|

Report from

Europe

Wood losing out to other materials in joinery sector

The performance of the EU27 wood joinery sector in 2020

was better than expected considering the huge economic

dislocation caused by the COVID-19 pandemic.

The pandemic tended to reinforce existing long term

trends in this sector including: a continuous increase in

joinery production in Germany offsetting a large decline in

Italy; wood's loss of share to other materials ¨C particularly

plastics - in windows and doors manufacturing; and an

increasing focus on other European countries in imports of

joinery products, particularly at the expense of tropical

countries.

These are the main conclusions to be drawn from analysis

of newly released Eurostat PRODCOM data which

provides a snapshot of the production and consumption

value of wood joinery products in the EU27 in 2020.

Rebound in construction lifts joinery sector

Eurostat data shows that the value of construction activity

in the EU27 fell by 4.9% in 2020. This was a much less

dramatic fall than forecast early in the pandemic as

activity rebounded rapidly in the third quarter of the year

after the sharp fall in the first lockdown in April/May

2020.

There was a bigger decline in construction activity in 2020

in those EU27 countries most affected by the pandemic

and where lockdowns conditions were particularly longlasting

and restrictive, including France (-15%), Spain (-

12.5%), Belgium (-8.2%), and Italy (-8.1%).

Construction activity was more resilient in Germany

(+2.9%), Denmark (+2.5%), Finland (0%), the

Netherlands (-0.3%), and Sweden (-0.8%).

Overall activity in the EU27 wood joinery sector was more

stable in 2020 than activity in the wider construction

sector. Eurostat data shows that the production value of

wood joinery and related products in the EU27 decreased

only 0.1% to €30.41 billion in 2020 following a slightly

larger decline of 1.5% in 2019.

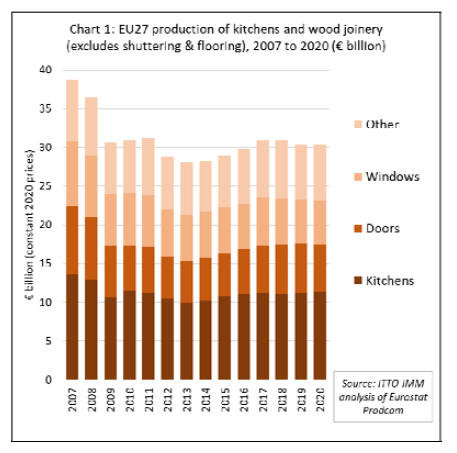

Total wood joinery activity across the EU27 was at

significantly higher level in 2020 than between 2012 and

2016 at the time of the European Debt Crises (Chart 1).

However, the overall figure hides significant variations

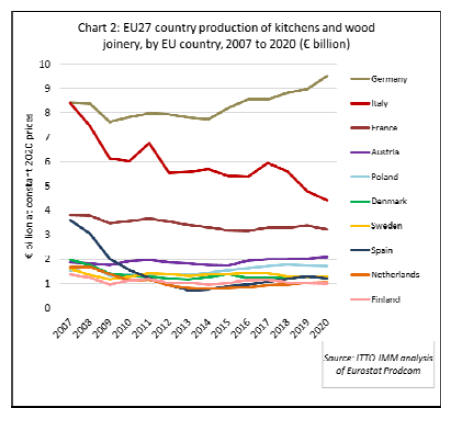

between EU27 countries (Chart 2). The most obvious

trend in recent years ¨C which accelerated in 2020 ¨C is the

persistent growth of joinery activity in Germany offset by

a large decline in activity in Italy. Although Italy was still

the second largest joinery manufacturing country in the

EU in 2020, the value of Italian production was less than

half that of Germany last year.

The value of joinery activity in Germany increased 6.0%

to €9.51 billion in 2020, a significant increase in the pace

of growth compared to only 1.6% the year before. In

contrast, production activity in Italy fell 7.8% to €4.41

billion in 2020 following a decline of nearly 15% in 2019.

Italy was more severely affected by COVID-19 than

Germany in 2020, but the contrast in performance with

Germany is also a reflection of a longer-term decline in

Italy's relative competitiveness in wood product

manufacturing.

Trends in wood joinery production in other EU27

countries have been much less dramatic. Joinery

production in France fell 4.9% in 2020, to €3.22 billion,

after rising 2.6% the previous year. Production in Austria

increased 3.6% to €2.09 billion in 2020, continuing a

gradual but consistent and long-term rise.

