Japan

Wood Products Prices

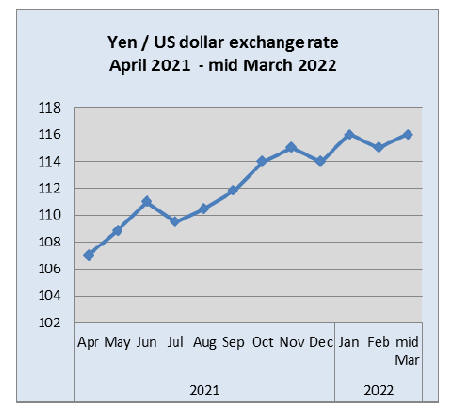

Dollar Exchange Rates of 10th

Mar

2022

Japan Yen 116.0

Reports From Japan

Contingency plans for

disruption of supply chains

Following RussiaˇŻs invasion of Ukraine Japan has moved

to impose sanctions together with the United States,

European Union members and other nations. Trade

statistics from JapanˇŻs Ministry of Finance show that in

calendar year 2021 the value of imports from Russia rose

35% from 2020 to yen1.5 trillion. This represents close to

2% of JapanˇŻs total imports. Imports from Russia were

mainly energy resourcesˇŞincluding liquefied natural gas,

coal, oil and nonferrous metals.

See:

https://www.nippon.com/en/japan-data/h01266/

Japan is identifying critical imports from Russia so as to

make contingency plans for potential disruptions to supply

chains as Russia has banned some exports in retaliation

against economic sanctions. In retailiation Russia has

named countries to which exports will be halted. Japan is

among the countries indentified and Russsia has

announced timber exports to Japan will be suspended until

31 December 2022.

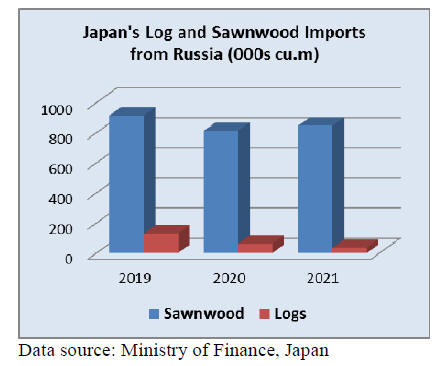

Russia is the largest sawnwood exporter and ranks the

seventh biggest exporter of wood products. Wood product

exports from Russia have increased rapidly in the past five

years led by sawn softwood and paper products.

See:

https://www.woodbusiness.ca/russias-invasion-of-ukrainewill-likely-halt-planned-forest-industry-investments/

Japanese companies in Russia struggle to pay

employees

Japanese companies are assessing whether their operations

in Russia can be maintained as Japan has joined the

US and EU in blocking international financial transactions

to and from Russia. A concern is that Japanese companies

with operations in Russia may not be able pay employees.

The collapse of the rouble has made sourcing cash

extremely difficult.

According to a government statement 32 Russian and

Belarusian individuals along with 12 entities including

military-related companies were added to the list of those

facing asset freezes in Japan.

See:

https://asia.nikkei.com/Politics/Ukraine-war/Corporate-Japan-gauges-Russia-risk-as-sanctions-deepen

and

https://japantoday.com/category/politics/update1-japan-imposesmore-sanctions-on-russia-belarus-over-ukraine-invasion

also

https://www.mitsui.com/mgssi/en/report/detail/__icsFiles/afieldfile/2016/10/20/160707m_kitade_e.pdf

Business conditions

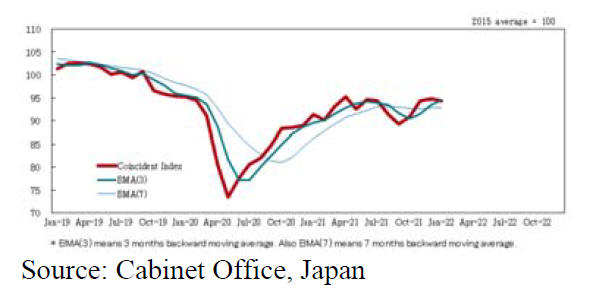

The Japanese economy in January showed a weakening of

prospects for the first time in four months. The January

fall came after a slight rise in December 2021. For the fifth

straight month the Cabinet Office maintained its

assessment that the domestic economy is "weakening".

