|

Report from

Europe

European plywood sector pushes

through pandemic

Expectations of the impact of the Covid-19 pandemic on

the European plywood sector turned out to be worse than

the reality.

Nevertheless, overall trading levels in the first half of 2020

are reported sharply down. Some fear business may not

return to pre-crisis levels until a vaccine is found for the

virus and there is concern among importers over the longer

term repercussions of the crisis for European national

economies, particularly for employment, with predictions

that Brexit may add to market stresses.

EU and UK plywood importers and distributors took a

range of steps to comply with social distancing and other

health guidelines throughout the lockdown, itˇŻs reported

that most of the sector did keep trading.

ˇ°We divided the workforce into teams, working several

days on, several off, both in order to meet distancing rules

and so that, if anyone fell sick, weˇŻd have a back-up,ˇ± said

a director of one leading EU importer.

Another company said its strategies differed across the

national markets it services. ˇ°In France at the height of the

pandemic and lockdown, we were down at one point to

around to around 10-15% of normal activity, so reined in

operations accordingly. In the UK only our main directors

came in, while everyone else worked from home, but in

the Netherlands, Belgium and Germany we pretty much

continued as normal,ˇ± they said.

A major UK importer distributor said they had furloughed

just six people out of a workforce of 90. ˇ°Our offices were

big enough to maintain distancing rules and we adapted in

other ways,ˇ± they said.

ˇ°For instance, delivery drivers stayed in vehicles to

minimise contact and we went even more paperless,

sending delivery and order notes to tablets and

smartphones. ItˇŻs really demonstrated the value of new

technology and digitization, with staff and supplier

meetings online and sales communicating with customers

remotely, all with no appreciable adverse impacts on

business. WeˇŻll probably stick with some of these

approaches post-pandemic. ˇ±

The fall in turnover in the first six months of 2020 varied

according to importersˇŻ product mix and national markets,

with estimates ranging from 15% to 35%. However, some

had expected a bigger contraction.

ˇ°Sales falling by between fifth and a third obviously is bad

news, but mid-March into April, when the health crisis

was at its peak and the media full of dire predictions, we

discussed contingences for a more serious situation,ˇ± said

one company.

A multi-national importer/distributor reported the French

market through April into May down 75%, the UK 65%

and Belgium 35%, but business in the Netherlands and

Germany was significantly less affected. ˇ°The Germans

and Dutch lockdowns either werenˇŻt as severe, or

businesses coped better,ˇ± they said. ˇ°The result was that

most customers were able to carry on near normally.ˇ±

One company said its sales in these two countries had

enabled it to maintain first half construction sector

business overall at 90-95% of 2019 levels. ˇ°We actually

saw surprisingly few site closures generally and also the

building sector had benefited from a mild winter, so

ongoing projects hadnˇŻt been interrupted or building starts

delayed due to bad weather. As a result, the sector went

into the pandemic period at strong levels of activity.

Demand from customers in infrastructure also held up

well. Projects were possibly brought forward by

contractors to take advantage of lower traffic levels and by

local and central government also to help maintain

economic activity.ˇ±

Merchants and small to medium sized distributors were

the mainstay of another importersˇŻ business from March

through June, particularly those servicing smaller builders

and private customers.

ˇ°Some bigger distribution chain customers and larger

construction contractors we service curtailed operations,

but traditional merchants were busy, as were builders

working on smaller projects, repair and refurbishment,

plus the DIY sector. Consumers clearly took advantage of

lockdown to do home improvements,ˇ± said an

importer/distributor.

UK importers painted a similar picture, with DIY trade

holding up particularly well. One had also seen strong

demand from retail and hospitality for plywood and OSB

to board up locked down premises.

UK construction activity varied from site to site, some

closing, others continuing, operating to health guidelines.

Most interruption was reported in Scotland where the

sector was hit by the strictest lockdown rules.

In common with most continental counterparts, a UK

company said their worst affected areas were packaging,

shop fitting, the exhibition sector and hospitality

refurbishment.

ˇ°Some shops have used it to refurb, but the sector

generally didnˇŻt go into lockdown in a strong position, due

in particular to online retail growth, so didnˇŻt have the

resources,ˇ± said the importer.

