|

Report

from

Europe

Slowing German economy drags down EU growth

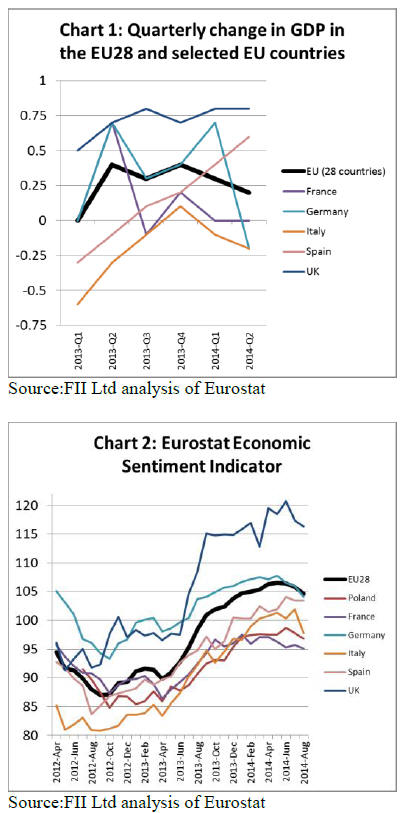

The EU28 group of nations recorded only 0.2% GDP

growth in the second quarter of 2014, down from 0.3% in

the first quarter (Chart 1). The slowdown was largely due

to contraction in Germany, Europe's biggest economy.

After expanding 0.7% in the first quarter of 2014,

Germany‟s economy slipped 0.2% in the second quarter of

the year as foreign trade and investment, particularly in the

construction sector, weighed on growth. Meanwhile

France recorded zero growth for the second quarter in a

row between April and June 2014, while Italy‟s economy

continued to contract.

Investor and business confidence in central and east

Europe has been undermined because of the crisis in

Ukraine - straining relations with Russia - raising fears of

an even weaker recovery because of the threat of

deepening sanctions.

There was better news from Spain where the recovery has

continued to gather pace this year, with GDP expanding

0.6% in the first quarter.

However, the UK is currently the strongest performer of

large European economies, with GDP growth of 0.8% in

both the first and second quarters of 2014.

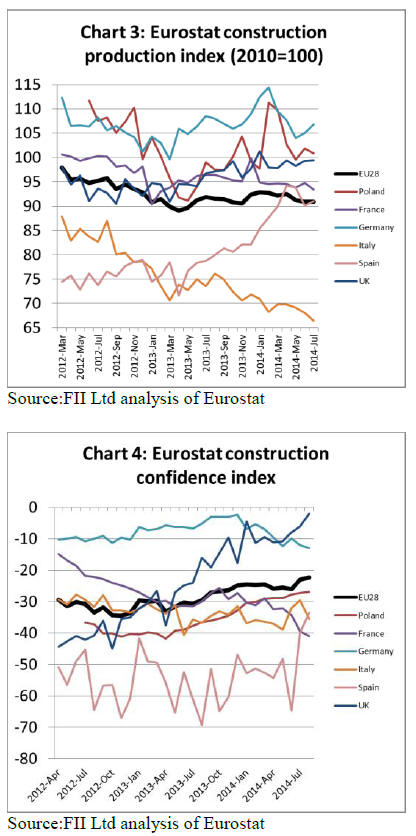

Trends in GDP growth are mirrored in Eurostat‟s

Economic Confidence Indicator (ECI), a forward-looking

index that measures perceptions and expectations in five

surveyed sectors (industry, services, retail trade,

construction and consumers) in all EU Member States.

The ECI for the EU as a whole was still over 100 in

August �C indicating above average economic sentiment.

However the ECI was declining between June and August

this year. The decline is apparent in all the major EU

economies with the exception of Spain.

Overall economic sentiment remains strong in the UK,

moderate in Germany and Spain, but weak and declining

in France, Italy and Poland (Chart 2).