See:

https://mainichi.jp/english/articles/20220308/p2g/00m/0bu/053000c

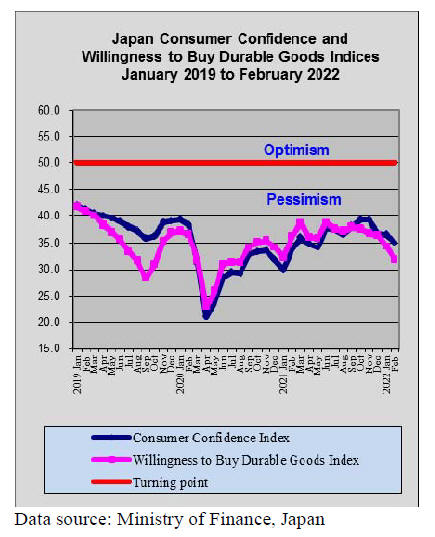

Consumer confidence down once more

Consumer confidence dropped in February for the third

consecutive month due mainly to a rise in Omicron

infections. The index provides an insight into consumer

expectations for the coming six months. An index below

50 indicates that pessimists outnumber optimists.

During the February survey many prefectures were still

under a corona semi-lockdown which limited

opportunities for consumers. The index for willingness to

purchase durable goods fell sharply in February as

consumers put off purchases.

Housing

Municipalities in Japan are providing support to

Ukrainians who have fled to Japan. The Immigration

Services Agency said evacuees have a 90-day residential

visa which can be extended or replaced with a longer-term

residential status that would allow them to work in

Japan. According to the United Nations High

Commissioner for Refugees more than 2 million Ukrainian

refugees had fled the country.

Yokohama City has indicated it is ready to support people

fleeing from Ukraine. Osaka prefectural government said

it is providing Ukrainian evacuees with free

accommodation while also offering employment and

educational support. Mie and Kanagawa Prefectures are

also offering accommodation to those fleeing Ukraine.

In addition to municipalities, Japanese companies are

stepping forward. Pan Pacific International Holdings

Corp., operator of the Don Quijote discount store

chain announced it will offer housing to 100 Ukrainian

families as well as jobs.

See:

https://www.japantimes.co.jp/news/2022/03/09/national/municipalities-companies-ukraine-evacuees-support/

Yen purchasing power drops

The Bank for International Settlements publishes real and

nominal effective exchange rates for major currencies. The

most recent data came as a surprise as it showed that the

yen's effective exchange rate (representing purchasing

power) is now as low as it was in the early 1970s when the

yen was first floated following the collapse of the Bretton

Woods and Smithsonian systems of fixed exchange rates.

See:

https://www.bangkokpost.com/opinion/opinion/2276139/howdid-japan-become-so-cheap-

Import update

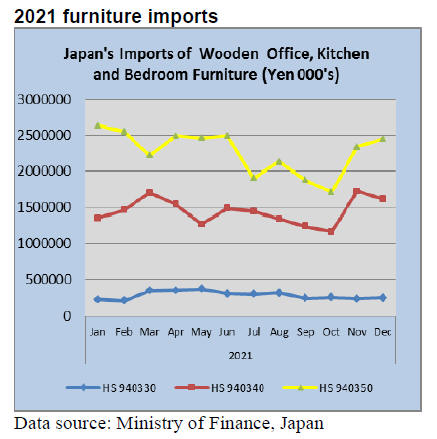

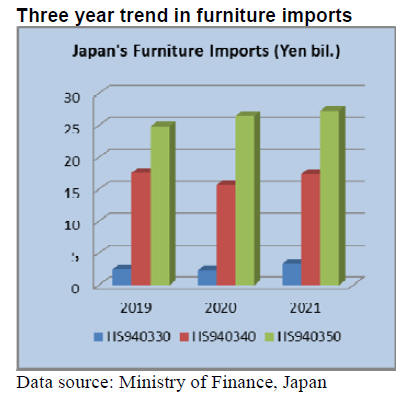

Furniture imports

The value of JapanˇŻs imports of wooden office, kitchen

and bedroom furniture all closed 2021 at a higher level

than in 2020. Remarkably, 2021 imports of wooden

bedroom furniture (HS940350) were higher than in 2019

as well as 2020.

