|

Report from

North America

Tropical hardwood imports dip

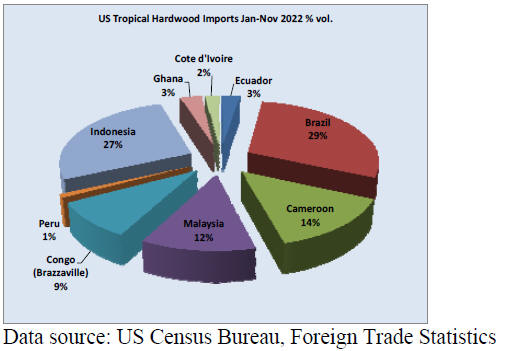

US imports of sawn tropical hardwood fell 10% in

November. The 18,578 cubic metres imported was the

lowest monthly total of the year except for August.

Volume of the most-imported woods all declined as

imports of Ipe fell 12%, Sapelli dropped 19%, and

Keruing plunged 52%.

Imports of Mahogany and Balsa both showed impressive

gains over October’s numbers. Imports were down for the

month from most trading partners yet imports from

Cameroon rose 38% and imports from Ecuador rose 68%

to both reach their strongest month of the year.

While direct year to year comparisons are difficult due to

changes in measurements by the US Department of

Agriculture, the total volume of sawn tropical hardwood

imported into the US in 2022 through November appears

to already be more than double that for all of 2021.

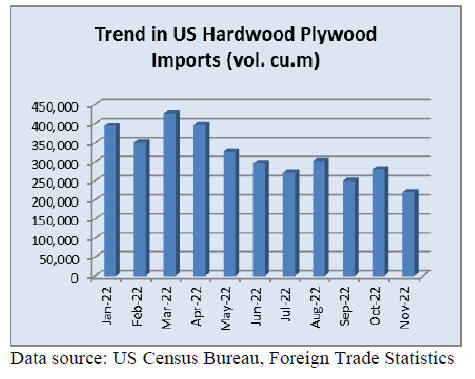

Hardwood plywood imports fall 21%

US imports of hardwood plywood declined by 21% in

November, falling to their lowest level since January

2021. The 220,249 cubic metres imported was 22.5% less

than that of November 2021.

Imports from Russia, which inexplicably inflated in

October, crashed in November falling 90% to their lowest

level in nearly 12 years. Imports from Malaysia,

Cambodia, China and Vietnam also fell sharply.

Despite the declines, total imports from nearly all trading

partners remain ahead of 2021 totals through November.

Total US imports of hardwood plywood are up 14% over

last year through November.

Veneer imports gain

US imports of tropical hardwood rose 9% in November as

imports from Africa soared. Imports from Cameroon rose

695% in November to an all-time record level while

imports from Cote d’Ivoire doubled to reach their highest

level since September 2018. These gains more than offset

sharp declines in imports from China and India.

Total imports for November were 65% higher than the

previous November while year to date imports are up 55%

over 2021. Imports from all major trading partners are

well ahead of 2021 year to date through November.

Hardwood flooring imports decline

US imports of hardwood flooring fell by 24% in

November to a level 27% less than that of November

2021. Imports from Brazil declined 66% while imports

from Malaysia slid 23%.

Imports from Indonesia continued their recent gains, rising

33% to top US$1 million for the first time since 2016.

Imports from Indonesia are nearly tripling 2021 totals year

to date through November. Despite the poor November

numbers, total imports of hardwood flooring remain ahead

of 2021 year to date, but now by only 8%.

Imports of assembled flooring panels continued to slide in

November, falling 3% from October to a level 17% lower

than that of last November. Imports from Brazil nearly

disappeared, falling 98%, while imports from Thailand

also fell sharply for the second straight month. Despite the

decline, total imports of assembled flooring panels year to

date are ahead of 2021 by 26% through November.

Moulding imports fall slightly while imports from China rebounded

While US imports of hardwood moulding decreased in

November by 4%, the month was still 21% better than the

previous November.

Imports from China, which dropped sharply in October,

rebounded in November gaining 99% while imports from

Brazil showed a 27% increase. Imports from Brazil are

ahead 81% year to date over 2021 through November.

Total US imports of hardwood moulding are up 25% year

to date.

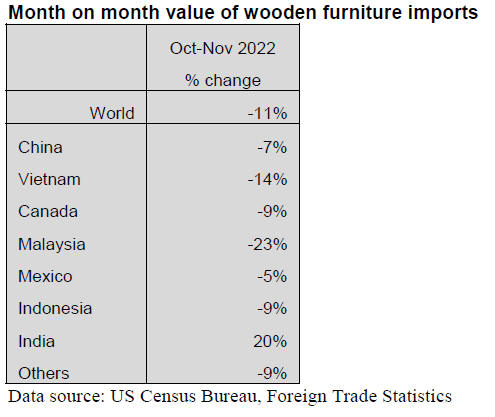

Wooden furniture imports fall in November

US imports of wooden furniture fell again in November,

declining for the fifth time in the last six months. At

US$1.80 billion, November imports were 11% below that

of October, but were 8% higher than that of November

2021. Imports from most suppliers were down, with

imports from Malaysia (down 23%) and Vietnam (down

14%) declining the most. With the exception of China,

imports from most countries remain up more than 10%

over 2021 year to date. Total wooden furniture imports

are ahead of 2021 by 7% year to date through November.

