Japan

Wood Products Prices

Dollar Exchange Rates of 10th

May

2021

Japan Yen 108.84

Reports From Japan

Country struggles to contain

fourth wave of infections

Japan put in place a third state of emergency in Tokyo and

some other areas late last month and has extended the

measures until the end of May as the country struggles to

contain a fourth wave of infections.

The restrictions on businesses have, once again, hit the

service sector hard and in April business confidence in this

sector fell at the fastest pace in a year as curbs aimed at

containing a resurgence of COVID-19 infections

depressed consumer spending.

Business analysts are beginning to suspect the changes to

businesses and society brought on by the pandemic could

be long lasting or possible irreversible. The structure of

the business sector in Japan, as elsewhere, is becoming

more polarised.

On the one hand digitalisation and work-from-home

demand have boosted the performance of some companies

on the other hand the transportation, restaurant and

tourism sectors have been devastated. There is a growing

view that even after the pandemic is controlled structure of

industries will alter.

Despite the severe situation the country finds itself in the

Cabinet Office insists that JapanˇŻs economy is

ˇ°improvingˇ± based primarily on a rebound in exports.

See:

https://www3.nhk.or.jp/nhkworld/en/news/20210503_03/

Big drop in household spending

The latest government data shows that year on year

household spending surged in March marking the biggest

single monthly gain in almost 2 years but this was not so

startling as it appears as spending in March 2020 tumbled

as the extent of the pandemic became known.

Data for April is not yet available but the new state of

emergency in the big cities and restrictions elsewhere

along with the slow and disorganised vaccination effort is

bound to drive spending down again.

Analysts forecast the Japanese economy will have fallen

into negative territory for the January-to-March period as

consumer spending, a significant driver of growth, was

impacted by the restrictions. Twelve research institutes

released projections ahead of the official GDP

announcement scheduled for18 May all estimate negative

annualised growth.

Early end to US stimulus would impact

yen/dollar

exchange rate

The US dollar firmed to over yen 109.65 in early May as

there were growing concerns over inflation in the US and

that this may signal an earlier than expected end to US

stimulus spending which was set to be wound down in the

final quarter of this year. Analysts now suspect this could

happen earlier.

Fast widening income gap impacting housing

market

Economists in Japan talk of a K-shaped recovery to

explain parts of the economy are improving while others

are not and this is illustrated with house prices.

In Japan house and apartment prices in city centres are

rising, driven up by high income earners but have been

declining in outlying suburbs as middle and low income

earners are keeping out of the market or, for those worst

affected by the economic impact of the pandemic, even

having to sell their homes.

A fast widening income gap is emerging between highincome

earners and non-regular employees especially

those in the food and service sectors as such workers have

been the hardest hit by the loss of jobs and wage cuts.

While prices of expensive condominiums in urban centres

are rising but prices for inexpensive single-family homes

in outlying areas are falling as a result of weak demand.

Nationwide, average home prices over the past 6 months

fell 6% from a year earlier and home sales fell 14%

reflecting the impact of the pandemic.

See:

https://asia.nikkei.com/Spotlight/Datawatch/Japan-s-Kshaped-recovery-emerges-in-home-prices-amid-COVID-crisis

Import update

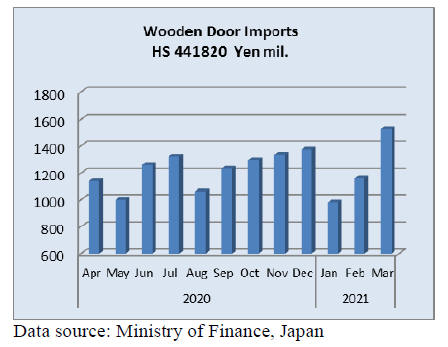

Wooden door Imports

JapanˇŻs first quarter 2021 imports of wooden doors

(HS441820) were up 5% on the same period in 2020 but

are still 20% below the value of first quarter 2019 imports.

In March 2021 manufacturers in China and the Philippines

provided most (87%) of JapanˇŻs wooden door imports

with manufacturers in Indonesia providing a further 5%

share of March imports. Shippers in China accounted for

62% of march door imports, up from levels in February.

Most of the balance was shipped from Europe and the US.

Year on year, March 2021 imports were 23% higher and

month on month there was an over 30% increase in the

value of wooden door imports.

