Japan

Wood Products Prices

Dollar Exchange Rates of 25th

January

2026

Japan Yen 153.42

Reports From Japan

Election platform - stimulus to drive a return to

inflation and growth

The Japanese Prime Minster has called a snap election and

is running on a platform of stimulus to drive a return to

inflation and growth after decades of stagnation. She

launched her campaign with a vow to suspend the

consumption tax on food for two years. How this will be

paid for rattled investors and impacted the bond market.

Moves in the bond market extended sharply after demand

faltered at a recent 20-year auction. At the same time,

inflation has been running above the Bank of Japan's (BoJ)

target for nearly four years and the prospect of more

spending has been pushing down on the currency.

See: https://www.asahi.com/ajw/articles/16298108

BoJ raised its growth forecast for fiscal 2025 and 2026

The (BoJ) retained its hawkish inflation forecasts and

stressed it will remain vigilant to price risks from a weak

yen, interpreted as policymakers intend to keep raising

still-low borrowing costs. The yen slumped initially

despite the hawkish tone before suddenly spiking in a

move that put traders on high alert for possible currency

intervention by Japanese authorities to prop up the ailing

currency.

In a press conference after the board's decision to keep

interest rates steady, BoJ Governor, Kazuo Ueda, said

steady wage hikes were prodding more firms to pass on

labour costs. The BoJ maintained its key policy rate at

0.75% in a widely expected decision after having just

hiked the rate from 0.5% in December.

In a quarterly outlook report, the BoJ raised its growth

forecast for fiscal 2025 and 2026 and maintained its view

the economy will remain on course for a moderate

recovery. It also revised up its core consumer inflation

forecast for fiscal 2026 to 1.9% from 1.8% three months

ago, adding that risks to the economic and price outlook

were roughly balanced.

The central bank also maintained its pledge to keep raising

rates if economic and price developments move in line

with its projections.

See: https://www.asahi.com/ajw/articles/16306297 - Google

Search

and

https://www.asahi.com/ajw/articles/16304466

Aiming for zero consumption tax on food

Prime Minister Sanae Takaichi has indicated she will aim

for realising a zero consumption tax rate on food items

within fiscal 2026, which starts in April. Takaichi, also

president of the ruling Liberal Democratic Party (LDP),

made the remark during discussions on the proposed tax

cut, a key issue in the upcoming House of Representatives

election.

The LDP included in its policy pledges for the election a

commitment to accelerate discussions on reducing the 8%

consumption tax rate to zero for food items for two years.

See: https://japannews.yomiuri.co.jp/news-services/jiji-

press/20260125-306511/

Modest economic recovery supported by wage

prospects and firmer consumer sentiment

Government policymakers recently repeated their long-

held view that the domestic economy is likely to remain

on a modest recovery track counting on continued wage

hikes amid labour shortages and pointing to a pickup in

consumer sentiment.

Japan’s exports posted their fourth straight year-on-year

increase in December to hit a record high of yen 10.41

trillion, surpassing the previous high of yen 9.91 trillion

reached in December 2024.

In its monthly report for January, the Cabinet Office

maintained its overall assessment saying the economy is

“recovering at a moderate pace, although the effects of the

U.S. trade policy are seen mainly in the auto industry.”

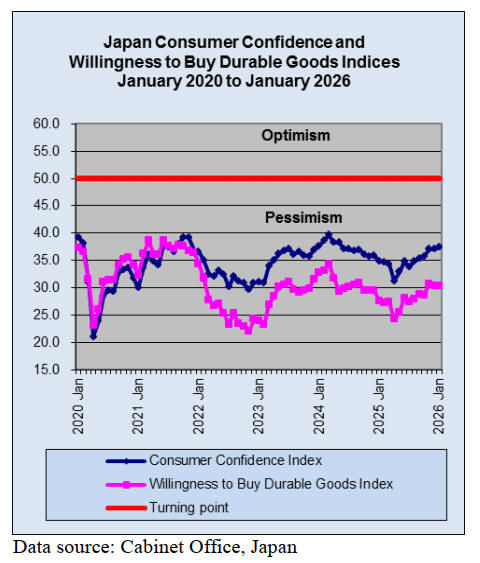

Japan's Consumer Confidence Index rose in January when

compared to the figure seen the previous month according

to the Cabinet Office data.

The overall livelihood index climbed to 36.8 as consumers'

willingness to buy durable goods rose. The employment

component gained while the income growth index went up

0.7 points to 42.0.

