|

Report from

Europe

EU wood furniture surplus narrows as imports rise

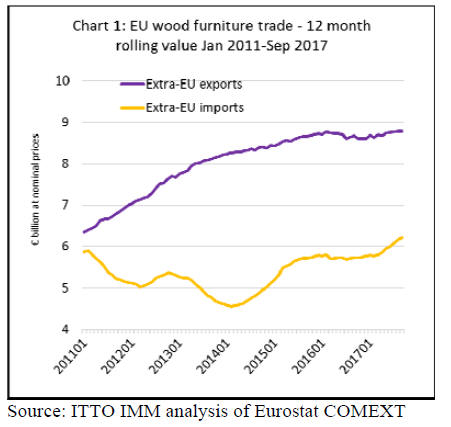

The EU has maintained a trade surplus in wood furniture

since 2011 when exports to non-EU countries overtook

imports from outside the EU. This surplus remained

broadly flat between the start of 2015 and the first quarter

of 2016 (averaging close to euro3 billion per annum), as

both imports and exports were stable.

However, the trade surplus narrowed sharply in the second

and third quarters of 2017 (to around euro2.6 billion per

annum) as imports began to pick up. (Chart 1)

The narrowing of the EU trade surplus is an encouraging

sign for external suppliers of wood furniture into the EU

that have struggled to compete in a market where domestic

suppliers account for around 85% of total share.

The dominance of EU manufacturers in this sector is due

to various factors including the strength of domestic

brands in terms of innovation and design, the obstacles to

overseas suppliers complying with complex EU technical

and environmental standard, and the expansion of

furniture manufacturing in EasternEurope, a location

which combines ready access to raw materials, relatively

cheap labour, and the internal EU market.

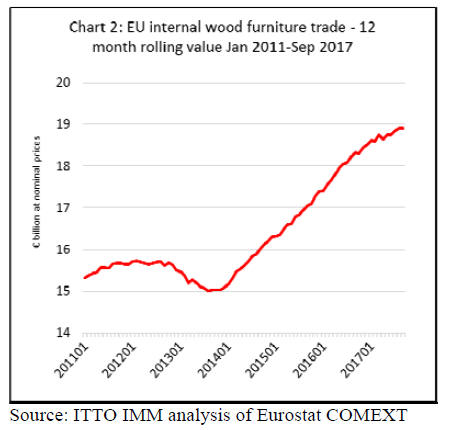

Improved economic conditions in pe have been driving a

rise in wood furniture consumption in the last three years.

Rising consumption combined with the growth of

manufacturing in Eastern pe, particularly in Poland,

Romania and Lithuania, is reflected in a rapid rise in EU

internal wood furniture trade, from an annual level of

euro15 billion at the start of 2014 to nearly euro19 billion

by the end of 2017. (Chart 2)

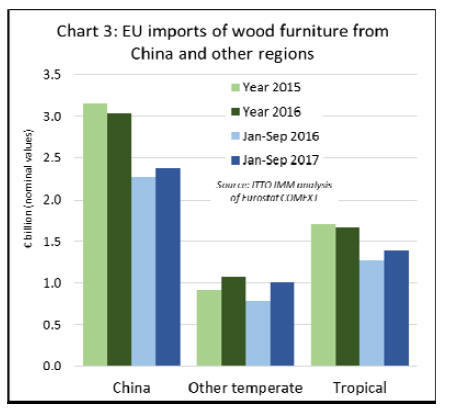

The pace of the rise in internal EU wood furniture trade

tailed off a little during 2017. However, last year there was

a rise in the pace of EU wood furniture imports from

outside the region. Between January and September 2017,

the EU imported euro1.39 billion of wood furniture from

tropical countries, nearly 9% more than the same period

the previous year. EU imports from China also increased,

by 4% to euro2.38 billion in the same period.

However, the biggest gains in EU imports of wood

furniture in 2017 were from other temperate countries,

notably Bosnia, USA, and Ukraine. EU imports from these

countries increased 28% to euro1.01 billion in the first 9

months of 2017, building on a 14% gain recorded the

previous year. (Chart 3)

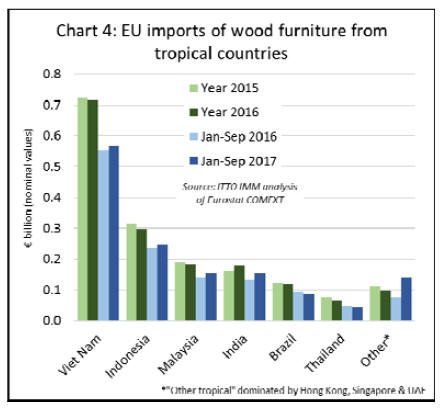

In the first nine months of 2017, EU imports increased

from all four leading tropical supply countries; rising by

3% from Vietnam to euro567 million, 4% from Indonesia

to euro246 million, 11% from Malaysia to euro154 million

and 16% from India to euro154 million.

