Japan

Wood Products Prices

Dollar Exchange Rates of 25th

February 2017

Japan Yen 112.14

Reports From Japan

Workers told ¨CLeave work at 3pm and spend

money

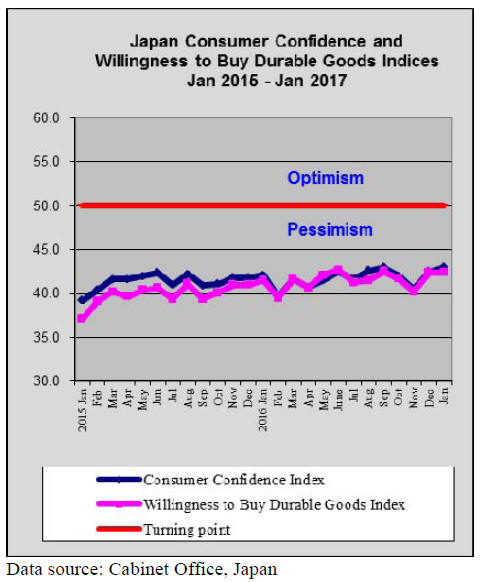

The Cabinet Office has downgraded its assessment of

consumer spending marking the first downgrade in almost

a year. Across Japan, households have been hit with higher

food prices and have become increasingly skeptical about

the prospects for the economy and wage growth. Put

together, this has resulted in households cutting back on

non-essential purchases such as household goods and

furniture.

The increasingly cautious view of consumer, if it

continues, will be a source of concern for policymakers

who are struggling to fight deflationary trends.

On the last Friday of each month, beginning 24 February,

companies across Japan were encouraged to send workers

home by 3pm. The object of this strategy is to let workers

get an early start to the weekend and begin spending by

eating out or taking advantage of special discounts offered

for late Friday flights and train journeys.

This so-called ˇ®Premium FridayˇŻ campaign has been

launched by the government and is supported by the

business community. In a country notorious for its culture

of long working hours this is a drastic change.

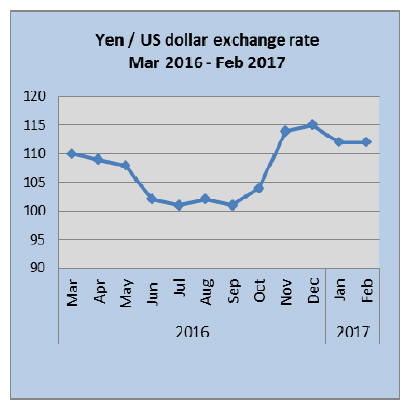

Weak Yen boosts exports but raises cost of

imports

A weaker yen drove exports and business sentiment higher

in the final quarter of 2016 which resulted in an

annualized 1% growth of the overall economy.

However, with consumption remaining subdued, the

prospects for early 2017 are subject to external influences

more than a stronger internal demand which the

government seeks.

In March the annual wage negotiations between unions

and management begin and early signs are that pay rises

will be similar to last yearˇŻs which will do nothing to boost

consumption.

This means the best hope for the economy is a weak yen

however the new US administration seems set to follow up

on its assertion that Japan is a currency manipulator which

could mean the yen will strengthen against the US dollar.

This would undermine JapanˇŻs export growth.

While a weak yen is good for exporters it is bad for

household spending and the prospects are rising for a clash

between the Bank of Japan, which supports a weak yen,

and the government that is trying to spur household

spending. In addition, any further yen weakness would

raise tensions between Japan and the US.

Apartment building boom in Tokyo coming to an end

The number of unsold new apartments in Tokyo has

reached a five year high which suggests TokyoˇŻs

apartment building boom is nearing its end.

Much of the energy in the Tokyo market for apartments

came from Chinese buyers but, with a crackdown on

Chinese citizens moving money offshore, the steam has

gone out of the market.

As the stock of empty apartments rise rents are

falling and

prices, especially for apartments near the Olympic Games

venues, have started to fall.

Data from the Real Estate Economic Research Institute of

Japan reports that the average price of a newly-built threebedroom

apartment in Tokyo rose 24% in January last

year the highest on pace record .