The value of wooden office furniture imports dipped in

2020 but recovered and ended 2021 higher than in 2019.

In contrast, imports of wooden kitchen furniture in 2021

had still not recovered to 2019 levels.

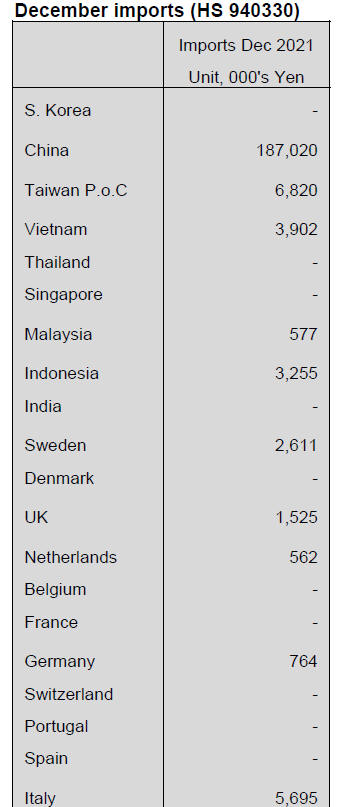

December office furniture imports (HS

940330)

The top shipper of wooden office furniture in December

2021 was China taking a much higher market share at 75%

compared to a month earlier. The other main suppliers in

December last year were the US (8%), Poland (4%) and

Taiwan P.o.C.

Year on year the value of imports of wooden office

furniture (HS940330) rose almost 15% in December 2021

building on the steady upward trend seen over the previous

few months. Month on month the value of wooden office

furniture rose 5%.

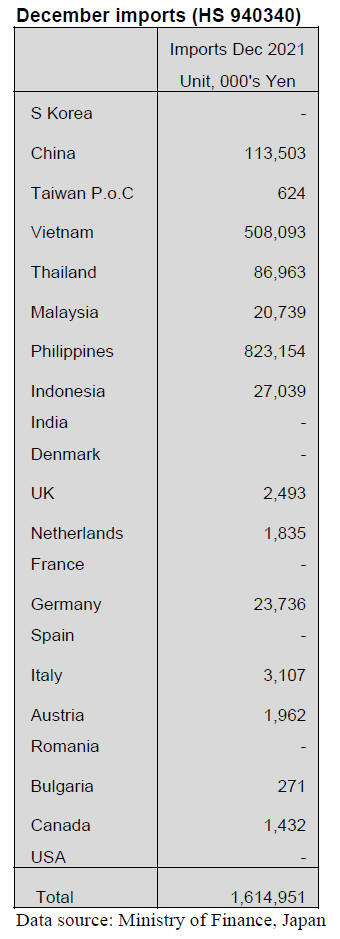

Kitchen furniture imports (HS 940340)

Following a very sharp rise in the value of wooden kitchen

furniture in November 2021 there was a 6% downward

correction in December. However, year on year December

2021 imports were some 13% higher.

Around 90% of JapanˇŻs December 2021imports of wooden

kitchen furniture came from just 3 sources; the Philippines

(51%), Vietnam (31%) and China (7%).

