|

Report from

Europe

EU wood imports rise to highest level since financial

crises

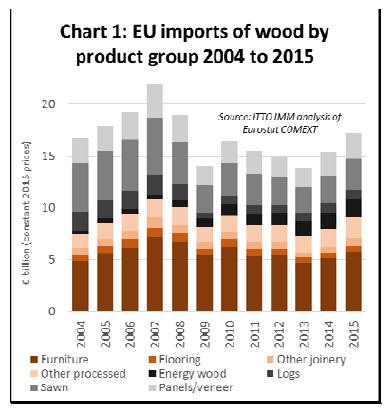

The total value of EU imports of wood products was

euro17.20 billion in 2015, 12% more than in 2014. This

followed an increase of 10% to euro15.3 billion in 2014.

In 2015 EU import value was at the highest level since

2008 just before the global financial crises (Chart 1).

The surge in the euro value of imports in 2015 was partly

owing to the weakness of the euro which on average was

valued around 20% less against the dollar in 2015

compared to 2014. This meant that euro import prices for

most products from the Americas and Asia increased.

Import volumes also increased across most wood product

groups in 2015 but to a lesser extent than euro value.

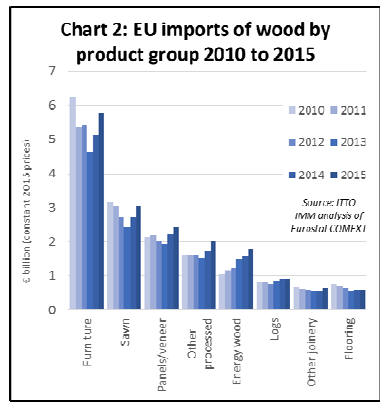

The euro value of imports increased across all wood

product groups in both 2014 and 2015 (Chart 2). Imports

of wood furniture, which had been declining to 2013,

rebounded 10% in 2014 and 13% in 2015 to reach

euro5.78 billion.

Imports of sawn wood rebounded from a low in 2013,

rising 10% in 2014 and 12% in 2015 to reach euro3.04.

Similarly imports of panels (mainly plywood) increased

13% in 2014 and 11% in 2015 to reach euro2.44 billion.

The long term rise in imports of energy wood continued in

2015 to reach an all-time high of euro900 million. Imports

of other joinery products (mainly doors and LVL for

window frames) were flat in 2014 but increased 22% to

euro658 million in 2015.

Imports of wood flooring increased 5% in both 2014 and

2015 to reach euro595 million. Imports of other processed

products increased 14% in 2014 and a further 17% in 2015

to euro2.02 billion.

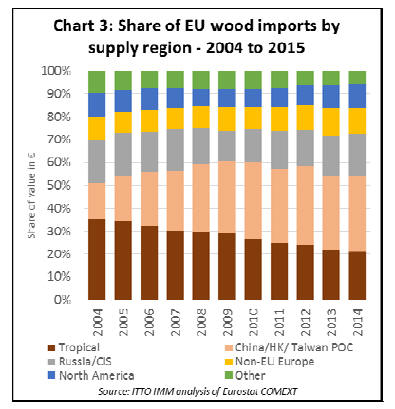

Total imports of wood products from tropical countries

increased 15% from euro3.28 billion in 2014 to euro3.78

billion in 2015. This followed a 6% increase between 2013

and 2014. In terms of share of overall EU imports, 2015

was notable for registering the first reversal in the fortunes

of tropical countries in the last decade.

The share of tropical countries in total EU wood product

import value fell continuously from 35% in 2004 to a low

of 21.4% in 2014, before rebounding slightly to 22.0% in

2015.

Tropical countries lost share initially to China in the

period 2009 to 2010, and then to North American, Russian

and non-EU European countries in the period 2011 to

2014.

However in 2015, tropical countries regained a little share

in import value mainly at the expense of Russia and non-

EU European countries. ChinaˇŻs share in EU imports

remained stable at 32.7% in both 2014 and 2015 (Chart 3).

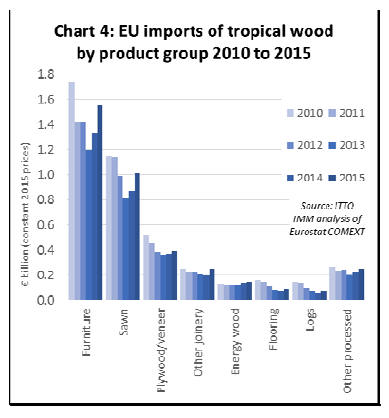

The recovery in EU imports of tropical wood products in

2014 and 2015 was particularly pronounced for furniture

and sawn wood, although there were more minor gains for

all other product groups (Chart 4).

