|

Report from

Europe

Unprecedented period of change in European wooden

furniture sector

The last two and half years, marked from the start of 2020

by the Covid-19 pandemic and from February this year by

war in Ukraine, have seen unprecedented changes in

EuropeˇŻs wood furniture sector. The sector has passed

through a period characterised by an initial but very short

lived fall in demand in the second quarter of 2020,

followed by rapid demand escalation at a time when

material shortages and other logistical challenges greatly

reduced availability.

During this relatively short period, major changes have

occurred in patterns of supply and demand, trade flows,

consumer preferences and working conditions, distribution

channels, design, and fashion trends. Companies

throughout the sector are having to evolve new strategies

in response to a transformed world.

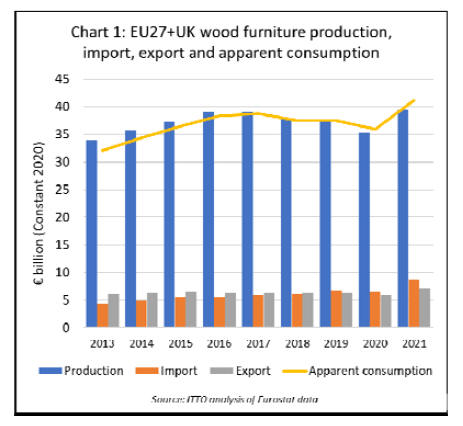

Recent trends in the value of production trade and

consumption of wood furniture in the EU27+UK are

shown in Chart 1. This highlights that wood furniture

production and consumption was weakening in the years

before the onset of the pandemic in response to sluggish

growth of the EU27+UK economy and intense

competition in global markets, particularly from Chinese

manufacturers whose sales in the US market were being

diverted elsewhere due to the trade dispute.

Due to the onset of the pandemic, there was an estimated

5% downturn in the euro value of EU27+UK wood

furniture production and 4% decline in consumption.

However this was followed in 2021 by an unexpectedly

strong 12% and 15% rebound respectively in production

and consumption.

According to CSIL, the Milan based furniture research

organisation (www.worldfurnitureonline.com), the last

two years of the European furniture sector have been

marked by a significant mismatch between supply and

demand.

A sharp reduction in production of wood and other

essential material inputs, severe logistical problems in

international trade, rapidly rising freight rates, shortages of

key staff, social distancing measures at manufacturing

plants, and a big increase in energy prices all placed limits

on production and supply.

This meant that, while furniture production and imports

rebounded strongly in many European countries, they

failed to keep pace with an even sharper increase in

demand. The rise in demand was mainly due to a shift in

consumer spending away from travel and leisure towards

home-related product categories and to cater for new home

offices with the rise in remote working. There was also

resumption in export market growth in 2021.

The mismatch between demand and supply caused a

general increase in furniture prices, initially at the

manufacturing stage and partly absorbed by

manufacturers, and then progressively transferred to final

consumers.

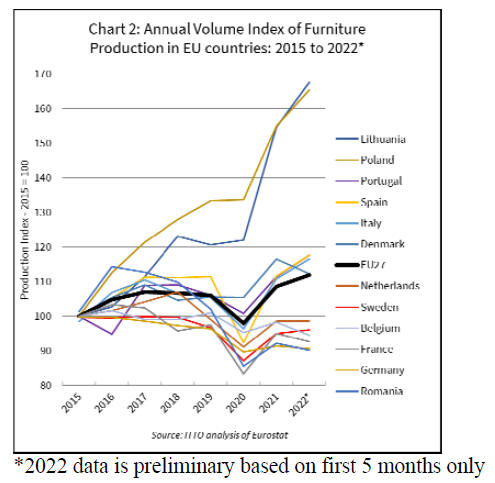

Furniture sector performance varied widely between

European countries. Eurostat data shows that while overall

EU27 furniture production had rebounded to pre-pandemic

levels before the end of 2021, production was still below

these levels in many countries including Germany, France,

Sweden, and Romania. In contrast production in some

countries, notably Poland and Lithuania, remained strong

even during the first year of the pandemic in 2020, and

continued to rise in 2021 and the first half of 2022 (Chart

2).

Looking forward, CSIL forecast that after the exceptional

rebound in European furniture production in 2021, 2022 is

expected to be another strong year on the demand side,

although the rebound effect will slow compared to last

year. This is partly due to reallocation of household

spending back towards travel and other leisure activities.

