided any significant

amount but this accounted for just 2.3% of all imports of

kitchen furniture.

The biggest losers in February 2014 were Vietnam (down

19.5%) and China (down 38%), on the other hand both the

Philippines and Indonesia increased exports of kitchen

furniture to Japan in February this year.

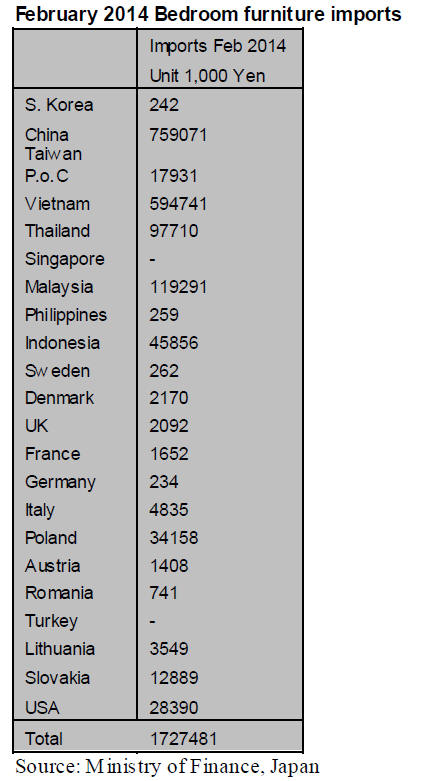

Bedroom furniture imports (HS 9403.50)

Japanˇ®s bedroom furniture imports increased throughout

2013 and reached a record high in January 2014.

February 2014 imports show a sharp reversal in fortunes

having corrected sharply to be down 28% on levels in

January. Despite the fall in February imports of bedroom

furniture were still some 8% higher than in February 2013.

The top three suppliers in February, as in January, were

China (44%), Vietnam (34.4%) with Malaysia (7%)

joining the league table with an export performance

double that of February.

The biggest losers in February were China (down 47%)

with Hong Kong and Singapore supplying no bedroom

furniture in February 2014 after a good performance in

January.

EU suppliers accounted for just 3.7% of Japanˇ®s February

bedroom furniture imports and this was down 22% on

levels in January. Imports from Poland fell while suppliers

in France managed a better performance in February.

|