|

1.

CENTRAL AND WEST AFRICA

End of rains in Cameroon, harvesting back on

schedule

Cameroon has, at last, started to welcome the beginning of

the dry season so harvesting conditions have improved.

Despite the rise in covid infections mills report no problem

with the work force and that production is back to normal

after the dismal situation during the extended rains. The

availability of containers for exports is still an issue and is

disrupting shipments and leading to a build in stocks of

sawnwood.

Large number of concession agreements withdrawn in

Gabon

The timber industry in Gabon is trying to assess the impact

of an announcement from the government on 17 January

withdrawing of a large number of concession agreements.

Companies affected reportedly have concession

agreements arranged many years ago and do not have the

appropriate documentation. This is likely to cause

considerable problems for the companies concerned.

Concession holders had just 8 days from 17 January to

respond.

As with Cameroon, the availability of containers is

hindering shipments from Gabon which producers say is

unfortunate as demand is firm in international markets.

According to the daily newspaper l'Union the governor of

Moyen-Ogooué Province, Barnabé Mbagalivoua, called a

crisis meeting with government labour officers and

workers' unions to decide action against a forestry

company which reportedly unfairly dismissed workers,

employed workers without a formal contract and also

failed to pay employee contributions to the National Social

Security Fund (CNSS).

See:

https://www.lenouveaugabon.com/fr/securite-justice/1701-17944-lambarene-des-exploitants-forestiers-chinois-interpellespour-violation-des-droits-des-employes

Rumours that felling tax to be raised in Congo

Opposition to the proposed log export quota in Congo set

to be introduced by the end of this year is growing with

exporters saying the 75%/25% quota needs to be

reconsidered.

Producers have indicated that there is a steady demand for

okoume especially and that buyers continue to show

interest in the redwoods such as sapelli and sipo. News is

circulating indicating changes in top management of the

forest authority have been made and that the change has

not impacted dealings between concessionaires and mills

and the government. In related news, it has been learnt that

the felling tax will be increased possibly in June this year.

Congo Basin certification system achieves PEFC

endorsement

The PEFC website has announced the Pan African Forest

Certification (PAFC) Congo Basin regional system has

achieved PEFC endorsement marking the first PEFC

regional forest certification system to be recognised.

PEFC says “members in Cameroon, Congo and Gabon

joined forces under the name of PAFC Congo Basin to

develop this regional certification system. The shared

language and the similar forestry conditions in the three

neighbouring countries enables them to share one system.

See:

https://pefc.org/news/pafc-congo-basin-regionalcertification-system-achieves-pefc-endorsement

ATIBT launches carbon commission

A wide range of stakeholders including producers, donors,

professional associations, certification bodies and various

experts recently met to discuss advancing an

understanding of carbon trading and carbon markets. One

of the main observations from the group was that forest

operators lack information on carbon financing and

dialogue with carbon market actors.

There were questions raised on the potential for carbon

storage through SFM in West African forests which it was

felt was not sufficient to be profitable at current prices.

The group identified objectives which were included in an

initial roadmap to address the overall objective.

See:

https://www.atibt.org/en/news/13114/launch-of-the-atibtcarbon-commission-making-the-link-between-forest-operatorsand-carbon-market-actors

Wood decking market study

Le Commerce du Bois has published the results of

a study conducted by Jean-Marc Mornas on prospects for

wood decking in France: ‘2017-2022 evolution, 2021

estimate and 2025 prospects’.

See:

https://www.lecommercedubois.org/files/upload/actualites/Marches/CP_Etude_Mornas_-_Marche_terrasse_bois_et_derives_2017_a_2021____VF_LCB.pdf

2.

GHANA

Wood product export markets

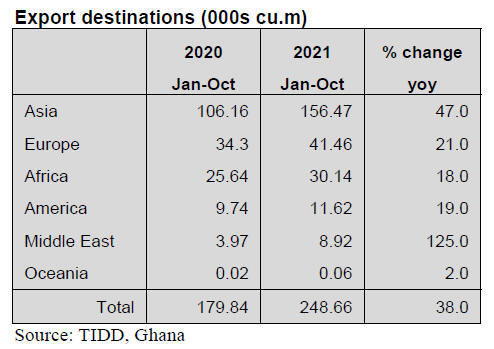

According to data from the Timber Industry Development

Division (TIDD), a total of 248,658 cu.m of wood

products were exported during the first 10-months of

2021. This compares to 179,835 cu.m recorded for the

same period in 2020 and was a 38% year on year growth.