There was also a significant rise in EU imports from Hong

Kong, Singapore and the UAE during the same period. In

contrast imports from Brazil fell 8% to euro85 million and

imports from Thailand declined 6% to euro45 million.

(Chart 4)

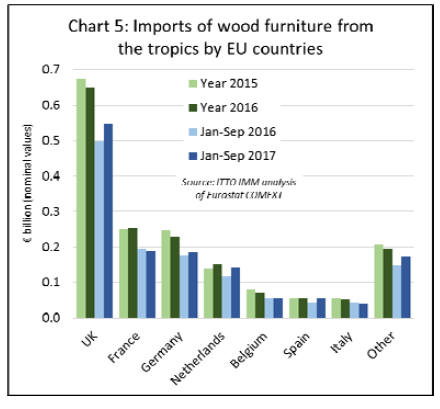

The increase in EU imports of wood furniture in the first

nine months of 2017 was concentrated in the UK (rising

9% to euro546 million), Germany (rising 4% to euro185

million), Netherlands (rising 21% to euro142 million) and

Spain (rising 31% to euro57 million).

Although the quantities are still quite limited, several

smaller EU markets also recorded significant percentage

increases in wood furniture imports from tropical countries

in 2017 including Sweden, Denmark, Poland, Ireland and

Greece. (Chart 5)

Global furniture production dominated by China

Total furniture production in the worldˇŻs 100 largest

countries, by GDP, was valued at USUS$430 billion in

2017. This is a key conclusion of ˇ°World Furniture

Outlook 2018ˇ±, the flagship publication of CSIL, the

Italian furniture research organisation.

The report includes details of the furniture sector in 100

countries which account for 90% of world population and

95% of world GDP. The report considers furniture in all

materials but excluding lamps and mattresses.

The CSIL report highlights the extent of ChinaˇŻs

dominance as the worldˇŻs largest furniture manufacturer.

Last year China alone accounted for nearly 40% of global

production. USA, the second largest producer, accounted

for 12%, followed some way behind by Germany (5%),

Italy (4%), India (4%), Poland (3%), Japan (2%), Vietnam

(2%), UK (2%) and Canada (2%).

The CSIL report shows that international trade in furniture

was USUS$140 billion in 2017, corresponding to around

1% of total global trade in manufactured goods. After a

sharp rise in the value of global furniture trade in the

decade prior to 2012, trade has remained broadly flat in

the past five years.

Furniture exports in China, the largest exporter, were

around US$51 billion in 2017, a slight gain on the

previous year but lower than in 2015.

Exports in Germany and Italy, the next largest, were both

valued at around US$11 billion in 2017, a level that has

hardly changed in the last 8 years. However, exports have

been rising in Poland and Vietnam, reaching around

US$10 billion and US$8 billion respectively in 2017.

The US is the worldˇŻs largest furniture importer, with

imports of around US$34 billion in 2017 having risen

continuously from only around US$24 billion in 2010. The

value of imports in the next largest importing countries ¨C

Germany (around US$13 billion in 2017), the UK (US$7

billion), France (US$7 billion) and Canada (US$6 billion)

¨C were broadly flat during the same seven-year period.

CSIL forecast that global consumption of furniture will

rise by 3.5% in real terms in 2018. The fastest growing

region continues to be Asia, with all other regions growing

between 1% and 3% in real terms.

While ChinaˇŻs furniture production continues to rise

rapidly, export growth is more subdued according to

CSIL.

Drawing on commentary from Chinese manufacturers,

CSIL reckons that Chinese furniture export growth is

unlikely ever to return to levels seen earlier this decade for

several reasons including: rising labour rates in China; the

progressive appreciation of the Renminbi against the US

dollar between 2003 and 2016; rising competition

particularly from Vietnam; and the rapid growth in

ChinaˇŻs internal demand.

Currently around 30% of ChinaˇŻs furniture production is

exported, but this proportion is gradually declining as

more product is sold into the domestic market.