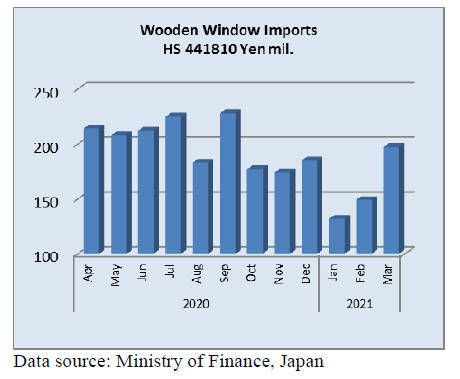

Wooden window imports

The value of JapanˇŻs wooden window (HS441810)

imports in the first quarter of 2021 was down 23% on the

same period in 2020 and down a massive 40% on first

quarter 2019 import values.

Year on year, March 2021 imports of wooden windows

were down 12% but month on month there was a 32%

increase in the value of imports. Three shippers, China

(46%), the US (24%) and the Philippines (15%) accounted

for most of JapanˇŻs wooden window imports in March

2021. The other significant shipper in March was Sweden

which accounted for around 9% of imports.

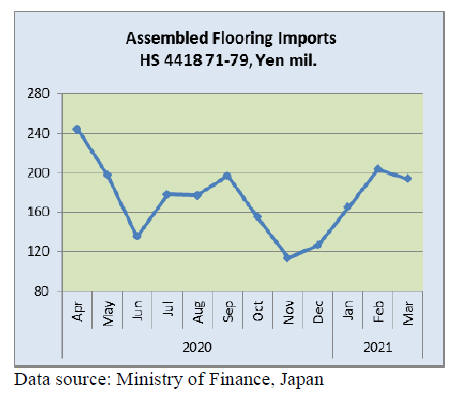

Assembled wooden flooring imports

The value of JapanˇŻs first quarter 2021 imports of

assembled wooden flooring (HS441871-79) was down 7%

compared to the same period in 2020 and 2021 imports

were 5% below that in the first quarter 2019.

Almost 60% of flooring shipments were of HS441875

with most coming from China and Malaysia.The second

largest category of wooden flooring was HS441879 which

accounted for just over 30% of all wooden flooring

imports. In this case, Indonesiaand the US were the main

suppliers.

Year on year, the value of JapanˇŻs imports of assembled

wooden flooring (HS441871-79) fell 7% and month on

month there was a similar 7% decline in the value of

imports. The March decline in flooring imports ended the

4 months of steady increases in the value of imports.