High inflation and soaring furniture prices are also

expected to have a dampening effect on down.

On the other hand purchasing in the commercial sector is

expected to remain robust.

Supply chain disruptions are expected to persist,

particularly due to rising energy prices, lack of qualified

workers, and the fallout from the Russia-Ukraine war. The

conflict is increasing material supply difficulties, notably

for timber products, and commodity prices are expected to

remain elevated at least for the remainder of this year. The

outlook for European inflation and wider economic growth

is heavily dependent on how the war in Ukraine will

unfold, the impact of sanctions and other measures, and

how these feed through into energy prices and consumer

confidence.

According to CSIL there are several positive factors

expected to maintain strong demand for furniture in

Europe in the coming months including the continuing

roll-out of the EU's Recovery and Resilience Facility

(RRF), some significant national level support measures,

such as a fiscal bonus in Italy which was extended into

2022, growth in residential construction in several

European countries, and improved export market prospects

for European manufacturers, driven both by increased

affluence of consumers in some emerging markets, and by

continuing efforts in the US to reduce dependence on

imports from China.

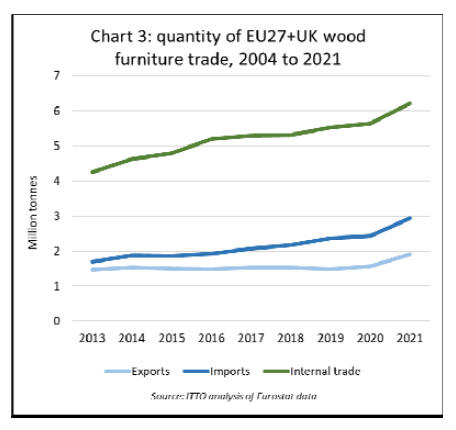

Recent trends in the quantity of European wood furniture

trade as revealed by Eurostat trade data are somewhat

surprising. The long-term rise in European trade which

began in 2013 as the European economy gradually

recovered from the 2008-09 global financial crises and

subsequent eurozone currency crisis, continued apparently

uninterrupted by the pandemic. The most notable recent

trend is the upturn in trade in 2021, apparent both in

EU27+UK external and internal trade (Chart 3).

Overall, the signs are that EU wood furniture

manufacturers, while still dominant inside the EU single

market, accounting for around 80% of total consumption

value in the region, have been gradually losing

competitiveness in other global markets.

Exports by EU27+UK manufacturers to other regions of

the world were broadly flat in quantity terms and slightly

declining in value terms before 2021. Last year,

EU27+UK wood furniture exports to countries outside the

region increased sharply, rising 21% to both euro value

and quantity terms, but it remains to be seen whether this

growth can be sustained.

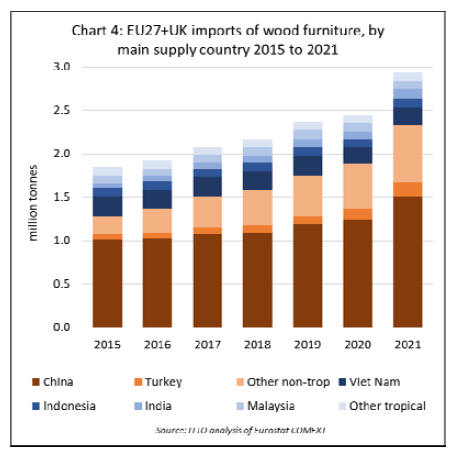

Meanwhile manufacturers outside the region, notably in

neighbouring non-EU countries and China, slowly

increased their share of the EU27+UK market in the years

before 2022. The share of non-EU suppliers in EU27+UK

wood furniture consumption increased to 21% in 2021, up

from 18% the previous year and 15% five years earlier.

Between 2015 and 2019, EU27+UK imports of wood

furniture from outside the region increased fairly

consistently at an average rate of 6% per year. In 2020, the

onset of the pandemic and related logistical problems led

to a slower rate of import growth of only around 3% to

2.44 million tonnes. Last year, import growth accelerated

sharply, rising over 20% to 2.93 million tonnes.

