The positive trend in the construction industry continues. The demand for all sawn timber ranges currently exceeds the supply, delivery delays are the result.

Most of the sawmill industry locations in Austria have a

below-average stock of needle saw logs. Market signals that are set

too late and weather conditions that are unfavorable for the timber

harvest are currently reducing the supply. Nationwide, there is very

brisk demand with slow normalization of logging. Provided that thaw

barriers or precipitation do not prevent the transport, the wood

provided is quickly transported away and taken over. There are

hardly any forest camps.

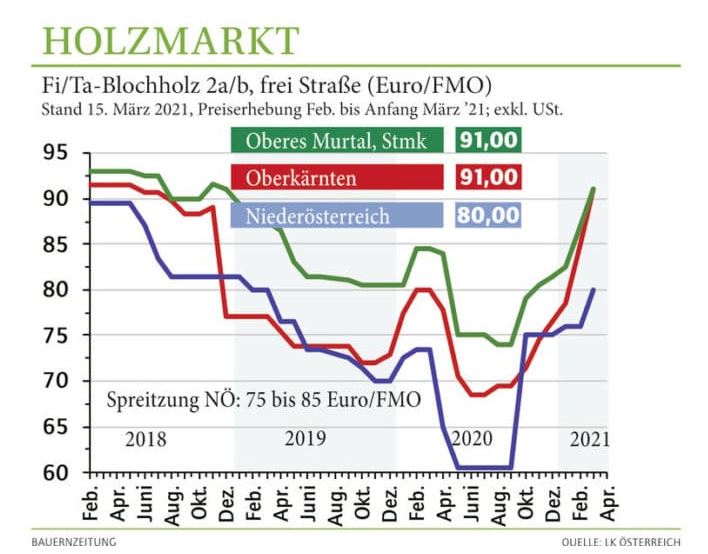

90 euro mark exceeded

In the southern federal states in particular, the price of wood for

the leading range of spruce, A / C, 2b has exceeded the 90 euro

mark. In some cases, delivery bonuses are also granted. Although the

prices have caught up a little even with the poorer qualities, the

difference to the main range is greater than usual. This makes it

all the more important to control the quality assessment at the

sawmill. It seems that prices in the damaging regions of Waldviertel

and Mühlviertel are deliberately kept low. In the wake of the

spruce, the sales opportunities for pine have also improved

significantly. The prices have been raised and are at the level of

previous years. Larch continues to maintain its price level, and

demand remains high.

The hardwood season is drawing to a close due to the weather. Oak

remains very much in demand. The sales opportunities for the beech

are unexcited.

The marketing of coniferous industrial logs has continued to relax

in terms of volume. This is primarily due to the somewhat lower

supply of saw by-products, due to the reduced cutting. Even

quantities that have already been stored for a long time are usually

transported away quickly and taken over quickly. The prices remain

stable. Red beech fiber wood is in normal demand again after the

reduced takeover in recent weeks.

Energy wood market remains

tense

The energy wood market remains tense due to reduced consumption.

With the exception of individual larger customers in Carinthia,

quantities outside of existing contracts are not to be marketed. The

prices are stable. There is still good demand for quality firewood.

The weather data show that the previous weather pattern in 2021 is

again too dry and too warm compared to the long-term average. The

forest protection situation will therefore remain tense.

All prices quoted relate to business transactions in the period

February - beginning of March 2021 and are net prices to which sales

tax is to be added. The following tax rates apply to the sale of

wood to entrepreneurs: with sales tax flat rate for all assortments

13%, with regular taxation for energy wood / firewood 13% and for

round wood 20%.

Source: LK Austria, market report as of March 15, 2021