|

Report from

Europe

Price inflation drives rise in value of UK tropical wood

product imports

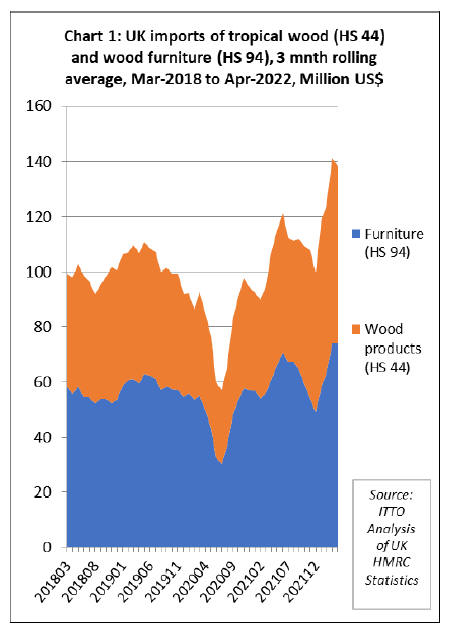

The import value of tropical wood and wood furniture into

the UK in the opening four months of this year were at an

unprecedented level of US$565 million (Chart 1). That is

36% more than the same period in 2021 when imports

were also high following a strong rebound after the

downturn during the first COVID lockdown in 2020.

In fact, this was by far the strongest start to the year in

terms of UK import value of tropical wood and wood

furniture products since at least before the 2008 financial

crises. It compares to an average import value of less than

US$380 million for the January to April period throughout

the whole decade prior to the onset of the pandemic in

2019.

The rise in UK import quantity of tropical wood and wood

furniture was much less dramatic in the first four months

of this year, at 118,000 tonnes, just 10% more than the

same period in 2021. This shows that price inflation was

the major factor behind the rise in import value.

Significant weakening of the value of the GBP on foreign

exchange markets since the end of April, combined with

the wider geo-political situation, implies that price

inflation will remain a key issue for UK importers in the

months of ahead. It also indicates that the current boom in

UK imports may well be short-lived.

Availability of hardwood and furniture products from the

UK's traditionally largest suppliers in Europe has become

even more challenging since Russia's invasion of Ukraine

encouraging importers to look more to tropical products.

COVID lockdowns have also seriously disrupted

availability of manufactured wood products from China.

Hardwood product prices were declining steadily from the

middle of last year to February this year. Even in February

prices remained at historically high levels and the

downward trend has reversed since RussiaˇŻs invasion of

Ukraine. UK government figures indicate that average

timber prices at point of sale to UK building firms were

30% up in the year to April 2022, compared with a year

earlier.

Freight rates also declined from the heights reached in the

third quarter of last year but are still at a historically very

high level. For example, the cost of a 40ft container from

China into the UK was US$11,000 at the start of this

month, less than its peak of US$14,700 in October, but a

huge rise from US$1,500 in summer 2020.

The war in Ukraine has seriously disrupted all supplies of

European and Russian hardwood products, partly because

of the direct effects of sanctions against Russia, partly the

immediate effects of the war on Ukrainian supply, and

partly because of the large numbers of Ukrainians, who

contribute a disproportionately large number of truck

drivers operating in Europe, who returned home during the

conflict. The war has also driven up energy costs, filtering

through into rising prices for all European manufactured

products, including for wood and furniture.

While higher import prices were the major driver of

increased UK import value in the opening months of this

year, the trend was partly due to continuing high

consumption in the UK, supported by post-COVID

government stimulus. Demand during this period was

particularly strong in housing repair, maintenance, and

improvement, a major source of hardwood demand and the

fastest growing part of the UK construction sector

following the initial COVID lockdown.

According to the UK Construction Products Association

latest survey, nearly half of materials firms in the UK said

sales had jumped in the first three months of 2022

compared to the fourth quarter of last year. Increased sales

were reported by around 50% of so-called ˇ°light sideˇ±

manufacturers of products like windows, doors and

kitchens.

However, prospects for the UK economy for the rest of

this year are far from promising. Economists have said it is

increasingly likely that the UK will sink into recession this

year. In June, the Paris-based OECD cut its UK growth

forecast for 2023 to zero, the lowest in the G20. Also in

June, the Bank of England raised interest rates to 1.25 per

cent to tackle fast rising inflation, which is expected to

reach 11% by October.