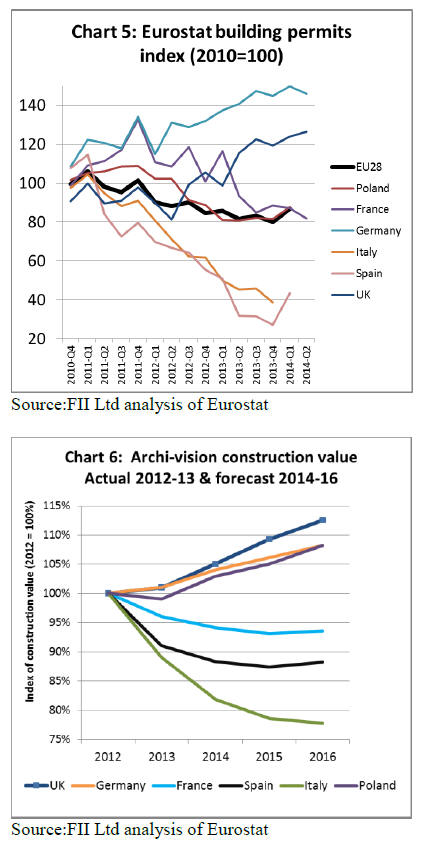

European construction flat at a low level

Although overall European construction activity hit

bottom in March 2013, it has risen only slowly since then

(Chart 3). Activity was strengthening to February this year

but has dipped again since April. The Eurostat.

Construction Confidence Index in the EU is still in

negative territory, indicating that many in the industry still

expect market conditions to deteriorate rather than to

improve in the next 3 months. However the trend in

market sentiment is gradually improving (Chart 4).

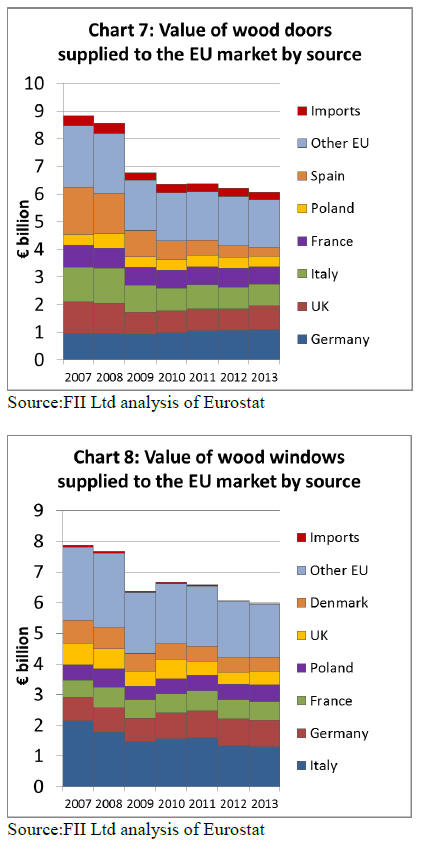

The latest EU-wide data for building permits shows that

these were declining until the last quarter of 2013 but

experienced an upturn in the first quarter of 2014 (Chart

5).

Rapid improvement in UK construction

Construction industry trends in 2014 have varied widely

between EU countries. The UK stands out this year as a

country where construction is recovering very rapidly. The

UK Construction Products Association (CPA) Summer

Forecasts suggest that total construction output will grow

by 4.7% in 2014 and a further 4.8% in 2015.

Furthermore, this expansion should continue with total

construction output forecast to rise 22.2% over the next

five years. In the 12 months of end of June this year, UK

housing starts were nearly 138000, 22% up on the

previous year and the highest level of house building since

2007. Private housing starts are now expected to grow

18% during 2014 and 10% in 2015.

Commercial construction in the UK has also seen a

significant resurgence in 2014. This is mainly due to big

ticket projects in London, although there are now also

signs of improving activity in other parts of the country.

The CPA expects commercial offices output in the UK to

grow 10% in 2014 and 8% in 2015.

The CPA‟s forecasts are slightly more optimistic than

those of the 2nd quarter Archi-vision survey of 1600

architects across Europe.

For the UK, Arch-Vision predict 4% growth of the UK

construction market in 2014 with this rate of growth

continuing in 2015 (+4%) and slowing to +3% in 2016

(Chart 6).

Slowdown in German and Polish construction in 2nd

Quarter

Construction activity in Germany and Poland has been

relatively robust compared to other European countries in

recent years. However seasonally-adjusted activity in both

countries fell away dramatically in the second quarter of

2014.

This seems to be primarily the result of the mild winter

which meant that many projects were brought forward into

the first quarter. There are indications that construction

activity in both countries will recover in the second half of

2014.

The 2nd quarter Archi-vision survey shows that architects‟

order books and turnover development in both Germany

and Poland were positive in the second quarter of 2014,

suggesting plenty of new building projects in the pipeline.

Archi-vision forecast continued slow growth in

construction activity in both countries between 2014 and

2016 (Chart 6)

Construction activity in Spain has been regaining strength

since the start of 2013. The Archi-vision survey indicates

two positive quarters for Spanish construction in a row in

the first half of 2014 as more architects report increasing

order books. Residential building permits have also been

rising in Spain this year for the first time since the

recession.