Joinery production in Poland has slipped a little after

rising strongly between 2013 and 2018, falling 1% to

€1.73 billion in 2020. This followed a 2% decline the

previous year.

Joinery production in Denmark (+0.8%), Sweden (+4.7%),

and the Netherlands (+1.9%) was resilient in 2020 in line

with less stringent lockdowns and good activity in the

wider construction sector in those countries.

Joinery production in Spain fell 6.4% to €1.21 billion in

2020 after making a large 9% gain the previous year. In

2018 and 2019, Spain's construction sector was at last

recovering after a very long period of stagnation since the

2008-2009 financial crises.

But in 2020 Spain was hit heavily by the pandemic,

experiencing large numbers of COVID cases, lengthy

lockdowns and massive losses in the tourist trade.

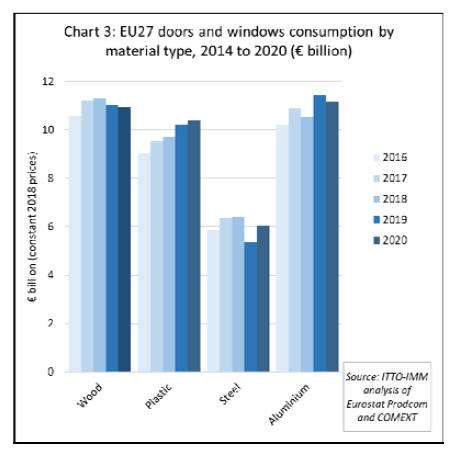

Part of the explanation for slow growth in wood joinery

activity in the EU27 in recent years is increased

substitution by alternative materials.

Eurostat PRODCOM data provides comparable data on

the total value of doors and windows manufactured in the

EU27 in wood, plastic, steel and aluminium respectively.

It shows that while manufacturing of wooden doors and

windows declined in 2019 and 2020, the value of plastic

door and window production has been increasing.

The value of manufacturing of steel doors and windows

declined sharply in 2019 but rebounded in 2020. The

manufacturing of aluminium doors and windows followed

the opposite trend, rising in 2019 but falling in 2020

(Chart 3).

Overall the share of wood in the total value of EU27 door

and window production fell from 30% in 2018 to 28% in

2020. Over the same period, the share of plastic increased

from 26% to 27%, aluminium increased from 28% to 29%,

while steel decreased from 17% to 16%.

There are a wide range of factors behind these shifts in

materials usage in the windows and doors sector, but

material supply and pricing have probably become more

prominent during the pandemic.

There have been widespread reports of extreme shortages

in the supply of timber, steel and aluminium, all of which

have experienced sharp price increases in the EU27 since

the start of the pandemic.

While plastic products were already taking market share ¨C

benefiting from their relatively lower cost ¨C manufacturers

of plastic products less affected by these shortages have

been well placed to take advantage of a surge in demand

for home improvement during the pandemic.

Longer-term, the growth in aluminium consumption in the

EU27 windows and doors sector has been significant.

Aluminium has always remained the default windows

product in the commercial market but has enjoyed

considerable resurgence within the residential window and

door market.

An important driver behind this has been aluminium bifold

and sliding doors as consumers demand greater space

and light within living areas. Another factor is the demand

for lower maintenance and greater strength in light weight

frames for high energy efficiency double and triple glazed

units.

A limitation of the PRODCOM data is that it does not

distinguish products made wholly in wood or metals from

those that are composites of both materials. The

development of wood-aluminium composite window

frames has been a key growth area in the EU27 in recent

years. These products combine the strength and efficiency

of aluminium with the thermal insulation and aesthetic

properties of wood.

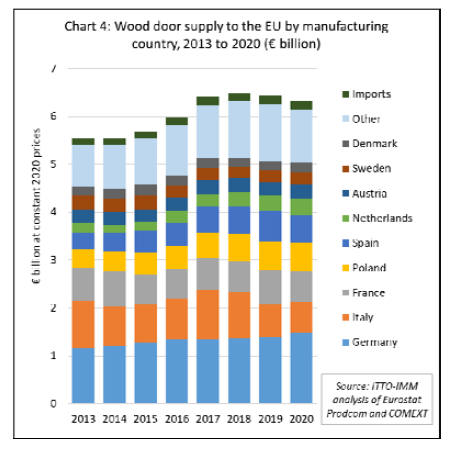

Germany, the largest wooden door manufacturer

Eurostat PRODCOM data shows that the total value of

wooden doors supplied to the EU27 decreased 2% to

€6.31 billion in 2020 following a 1% decline the previous

year. Most new wooden door installations in the EU27

comprise domestically manufactured products.