The latest S&P Global / CIPS UK Construction

Purchasing Managers Index (PMI) report for May

indicates that the wider economic slowdown is beginning

to filter through into declining UK construction sector

activity. The report notes that "Though still offering a

comfortable margin above the no change mark, the

construction sector saw growth ease to a four-month low

with the usual suspects taking the heat out of the recovery

¨C elevated inflation, future uncertainty and supply-chain

disruptionˇ±.

The PMI report goes on to say that ˇ°The UK housing

sector in particular showed further signs of fragility with

the worst performance since May 2020 and moving closer

to the danger zone of negative territory. Affordability

concerns will be weighing on the mind of potential house

buyers grappling with escalating costs for everyday items,

resulting in a postponement of big purchases until the UK

economy shows more resilienceˇ±.

Furthermore, "The lack of positive sentiment was also

reflected in construction companiesˇŻ confidence over the

next 12 months, with optimism dropping to the weakest

since August 2020ˇ±.

The PMI report also suggests that recent strong material

purchases in the UK construction sector are partly driven

by a desire to beat anticipated price increases in the

months ahead as inflation rates are exceedingly high.

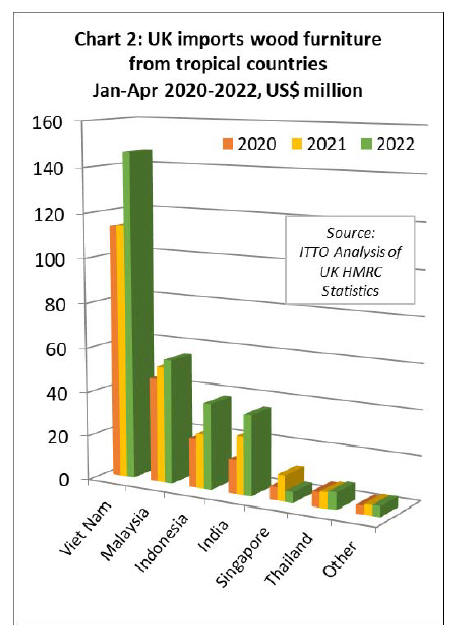

Indonesia leads rise in tropical wood furniture imports

into the UK

The UK imported US$284 million of tropical wood

furniture products in the first four months of 2022, which

is 23% more than the same period in 2021. In quantity

terms, wood furniture imports were 64,000 tonnes during

the four month period, the same level as the previous year.

This indicates that the rise in value was driven more by

price inflation than strong demand.

Import values increased from all four of the leading

tropical supply countries to this market in the opening four

months of this year compared to last including Vietnam

(+28% to US$147 million), Malaysia (+7% to US$56

million), Indonesia (+59% to US$39 million) and India

(+39% to US$36 million). Imports from Singapore, which

increased sharply last year due to shipping problems

elsewhere in Southeast Asia, fell back 59% to more a

"normal" level of just US$5 million in the four month

period (Chart 2).

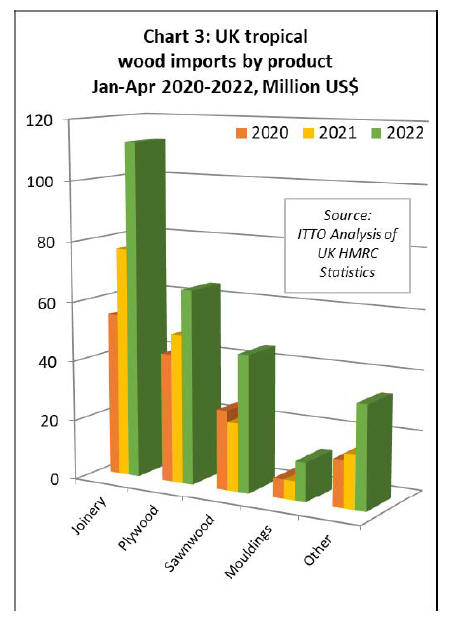

UK tropical wood imports up 72% in the first two

months of 2022

Total UK import value of all tropical wood products in

Chapter 44 of the Harmonised System (HS) of product

codes were US$271 million between January and April

this year, 55% more than the same period in 2022. In

quantity terms imports increased 16% to 118,000 tonnes

during the period.

Compared to the first four months last year, UK import

value of tropical joinery products increased 46% to

US$112 million, import value of tropical plywood was up

30% to US$65 million, import value of tropical sawnwood

increased 100% to US$46 million, and import value of

tropical mouldings/decking also increased 100% to US$13

million (Chart 3).