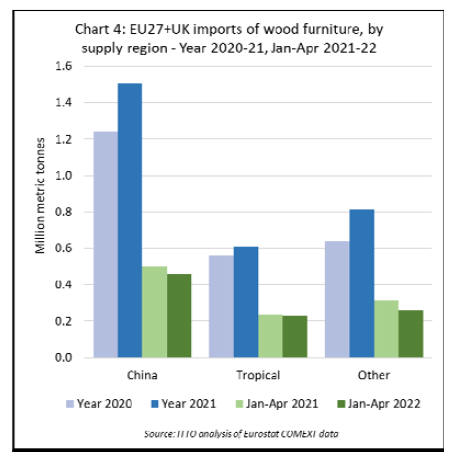

In recent years, by far the largest growth in EU27+UK

wood furniture imports in quantity terms was from China

(Chart 4). In terms of percentage growth rate, the largest

growth was from countries neighbouring the EU, notably

Turkey, Ukraine, Belarus, Serbia and Russia. EU27+UK

wood furniture imports from tropical countries averaged

no more than 2.4% per annum between 2015 and 2019,

and then fell 10% to 560,000 tonnes in 2020. Last year,

imports of tropical wood furniture rebounded 10% to

610,000 tonnes.

Notwithstanding CSILˇŻs prediction of continuing good

demand for furniture in Europe in 2022, EU27+UK

imports of wood furniture were down 10% in quantity

terms, to 950,000 tonnes, in the first four months of this

year. Import tonnage decreased from all main supply

regions during the first four months of 2022; by 8% from

China to 460,000 tonnes, by 3% from the tropics to

230,000 tonnes; and by 17% from other countries to

260,000 tonnes (Chart 4).

The decline is indicative of severe supply problems caused

most notably by the renewed COVID lockdown in parts of

China, and the war in Ukraine and associated trade

sanctions against Russia and Belarus.

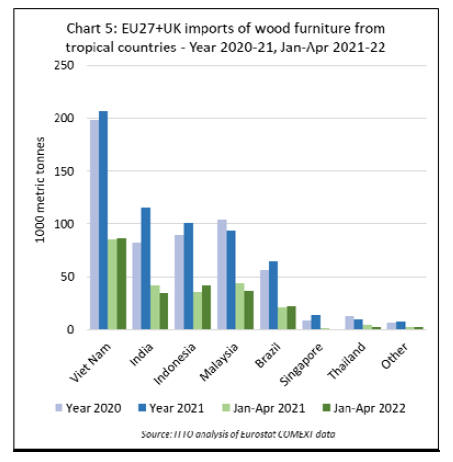

Of tropical countries supplying wood furniture to the

EU27+UK, Indonesia recorded the largest gain in this

market in the first four months of 2022, rising 18% to

42,000 tonnes. Imports also increased from Brazil, by 8%

to 22,000 tonnes.

Imports from Vietnam were stable at 82,000 tonnes.

Imports from all other leading tropical supply countries

declined, including India (-16% to 35,000 tonnes),

Malaysia (-15% to 37,000 tonnes), Thailand (-39% to

3,000 tonnes) and Singapore (-53% to 1,000 tonnes)

(Chart 5).

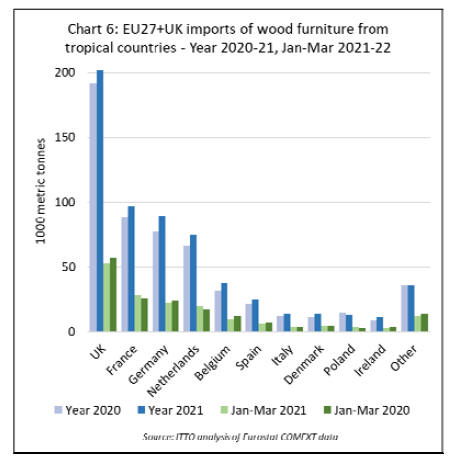

Tropical wood furniture import trends varied very widely

between EU27+UK countries in the opening months of

this year, with no clear pattern emerging (Chart 6).

In the first quarter of 2022, a rise in imports was recorded

in the UK (+8% to 57,500 tonnes), Germany (+6% to

23,800 tonnes), Belgium (+29% to 12,600 tonnes), Spain

(+7% to 7,000 tonnes), Italy (+9% to 4,300 tonnes) and

Ireland (+24% to 3,500 tonnes). However imports declined

into France (-8% to 25,900 tonnes), Netherlands (-16% to

16,900 tonnes), and Poland (-18% to 3,300 tonnes).

Imports into Denmark were stable at 4,400 tonnes during

the three month period.