However, government austerity is still a major constraint

in Spain and building permits for non-residential

construction have fallen again this year. Arch-Vision

forecast that Spanish construction activity will decline 3%

in 2014 and a further 1% in 2015, but will recover by 1%

in 2016 (Chart 6).

Depressed construction in Italy

Construction activity in Italy remains depressed. The

construction production index for Italy continued to

decline to July 2014 and is now only 65% of the level of

2010 (Chart 3). The latest data for Italian building permits

shows these falling sharply during 2013.

The Archi-vision survey shows that, after several bad

quarters in 2013, Italian architects experienced another big

drop in order book and turnover development in the

second quarter of 2014.

The confidence indicator for Italian construction is stable,

but at a low level (Chart 4). Therefore the outlook for the

next twelve months is not promising. Archi-Vision predict

that the Italian construction market will fall by 8% in 2014

and a further 4% in 2015. The decline might then level off

in 2016.

Construction activity in France declined sharply at the end

of 2014 and confidence in the sector remains low. The

Archi-vision survey indicated a sharp fall in architect‟s

order books in the fourth quarter of 2013.

The Construction Confidence Indicator for France has

continued to fall this year (Chart 4). However, other

indicators suggest the market may be close to bottom.

French building permits for residential buildings showed a

negative trend for the whole of 2013, but stabilised in the

first two quarters of 2014. Building permits for nonresidential

construction registered a slight increase. Archi-

Vision forecast that French construction activity will

decrease in 2014 (-2%) and 2015 (-1%), but will stabilise

from 2016 onwards.

Slow improvement in Dutch and Belgian construction

There are signs of improving construction activity in the

Netherlands. The Archi-vision survey indicates that order

books and turnover for architects in the country increased

in the second quarter of 2014, the third consecutive quarter

of growth.

Other indicators suggest gradual improvement in both

residential and non-residential construction in the

Netherlands. This positive development is partly driven by

a temporary reduction in VAT on rebuilding, renovation

and repair, a measure now due to end on 1 July 2015.

Archi-vision predict a small increase in Netherlands

construction activity in 2014 (+1%), gradually

strengthening in 2015 (+2%) and 2016 (+3%).

In Belgium, the Archi-vision survey also indicates a

gradual improvement in construction sentiment and

activity since mid-2013. Belgian building permits are

rising slowly, mainly due to growth in the residential

sector. Archi-vision forecasts consistent 2% per annum

growth in Belgian construction during the period 2014 to

2016.

European wood joinery production continues to

decline

According to newly-published Eurostat data, the total

value of EU production of wooden doors and windows

declined in 2013. EU imports of both commodities fell

even more sharply. Domestic producers increased their

already hugely dominant position in these market

segments.

EU wooden door production was €5.79 billion in 2013,

down 2.1% compared to the previous year (Chart 7).

Wooden door production increased in all three of the

largest manufacturing countries: Germany (+2.6% to

€1110m), the UK (+6.9% to €840m) and Italy (+2.2% to

€780m).

However, this was offset by a sharp fall in production in

France (-7.3% to €640m) and Spain (-25.2% to €330m).

Production in Poland remained static at €380m.

EU wood window production fell 1.76% from €6.07

billion in 2012 to €5.96 in 2013 (Chart 8). The decline was

mainly due to a 3.2% fall in production in Italy, the largest

wood window manufacturing country, from €1340m in

2012 to €1300m in 2013.

Production in Denmark also continued a long-term

downward trend, falling a further 4.7% to €440m in 2013.

Production in Germany and France remained stable,

respectively €870m and €610m in both 2012 and 2013.

However, production increased in Poland (+7.1% to

€550m) and the UK (+14% to €450m) during 2013.

The downward trend in EU production of wood windows

and doors is partly the result of the decline in overall

construction activity. This has been particularly

pronounced in the new build sector with the result that

renovation and refurbishment activity is now a much more

important driver of demand.

Around 60% of all windows manufactured in Europe are

now utilized in the renovation sector and only 40% in the

new build sector.