For further details:

https://www.worldfurnitureonline.com/research-market/worldfurniture-

outlook-0058524.html

Growth in hospitality sector creates new opportunities

According to recent CSIL research carried out with focus

on 16 Western pean countries, the total value of the pean

market for contract furniture and furnishings in 2016 was

euro7.5 billion while total production was 9 billion.

The sector was expanding in 2016 with yachting, luxury

retail, and the hospitality sectors (hotels, bars and

restaurants) being the fastest growing segments while

sectors dependent on public funds, such as schools and

hospitals, were much less dynamic.

CSIL has also carried out detailed research on the global

development of hotel rooms, a sector significant for

tropical hardwoods due the relatively large amount of

higher end furniture and finishing materials used. CSIL

estimate that in 2016 the total global stock of hotel rooms

was 16 million with most recent growth in the Asia-Pacific

region.

Between 2012 and 2016, the share of hotel room in the

Asia Pacific region increased from 22% to 26%, while the

share declined in pe from 30% to 28% and in North

America from 41% to 38%. The share of hotel rooms in

Africa, the Middle East, and South and Central America

remained stable with values ranging between 3% and 5%.

CSIL estimate that 650,000 hotel rooms were under

construction globally in 2016, of which 40% were in Asia-

Pacific, while North America accounted for 29% and

Europe only 10%. However, demand for new hotel rooms

is expected to remain high in all regions with the glow

flow of tourists forecast to increase 3% per year on

average until 2030.

While Asia-Pacific has seen the most recent growth, the

US continues to be the leading world market for hotel

furniture and furnishings, accounting for 36% of total

global demand in 2016. The Asia-Pacific region is now the

second largest market, accounting for 28% in 2016,

overtaking Europe which accounted for 26%, followed by

Africa and the Middle East (7%), and Central and South

America (3%).

Total sales of hotel furniture and furnishings were at a

similar level in the United States and China in 2016, in the

region of US$5 billion in each country.

Other large markets with demand between US$1 billion

and US$5 billion are Germany, the UK, Japan, Canada

and Russia. Countries currently with smaller markets but

where demand is rising rapidly include Australia, UAE,

Thailand, Indonesia, Singapore, and the Philippines.

CSIL estimates that the rate of worldwide construction of

hotel rooms is likely to have increased nearly 10% in 2017

to 710,000, with Asia-Pacific accounting for 37% of the

total, North America for 33%, the Middle East for 12%,

Europe for 10%, Africa for 5% and South America for

4%. CSIL expect that this rapid rate of growth will

continue in 2018.

ITTO/EC IMM Report

ITTO/EC IMM Report

New IMM website with regular information on tropical

trade in the EU

The FLEGT Independent Market Monitoring (IMM)

mechanism, which is hosted by ITTO with EC funding,

has just launched a new website at www.flegtimm.eu. The

first edition of the free IMM Newsletter can be accessed at

the website and there is also the opportunity to sign up to

future editions which will be released at least quarterly.

The IMM, which began operation in 2014, uses trade flow

analysis and market surveys to independently assess

market impacts of FLEGT Voluntary Partnership

Agreements (VPAs). During 2017, the IMM expanded its

market research programme to cover seven key EU

countries, which account for roughly 90% of EU tropical

timber imports from VPA partner countries.

IMM market research has been based on online surveys

and structured interviews with trade representatives,

government agencies and NGOs.

This market research programme runs alongside IMMˇŻs

analysis of trade flow statistics and other timber trade

related data, most recently presented in the IMM report

"FLEGT VPA Partners in EU Timber Trade 2014 to 2016"

(also now available at www.flegtimm.eu).

The IMM Newsletter includes insights from the IMM EU

market scoping surveys as well surveys of Indonesian and

Ghanaian companies exporting forest products into the

EU.

It also covers an analysis of EU-Indonesia timber trade

since the start of FLEGT licensing and background

information on how the Indonesian system works, as well

as analysis of FLEGT-licensing teething troubles and EU

economic trends.

Interviews with Mike Worrell of the UK Timber Trade

Federation and Dr RufiˇŻie of the Indonesian Ministry of

Environment and Forestry provide further insights into

Indonesian FLEGT licensing, while VPA Joint

Implementation Coordinator Edwin Shanks explains next

steps towards VPA implementation in Vietnam.

The IMM website will be developed further in 2018,

providing constantly updated data on EU timber trade and

market trends, as well as details of IMM research and

activities.

|