Major structural changes in European furniture

distribution

A new CSIL report highlights major structural changes in

EuropeˇŻs furniture sector. Although some of the trends

have been underway now for at least a decade, recent

events have brought about accelerating change. According

to the report, major trends include:

An unprecedented increase in online sales that now

account for over 10% of the total European furniture

market. The pandemic outbreak accelerated a massive

change in consumer behaviour shifting from offline stores

to e-commerce. Moreover, the e-commerce channel has

bolstered international penetration enabling leading

furniture retailers to expand into new markets at lower

costs (including countries where they may have a limited

network of stores).

A slightly decreasing share of the overall market occupied

'specialist' retailers. This trend is mainly due to the

increasing role of the online channel that has eroded

market share of organized chains specialized in home

furniture and of independent stores. The latter particularly

suffered in 2020 during the months of lockdown.

Relative stability of market share of ˇ®non-specializedˇŻ

retailers. During and after the pandemic outbreak, home

improvement projects increased particularly benefitting

DIY chains. DIY chains were also able to remain open

during the months of the lockdowns while other

competitors were forced to close.

Changing behaviour of consumers impacting on

distribution of big supermarkets and hypermarkets.

Shopping districts in large towns and city centres have

become a far more attractive place to purchase. Leading

international furniture retail chains, such as IKEA and

Maisons du Monde are developing new store concepts.

For more than half a decade, IKEA has been a singleformat

retailer. However it is now investigating new ways

of meeting customer needs. For example by establishing

stores in inner-city locations and by balancing the big-box

superstore format with smaller format stores that use

digital technology to provide access to the full product

range.

More details are available the 2022 edition of CSIL report

ˇ°Furniture Retailing In Europeˇ± which provides analysis

of home furniture distribution in 13 European countries

(Austria, Belgium, Denmark, Finland, France, Germany,

Italy, the Netherlands, Norway, Spain, Sweden,

Switzerland and the United Kingdom), including trends In

home furniture consumption, market forecasts, data by

country, analysis by distribution channel, retail formats

and sales performances of leading home furniture retailers.

See:

www.worldfurnitureonlIne.corn

Strong outdoor furniture market in Europe

The outdoor furniture market in Europe is one of the best

performers in the furniture sector, according to a new

report focused on this sector just published by CSIL. Total

annual sales of outdoor furniture in Europe are estimated

by CSIL to be around €3.3 billion. Following a slight

reduction in 2020 the sector recorded a double-digit

rebound in 2021, well above the sector average.

The largest outdoor furniture markets within Europe are

Germany, the United Kingdom, France, and Italy,

accounting for a combined market share of over 50%.

According to CSIL, consumption of outdoor furniture in

Europe is expected to continue to increase in 2022 and

2023.

During the first part of the pandemic (2020) the drop of

the outdoor furniture market was contained. Good retail

sales offset a sharp decline in contract sales. However,

starting from 2021 most manufacturers also experienced a

rebound of the contract sector as many activities put on

hold the previous year were restarted.

The hospitality industry is an component of outdoor

furniture demand in Europe. Official Eurostat statistics

released by Eurostat and reported by CSIL show a

significant fall in the number of hotels in Europe in 2020

as a main consequence of Covid-19.

However, with some of the world's most popular tourist

destinations, Europe has seen a revival in domestic and

inter-regional travel in the past year. International arrivals

to Europe increased nearly 75% in 2021.

There is now optimism that delayed projects in the hotel

and wider tourist sector will soon be completed.

According to data from Lodging Econometrics at the end

of 2021, Europe's hotel construction pipeline stood at

1,824 projects and nearly 300,000 rooms. A further 474

new hotels and 70,000 rooms are expected to open in 2022

and 504 new hotels with 75,015 rooms in 2023.

The outdoor sector is much more dependent on imports

than other furniture sectors in Europe. Slightly more than

half of all outdoor furniture imported by EU countries is

from countries outside the EU, with around 60% of non-

EU imports derived from China and 30% from tropical

countries in Southeast Asia.

There has been a long term rising trend in European

imports of outdoor furniture from outside the region,

although CSIL believes that recent factors, such as the raw

materials shortages and high freight rates may lead to a

partial reshoring of sourcing activities in the next few

years.

CSIL note that the outdoor furniture market is served via a

wide variety of channels, both specialist and non-specialist

distributors, from large scale retail chains to small

independent stores, and from 'pure' online players to brickand-

mortar operators.