The table below shows the market performance for 2021

compared to 2020.

Of the 248,658 cu.m shipments to Asia (63%), Europe

(17%) and Africa (12%) accounted for 92% of the total

export volume for the period with three other geographic

zones accounting for the balance.

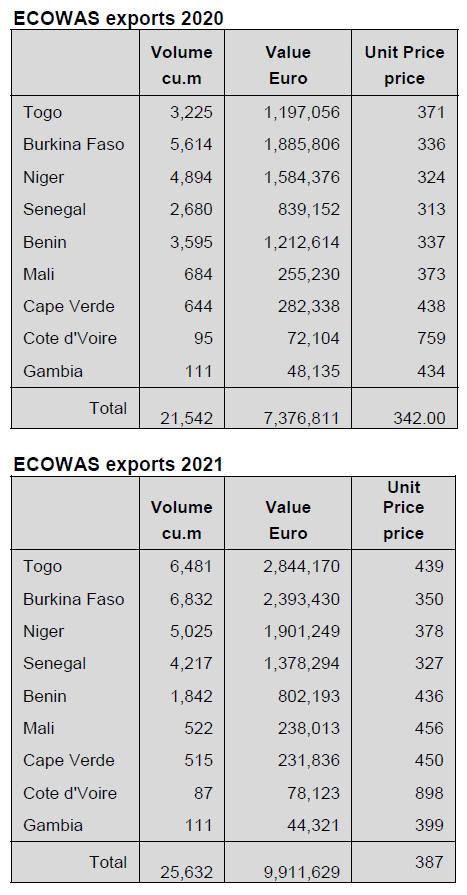

Total shipments to the ECOWAS sub-region increased to

25,632 cu.m in 2021 from 21,541 cu.m in 2020, a growth

of 19% . The table below shows the ECOWAS market

destinations with their corresponding volume, value and

unit price.

Burkina Faso, Togo, Niger and Senegal were the leading

importers of Ghana’s wood products and recorded

significant volume growth in 2021 compared to 2020.

These countries together accounted for the 88% of the

total 25,632 cu.m shipped to ECOWAS member countries

in 2021.

The average unit price for ECOWAS member countries

trading with Ghana improved in 2021 compared to 2020,

except Gambia. The average price increased from

Euro342/cu,m in 2020 to Euro387/cu.m in 2021.

West African countries have for several years been the

major markets for Ghana’s plywood with Togo, Niger and

Burkina Faso topping the list. Currently, about 80% of

Ghana’s plywood exports are shipped to West African

markets.

Land use map to identify forest cover

The Forestry Commission, in partnership with local and

international agencies, has developed a land use map

which delivers a detailed view of the country’s forest

cover. Based on the latest map it has been established that

Ghana has a total of 6.5 million hectares of both open and

closed forests.

The land use map which, a project of the Resource

Management Support Center (RMSC) of the Forestry

Commission, received support of the UK space agency,

Ecometrica, the technical wing of the Forestry

Commission (Resource Support Center), Faculty of

Renewable Natural Resources of the Kwame University of

Science and Technology (KNUST) and the Forest

Research Institute of Ghana (FORIG).

See:

https://ghana-nationallanduse.knust.ourecosystem.com/interface/

Two online applications for forestry sector

The Forestry Commission has launched two online

applications; the Digitalised Property Mark Registration

and Renewal (e-property mark registration) and the

Electronic Wood Tracking System.

When launching the applications the Minister for Lands

and Natural Resources, Samuel A. Jinapor, said it is the

President’s vision to promote socio-economic

development through digitisation and the Forestry

Commission is playing its part.

The E- Property Mark Registration App. allows applicants

to register, renew and extend contracts online while the

electronic Wood Tracking System platform is designed to

track wood from the point of harvest to the point of sale in

order to ensure transparency and to be able to verify the

origin of wood products.