ˇ°WeˇŻve also seen a sharp downturn in anything to do with

manufacturing. That includes sales to the automotive

sector, boat building and particularly furniture

production.ˇ±

Another continental importer described the packaging

business as a ˇ®disaster areaˇŻ ¨C down at least 50%. ˇ°ItˇŻs

dependent on transport of goods which, of course, was

severely curtailed,ˇ± they said.

Serious interruption of Chinese plywood supply to

Europe

On supply, some interruption was reported out of

Indonesia and Malaysia due to the lockdown; some

factories reported to have closed for several weeks, others

reduced output. But the major issue was with the Chinese

product. The combined effects of Chinese New Year and

pandemic saw shipments dry up.

The impact was partially softened by lower demand in

Europe, but companies still report they are coming close to

selling out.

ˇ°WeˇŻd stocked up as usual ahead of New Year. But rather

than the usual two to three weeks hiatus in supply, it was

seven to eight, mid-January to the end of March,ˇ± said an

importer.

ˇ°Basically, we cleared our stocks and most customers

were sold out, particularly on film-faced and other

construction and industrial product. Even now, whateverˇŻs

coming in from China is presold and immediately going

out again.ˇ±

Through May, Chinese and other S.E Asian supply was

reported to have recovered and combined with slight

weakening of the yuan, the consequence, said an importer,

is that there is now more ˇ°flexibility on priceˇ±. ˇ°ItˇŻs

generally not substantial, although there are some

suppliers hungrier for business than others and open to

offers,ˇ± they said.

Despite the supply issues, bar moderate weakening in

Chinese product more recently, importers report S.E.

Asian prices have been stable over the last few months,

with just ˇ°minor adjustmentsˇ±.

The supply of Brazilian elliottis and Russian birch

plywood, however, has been on a downward trend, the

former falling 20 to 25% over the first half of 2020, the

latter 10%.

ˇ°Combined with the weakening of the Brazilian real,

which, despite slight recent recovery early June was still

25% to 30% lower than at Christmas, this left European

importers who bought January and February, when prices

were actually increasing, with expensive stocks theyˇŻve

had to discount,ˇ± said one company.

ˇ°There are signs prices have bottomed out, but, with the

pandemic worsening in Brazil and their domestic market

contracting, you never know.ˇ±

Russian price cutting was described as an ˇ°over reaction to

market conditionsˇ±. ˇ°[Russian] suppliers have had

problems. First, they had a mild winter and log shortages,

then came the pandemic and contraction of the building

interiors market, which is significant for them,ˇ± said an

importer.

ˇ°But Russian suppliers seemed to get into a race for the

bottom. Whether theyˇŻve reached it yet is unclear. These

are big companies which may have room for more cuts. As

with elliottis, itˇŻs meant write offs and particularly bigger

stock-holding importers losing a lot of money.ˇ±

European plywood imports slump

According to analysis of latest UK Government and

Eurostat statistics, total plywood imports by the

EU27+UK (excluding internal trade) dropped by 16% to

1.58 million cu.m from January through April this year

compared to the same four months last year. This follows

a dip of 5.3% to 4.4 million cu.m for the full year in 2019.

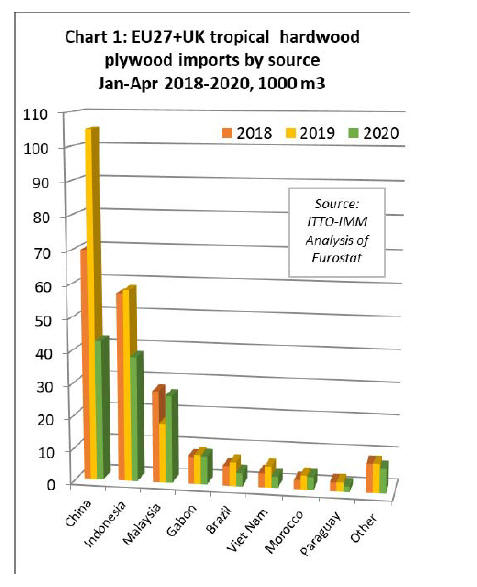

EU27+UK tropical hardwood plywood imports, including

both direct from the tropics and from non-tropical

countries, were 137,000 cu.m between January and April

this year, 38% less than the same period in 2019.

EU27+UK tropical hardwood plywood imports from

China from January through April were 59.5% lower at

43,000 cu.m.