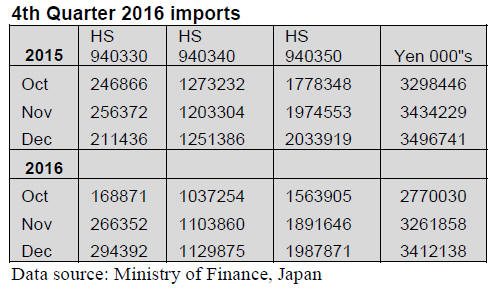

JapanˇŻs wooden furniture imports

JapanˇŻs 2016 wooden furniture imports (HS 940330,40

and 50) fell around 3% in yen terms against levels in 2015.

Overall, wooden office furniture imports were down 6%

year on year, wooden kitchen furniture imports dropped

around 4% year on year and bedroom furniture imports

also fell but by a smaller margin (-2.3%).

While there is no clear cyclical trend in imports of either

office or kitchen furniture, imports of bedroom furniture in

2015 and again in 2016 show a distinct cyclical trend.

In both years in the first half of the year imports drifted

down only to begin climbing again in the second half of

the year.

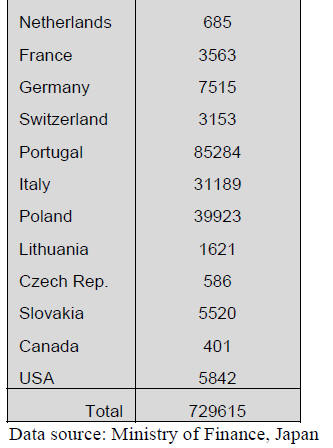

4th Quarter 2016 office furniture imports (HS

940330)

China, Portugal and Poland, in order of rank, were the top

suppliers of wooden office furniture to Japan in the final

quarter of 2016.

Together these three shippers accounted for over 80% of

JapanˇŻs wooden office furniture imports in the last quarter

2016.

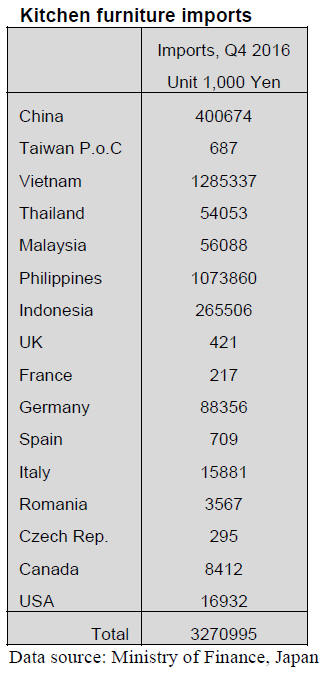

4th Quarter 2016 kitchen furniture imports (HS

940340)

Year on year, JapanˇŻs 2016 imports of wooden kitchen

furniture were down 4% and in the final quarter of 2016

fell by the same amount compared to the same period in

2015.

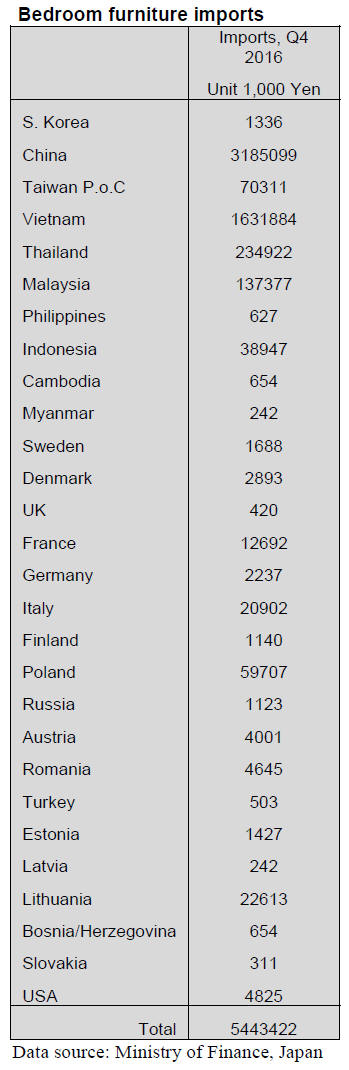

4th Quarter 2016 bedroom furniture imports

(HS 940350)

Just two suppliers, China (59%) and Vietnam (30%)

accounted for almost 90% of JapanˇŻs imports of wooden

bedroom furniture in the fourth quarter of 2016. This

mirrors the trade throughout the year with the two largest

shippers dominating imports.