In terms of inflation expectations, the share of respondents

anticipating higher prices over the next year fell 0.5

percentage points from December.

See

:https://www.tradingview.com/news/macenews:743dedfef094b:0

-japan-govt-continues-to-see-modest-economic-recovery-on-

sustained-wage-hike-prospects-brighter-consumer-sentiment-

amid-easing-inflation/ - Google Search

and

https://www.tradingview.com/news/te_news:520976:0-japan-

consumer-morale-highest-in-21-months/

Market anticpates currency intervention

On Monday 27 January the yen gained amid broad

weakness in the dollar as traders remained on heightened

alert over possible Japanese intervention to halt the

currency’s recent slide. The Japanese currency jumped as

much as 1.2% versus the dollar. Volatility in foreign-

exchange markets came as Japan’s currency advisor,

Atsushi Mimura, said authorities in Tokyo will respond in

close coordination with their counterparts in Washington.

See:

https://www.japantimes.co.jp/business/2026/01/26/markets/yen-

extends-gains-dollar-pressure/ - Google Search

Foreign investors accounted for 27% of real estate

transactions in in Japan in 2025

According to the media a review of regulations governing

real estate ownerships is being considered and that after

gaining a better understanding of the situation the

government will contemplate imposing restrictions on real

estate acquisitions by foreign nationals.

However, concerns have been raised that excessive

regulations of real estate transactions could hinder

economic activity driven by investment.

The Asahi article points out that implementing regulations

targeting foreigners alone is considered difficult because

Japan is a signatory to World Trade Organization

agreements that uphold the principle of non-

discrimination.

See: https://www.asahi.com/ajw/articles/16230489 buyers

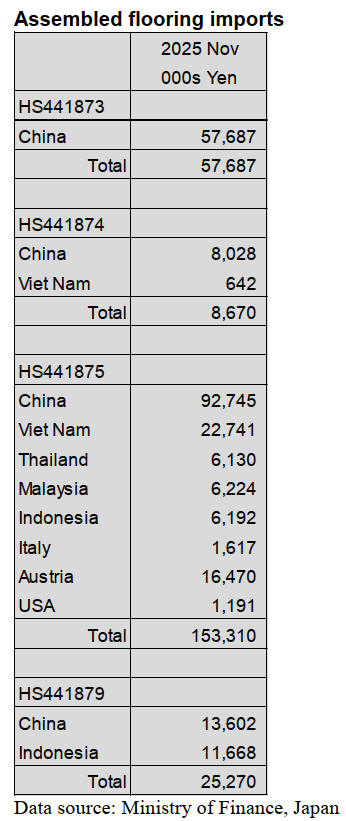

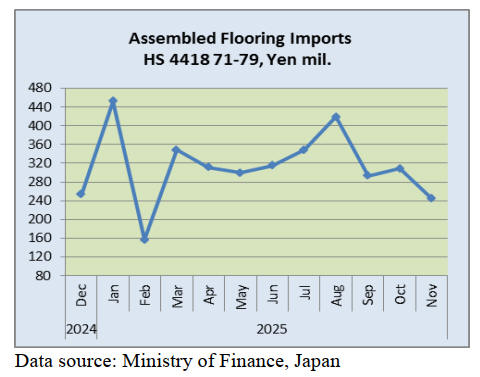

Assembled wooden flooring - Import update

The October rise in the value of assembled wooden

flooring (HS441871-79) faded in November but if the

trend in previous years holds there may be another uptick

in December.

Year on year the value of November 2025 imports was

down over 20% compared to the level in November 2024

and month on month there was a 20% decline in the value

of imports.

Of the various categories of assembled flooring

imports in

November, 62% was of HS 4418-75 (72% in October)

China and Vietnam being the top shippers, however, these

two shippers saw a sharp drop in the value of shipments to

Japan as did shippers in Thailand.

For the other categories HS4418-79 accounted for 24% in

November (22% in October) followed by HS4418-79

at10% (4% in October) and HS4418-74, 4% (2% in

October).

For HS4418-73 imports all originated in China. Shippers

in China and Indonesia were the only shippers of HS4418-

79 in November.

