| Home: Global Wood |

|

Industry News & Markets |

| Home: Global Wood |

|

Industry News & Markets |

|

Wood Products Prices in UK and Europe 01 – 15th Aug 2023 | ||||||||||||||||||||||||||||||

|

Report from Europe

EU renews anti-dumping measures on Chinese okoumé plywood On each occasion this has led to the announcement of another 5-year extension. The request for review was based on the grounds that the expiry of the measures would be likely to result in recurrence of dumping and injury to the EU industry. The duties renewed on 13 June are unchanged from those originally imposed in November 2004, requiring payment of between 6.5% and 23.5% by four named Chinese manufacturers and 66.7% by all other Chinese manufacturers. The four manufacturers paying lower duties had co-operated during the original anti-dumping investigation and shown that the “injury-margin” for their products was less than calculated by the EU for other Chinese manufacturers.

Signs of greater resilience in EU okoumé plywood manufacturing sector

The latest review suggests that while the EU sector is

The product covered by the anti-dumping duties and

The product is used for a variety of end-uses in the EU,

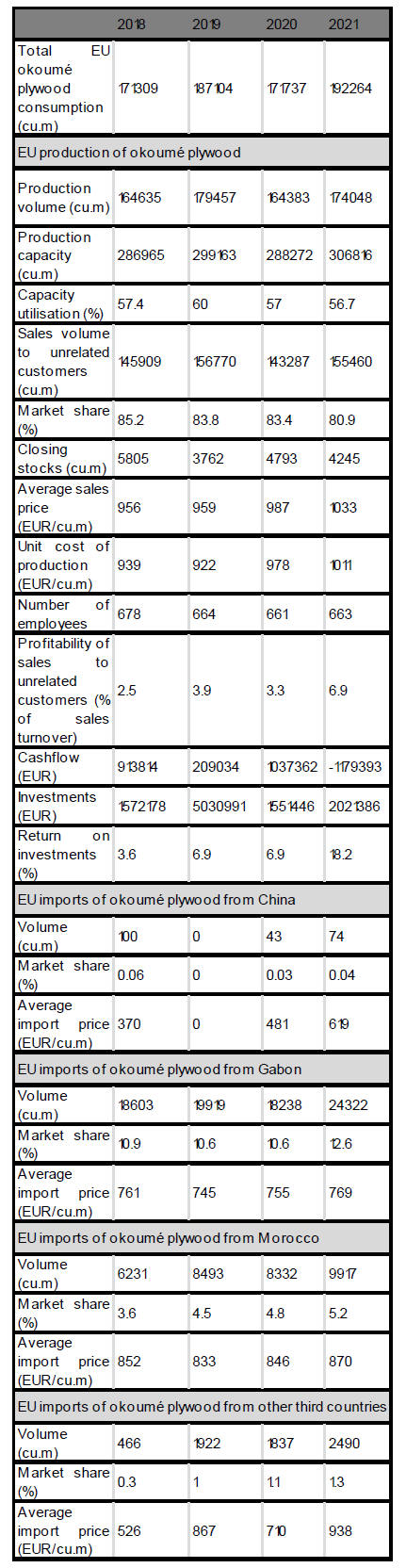

The EC’s analysis shows that EU consumption of okoumé

Although a positive recent trend, consumption is still a

EU production of okoumé plywood was 164,600 cu.m in

This compares to production of around 146,000 cu.m per

Summary data from the EC’s review analysis on EU

EU manufacturers share of the EU market for okoumé plywood decreased from 85% in 2018 to 81% in 2021. Share was lost primarily to imports from Gabon and Morocco. However, in this instance the longer-term trend is more positive for EU manufacturers whose share of the market was only around 70% during the 2012-2015 period. Employment in the EU okoumé plywood manufacturing industry remained stable at around 670 people between 2018 and 2021, but this was a significant rise from less than 500 in 2015. Sales prices of okoumé plywood manufactured in the EU increased from 956 EUR/cu.m in 2018 to 1033 EUR/cu.m in 2021. These prices are considerably higher than the 2012-2015 review period when they were around 770 EUR/cu.m. Over the long term though, they represent only moderate gains – and a significant decline in real terms when account is taken of inflation - compared to around 900 EUR/cu.m during the 2008-2009 period. Furthermore, the prices achieved between 2018 and 2021 are only just sufficient to cover the unit costs of production which increased from 939 EUR/cu.m in 2018 to 1011 EUR/cu.m in 2021. Profitability on sales is therefore still low, though it did increase from 2.5% of turnover in 2018 to 6.9% in 2021. Loss of EU manufacturers’ share of the market between 2018 and 2021 was at least partly due to higher prices compared to competitors in Gabon and Morocco. Average prices for EU imports of okoumé plywood from Gabon were relatively stable at around 760 EUR/cu.m between 2018 and 2021, while prices from Morocco increased from 850 EUR/cu.m to 870 EUR/cu.m during the same period. The EC compared EU sales prices of domestic, Gabon and Moroccan manufacturers during the review period with commercial offers solicited from Chinese manufacturers by email for delivery to the EU and other third countries (in the Middle East, Türkiye, and the United Kingdom). These prices were, at CIF level, 686 EUR/cu.m for full okoumé and 458 EUR/cu.m for faced okoumé for the EU market, and 371 EUR/cu.m for faced okoumé for third countries.