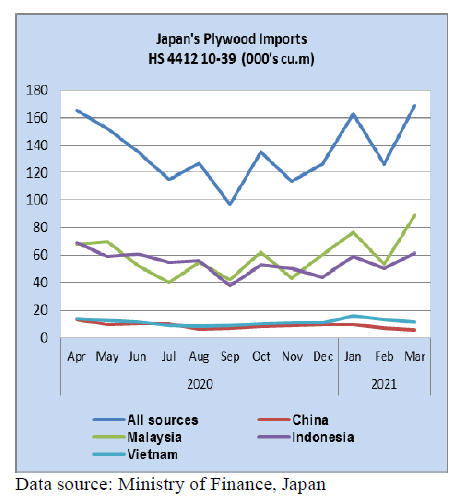

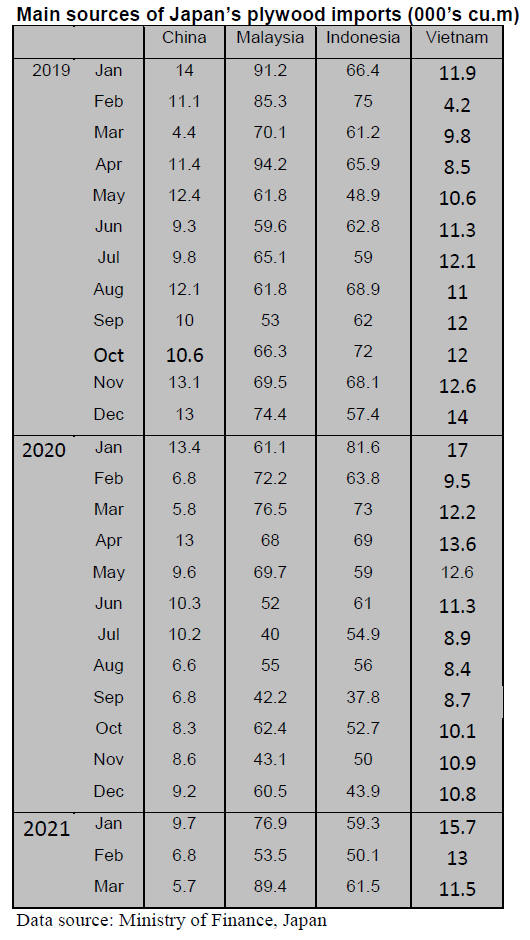

Plywood imports

JapanˇŻs first quarter 2021 imports of plywood (HS441210-

39) were down 8% on the same period in 2020 and were

down 11% on the volume of first quarter 2019 imports.

After a sharp drop in the volume of plywood imports in

February there was a correction in March which saw the

level of imports jump over 30% compared to February

with most of the increase being the result of higher

shipments from Malaysia, up almost 70% on February

shipments. Shipments of plywood from Indonesia, the

second largest shipper in March also increased but

shipments from Vietnam and China each declined in

March compared to levels in February.

Of the various categories of plywood imports HS441231

accounted for 91% of March 2021 imports with

HS441234, the second highest category.

Trade news from the Japan Lumber Reports (JLR)

The Japan Lumber Reports (JLR), a subscription trade

journal published every two weeks in English, is

generously allowing the ITTO Tropical Timber Market

Report to reproduce news on the Japanese market

precisely as it appears in the JLR.

For the JLR report please see:

https://jfpj.jp/japan_lumber_reports/

A third wood shock hits Japan

The first wood shock in early 1990s was triggered by

environmental issues and the prices of imported wood

products soared. The second wood shock occurred in 2006

when Indonesia restricted timber harvests.

Now Japan is suffering the third wood shock with

unprecedented supply shortage and sky-high prices.

Reasons are demand expansion of the U.S.A. and China,

which push the wood products prices higher. Another

reason is shortage of containers, which causes delayed

shipments.

The extreme supply shortage dried up inventory in the

distribution channels and dealers are desperately looking

for substituting materials.

To supplement shortage of imported wood products,

demand rushes to domestic wood which market is

climbing fast. This is abnormal situation as there is no

products available regardless of the prices. One of major

precutting plants started reducing taking orders by 10%

since April because it realises that necessary building

materials are not available.

The Japan Laminated Lumber Manufacturers Association

warned that the manufacturers are facing extreme

difficulty to obtain lamina with unexperienced high prices

so the manufacturers may have to reduce the production

by 20% after May. One of major laminated lumber

manufacturers, Timberam has already taken curtailment

program since April with 25% lower production.

Market of structural laminated lumber peaked in 2018 then

it had kept falling. With COVID 19 pandemic, the prices

of whitewood laminated post were down to about 1,750

yen per piece and redwood laminated beam prices were

about 50,000 yen per cbm delivered but considering high

cost of lamina, redwood beam prices should be 80,000 yen

and whitewood post should be 2,500 yen per piece.

In the second half of last year, demand recovered steeply

in China and the U.S.A. while Japan market remained

dormant so purchase power by Japan dropped relatively.

As a result, offers for Japan declined.

Container shortage caused delayed shipments. This

delayed shipments for the suppliers. Even when the

cargoes are ready for shipments they sit at loading ports so

for the suppliers are now reluctant to look for containers

and ship for Japan.

Even loaded containers hung up at transshipment ports

like Shanghai and Pusan so Japan market runs out

inventory of imported wood products. Delayed shipments

mean order balances of suppliers increases then suppliers

reduce new offers.

In 2020, world economy seemed to stagnated by COVID

19 pandemic but China succeeded to contain corona virus

spread and the economy recovered steeply in the second

half of the year. The U.S.A. record low mortgage interest

rate and house quarantine stimulates housing market and

the lumber market shot up sky-high.

In short, Japan is left behind from world market. Not only

North American and European products but the prices of

log and lumber from Russia, New Zealand and Chile

soared after January of 2021.