See:

https://fcghana.org/news_summary.php/

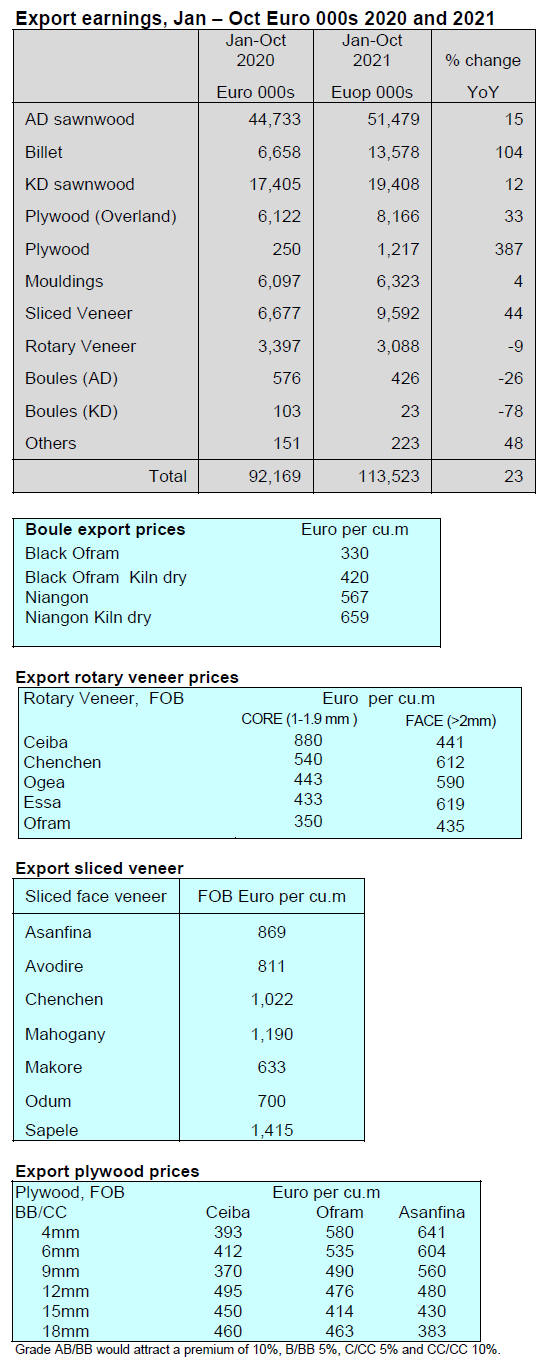

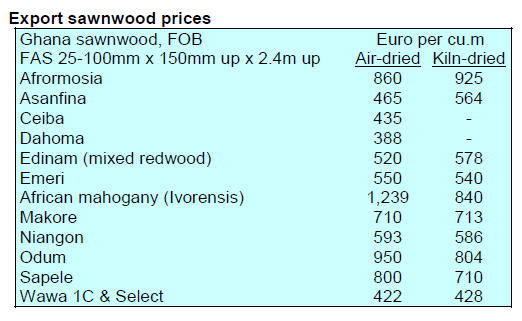

Correction, In addition to a duplication of tables our

correspondent has found some errors in the export

statistics he provided. Revised export volume and value

tables are provided below.

3. MALAYSIA

Reduce dependence on natural forest resources

says

minister

Malaysia recorded a slight increase in earnings from

timber exports between January and October 2021

compared to 2020. Among the products that contributed

most were wooden furniture, sawnwood, plywood and

mouldings.

The Ministry of Plantation Industries and Commodities

(MPIC) aims to achieve RM24 bil. from timber exports in

2022 as the industries take advantage of the latest

advanced technologies, introduce new products and solve

the problem of finding skilled workers.

MPIC Deputy Minister, Willie Mongin, called on the

industry to be imaginative in coming up with alternative

raw material thus reducing dependence on tropical timber

and rubberwood. He also stressed the importance of

providing good accommodation for workers in order to

meet the Workers' Minimum Standards of Housing and

Amenities Act 1990 (Act 446).

See:https://www.nst.com.my/news/nation/2022/01/763184/malaysiagained-rm179-billion-timber-exports-2021?topicID=1&articleID=763184

Regional Comprehensive Economic Partnership

(RCEP)

The timber industry is looking at RCEP as a new driver of

Malaysian domestic and international business activities in

the post-pandemic period. Malaysia is likely to be the 12th

RCEP signatory as the Instrument of Ratification was

submitted to the ASEAN Secretariat on 17 January. RCEP

will enter into force for Malaysia on18 March 2022 as

Malaysia joins 11 other signatories Singapore, China,

Japan, Brunei, Cambodia, Laos, Thailand, Vietnam,

Australia, New Zealand and South Korea.

|