Imports of tropical hardwood plywood also declined

sharply from Indonesia (down 34.6% at 38,000 cu.m),

Gabon (down 3.3% at 9,000 cu.m), Brazil (down 43.9% at

4,000 cu.m) and Viet Nam (down 45.8% at 4,000 cu.m).

However imports from Malaysia were up 47.1% at 27,000

cu.m (Chart 1).

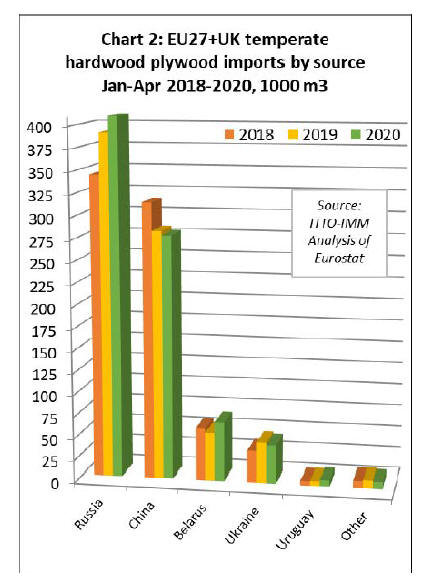

In contrast to tropical hardwood plywood, EU27+UK

imports of temperate hardwood plywood were up 3.1% at

815,000 cu.m in the first four months of 2020. Imports of

this commodity from Russia were 4.8% ahead at 410,000

cu.m, from Belarus up 22.7% at 67,000 cu.m, and

Uruguay up 31.9% at 7,000 cu.m.

However, imports of temperate hardwood plywood from

China were down 1.7% at 278,000 cu.m and from Ukraine

down 5.6% at 44,000 cu.m (Chart 2).

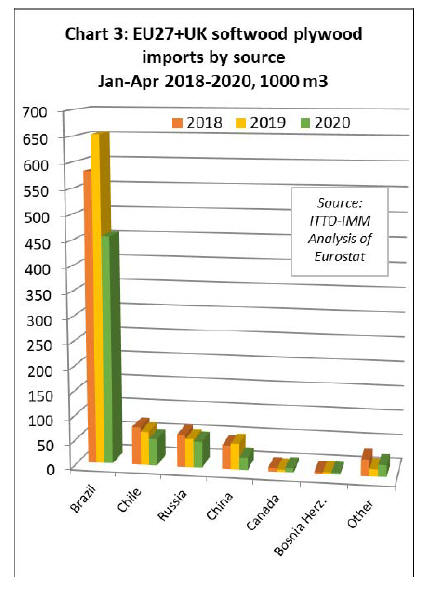

EU27+UK imports of softwood plywood declined 27.1%

to 623,000 cu.m in the first four months of 2020. Imports

from Brazil were 30.3% lower at 456,000 cu.m, from

Chile down 20.9% at 54,000 cu.m, Russia down 7.5% at

53,000 cu.m and China down 52.7% at 25,000 cu.m, while

those from Canada rose 77.5% to 8,000 cu.m (Chart 3).

Uncertain outlook for European plywood market

As for the outlook for the European plywood sector,

importers said it remained a difficult call. ˇ°There are so

many variables,ˇ± said one company. ˇ°ThereˇŻs anxiety

about a second spike in Covid-19 in Europe, and weˇŻve

already seen renewed outbreaks and subsequent localized

lockdowns in Germany.

ˇ°ThereˇŻs been consumer confidence and market recovery

from mid-May through June and we see the position

continuing to improve through the summer, but it wonˇŻt

take many more such instances for that to be threatened.

ThereˇŻs talk too of the risk of company failures and

accelerating job losses as government pandemic business

support programmes are wound down, with

unemployment forecast to be a major drag on the

European economy. Then thereˇŻs the worry of the course

of the disease elsewhere in the world.ˇ±

Prospects in construction are also causing concern. ˇ°I

think weˇŻll see an upturn in activity as those projects that

were delayed come back on stream, with more work done

than normal through July and August,ˇ± said an importerdistributor.