The EU27ˇŻs domestic production also declined by 2% in

2020, to €6.13 billion (Chart 4).

There was significant variation in the performance of the

wooden door sector in EU27 countries in 2020. Production

in Germany, now by far the largest wooden door

manufacturing country, increased 5% to €1.47 billion

during the year, continuing an uninterrupted rise since

2009.

Wooden door production in Italy fell 4% to €660 million

in 2020, a relatively minor decline compared to the 27%

decrease the previous year. Production in France fell 8%

to €650 million in 2020 after a 9% rise in 2019.

Production in Spain was down 10% to €580 million in

2020 after a 9% gain in 2019.

Elsewhere there was robust wooden door production

during 2020, with a rise of 5% to €330 million in the

Netherlands, 4% to €250 million in Sweden, and 9% to

€200 million in Denmark. Production was stable in Poland

and Austria during 2020, at €590 million and €300 million

respectively (Chart 5).

Wooden door imports into the EU27 decreased by 4% to

€184 million in 2020 (Chart 6). Imports accounted for

2.9% of the total euro value of wooden door supply to the

EU27 in 2020, slightly less than 3.0% the previous year.

Due to rising freight rates and other supply issues, a

smaller share of EU27 wooden door imports were sourced

from tropical countries during 2020. Total EU27 imports

from the tropics were €40.2 million in 2020, 11% less than

in 2019. This contrasts with a decline of only 2% from

temperate countries to €143.8 million in 2020.

In 2020, wooden door imports were down 8% to €31.6

million from Indonesia, down 8% to €3.5 million from

Brazil, down 31% to €2.5 million from Malaysia, and

down 31% to €1.6 million from Vietnam. EU27 imports of

wooden doors from China, still the largest single external

supplier, fell 14% to €49.9 million in 2020. In contrast,

imports from Ukraine increased 22% to €16 million in

2020 building on a 23% increase the previous year.

Wooden door imports from the UK, now an external

supplier to the EU27, fell 16% to €13.8 million in 2020,

partly owing to pandemic related supply problems and

partly to changing distribution networks after the UK's

departure from the EU at the start of 2020.

An even more pronounced decrease in EU27 door imports

from the UK is expected in 2021 as the UK only left the

EU single market on 1st January this year following a 12

month transition period.

The European wooden door industry is now dominated by

products manufactured using engineered timber driven by

requirements to comply with higher energy efficiency

standards and efforts to provide customers with more

stable products and long-life time guarantees.

Another key trend is towards composite doors with a steelreinforced

uPVC outer frame with an inner frame

combining hardwood and other insulation material. These

products are designed to combine strength, security,

durability, high energy efficiency, with a strong aesthetic.

There may be a place for tropical hardwoods in the design

of these products with manufacturers looking to combine

high quality, consistent performance, regular availability,

and good environmental credentials with a competitive

price.

EU market for wooden windows

The total value of wooden windows supplied to the EU27

fell 1% to €5.76 billion in 2020 following a 4% decline the

previous year (Chart 7).

The supply of wooden windows to the EU27 is

overwhelmingly dominated (over 99%) by domestic

production which fell 0.6% to €5.72 billion in 2020. Italy

just maintained by the slimmest of margins its position as

the largest wooden window manufacturer in the EU in

2020, despite production slumping 25% to €950 million.

Wooden window production also declined in Poland (-2%

to €680 million) and France (-4% to €480 million) during

the year.

Production in Germany increased 8% to €940 billion in

2020 after a 0.5% rise the previous year. In 2020

production also increased in Austria (+2% to €470

million), Denmark (+5% to €430 million), Sweden (+2%

to €420 million), and the Netherlands (+1% to €270

million) (Chart 8).

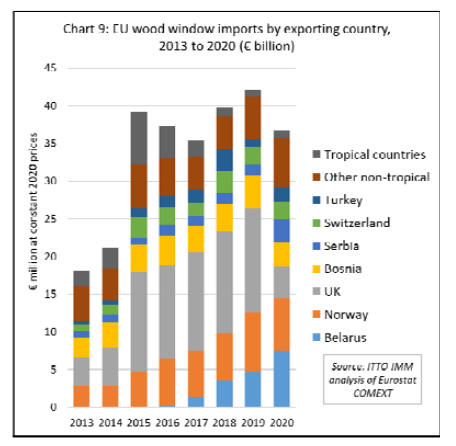

EU imports of wooden windows from outside the EU

decreased by 13% in 2020 to €36.7 million (Chart 9).