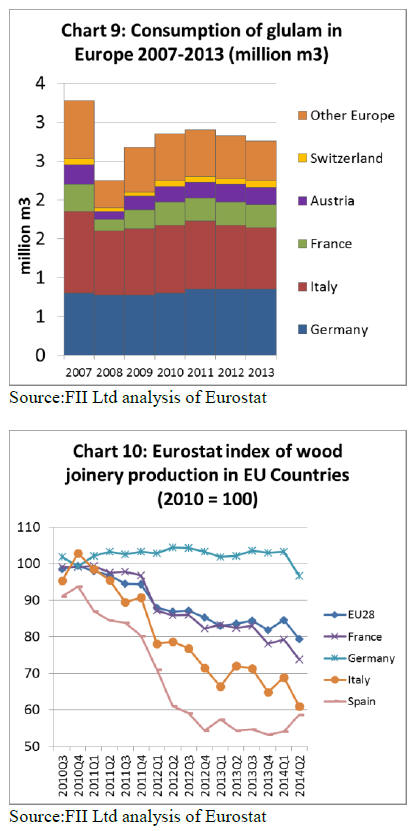

European production and consumption of glulam, used in

large dimensions for structural applications and smaller

dimensions for windows, also declined in 2013 (Chart 9).

Consumption declined 4% in Italy to 790,000 cu.m and

2% in Austria to 220,000 cu.m. However consumption

was stable in Germany and France in 2013 at around

830,000 cu.m and 300,000cu.m respectively.

The Eurostat index of joinery production in EU countries

(which excludes flooring but includes doors, windows and

glulam) shows that production increased slightly in the

first quarter of 2014 but then fell away sharply in the

second quarter (Chart 10). An upturn in joinery production

in Spain and the UK in the second quarter of this year was

insufficient to offset a downturn in Germany, France and

Italy.

Energy efficiency helps drive joinery sector demand

In addition to underlying economic growth, future

development of the construction sector is heavily

dependent on legislation to improve energy efficiency of

the existing building stock in European countries. Various

new measures are expected to encourage more rapid

growth in the window and doors sector than in the overall

construction sector.

In December 2012, the EU published a new Energy

Efficiency Directive requiring Member States to

implement most of its provisions by 5 June 2014.

The Directive establishes a common framework of

measures for promotion of energy efficiency to ensure the

achievement of the EU‟s 2020 20% headline target on

energy efficiency and to pave the way for further energy

efficiency improvements beyond that date.

All EU-28 countries are now required to use energy more

efficiently at all stages of the energy chain �C from the

transformation of energy and its distribution to its final

consumption. Most countries have identified

improvements in existing building stock as one of the most

cost-effective ways to meet the Directive. They are

therefore introducing building regulations with tighter

energy efficiency requirements for windows and doors.

EU Member States are also obliged under the Directive to

renovate at least 3% of buildings owned and occupied by

the central governments starting from 1 January 2014.

They must also include energy efficiency considerations in

public procurement so as to purchase energy efficient

buildings and products.

Given wood‟s strong natural insulation qualities and recent

improvements in wood manufacturing technology, the

wood window and door sector is well placed to exploit

these new opportunities. However, competition is intense

and other material sectors are gearing up research and

development and marketing activities.

The wood industry in Europe faces a particularly strong

challenge from the PVC sector which accounts for at least

two thirds of the windows market in many EU Member

States. Aluminium windows also account for a

comparatively large share of the market, particularly in

Spain, Portugal and Italy, partly explained by relatively

low price for these windows.

A recent report by independent market analysts Ceresana

forecasts a consistent rise in demand for window and door

units across the EU until 2020 driven by a gradual

improvement in construction activity and a significant rise

in refurbishment. Solid wood windows are anticipated to

lose market share, both to PVC and to wood/aluminium

composite windows.

However, wood (mainly veneer and laminate doors) is

expected to continue to dominate the interior door market

and to maintain share (currently around one third) of the

external door market.