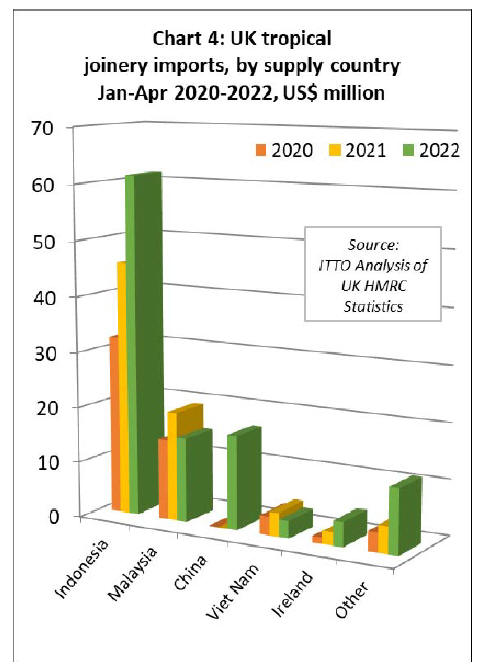

After the sharp dip in UK imports of tropical joinery

products during the first lockdown period in the second

quarter of 2020, imports of this commodity group have

progressively built momentum.

This trend is mainly driven by Indonesia for which UK

joinery imports, mainly consisting of doors, were US$61

million in the first four months this year, 34% more than

the same period in 2021 (Chart 4). In quantity terms, UK

joinery imports from Indonesia were 19,000 tonnes in the

first four months of this year, 6% more than the same

period in 2021.

UK imports of joinery products from Malaysia and

Vietnam (mainly laminated products for kitchen and

window applications) started this year more slowly.

Import value from Malaysia was US$15 million in the

January to April period, 23% less than the same period last

year. In quantity terms, imports from Malaysia were 4,800

tonnes, 35% less than the same period in 2021. Joinery

imports from Vietnam of 834 tonnes valued at US$3

million were respectively 39% and 26% less than the same

period last year.

UK imports of Chinese tropical joinery products, nearly all

comprising doors, were 6,200 tonnes with value of US$17

million in the first four months of 2022, up from negligible

levels in previous years. Due to introduction from 1st

January 2022 of new product codes in the EU Combined

Nomenclature (still mirrored by the UK post-Brexit) it is

now possible to identify wood doors and windows

manufactured using a wider range of tropical wood species

in UK and EU trade statistics.

The apparent rise in imports of "tropical" wood joinery

from China is very likely due to these products now being

identifiable as of tropical species, whereas previously they

were classified as "other non-coniferous" in the trade

statistics and excluded from the figures for tropical wood

imports.

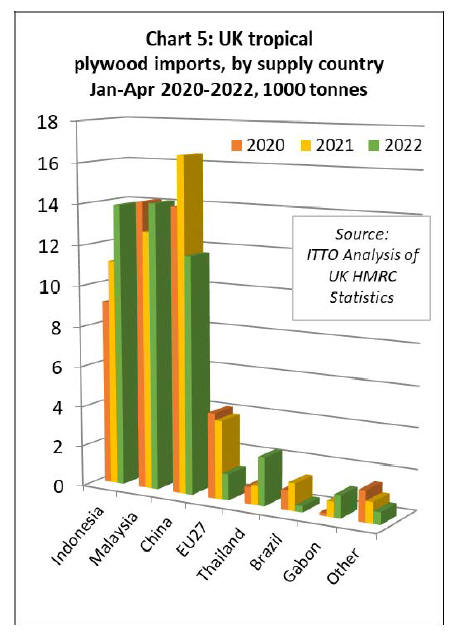

In the first four months of 2022, the UK imported 45,400

tonnes of tropical hardwood plywood, 6% less than the

same period last year. Tropical hardwood plywood

imports from Indonesia have made gains this year, while

imports from China have continued to slide (Chart 5).

The UK imported 13,900 tonnes of tropical plywood from

Indonesia in the first four months of this year, a gain of

25% compared to the same period last year. Imports from

Indonesia, which increased sharply in the first two months

of the year, slowed in March and April.

In contrast, UK plywood imports from Malaysia were very

slow in the opening two months this year but strengthened

in March and April. By the end of the first four months,

the UK had imported 14,100 tonnes of plywood from

Malaysia, 11% more than the previous year.

The UK imported 11,700 tonnes of tropical hardwood

plywood from China in the first four months this year,

29% less than the same period in 2021, trade having been

affected by COVID lockdowns in China. At the same

time, Brexit is impacting on UK imports of tropical

hardwood plywood from EU countries which were just

1,300 tonnes in the opening four months of this year. This

compares to around 4,000 tonnes during the same period

in the last two years.