Overall the role of non-specialist retailers is higher in this

sector than for most other furniture sectors such as

upholstery, kitchen furniture, and office furniture. DIY

chains and garden centres are still pivotal sales channels.

However, there has been some growth in sales via more

specialist retailers in recent years, first as the large-scale

furniture chains expanded outdoor collections and more

recently as more independent retailers are promoting

designer outdoor brands.

The e-commerce channel is also growing rapidly. Both

manufacturers and retailers are extending their web

marketing activity and upgrading their on-line presence.

No longer do they only display product pictures and

prices, but also seek to guide and inspire customers with

design suggestions and case studies.

On design and fashion trends, CSIL highlight the

increased focus on the interaction between indoor and

outdoor spaces within the home. Already a feature of the

market before the pandemic, it has become even more

significant during the lockdown period as consumers were

encouraged to enhance their home living experience.

More people have been turning outdoor areas into a 'green

living-rooms'. The borders between indoors and outdoors

are merging and there is more demand for dual purpose

furniture items that can be moved inside and out.

With high levels of urbanisation, there is particular

demand for furnishings for smaller gardens, roof terraces

and balconies.

Manufacturers are responding by producing narrow tables

and loungers and more multifunctional items, whose

backs, arms and sitting areas can be readily adjusted or

repositioned, to offer flexibility. Just as living rooms are

moving outdoors, so too are dining rooms. Manufacturers

are now developing flexible open-air dining room

furnishings such as extendable tables. Teak is still popular,

but more often than not it is combined with other materials

such as aluminium, ceramic, and waterproof outdoor

fabrics. And the strong focus on sustainability, low

environmental impact, and use of ˇ°naturalˇ± and ˇ°ecofriendlyˇ±

materials only grows stronger in Europe.

More details ˇ®The European Market for outdoor furnitureˇŻ, CSIL,

May 2022,

www.worldfurnitureonline.com

Furniture sector needs new strategies in time of

uncertainty

An article by Mindaugas Morkunas, Head of Sales Eastern

Europe and CIS for Henkel, a German company supplying

chemicals to the worldwide furniture industry, highlights

key recent trends in the global furniture sector and

provides advice on strategic responses.

According to Morkanus, ˇ°due to the global pandemic, the

international trade system experienced the biggest

disruption since the Second World Warˇ±. He notes the ongoing

ˇ°turmoilˇ± in the furniture supply chain with

additional layers of uncertainty now appearing due to the

new COVID-19 outbreaks in China, RussiaˇŻs war in

Ukraine, and other global challenges.

Morkanus suggests that the biggest risk for the furniture

industry in Europe is the possible recession. ˇ°Some signs

are already there, as huge furniture players are decreasing

production since warehouses are already full. Buying

furniture while war is around the corner certainly isnˇŻt

among customersˇŻ top prioritiesˇ±.

There are on-going significant changes in the way

furniture companies view supply chains and inventory,

says Morkanus. ˇ°As it is getting difficult to predict

consumer demand, the furniture businesses are moving

from a Just-in-Time to a Just-in-Case approach.

The goal of this type of inventory management is to

minimize the probability that products will go out of stock.

Knowing all the challenges in the supply chain, producers

are trying their best to build stock with additional raw

materials. However, this can increase the backlog in

supply even more as demand is still growingˇ±.He suggests

that now, more than ever, it is crucial for furniture

manufacturers to build a resilient supply chain.

He suggests three main ways to achieve this:

Moving closer to the market, or ˇ°nearshoringˇ±

which Morkanus notes from his own experience

is already happening. ˇ°Geographically closer

countries can offer many benefits ¨C from

improving control of the supply market to quicker

transit for the end consumerˇ±.

Moving to a lower price segment in production to

reach more customers. Morkanus suggests that

ˇ°as raw material, energy, and transport costs are

skyrocketing, furniture becomes more expensive.

The only way to still reach low-income customers

is to move towards the production of lower-cost

furniture using cheaper raw materials. The

drawback here is obvious ¨C the quality will

decrease. However, quality is not the main focus

for many customers nowadays ¨C affordability is

often more importantˇ±.

Securing alternative raw materials suppliers.

Morkanus observes that ˇ°In most cases,

producers have one main supplier per raw

material. Now it seems like a good idea to move

towards having even 3-4 of themˇ±.

See:

https://www.mdpi.com/2071-1050/12/11/4343

|