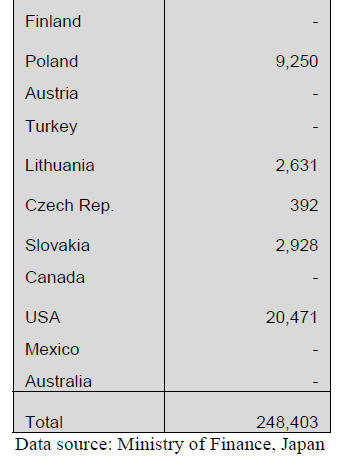

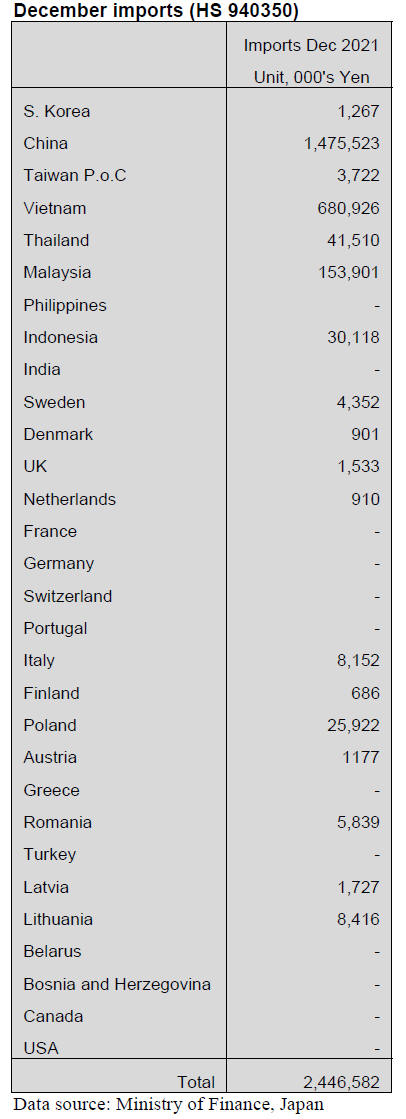

Bedroom furniture imports (HS 940350)

The third quarter of 2021 saw a steady increase in the

value of JapanˇŻs imports of wooden bedroom furniture

reversing the downward trend that began mid-year and

pulling overall imports for the year up above that for 2020

and even above the value of 2019 imports. The top

suppliers in terms of value in December 2021 were China

(60%) and Vietnam (28%). Shipments from both countries

were impacted by logistic problems.

When the value of imports from Malaysia (6%) and

Poland are include with those from the two top shippers

then around 95% of JapanˇŻs wooden bedroom furniture

imports have been accounted for. Year on year, December

2021 imports were 9% higher and month on month

December imports were 4% higher.

Trade news from the Japan Lumber Reports (JLR)

The Japan Lumber Reports (JLR), a subscription trade

journal published every two weeks in English, is

generously allowing the ITTO Tropical Timber Market

Report to reproduce news on the Japanese market

precisely as it appears in the JLR.

For the JLR report please see:

https://jfpj.jp/japan_lumber_reports/

Confusion by the Russian invasion

After Russia invaded Ukraine there are rising concerns as

to trade. One is payment after SWIFT excluded major

Russian banks and another is shipping. At this stage,

nothing is clear yet as to banking system.

Shipping problem is serious. The European authorities

deny transshipping containers for Russian destinations.

Large container ships unload for transshipping at

European ports like Rotterdam and Hamburg onto smaller

vessels for Russia.

There are three major ports in Russia, St. Petersburg on

Baltic Sea, Novorossiysk on Black Sea and Vladivostok in

the Far East. These three ports receive74% of all container

cargoes.

Major container shipping companies have stopped taking

orders for Russia. Also marine insurance for the Russian

ports is now categorised as war zone so that insurance

premium is extremely high so shipping companies are

refusing to call Russian ports.

It is expected there will be confusion in the wood products

trade as this is totally new experience like COVID-19

epidemic so everyone has to keep watching the changes in

the situation. Many wood product manufacturers in

Europe rely on raw materials from Russia and Ukraine. If

payment system stop the supply of wood stops.

Russian logs and lumber import in 2021

The total volume of softwood logs from Russia is about

32,000 cbms, 35.2% less than 2020.The volume of red

pine KD taruki is 505,000 cbms, 7.4% less than last year.

There was not only a decrease of volume but also serious

problems of delays of arriving to Japan in 2021.

There were three kinds of softwood logs such as larch, red

pine and whitewood, which were imported to Japan in

2020 and the volume was under 100,000 cbms. The

volume of these three kinds did not exceed in 2021.

The manufacturers, which convert larch or red pine logs to

lumber, were getting less in Japan. A ban of exporting logs

from Russia in January, 2022 had a big influence.

The exporting logs just before the ban was in

December,

2021 and the volume of larch was around 4,000 cbms. It

was around 5,600 cbms in December, 2020. The volume

of lumber was 600,000 cbms. It is straight two years.