The EC concluded that prices offered by Chinese manufacturers for okoumé

plywood were substantially less than both EU manufacturers and

manufacturers in other third countries. Chinese okoumé plywood would

switch to EU market without anti-dumping measures says EC The EC also estimated total plywood production capacity in China at 270 million cu.m per year at the end of 2021. The EC concluded that “Given the large production capacities in the PRC, that dwarfed the EU demand of 192,000 cu.m in the review investigation period (2021) regardless of the figure taken and that only a change from other types of wood to okoumé is needed to produce okoumé plywood, there is a high likelihood that Chinese producers would use their large production capacity to shift their production from other types of plywood towards the more lucrative okoumé plywood for export to the Union if the measures expire”. The EC also suggested that the EU market would be “attractive” to plywood manufacturers in China since, during the review period, “Chinese exports prices of okoumé plywood to the Union market were higher than the Chinese export prices to all other third markets for which commercial offers were available. Namely the export price offers at CIF level to the Union market were, on average, 23% higher than export prices to third countries at CIF level”. The EC also note that other consuming countries are implementing “trade defence measures” on imports of Chinese plywood, including: the Republic of Korea (anti-dumping measures on plywood with at least one outer ply of tropical wood: of a thickness less than 3,2 mm); Morocco (anti-dumping measures on all plywood); USA (anti-dumping and countervailing measures on hardwood plywood); and Türkiye (anti-dumping measures on certain types of plywood). According to the EC “These measures contribute to export limitations for Chinese plywood producers and to the existence of sustained significant spare capacity of plywood in China and render the Union market more attractive for Chinese plywood imports”. The EC concluded that “there is a strong likelihood that dumping would recur if the current measures were allowed to lapse. In particular, the level of the normal value established in the PRC, the level of Chinese export prices to third country markets and the Union, the attractiveness of the Union market and the availability of significant production capacity in the PRC all point to a strong likelihood of recurrence of dumping in case the current measures would be allowed to lapse”.

Details of the EU’s decision to the anti-dumping measures, including the

full investigation, are available at:

European wood-based panel production fell in 2022 The output, relating specifically to EPF member countries, totalled 59.8 million cu.m. Consumption of wood-based panels followed a similar pattern, with a reduction of 7% (60.8 million cu.m) compared to 2021. The TTJ derived the figures – which are contained in the newly-published EPF Annual Report 2022-2032 – from comments made by Clive Pinnington, EPF managing director, to the EPF AGM and conference in Santiago de Compostela in Spain on 23 June which was attended by about 200 representatives from the global wood-based panels industry. According to the TTJ, Mr Pinnington also told delegates that essentially 2022 H1 had an “OK” performance, but H2 was “not quite a catastrophe, but nearly”, with the furniture industry in particular suffering in H2 with a 5% reverse. The EPF figures quoted by the TTJ show that European particleboard production reduced 6.9% in 2022 to 32.1 million cu.m. However, European particleboard production capacity increased by 1% in 2022 and is expected to rise by another 3.3% this year. MDF suffered a more severe production output decline in 2022 with a 9.3% dip to 12.5 million cu.m, though TTJ note that the comparison year (2021) had seen a sharp rise in output of 7.7%. The OSB sector saw a 10.7% decline in production to 6.4 million cu.m, while softboard (predominantly wood fibre board insulation) suffered an 8.9% reverse to 5.1 million cu.m. European plywood production was down by 2.5% in 2022 to 3.1 million cu.m. According to TTJ, again quoting the EPF, consumption of wood-based panels in the key furniture industry declined by 1% in 2022. The furniture industry consumed 48% of all wood-based panels last year, down from 49% in 2021. | ||||||||||||||||||||||||||||||

|

Abbreviations

| ||||||||||||||||||||||||||||||

|

Source:ITTO' Tropical Timber Market Report |