The third ranked supplier in the fourth quarter 2016

was

Thailand which contributed a modest 4% to total fourth

quarter imports of this product.

Trade news from the Japan Lumber Reports (JLR)

For the JLR report please see:

http://www.nmokuzai.

com/modules/general/index.php?id=7

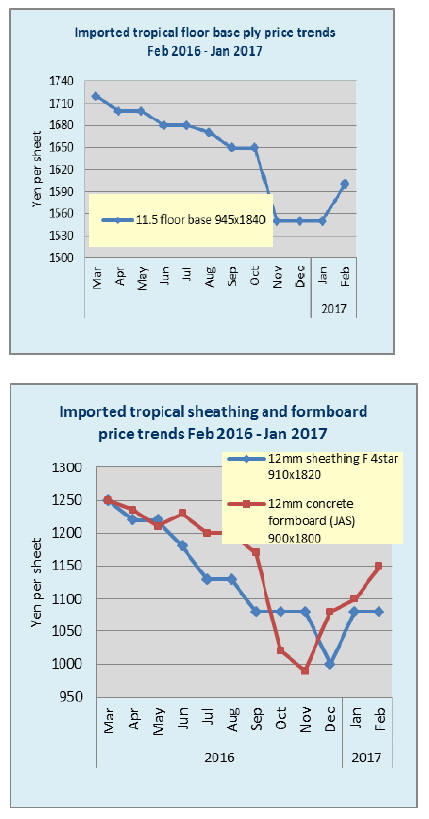

Plywood supply in 2016

Total plywood supply in 2016 was 5,834,200 cubic

meters, 3.1% more than 2015. In this, domestic supply was

3,063,500 cbms, 10.6% more than 2015. This is first time

to reach three million cbms after nine years since 2007.

Imported plywood was 2,770,600 cbms, 4.0% less than

2015. This is two straight years decline under three million

cbms. Share of domestic and imports reversed with 47.5%

of imports and 52.5% of domestic supply. This is the first

reversal of share in 21 years.

In 2016, domestic supply increased by about 10% then the

imports continued to decline so the total was almost

unchanged from 2015. In 2016, the yenˇŻs appreciation

sharply progressed in early year then in late 2016, the yen

depreciated so the price increase of imported plywood was

necessary so the importers and wholesales had hard time

all through the year.

Despite slow movement of imported plywood, it is

noticeable fact that monthly average of 238,800 cbms of

imported plywood continued through the year. This tells

there is firm demand for imported plywood even when the

demand is shifting to domestic plywood, wooden board

and non-wood materials.

In domestic production, softwood production was

2,897,200 cbms, 11.9% more than 2015. Structural

softwood plywood production was 2,786,500 cbms, 17.7%

more, which is more than total imported plywood supply.

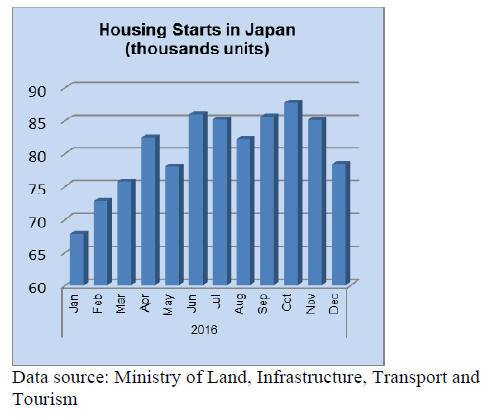

The demand for softwood plywood had been very active

all through the year by strong housing starts so the

shipment of soft wood plywood was 2,939,000 cbms,

9.1% more than 2015.

The inventory peaked in March with 128,400 cbms then it

had been declining month after month and the December

inventory was only 82,500 cbms.

In imported plywood, Malaysian supply was 1,075,500

ccbms, 10.3% less than 2015. Indonesian supply was

903,300 cbms, 5.2% more, which was supported active

demand for floor base. Chinese supply was 616,600 cbms,

5.0% less.

JapanˇŻs log export in 2016

According to the trade statistics of the Ministry of

Finance, total log export in 2016 was 644,257 cubic

meters, 6.1% less than 2015. Kyushu took 79.6% share of

log export. Total value was 7,735 billion yen, 15.1% less.