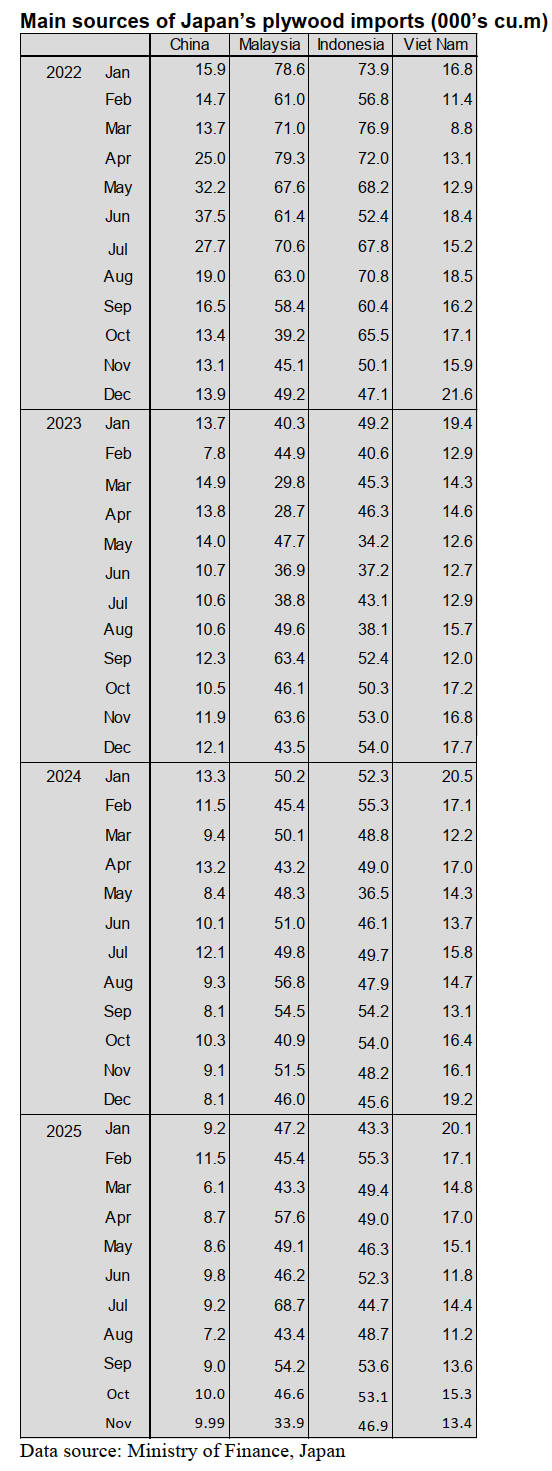

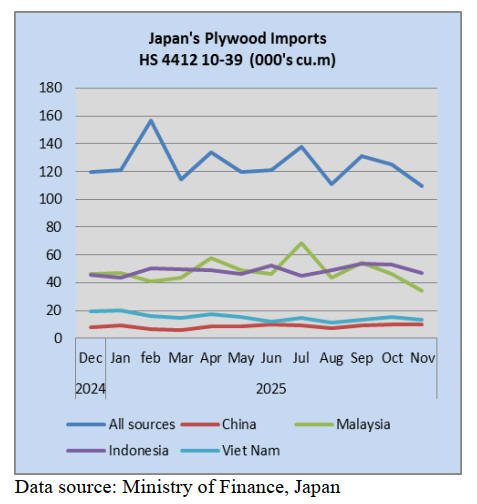

Plywood imports

Indonesia and Malaysia continued as the top suppliers of

plywood to Japan in November and the combined volume

of shipments accounted for 73% of Japan’s plywood

imports (79% in October). The other top shippers being

Viet Nam and China. November 2025 plywood arrivals

were slightly down compared to the volume of October

with shippers in Malaysia and Indonesia posting declines.

In November 2025 arrivals of HS441210-39 were reported

at 109,850 cu.m (215,755 cu.m in October). As in previous

months of the various categories of plywood imported in

November 2025, HS441231 accounted for most (91%).

Trade news from the Japan Lumber Reports (JLR)

The Japan Lumber Reports (JLR), a subscription trade

journal published every two weeks in English, is

generously allowing the ITTO Tropical Timber Market

Report to reproduce news on the Japanese market

precisely as it appears in the JLR. For the JLR report

please see: https://jfpj.jp/japan_lumber_reports/

Demand and supply of lumber at Tokyo port

According to Tokyo Lumber Terminal Co., Ltd., the

inventory of lumber at the end of November 2025 is

139,000 cbms, 5.2 % less than October 2025. It is for the

first time in six months to decrease.