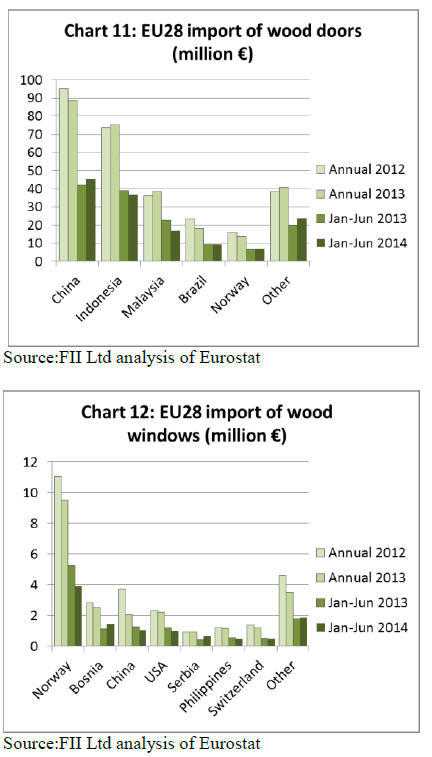

No change in EU imports of wood doors in 2014

Imports of wood doors into the EU were valued at €139m

in the first 6 months of 2014, exactly equivalent to the

same period the previous year (Chart 11). Imports from

China increased 7.6% to €45.6m, but these gains were

offset by declining imports from Indonesia (-5.8% to

€36.8m) and Malaysia (-25.6% to €16.8m). Imports of

wood doors from Brazil remained stable at €9.2m during

the period. Imports currently account for around 4.5% of

the total value of EU wooden door consumption, down

from 5% in 2010.

EU imports of wood windows continue to decline

The EU market for wood windows is very heavily

dominated by domestic producers. Imports currently

account for only 0.4% of the total value of EU wooden

window consumption, down from 0.8% in 2007. Most

wood windows imported into the EU derive from other

European countries, notably Norway and Bosnia.

In the first 6 months of 2014, imports fell from most of the

leading supply countries including Norway, China, the

USA, Philippines, and Switzerland. However there was a

slight increase in imports from Bosnia and Serbia (Chart

12).

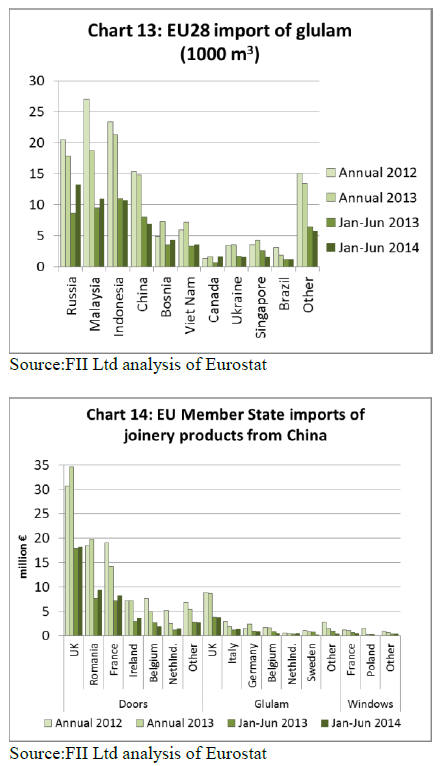

Recovery in EU glulam imports in 2014

The EU imported 61,400 cu.m of glulam products in the

first half of 2014, 9% more than the same period in 2013.

Imports from Russia increased 54% to 13,300 cu.m in the

first six months of this year (Chart 13). As a result Russia

has overtaken Malaysia to become the largest external

supplier of glulam to the EU this year.

However there was also a 16% increase imports from

Malaysia to 11,000 cu.m this year. Meanwhile imports

declined 2% to 10,700 cu.m from Indonesia and 14% to

6,900 cu.m from China. Imports of glulam account for

around 5% of total EU consumption of this commodity.

Much of the imported glulam consists of dimension

product for window manufacturing. Glulam imports from

Russia and China are primarily pine and larch. Imports

from Malaysia and Indonesia consist of meranti.

EU28 imports of joinery products (excluding flooring)

from China had a value of €54.5 million in the first 6

months of 2014, 3% more than the same period the

previous year. This partially reverses the 9% decrease (to

€108m) in EU28 imports of Chinese joinery products

between 2012 and 2013.

Chart 14 summarises EU imports of joinery products from

China by product group and EU Member State. Doors

make up the bulk of EU joinery trade with China, with

total value of €88.5 million in 2013. The EU and Romania

are the main European markets for China‟s wooden doors

and both countries have been importing rising quantities

over the last 2 years.

Imports of Chinese wooden doors by France, the third

largest market, declined between 2012 and 2013, but have

increased again this year.

The UK is the only EU country importing significant

quantities of glulam products from China, with value of

around €8.7 million in both 2012 and 2013. UK imports of

Chinese glulam products were €3.8 million in the first 6

months of 2014, 1.6% less than the same period in 2013.

EU imports of finished wood windows from China are

negligible and declining. EU imports of this commodity

fell from €3.7 million in 2012 to €2.1 million in 2013. In

the first half of 2013, EU imports of Chinese wood

windows were only €1 million, mainly destined for France

and Poland.

|