New forestry basic plan

The Forestry Policy Council of the Ministry of

Agriculture, Forestry and Fishery discussed new forestry

basic plan. In this, total wood demand forecast in 2030 is

87,000,000 cbms, 5,000,000 cbms more than 2019 in

which domestic wood demand 42,000,000 cbms,

11,000,000 cbms more than 2019.

Measures to stimulate low reforestation are necessary and

to revise registration system of harvest and reforestation.

Present policy was approved by the Diet in May 2016.

Revised plan is made by May 2021, aiming approval of

the Diet in June after collecting public comments. The

plan is base to acquire necessary budget. Use of domestic

timber in 2025 of 40,000,000 cbms set by present plan is

unchanged then in 2030, the volume further increase by

2,000,000 cbms.

By use, 19,000,000 cbms for lumber, 6,000,000 cbms

increase. Judge in from the fact that the increase in five

years during 2014 to 2019 was only 1,000,000 cbms, this

target seems unrealistic. Total wood demand of

79,000,000 cbms in 2025 by the plan is surpassed actual

demand already so target in 2025 increased to 87,000,000

cbms. Increased demand is mainly fuel, which majority is

imported materials.

Therefore, percentage of domestic wood in total demand

would be 46% in 2025 and 48.3% in 2030. Present plan

estimates the percentage in 2025 is 50.6%.

For target of 2030, domestic wood supply is 42,000,000

cbms. Thinning is 450,000 hectares, 80,000 hectares more

than 2018. Reforestation is 70,000 hectares, 40,000

hectares more. Estimated number of workers engaged in

forestry in 2020 are 43,000.

Assuming the same number of workers is maintained in

2030, increased work load can be digested by improved

efficiency but it is doubtful that the same number of

workers can do reforestation and underbrush cleaning,

which areas are doubled from present base.

Actually, it is estimated that number of forest workers in

2030 would drop down to 38,000 so it is necessary to train

workers, who can do both harvest and reforestation.

Heating up of domestic lumber market

In Tokyo market, lumber market prices are abnormally

soaring. Supply shortage of everything of imported and

domestic wood products stimulate both actual demand and

speculative demand and large demand pushes the prices up

rapidly.

Particularly in auction market, where actual lumber is

available at the spot, bidders are swarming for limited

supply and 0n April 7, cedar post prices surpassed cypress

post at 80,000 yen, which is absolutely insane and

sawmills are asking buyers to calm down since this is

unwilling development. High prices do not increase the

supply volume.

In Tokyo market, lumber price increase has started since

last March since imported wood products decrease sharply

and the prices are soaring then things get hotter in April.

KD cedar 3 meter 105 mm post square prices are 65,000

yen and KD cypress 105 mm sill lumber prices are 75,000

yen. They are about 7,000-10,000 yen higher than March

and higher prices pop up in auction markets.

In auction market on April 7, auction started with 60,000

yen on 3 meter 105 mm KD cedar post square then

bidding shot up to 80,000 yen in short time. Successful

bidderˇŻs price of 3 meter KD cypress 105post square is

68,000 yen and 76,000 yen on 4 meter cypress 105 mm sill

square. Prices on others like green lumber are also

climbing largely.

In March, main purchase was speculative since everybody

thought purchase now before the prices go sky-high but

now purchasers actually need lumber now. Sellers are out

of control.

Meantime, precutting plants set the prices quarterly basis

for house builders so present prices on KD cedar post are

50,000-55,000 yen and cypress KD sill square are 60,000-

65,000 yen. It is certain that the prices jump up in next

round.

Log prices are also bullish and further increase is certain

toward rainy season.

Sudden increase of orders of plywood

There are increasing orders on domestic softwood

plywood in recent weeks despite demand slow season.

The manufacturersˇŻ plywood inventory has been very low

and in late March one plywood mill suffered fire damage

so that the production dropped.

From beginning of the year, demand for cedar logs has

kept growing due to short supply of imported wood

products so that cedar log prices climbed steeply.

Many plywood mills will stop the operation for about

ten

days for maintenance of the mill when there are series of

holidays in early May.

Plywood manufacturers proposed higher price of 950 yen

per sheet delivered on 12 mm 3x6 panel since April 1

because of high cost of cedar logs and tight inventory.