ˇ°But, as these projects complete, are we going to see new

ones starting? Some governments are pump priming the

sector, with Germany and the UK, for instance, promising

multi-billion infrastructure spending. But not everyone is

going to have that kind of resource.ˇ±

These concerns are borne out by latest forecasts from

Euroconstruct. It predicts that its 19 member countries in

2020 will see an overall contraction in construction

turnover to €1.5 trillion, the lowest figure since 2015. In

Germany the fall will be just 2.4%, but in the UK and

Ireland could be as severe as 33% and 38% respectively.

While building output will start recovering in 2021,

Euroconstruct predicts that in 2022 it will still only be

back to 2018 levels. Euroconstruct adds that there are

also downside risks to its forecast, the most significant

being the coronavirus and its containment.

Adding to importersˇŻ challenges, they also report greater

difficulty in meeting EUTR due diligence requirements

due to a combination of having furloughed their own

personnel, and suppliersˇŻ offices also being short-staffed,

so processing documentation more slowly. ˇ°And EU

competent authorities are making no allowances,ˇ± said one

company.

Another reported that the Belgian competent authority is

also scrutinizing FLEGT-licensed cargoes more closely.

ˇ°Whether itˇŻs to do with IndonesiaˇŻs proposed then

abandoned move to drop the obligation on companies to

provide legality assurance on timber exports is unclear,ˇ±

they said. ˇ°But it seems excessive.ˇ±

A UK importer voiced the sectorˇŻs consensus about the

immediate future. ˇ°Business continues to pick up and

weˇŻre being positive, but itˇŻs going to be challenging. We

think our new norm will be about 15-20% below 2019

business levels; where we were doing £10 million a

month, weˇŻll now be on £8-8.5 million,ˇ± they said.

ˇ°We hope to be proved wrong, but at the moment we canˇŻt

see that changing significantly until a Covid-19 vaccine is

out there.

ˇ°Then thereˇŻs the downside risk posed to us and the rest of

Europe by Brexit. The pandemic has taken months out of

negotiations and the risk of the UK exiting the EU without

a trade deal is reported as very real. On top of the health

crisis, that could be tough to cope with. Our hope is that

they extend the transition period so they can come to a

deal and we only have one crisis to manage.ˇ±

Brexit ˇ®rears its headˇŻ once more

In a recent blog post, the UK TTF Managing Director

David Hopkin notes that ˇ°just when we thought it was safe

to go back into work from COVID-19, the lurking beast of

Brexit has reared its head once moreˇ±.

Mr. Hopkins was responding to issues raised by UK

government announcements on the VAT and trade tariff

regime planned to be implemented in the UK after the

current Brexit transition period has ended, from 1st January

2021, in the event of no deal with the EU ¨C or even in the

event of a deal being reached.

According to Mr. Hopkins ˇ°as negotiations continue, the

threat of no-deal Brexit ¨C something everyone said they

wanted to avoid ¨C now looks increasingly likely. Indeed,

there often seems little difference between the deal the

Government wants, and no-deal anywayˇ±.

Mr. Hopkins goes on to note that ˇ°the issues around this

are multiple and various. None are insurmountable, but all

need to be discussed openly and transparently with

sufficient time to consider all sides of the argument. But,

time and scrutiny are the very things the Government is

keen to avoid in its rush to the finish line.

ˇ°Already we have seen the Government U-turn on a huge

number of areas where previously we had been given

concrete assurances and thought we had certainty for

example, payment of VAT on imports. Last year, the

Government, in a signed letter from the Chancellor,

assured TTF that importers could continue the same

regime as before and defer payments over time to ease

cash-flow.

ˇ°In February, the Prime Minister broke this promise,

telling all businesses that VAT would be payable upfront,

in one sum, on all imports. This poses huge problems for

smaller importers. Promises on frictionless trade, tariffs

and other areas of business have gone the same way.

Mr. Hopkins then referred to the discussions the TTF has

held with members on the proposed ˇ°UK Global Tariffˇ±

published on 19 May. The tariff will apply to all goods

imported into the UK unless the goods come from

countries that are part of the GSP system or from countries

that have a trade agreement with the UK.

Mr. Hopkins was sharply critical of the UK governmentˇŻs

ˇ°proposed new tariffs for engineered timber and plywoodˇ±

noting that ˇ°we were previously told these would never be

imposedˇ± and that ˇ°we will be looking at how we can

overcome this and other issues within the post-Brexit

regimeˇ±.