EU imports of wood furniture from tropical countries

increased 11% to euro1.33 billion in 2014 and by a further

16% to euro1.55 billion in 2015.

Imports of sawn wood from tropical countries increased

7% to euro0.87 billion in 2014 and by a further 16% to

euro1.02 billion in 2015. Imports of plywood and veneer

from tropical countries increased more slowly, by 1.4% to

371 million in 2014 and by 6% to euro394 million in

2015.

The long-term shift in EU tropical wood imports away

from primary and secondary wood products in favour of

tertiary products continued in 2014 and 2015. The value of

tertiary processed tropical wood products imported by the

EU increased from 55% of total import value in 2013 to

57% in 2015.

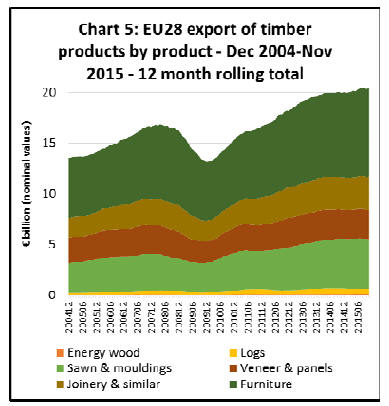

Rising EU trade surplus in wood products

The relative weakness of EU currencies, combined with a

strong focus on reducing costs and improving efficiency in

the European wood sector and the slow growth of

domestic consumption, contributed to a sharp rise in EU

exports of wood products to non-EU countries between

2009 and 2015 (Chart 5).

In 2015, the value of EU exports of wood products were

running at their highest ever level at over euro20 billion.

In 2015, the EU had a euro3 billion trade surplus in wood

products which compares to a euro3 billion deficit before

the financial crises. EU export growth has been

concentrated in sawn wood, joinery (notably flooring and

glulam products) and wood furniture.

Although around 30% of EU wood product exports

consistently go to neighbouring European countries

(mainly Switzerland and Norway), since the global

financial crises there has been a significant in rise in

exports to Africa, the Middle East and China alongside

traditional markets in North America and the CIS.

For wood exporters selling into the EU, the weakness of

the euro and sharp rise in the EUˇŻs wood trade surplus

imply intense competition from domestically harvested

timber and manufactured wood products. Due to the wide

diversity of wood manufacturing activities in the EU, this

is true of nearly all wood sectors.

Even in those wood sectors where European

manufacturers have traditionally been weak and more

dependent on imports, such as in supply of durable goods

for outdoor use and in appearance grade wood, new

innovative products are taking share from external

suppliers.

Key innovations include a wide range of new surface

finishes to enhance the appearance and performance of

panel products, and thermal and chemical modification

processes to enhance the durability of domestic wood

species.

At the same time, with traditional markets growing only

slowly, EU wood manufacturers are developing new

products designed to extend the range of wood into new

sectors traditionally dominated by other materials, notably

steel and concrete.

For example, EU production of cross-laminated timber ¨C a

product which can successfully compete with steel and

concrete in high-density urban construction ¨C increased

from 100,000 m3 in 2005 to 700,000 m3 in 2015.

Legality verification and certification in EU wood

supply

Just how much of the wood traded internationally derives

from legal and sustainable sources is a question frequently

asked by both timber buyers and policy-makers in the EU.

The question has become particularly relevant now that

the EU Timber Regulation obliges all importers to

demonstrate that there is a negligible risk of any illegal

wood entering their supply chains. Unfortunately there is

not a simple answer to this question.

One issue is how to define terms like "negligible riskˇ± and

ˇ°sustainably" sourced. There are large areas of forest

around the world where there is very little risk of illegal

harvest and that would be considered "sustainable" against

most measures, but are not independently verified or

certified. This is particularly true of forests owned and

managed by communities or private non-industrial forest

owners.

Another issue is that certification systems do not measure

the volume of trade in certified products. Typically they

only monitor the area of certified forest and the numbers

of chain of custody certificates issued.

Nevertheless, efforts have being made to overcome these

problems. In 2012, Forest Industries Intelligence (FII) Ltd,

a UK-based company, devised a procedure to estimate

"level of exposure to 3rd party verified/certified wood".

This formed part of a project joint funded by the UK

Department for International Development (DFID), the

EU Timber Trade Action Plan, and European Timber

Trade Federation (ETTF).

That 2012 assessment has now been updated by the ITTO

Independent Market Monitoring (IMM) Project which is

monitoring the market impact of the FLEGT Voluntary

Partnership Agreements (VPAs).

The ˇ®level of exposureˇŻ is a rough measure to identify gaps

in forest coverage of independent certification and legality

verification systems. It is based on the percentage area of

certified or legally verified commercial forest area in each

individual supplier country.

For example, if 40% of its forest area is known to be

independently certified or legally verified, the level of

exposure of a countryˇŻs wood production and exports is

also assumed to be 40%.