Imports from Belarus, now the largest external supplier,

increased 61% to €7.5 million in 2020, continuing a rising

trend that started in 2017. However imports fell from

Norway (-10% to €7.1 million), the UK (-71% to €4

million) and Bosnia (-24% to €3.3 million).

Only a tiny quantity of wooden windows is imported into

the EU from tropical countries. After a spike in imports of

€7 million in 2015, mainly from the Philippines, imports

from tropical countries fell to less than €1 million in 2019

and were still around that level in 2020.

While tropical countries are not significantly engaged in

the EU market for finished windows, this sector is of

interest as a source of demand for tropical wood material.

From this perspective, a notable trend in the EU window

sector ¨C as in the door sector - is towards use of

engineered wood in place of solid timber. This is

particularly true of larger manufacturers producing fullyfactory

finished units that buy engineered timber by the

container load.

Increased use of engineered wood is closely associated

with efforts by window manufacturers to meet rising

technical and environmental standards, provide customers

with long lifetime performance guarantees and recover

market share from other materials.

Increased focus on energy efficiency means that tripleglazed

insulating window units with very low U-factors

are now more common than double-glazed units in

Europe. These units demand thicker, more stable and

durable profiles that in practice can only be delivered at

scale using engineered wood products or by combining

wood with aluminium and steel in composite products.

The quality and engineering of wooden windows has

undergone a revolution in the EU in recent years so that

manufacturers are now able to deliver products with many

of the benefits previously reserved only for the best quality

tropical hardwood frames using softwoods and temperate

hardwoods.

Factory-finished timber windows are given a specialist

spray-coated paint finish for even and durable coverage

which might only need redoing once a decade. The

lifespan of factory-finished engineered softwood frames is

now claimed to be about 60 years, while thermally or

chemically modified temperate woods can achieve around

80 years.

Nevertheless, smaller independent joiners producing

bespoke products in low volumes still tend to rely on solid

timber purchased from importers and merchants to

manufacture window frames. Tropical woods such as

meranti, sapele and iroko continue to supply a high-end

niche in this market sector.

The opportunities for wood suppliers in the EU27

windows sector are significant ¨C the total value of wooden

windows sold in the EU27 in 2020 was €5.24 billion, a 1%

gain compared to €5.19 billion the previous year.

The downside is that this is a highly competitive market

that has yet to achieve any significant growth despite all

the promise offered by wood's excellent thermal insulation

and other environmental credentials compared to other

materials and the recent strong emphasis on improved

product performance and efficiency.

When adjusted for inflation, the value of EU27 wooden

window consumption in 2019 was at the lowest level

recorded for at least the last twenty years ¨C and the

increase in consumption in 2020 was only marginal.

Perhaps more than ever before, there is now an

opportunity to turn the tide. There is a very strong focus

in the COVID-19 recovery plans on long-term economic

and social ˇ°resilienceˇ±. NextGenerationEU, the €750

billion ($888 billion) economic recovery instrument now

being rolled out across the EU in response to the

pandemic, is explicitly linked to the EU Green Deal, a

radical project to cut EU emissions by 55% compared to

1990 levels by 2030 on the way to making the EU climate

neutral by 2050.

37% of NextGenerationEU finance is earmarked for

achievement of European Green Deal objectives with

activities to include a large program of building renovation

and support for the ˇ°circular economyˇ± and sustainable

investment. There is a rising expectation that demands for

formal Environmental Product Declarations (EPDs) and

so-called Product Environmental Footprints (PEFs), will

become much more widespread, particularly in the

construction sector as more building projects are subject to

mandatory environmental assessment.

The projected costs of these Green Deal measures are

enormous, requiring an additional €82 billion to €147

billion in spending every year until 2030, about half a

percentage point of the EUˇŻs GDP. Beyond 2030, the

additional investments are 1% to 2% of GDP, about €4.6

trillion between 2031 and 2050.

If wooden products, with all their carbon benefits and

natural and sustainability credentials cannot thrive in this

market environment and begin to retake share from fossil

fuel intensive materials like plastics, aluminium and steel,

then they never will.

|