While that is the TTF perspective, other observers have

been more generous to the UK government stance on

tariffs, suggesting that, at this stage of trade negotiations

with the EU and other partners, rather than unilaterally

removing tariffs now, it makes sense for the UK to keep

the flexibility to cut tariffs in future.

Furthermore, the tariffs the TTF refer to are not ˇ°newˇ± in

the sense that they have always been imposed on supplies

from outside the EU. What is ˇ°newˇ± is that UK imports

from EU countries would now be subject to the same

constraints.

While disruptive to existing UK supplier relationships

with the EU, it would enhance the competitiveness of

other suppliers to the UK, including in the tropics, who

would be treated on a level playing field.

For this reason, non-EU suppliers of those wood products

currently subject to tariffs for import into the EU ¨C which

include veneer, plywood, other laminates, panels,

marquetry, doors and windows, picture frames, bamboo

and rattan furniture, and wood furniture components ¨C

would all benefit in the UK market in the event of a ˇ°no

dealˇ± Brexit, even if the UK were to simply adopt the

EUˇŻs existing tariff schedule.

Of course, this benefit is only in terms of relative

competitiveness and takes no account of the potentially

serious and detrimental hit to the overall economy of the

UK, and to a lesser extent the EU, in the event of a no-deal

Brexit. From that best perspective, no-deal is best avoided.

In practice the UK is not proposing to simply replicate the

existing EU tariff schedule, but to adjust it to better reflect

the UKˇŻs own interests. Certain EU industries that the EU

is helping to protect through the tariff schedule have little

or no presence in the UK. The UK can be expected to

either reduce or totally remove tariffs for these sectors.

In practice the UK home-grown wood products sector is

relatively small and narrowly focused compared to many

other European countries ¨C the commercial forest resource

being heavily oriented towards spruce plantations.

The country has a very long tradition of importing to fulfil

its wider wood needs, more so than elsewhere in the EU,

and therefore is likely to be more inclined to reduce wood

import tariffs.

This discussion is academic for quite a few wood

products. The EU already imposes zero-tariffs on all logs

and rough sawn timber, together with all finished wood

furniture, as well as for all types of wood fuel, including

chips, pellets, charcoal, sleepers, tools, shuttering, shingles

and shakes, posts and beams, glulam, tableware and

kitchenware.

For nearly all wood product groups where the EU applies

tariffs, the UK is now proposing either to reduce or

eradicate tariffs for UK global imports. The main changes

proposed are as follows:

The EU tariff of 2.5% that applies to all ˇ°sandedˇ±

sawnwood would be reduced to zero in the UK.

The EU tariff of 2% specific to tropical hardwood

that is ˇ°planedˇ± would be reduced to zero in the

UK.

The EU tariff on veneers, which ranges between

3% to 6% depending on degree of processing and

species, would be reduced to zero in the UK.

The EU 7% tariff on plywood, including with

outer ply of tropical hardwood

(4412110/44123190), other hardwood

(44123300/4412400), and softwood (44123900),

would be reduced to 6% in the UK.

The EU 7% tariff on MDF and other fibreboard,

OSB and other particle board would be reduced

to 6% in the UK.

The EU 2.5% tariff on picture frames and similar

products made of tropical wood, would be

reduced to 2% in the UK.

The EU 3% tariff on wooden doors and door

frames, windows and window frames, parquet

flooring panels, which applies to all wood species

including tropical wood, would be reduced to 2%

in the UK.

The EUˇŻs 3% tariff on statuettes and jewelry and

cutlery boxes made specifically of tropical wood,

would be reduced to 2% in the UK.

The EU 4% tariff on wood packing cases, boxes,

crates, box pallets and similar, would be reduced

to zero in the UK.

The EU 5.6% tariff on bamboo and rattan

furniture would be to 4% in the UK.

The EU 2.7% tariff on wooden furniture

components would be reduced to 2% in the UK.

The only wood products where the UK proposes to retain

the existing EU tariff are: laminates and veneered panels

under 441294 and 441299, for which there is a tariff of 6%

or 10% depending on the exact specification; bamboo

plywood which will continue to be subject to a 10% tariff;

and wood marquetry, subject to a 4% tariff.

The UK is not proposing to increase tariffs on any wood

products.

|