Meanwhile, residential furniture orders continued to

plummet, falling 30% in October 2022 from the same

month in 2021, according to Smith Leonard’s latest

Furniture Insights survey. Year to date, orders are down

29%. These declines were seen for nearly all survey

respondents—88% reported a decline in orders for the

month, while 91% reported a decline for the year.

Smith Leonard’s Ken Smith wrote that he’s concerned

with receivable levels, as many dealers are seeing big

slowdowns at retail. Inventories were flat from September

but up 47% from last year.

“We knew that the good business in late 2020 and 2021

would not continue,” said Smith. “As the slowdown

happened, the results have been a bit harsh as to how slow

it has become. Maybe it does not feel so bad for some

since backlogs were built so high, (as) production and

shipping have been able to keep things moving, but it is

beginning to feel not so good as backlogs have declined

significantly for so many.”

See:https://www.furnituretoday.com/financial/furnitureorders-fall-30-in-october-has-the-recession-begun/

US furniture industry faced multiple problems in 2022

Furniture retailers and suppliers alike saw big swings in

supply and demand throughout 2022, making it difficult to

properly adjust. Much of the turmoil was a result of the

waning COVID pandemic.

Here are five of the biggest problems the industry faced

over the year according to Furniture Today:

Ocean container rates -- Perhaps the most infamous issue

during the latter half of the pandemic was soaring

container rates, which saw unprecedented rises. In

September 2021, average spot rates reached their peak at

US$10,377 per 40-foot container according to Drewry

World Container Index. That number is nearly 10 times

higher than pre-pandemic 2019’s average of US$1,420.

Low demand -- The home furnishings industry saw record

demand in 2021 and the first quarter or so of 2022, before

the faucet was shut off with a thud. Inflation then reared

its head, along with a slowing of the overall economy,

soaring gas prices and more. Since then, the industry has

been in steady decline. Manufacturing orders have dipped

every month since May and show no signs of ceasing that

pattern any time soon.

Labour -- The labour shortage – particularly for domestic

manufacturers – has been a problem affecting the industry

for some time. It hasn’t shown much of an improvement

this year.

Inland freight -- Domestic manufacturers and importers

alike struggled more with inland freight and trucking,

especially in the latter half of the year.

“Inland freight is awful,” said Rusty Morris, vice president

of sales and marketing at American Woodcrafters, which

imports from Indonesia. “Pricing is ridiculous. Fuel and

labor costs are up. It’s making it difficult to hit our

strategy of expanding west of the Mississippi.”

The issue, at least on the price side, may be improving.

Transportation capacity rose in November, pushing prices

downward at their fastest rate on record.

Inventory -- Through most of 2021, retailers were buying

what they could simply to have available product, due to

supply delays and disruptions. As 2022 hit, supply

improved and demand lessened, and many retailers found

themselves with a glut of product. Inventory still sits high

for many as 2023 comes into the fold, but the situation

may be improving.

See:https://www.furnituretoday.com/industry-issue/the-top-5-issues-affecting-the-furniture-industry-in-2022/

Housing tough time ahead for builders

According to experts interviewed by US News and World

Report, several factors may make building a house or

buying a new construction home more expensive – or

harder to find – in 2023.

The biggest obstacle for homebuilding in 2023 is the more

pessimistic outlook coming from builders themselves –

and it’s been low for some time. “Homebuilder sentiment

has been down in every month of 2022,” says Orphe

Divounguy, senior economist for Zillow.

The continued decline in builder confidence and

subsequent builder slowdown means catching up on the

millions of housing units the US needs is further in the

distance. This means a continued housing shortage that

will keep prices higher.

Further, the rise in interest rates, combined with already

sky-high home prices, has led to many buyers opting to

hold off on shopping for a home. “The buyer’s purchasing

power has decreased 25% to 30%, … and that rapid

decrease (in affordability), or increase in interest rates, has

caused … a disruption in the housing market,” says Noah

Breakstone, CEO of BTI Partners, a Florida real estate and

land developer.

On the positive side, structural lumber is significantly

cheaper than it was in 2021 – less than one-third the price

in December 2022 compared to December 2021,

according to Trading Economics. Other construction

materials, from concrete to ceramic tile and asphalt

roofing, have all risen moderately since 2021. Also,

properties planned, permitted and sold months prior are

still being delivered as completed houses, and the rate at

the end of 2022 shows growth compared to the same time

in 2021, when materials availability and supply chain

issues were more exacerbated.

See:

https://www.forbes.com/sites/brendarichardson/2022/12/19/experts-predict-what-the-housing-market-will-look-like-in-2023/?sh=596a08eabfc0

Disclaimer: Though efforts have been made to ensure

prices are accurate, these are published as a guide only.

ITTO does not take responsibility for the accuracy of this

information.

The views and opinions expressed herein are those of

the correspondents and do not necessarily reflect those

of ITTO

|