Incoming volume dropped significantly by 33.4%,

reflecting quarterly shipment adjustments by shippers and

trading firms and reduced monthly contract purchases

under the ongoing yen depreciation.

Meanwhile, shipments failed to recover to the September

and October levels. Looking at daily figures, product

inflows were 2,076 cbms against outflows of 2,502 cbms,

a 1.7% month-on-month decline. While this is in line with

April–September levels and does not indicate sluggish

demand, it was below the 2,600 cbms expected by the

Tokyo Lumber Terminal.

European lumber inflows amounted to 11,541 cubic

meters, down 42.1% month-on-month. Shipments totaled

14,448 cbms, a 12.1% decline from the prior month, with

inventories at 42,075 cbms, down 6.3%.

Since November, the weak yen has driven up costs,

making it difficult for shippers and trading companies to

increase the volume of lumber contracts from the U.S. and

Canada. Incoming volume was 8,492 cbms, down 25.7%

from the previous month, while outgoing volume was

8,529 cbms, a 29.9% decrease month-on-month. Stock

volume was 30,632 cbms, a 0.1% month-on-month

decrease.

Imports of Russian lumber totaled 5,172 cbms, down

39.7% from the previous month; outgoing volume was

9,846 cbms, a 4.1% decrease; and inventories stood at

35,324 cbms, down 11.7% month-on-month.

Russian lumber

Russian lumber prices, particularly for imported red pine

battens, are showing a bearish trend at the origin. Until

now, local sawmills have resisted price cuts due to high

production costs. However, with shipments to destinations

other than Japan stagnating and demand in Russia and

Central Asia slowing as winter sets in, they are now

showing a willingness to negotiate prices in order to

increase supply to Japan, which is relatively easier to sell

into.

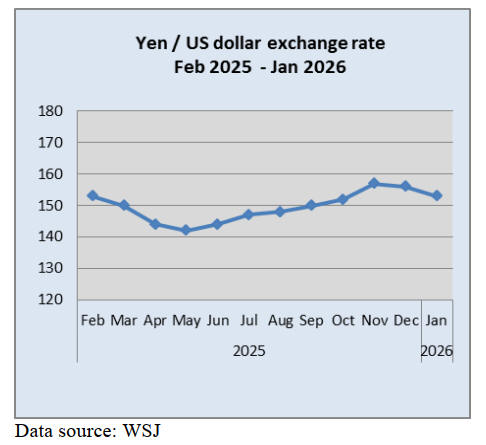

However, with the yen weakening to the ¥155 range

against the dollar, landed costs remain high at around

¥95,000 per cubic meter (Ontario delivery).

In the domestic market, excess inventory in the Tokyo

metropolitan area has yet to be resolved. At the Tokyo

Lumber Terminal, although shipments exceeded arrivals in

November, inventories remain around 35,000 cubic

meters, which is considered high for this time of year.

On the price front, with distribution stocks largely

consisting of high-priced material, there is little room for

reductions, leaving current prices unchanged. As a result,

transactions are sluggish, and in the product market

retailers are limiting purchases to small, immediate needs.

Radiata pine logs and lumber

The wood packaging materials market showed a modest

recovery trend in September and October, but shipments

did not grow as expected from November onward, and in

December demand is clearly lower compared with the

same month last year.

For 2025, import volumes are projected at 140,000 cubic

meters for Chilean radiata pine lumber, an 18% decrease

from last year, and 195,000 cubic meters for New Zealand

radiata pine logs, also an 18% decline.

Chilean radiata pine lumber is projected to fall by half

compared with pre-COVID 2019 levels, while New

Zealand radiata pine logs are expected to decline by 45%

from the same year, both representing significant

decreases. The origin price of Chilean radiata pine lumber

remains at US$340 per cubic meter (C&F), but with the

exchange rate weakening from ¥146 to ¥153 to the dollar,

about a 4% decline, import costs for this material are

rising. At present, the domestic market price for Chilean

radiata pine squared timber is holding steady at around

¥63,000 per cubic meter (delivered to packaging

companies, including transport and fumigation costs).

The origin price of New Zealand radiata pine logs for the

Japanese market is holding steady at around US$160 per

cubic meter (C&F).

The price of domestically sawn slab boards is also holding

steady at around ¥66,000 per cubic meter, delivered to

wholesalers. Meanwhile, the price of the same material for

China is US$ 112–116 per cubic meter (C&F), down by 3

dollars from the previous month.

|