The certified/verified forest areas are calculated by

comparing data from the various certification and

verification systems with UN FAO figures for areas of

productive forest land.

ˇ®Level of exposureˇŻ data can be broken down by

verification system, including FSC, PEFC, or operatorbased

systems of legality verification (such as SGS TLTV,

Smartwood VLO, or OLB). For this assessment, wood

from countries covered by FSC-endorsed National

Controlled Wood Risk Assessment is also considered ˇ®3rd

party verifiedˇŻ.

To avoid double counting, areas dual certified to FSC and

PEFC are accounted separately. Adjustments are also

made for a few countries, such as Brazil and the USA,

where there is a big difference in the level of certification

in hardwood and softwood forests.

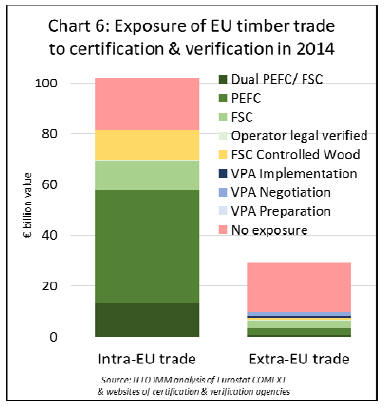

The new assessment indicates that in 2014, around 80% of

internal EU trade in timber products (including all wood,

wood furniture, pulp and paper) was ˇ°exposedˇ± to some

form of certification or legality verification. This is simply

due to the fact that a very large proportion of forest area

within the EU is either certified or assessed to be low risk

of illegal harvest in an FSC national controlled wood

assessment (Chart 6).

Limited access to certification for wood imported from

outside EU

In contrast to intra-EU trade, level of exposure to some

form of certification or legality verification of all EU

timber products imports from outside the EU was only

around 25% in 2014. While low, this figure is heading in

the right direction, rising from 19% in 2007.

The assessment also indicates that if all timber from the 17

countries that are now engaged in FLEGT VPAs had been

licensed in 2014, the level of exposure to legally verified

timber in EU external trade would have been 8% higher, at

33%.

The increase due to VPA countries excludes areas already

certified or legally verified in these countries (notably by

SVLK in Indonesia, PEFC/MTCS in Malaysia and FSC in

Central Africa) which are already included in the 25%

figure.

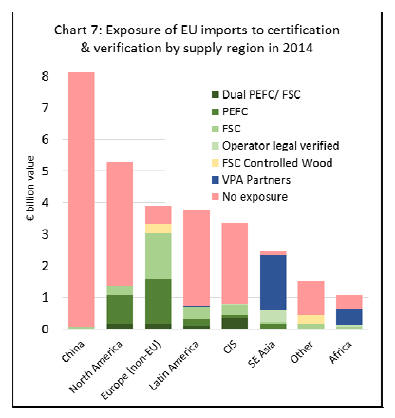

Obviously that leaves a large proportion of imports which

are unlikely to be from third party certified or legally

verified sources. Chart 7 shows that China dominates

amongst EU-supplying countries with low exposure to

verified timber. China's level of exposure to certification is

set to increase significantly.

The 2014 data does not include figures for the China

Forest Certification System (CFCS) which was endorsed

by PEFC in February 2014 but had yet to register any

PEFC-certified forest at the end of that year.

By the end of 2015, 5.6 million hectares were registered as

PEFC certified in China and more recent reports from the

China State Forestry Administration indicate that around

10 million hectares of forest are now certified ¨C although

most of that area is natural protection forest and ChinaˇŻs

large area of production plantation forest is still largely

uncertified.

North America is identified as another region with ˇ°low

exposureˇ± to legality verification and certification. Most

commercial forest land in Canada is certified. In contrast,

the U.S. has a large area of private non-industrial forest

land which is not certified. The US government also has a

long-standing policy commitment not to pursue

certification of federal forest lands.

Latin America is assessed to have relatively low level of

exposure to certification and verification. However this

figure is severely distorted by reliance on forest area to

calculate the index.

The Amazonian rain forest is, of course, huge and only a

tiny proportion is certified. But this area only contributes a

relatively small volume of timber to international trade.

Most of wood product imported into the EU from Brazil

now constitutes softwood or eucalyptus from plantations

outside the tropical zone, many of which are certified.

Therefore the index probably underestimates the real level

of exposure of Latin American wood products in trade.

While the VPA process captures only a relatively small

proportion of total EU imports of timber and timber

products, it is very significant amongst tropical supplying

countries in South East Asia and Africa.

If all timber products imported by the EU from VPA

countries were FLEGT licensed, the level of exposure to

verified timber from Southeast Asia would rise from 25%

to 95% and from Africa from 11% to 60%.

|