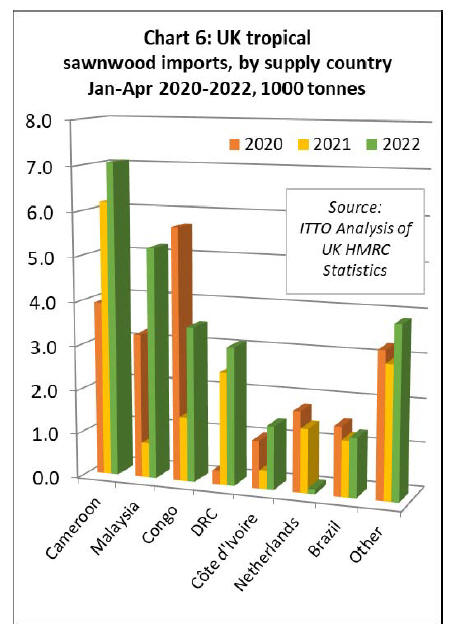

Shift in countries supplying tropical sawnwood to the

UK

UK imports of tropical sawnwood started this year

strongly. Imports were 25,600 tonnes in the first four

months of 2022, 50% more than the same period last year.

In addition to making major gains overall, there were big

changes in the countries supplying tropical sawnwood to

the UK in the opening months of this year (Chart 6).

This is indicative of the major shifts in hardwood markets

since the start of the pandemic which have led to

significant supply shortages and sharply increasing prices

in many supply regions and continuing high levels of

demand in markets like the UK.

UK imports of tropical sawnwood from Cameroon were

7,100 tonnes in the first four months of this year, 14%

more than the relatively high level in the same period last

year. UK imports from Malaysia, which had fallen to little

more than a trickle in recent years, were 5,200 tonnes in

the first four months this year, nearly a 6-fold increase

compared to the same period last year.

UK imports of tropical sawnwood from the Republic of

Congo (RoC) were 3,500 tonnes in the first four months of

this year, nearly three times the level of last year but still

well down on the pre-pandemic level. Meanwhile there

has been a significant rise in UK imports of sawnwood

from DRC, which were 3,100 tonnes in the first four

months this year, a gain of 23% compared to the same

period last year.

UK imports from DRC were negligible before the

pandemic. UK imports of tropical sawnwood from Côte

d'Ivoire were 1,400 tonnes in the first four months this

year, a 240% increase compared to negligible imports in

the same period last year.

Imports of tropical hardwood sawnwood from Brazil were

1,300 tonnes in the first four months of this year, 6% more

than the same period last year but still down on the prepandemic

level.

Indirect UK imports of tropical sawnwood from EU

countries have fallen dramatically since the UKˇŻs

departure from the EU single market on 1st January 2021.

Total UK imports from EU countries were 1,600 tonnes in

the first four months of this year, 48% less than the same

period last year.

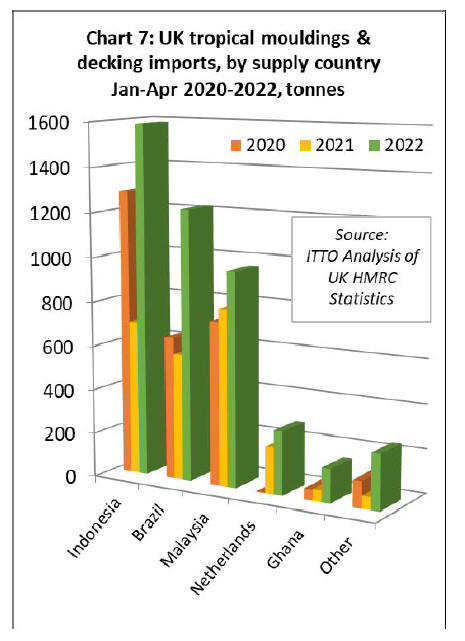

UK imports of tropical hardwood mouldings/decking were

relatively high in the opening four months of 2022, at

4,500 tonnes, 87% more than the same period the previous

year. This is another commodity group for which there has

been particularly strong demand in the UK, combined with

sharply tightening supply since the start of the pandemic.

The war in Ukraine and sanctions on Russia are expected

to lead to even tighter supplies of non-tropical decking

products that directly compete with tropical decking in the

short to medium term.

UK imports of decking/mouldings increased sharply from

Indonesia and Brazil in the first four months of this year.

Imports of 1,600 tonnes from Indonesia were 128% more

than the same period last year. Imports of 1,200 tonnes

from Brazil were 113% up on the same period in 2021.