Precutting plants were inattentive to plywood supply in the

first quarter since precutting orders were slow despite

sharp drop of supply of North American and European

wood products in January and February. Plywood

manufacturers have been taking production curtailment

program to avoid excess supply so the inventory at the end

of February was 103,000 cbms, only 0.4 month of normal

monthly shipment.

Demand for domestic logs climbed to replace short

supplied imported wood products so the demand increased

all over Japan and log prices increased by 20%

everywhere. In particular, log prices are very firm in the

Western Japan, where stock of cedar is relatively low so

every users scramble cedar logs. On March 20, one

plywood mill in the Eastern Japan had fire accident and

the production will be less in April.

Now precutting plants started worrying about possible

supply shortage of plywood like imported products so they

are hurriedly procure plywood before thing get critical as

demand busy season is approaching.

South Sea (tropical) logs

South Sea log market in Japan is quiet. After major user of

South Sea logs stopped the operation, log demand sharply

declined and other log users are switching to use veneer

instead or other planted species. Lumber demand of South

Sea species is also stagnating as demand like truck body is

not active.

Chinese made laminated free board prices are climbing as

prices of raw materials like Russian red pine and New

Zealand radiate pine are climbing. Indonesian mercusii

pine free board prices are also climbing but the demand in

Japan is inactive so once purchase activities slow down,

upward move by the suppliers may simmer down.

There is some demand for natural wood decking of South

Sea species but the volume is very small.

Price increase of decorative plywood

Base board of decorative plywood is South Sea hardwood

thin plywood mainly from Indonesia. The supply of

Indonesian plywood has been declining and the prices are

soaring. There is no possibility of recovering and the

supply shortage may become critical in June.

Daishin Plywood in Niigata stopped the operation and one

of Indonesian plywood plants lost JAS qualification.

These two make supply situation much worse.

By prolonging supply tightness and continuous climb of

prices of thin plywood, base board is switched to MDF

and particleboard but 40% of decorative plywood base is

thin plywood from Indonesia yet. There are other base

board like domestic softwood and planted species but

there is strong demand of South Sea plywood for moisture

resistance.

However, shortage of South Sea plywood is critical now a

days. Price of South Sea plywood base product is almost

double of MDF base product. 70% of the cost of

decorative plywood is base board. 2.5 mm 3x6 plywood

prices are 25% higher than April last year and it would be

nearly 40% by May.

Marutama Plywood in Hokkaido raised sales prices of

decorative plywood by more than 10% since April 21.

Sumitomo Forestry Crest Co., Ltd. (Nagoya) raised the

prices by 10-20% since March. Kutok Corporation

(Osaka) will increase the prices by 15-20% since May 21.

Marufuji Kenzai (Saitama Prefecture) consider higher

prices since May.

Loss of Daishin Plywood is big blow for the

manufacturers as Daishin used to produce small volume of

special size products. There is no other plywood mills

doing such custom order manufacturing. Switching to

MDF base board will progress more but MDFˇŻs cost is

also getting higher due to higher import wood chip and

adhesive.

Tie-up for utilisation of domestic wood

Three house builders tie-up and formed Japan Wood

Housing Association to promote using domestic wood.

Sanei Architecture Planning Co., Ltd (Tokyo), Open

House Co., Ltd. (Tokyo) and KI-star real estate co., Ltd.

(Saitama prefecture) are collaborating to change building

materials from imported materials to domestic wood.

Three companies are builders of unit built for sale.

Purpose of the Association is supply of high quality house,

preservation of forest by using domestic wood and build

system to supply domestic wood products stably in

volume and price.

Sanei will build about 2,000 units in 2021 and switch all

the building materials to domestic wood products since

May. Post is cedar laminated, beam is larch laminated, sill

is KD cypress, stud and brace are KD cedar and taruki is

cedar LVL. KI builds about 4,000 units built for sale and

percentage of domestic wood is about 70%. Since April, it

plans to build 100-200 flat ordered units with 100%

domestic materials.

Open House supplies mainly three stories units, which is

difficult to use all domestic wood in terms of strength so it

will change to two stories units. It builds about 9,000 units

a year and 20-30% will be two stories unit.

Handling of domestic wood differs by the company so

each will try to change to domestic wood in possible parts.

The groupˇŻs annual wood consumption is about 33,000

cbms and it is considering to plant trees in the North East

Japan to establish cycle of planting, nursing, harvesting

and use of planted wood.

|