The prices skyrocketed at the beginning of 2021 in Russia.

Red pine KD taruki was US$1,000, CIF per cbm, before

last summer. Red pine genban was US$ 700, CIF per cbm.

The supply did not increase even though the prices were

extremely high. One of reasons is that logs were exported

to China mostly.

A lack of containers caused delays of arriving to Japan.

Another reason is that much demand of wood were in all

over the world. The delays have been continuing. The

products, which were agreed to a contract in last summer,

had just arrived in February, 2022.

Imported lumber inventory at Tokyo

Imported lumber inventory at Tokyo harbor at the end of

January was 7.9% more than December with 178,000

cbms. This is three consecutive months increase.

Bulk ship of North American lumber arrived one in

December and another in January then delayed shipments

of European lumber and Russian lumber arrived one after

another.

The inventory at the end of January last year was only

71,000 cbms so now itˇŻs 2.5 times more. The arrivals

increased in December and January so the inventory

jumped up from the bottom of last NovemberˇŻs 131,000

cbms.

By source, North America is 54,000 cbms, 2.57 times

more than a year ago. Europe is 54,000 cbms, 3.6 times

more. Russia is 33,000 cbms, 2.2 times more. China and

others are 31,000 cbms, 1.9 times more. Increase of

European lumber is conspicuous. However, compared to

two years ago, North America increased by 45.9% but

European is only 5.9% more and Russian is 3.1% more.

Bulk ships from North America were three in last

December and one in January with total volume of 37 M

cbms with December arrival of 42,000 cbms so unusually

high supply because the supplier took additional orders in

fear of log shortage in the first quarter so the first quarter

supply will drop.

Problem is that the market in Japan is becoming bearish

with heavy inventory but worldwide wood market is

recovering and the prices are climbing again. Daily

shipment volume in January was 3,610 cbms, 29.9% more

than December.

This is the highest since September 2019 so the inventory

should decrease speedily. With bearish mood, second

quarter contract volume is expected to decrease largely.

Inventory shortage may become serious in summer

months.

Price hike of softwood plywood

Plywood manufacturers in Japan announced to increase

the sales prices of softwood plywood by 100 yen to 1,700

yen per sheet on 12 mm thick 3x6 panel since March

1.Producing cost has been climbing much faster than the

manufacturers expected. Cost of cedar log and adhesive is

increasing month after month.

Log prices in the North East continue climbing as

competition with laminated lumber mills is keen and even

plywood mills outside the region are now buying logs in

the North East so cedar 4 meter log prices are now15,000

yen per cbm delivered, 1,500 yen up from last month and

larch log prices are 22,0000-25,000 yen , 2,000-3,000 yen

up from January.

Plywood mills use Russian made larch veneer but

deliveries are delayed by rough sea in winter and difficulty

of securing shipˇŻs space. Adhesive prices also continue

climbing as oil and natural gas prices are soaring so

adhesive manufacturers are likely to ask price hike further

more.

Demand for plywood is active mainly by precutting plants

so demand continues more than the production.

Precutting plants buy allocated volume even if they do not

need in fear of future supply shortage.24 mm and 28 mm

3x6 panel prices are up by 100 yen at 3,400 yen and 3,950

yen.

Of immediate concern to plywood mills is procurement of

material logs. Particularly in the North East, snow fall is

much more than normal years and log prices continue

climbing. Precutting orders are not increasing while the

plants are busy processing orders they have now. Orders

are declining in heavy snowed areas. Precutting plants

keep buying plywood in an anticipation of demand

increase in coming months and keep extra volume in

inventory.

For plywood mills not only high cost of logs but other

factors are inflating such as oil and natural gas, trucking

cost and adhesive cost so overall producing cost continues

climbing.

South Sea plywood manufacturers are struggling tight log

supply and inflating adhesive cost so they are determined

to pass higher cost onto sales prices.

In Japan, it is time to make purchase as the inventory

continues declining but offer volume by South East Asian

plywood manufacturers is very limited, about a half of

normal period so it is hard to buy what they need then the

market in Japan is uncertain so importers are hesitant to

make future purchase.

|