Imports from Malaysia increased 21% to 1,000 tonnes

during the four month period. (Chart 7).

Leading media outlets highlight mounting concern

over European wood supply

The extent of concern surrounding disruption to wood

supplies in Europe due to the war in Ukraine is highlighted

by this issue now being the focus of reports by mainstream

media outlets in the region.

On 19 June, the London-based Financial Times (FT)

published an article under the headline ˇ°Ukraine war hits

global timber trade and adds to risks for forestˇ±

(https://www.ft.com/content/d6388b32-757b-4484-95ff-720b4b2319f3).

The articles notes that ˇ°The war in Ukraine has caused

serious disruption to the global timber trade and increased

concerns over forest destruction as exports are interrupted,

environmental protections are lifted and Kyiv redirects

manpower away from fighting wildfires to the front lineˇ±.

The FT reports that international sanctions imposed over

MoscowˇŻs invasion of Ukraine have curbed supplies from

Russia, the worldˇŻs largest exporter of softwood timber,

and Belarus, while the conflict has severely hampered

production in Ukraine.

It is noted that ˇ°the three countries accounted for a quarter

of the worldwide timber trade last year, according to

industry figures. They exported 8.5mn cubic metres of

softwood to Europe last year, just under 10 per cent of the

regionˇŻs demand. Russia, the worldˇŻs largest exporter of

softwood, alone produces about 40mn cubic metres a

yearˇ±.

ˇ°Timber producing and exporting nations are taking steps

to make up the shortfall, including loosening some

environmental protections to increase productionˇ±,

according to the FT. In Ukraine itself, the FT notes that

ˇ°Soon after FebruaryˇŻs invasion, Kyiv lifted a regulation

that prohibits logging in protected forests during spring

and early summer, as part of a bill to increase the

countryˇŻs defence capabilities during martial law, partly

by boosting export earningsˇ±.

The FT quotes UkraineˇŻs environmental protection

ministry as stating earlier this year that ˇ°the sanctions

offered the country the chance to increase its share of the

European timber market in RussiaˇŻs place and boost

financing of post-war reconstruction effortsˇ±.

The FT goes on to suggest that ˇ°Other exporters including

Estonia, Finland and the US are also seeking to increase

logging volumes. In the US, the House Committee on

Natural Resources in April introduced the No Timber

From Tyrants bill, which would ban imports of wood

products from Russia and Belarus and authorise an

equivalent amount of domestic harvesting in 2021 to make

up for lost importsˇ±.

According to the FT, ˇ°Earlier this month Estonia

announced a relaxation of logging restrictions on stateowned

land, which is home to about half of the countryˇŻs

forests. As a result, the area of land logged will increase

by almost a quarter to 2,400 hectaresˇ± and ˇ°Finland is

expected to boost harvesting volumes by 3 per cent for

each of the next two yearsˇ±.

Another recent mainstream media article ¨C this one in

Dezeen published 17 June, one of the worldˇŻs most

influential architecture, interiors and design magazines

(https://www.dezeen.com/2022/06/17/timber-shortageukraine-

war-news/) states that ˇ°architects and designers

are struggling to source wood for their projects as Russia's

invasion of Ukraine has brought imports from the region

to a standstill, threatening stocks and driving up prices

across the continentˇ±.

According to Dezeen, studios in Europe are ˇ°reporting that

costs for solid oak and birch plywood have doubled in the

last few months, while others have seen the price of

structural timber go up by around 20 per centˇ±. The article

quotes Sean Sutcliffe, co-founder of British furniture

maker Benchmark: "Everyone is really worried about

their supply chains. We have projects where it would now

cost me more to buy the wood that I'm charging for the

whole thing." Birch plywood is "just not available

anymore", Sutcliffe said.

In another quote, Signe Bindslev Henriksen of Danish

design studio Space Copenhagen is reported as saying that

solid oak ˇ°is almost like gold at the moment. Everybody is

using up all their stock. Suppliers and manufacturers can

deliver right now but in just a few months' time, it'll be all

gone."

Dezeen notes that while most European wood imports

from Russia, Belarus and Ukraine go to the Baltic states,

Germany and Finland, ˇ°architects and designers say the

knock-on effects are being felt across Europe.ˇ±

Sean Sutcliffe is reported as saying that "we didn't

actually buy any Ukrainian or Russian wood. But of

course, all the people that did are now crowded into

Western Europe, which is where our supply chain comes

from." Due to svere shortages of European oak,

Benchmark are reported to be making all new products

presented at Clerkenwell Design Week last month from

local British ash and American red oak.

|