In 2016, log exporters had hard time with strong yen and

slow down of Chinese economy but they tries to maintain

the business by performing the contracts despite negative

factors. KyushuˇŻs export volume was 513,089 cbms, 2.8%

less than 2015. Export business increased some in the first

half then it decreased in the second half.

Total value of log export in Kyushu was 5,980 billion

yen, 12.7% less. After the second half of last year, the yen

weakened then there are increasing inquiries from China

and number of log exporter increased so that export log

prices in Kyushu are climbing.

By port, Shibushi, the largest export port previous year,

exported 199,323 cbms and maintained the top export port

in 2016.Sendai exported 31,772 cbms so total volume

from Kagoshima prefecture increased some from 2015.

Other ports are Hososhima with 63,436 cbms, Minamata

with 36,141 cbms, Sakai with 11,396 cbms, Shimizu with

12,710 cbms, Kanda with 4,993 cbms, Yokkaichi with

4,982 cbms.

By species, cedar was heavy from Shibushi, Hososhima,

Yatsushiro and Saheki, all Kyushu ports. Cypress was

main from Yatsushiro, Imari and Minamata, all Kyushu

ports. Other softwood log export ports are Hakodate and

Rumoi, all Hokkaido ports, which shipped species like

larch.

Meantime, total lumber export in 2016 was 83,700 cbms,

47% more than 2015. Lumber volume for Korea is flat but

for China, it increased considerably. Main shipping ports

are Tokyo with 25,535 cbms, Hakata with 10,411 cbms,

Matsuyama with 4,427 cbms, Nagoya with 5,636 cbms,

Moji with 2,958 cbms, Kouchi with 2,750 cbms,

Hiroshima with 2,548 cbms, Mizushima with 2,504 cbms

and Hososhima with 2,119 cbms. By species Kyushu ports

shipped mainly cedar and Shikoku and Chuugoku ports

shipped mainly cypress

South Sea (Tropical) logs

Both Sarawak and Sabah, Malaysia are in rainy season and

rain continues day after day. While some coastal part of

Sabah has improved weather. Sarawak suffers heavy rain

everywhere. Together with severe control of illegal

harvest, Sarawak log production is very low. Therefore

export log suppliers remain very bullish.

Japanese log importers are indecisive for future log

purchase due to unstable exchange rate fluctuation.

In PNG and Solomon Islands, there has been talks of

higher log export duty but so far there is no official

increase by strong opposition by log exporters. If the duty

increases materialize, log prices would be up and supply

volume may change.

In Japan Sea side ports in Japan, cleaning and renovation

of lock gate are done in every two years and it is being

done now and the gate will be closed until end of February

or March.

Plywood mills in Niigata have procured enough logs until

April. Some South Sea hardwood plywood

mills in Japan reduce their own production then buy

plywood from South Sea countries as consignment

and maintain the same amount of sales of plywood. With

tight supply of logs in Malaysia and decreasing

plywood production in Japan, log purchase by Japan will

further decline.

Present export log prices of Sarawak meranti are US$276-

278 per cbm FOB on regular, US$255-260 on meranti

small and US$240-245 on super small.

European lumber import in 2016

Total import of European softwood lumber in 2016 was

2,736,628 cbms, 14.8% more than 2015 and this was the

highest since 2013. Supply of stud and lamina increased

by active housing starts of wooden units and structural

laminated lumber. In particular, increase of lamina is

noticeable, which supply had been tight all through the

year.

The European suppliersˇŻ aggressive production for

Japan,

stimulated by higher export prices by strong yen,

contributed increased import. Stud, taruki and 2x4

lumber, which are planed processed products are 936,528

cbms, 7.7% more. Semi ¨Cfinished products like lamina and

genban are 1,800,100 cbms, 18.9% more.

By source, Finland, which is the main source of lamina,

was 941,468 cbms, 13.2% more. Sweden was 767,584

cbms, 19.9%. These two countries exported more than

1,700,000 cbms, which took 62.5% share in total

European lumber.

Finland volume increased by newly built Keitele group

mill so not only semi-finished lamina and genban but

finished products like stud increased. Austria, where Stora

Enso has sawmills, shipped 354,432 cbm, 13.3% more

while Rumania, where Schweighofer has sawmills,

decreased to 238,835 cbms, 11.1% less.

Germany, where Schweighofer newly acquired sawmills,

shipped 133,326 cbms, 117.5% more. Czech was 107,312

cbms, 4.5% less. Latvia was 131,194 cbms, 20.1% more.

Estonia was 48,196 cbms, 30.8% more.

Supply of stud was unstable due to tight supply of quality

logs in the first half of the year then with higher export

prices stimulated supply in the second half of the year.

North American log import in 2016

North American log import in 2016 was 2,790, 662 cbms,

8.8% more than 2015. This is the first increase after three

years. U.S.A. increased 2.7% and Canada also increased

by 22.2%. Douglas fir logs increased by about 30% due to

recovery of plywood demand and strong demand for

lumber.

However, both did not make 2014 level and total was

under 3 million cbms for two straight years.

By species, Douglas fir was 2,542,547 cbms, 9.8% more

than 2015. Hemlock was 155,265 cbms, 20.5% more.

Spruce was 41,448 cbms, 31.1% less. Yellow cedar

(cypress) was 12,162 cbms, 11.4% less. Red cedar was

5,533 cbms, 42.4% less. White fir was 36 cbms, 91.5%

less. Hardwood was 33,671 cbms, 3.1% less.

Both Douglas fir and hemlock increased but others are all

down. Douglas fir sawmills increased the production in an

anticipation of rush-in demand before consumption tax

hike then plywood mills, which reduced the production in

2015, made a full operation in 2016 by active demand so

both contributed to increase Douglas fir volume.

Volume from the U.S.A. was 1,733,391 cbms, 2.4% more

then volume from Canada was 809,156 cbms, 29.9%

more. Market of Canadian Douglas fir was mainly

plywood then since 2016, Chugoku Lumber, the largest

Douglas fir lumber manufacturer in Japan, started

purchasing Canadian Douglas fir so this contributed

increase of Canadian Douglas fir log import.

Despite increase of Canadian logs, U.S.A. remains

dominant supply of Douglas fir logs. If Canada puts up

more logs for export, Japan would be buying more

Douglas fir logs from Canada.

Hemlock volume from Canada was 149,168 cbms, 19.6%

more while that from the U.S.A was 6,097 cbms, 47.4%

more. Spruce from Canada was 11,804 cbms, 69.4% less

and from the U.S.A was 29,644 cbms, 37.5% more.Yellow

cedar volume from Canada was 7,632 cbms, 20.8% less

and from the U.S.A. was 4,530 cbms. 10.9 % more. Red

cedar from Canada was 2,251 cbms, 68.0% less and from

the U.S. A. was 3,282 cbms, 28.3% more.

North American lumber import in 2016

Imported lumber volume in 2016 was 2,235,652 cbms,

4.4% less than 2015. This is three consecutive yearsˇŻ

decline. New wooden housing starts were 8.3% more than

2015 but the market share of North American lumber

dropped by supply expansion of competing materials. Also

supply decrease for Japan market by active North

American lumber market. Particularly Douglas fir lumber,

which is used for traditional type housing in Japan,

dropped by 11.6%. Compared to recent peak of 2013, it is

34.2% drop.

By species, SPF was 1,347,236 cbms, 0.2% less than

2015. Douglas fir was 419,133 cbms, 11.6% less.

Hemlock was 293,897 cbms, 1.5% less. Yellow cedar was

68,490 cbms, 17.2% less. Sitka spruce was 11,524 cbms,

29.8% less.Hardwood was 50,914 cbms, 16.8% less so all

the species decreased from 2015.

2x4 SPF lumber has no other substitution so it should

increase as 2x4 housing starts increases, which was 7.9%

more but in the first half of the year, the housing demand

was slower then in the second half, supply got tighter so

Japan could not purchase enough volume.

Softwood lumber agreement between U.S. and Canada,

which imposed 15 % duty on export lumber from Canada,

expired on October 2016 so the lumber shipment from

Canada to the U.S. increased.

Douglas fir lumber had to compete with European lumber,

domestic lumber and Douglas fir lumber manufactured by

domestic sawmills. By source, Canada was 217,500 cbms,

7.3% less and the U.S.A. was 201,633 cbms, 15.7% less.

Hemlock did not drop so much but compared to 2014, it is

13.2% less. In the second half of the year, hemlock supply

was ample. Yellow cedar and red cedar were largely

affected active shipment for the U.S. market and resultant

higher prices.

|