US Dollar Exchange Rates of

10th

February

2026

China Yuan 6.91

Report from China

Decline in 2025 sawnwood imports

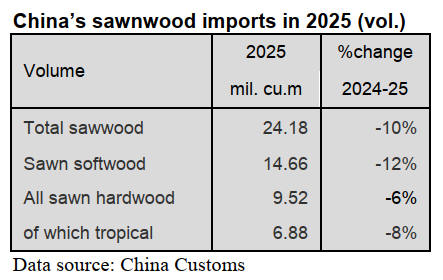

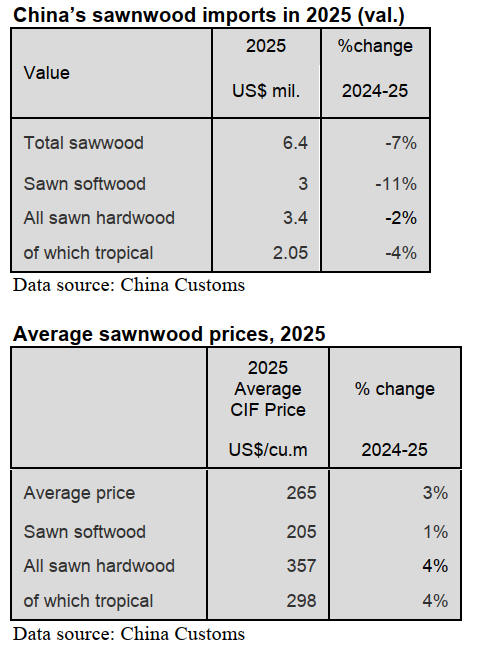

According to data from China’s Customs, 2025 sawnwood

imports totalled 24.18 million cubic metres valued at

US$6.40 billion, a year on year decrease of 10% in

volume and 7% in value on 2024. The average price for

imported sawnwood in 2025 was US$265 per cubic metre,

a year on year increase of 3%.

Of total sawnwood imports, sawn softwood imports fell

12% to 14.66 million cubic metres accounting for 61% of

the national total. The proportion of sawnwood imports

reduced about 1 percentage points year on year. The

average price for imported sawn softwood was US$205

per cubic metre in 2025, up 1% year on year.

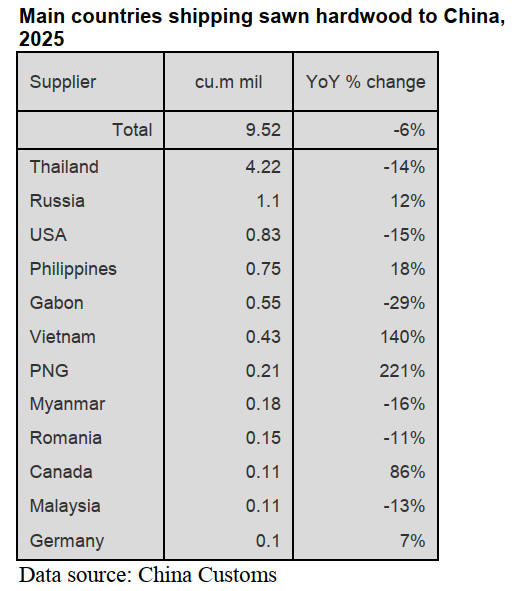

Sawn hardwood imports totalled 9.52 million cubic metres

valued at US$3.40 billion, a year on year decrease 6% in

volume and 2% in value on 2024. The average price for

imported sawn hardwoods was US$357 per cubic metre, a

year on year increase of 4% year on year.

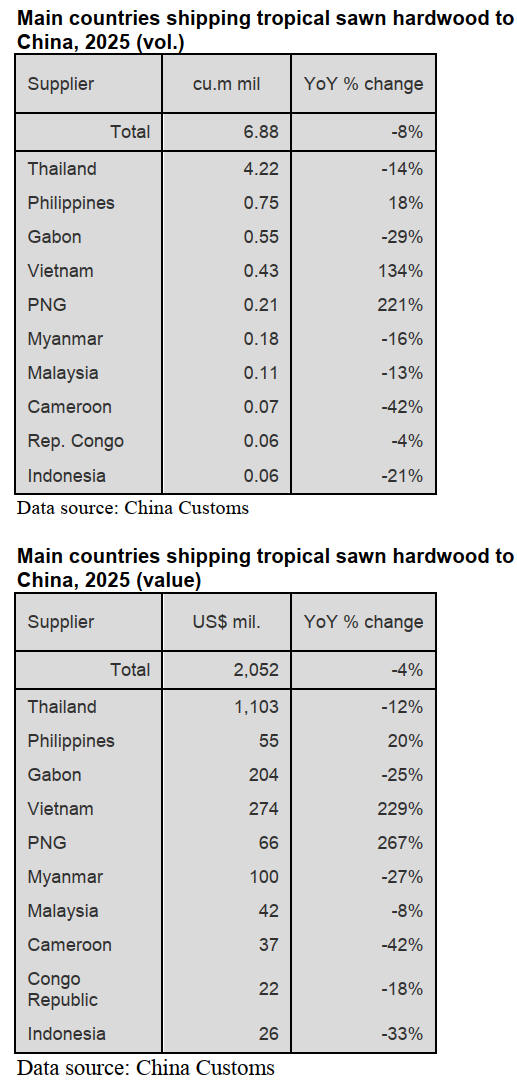

Of total sawn hardwood imports, tropical sawn hardwood

imports were 6.88 million cubic metres valued at US$2.05

billion, a year on year decrease of 8% in volume and 4%

in value and accounted for about 28% of the national total.

The average price for imported tropical sawn hardwood

was US$298 per cubic metre, up 4% year on year.

The main reason for the decline in sawnwood imports was

the reduction in domestic demand. As the main driving

force for the import of sawnwood, the deep adjustment of

the domestic real estate market was the primary factor.

Currently, the new housing construction area has

plummeted by 64% compared to the average level over the

past decade, directly leading to a contraction in the

demand for construction materials including sawnwood.

Market data confirms the severe situation.

The proportion of new home sales in total transactions has

sharply declined from over half in 2022 to 26% in 2024

and the downward trend continued in 2025. The real estate

market in China remained sluggish which slowed

construction and manufacturing industries leading to a

decline in demand for sawnwood.

The real estate industry is the main downstream sector for

wood consumption. The number of new housing starts in

2025 decreased and the transaction volume of second-hand

houses declined resulting in a significant cooling of

demand for sawnwood from developers, decoration

companies and furniture factories. This contraction on the

demand side is the most direct reason for the decline in

sawnwood imports. The industry generally believes that

this trend is unlikely to be reversed in the short term.

Other key factors affecting imports were inventory

backlogs and cautious purchasing.

Due to the high domestic sawnwood inventory, traders and

processing enterprises generally adopted the "sales-driven

purchasing" strategy, reducing their willingness to

replenish stocks which further suppressed sawnwood

demand.

Another reason was supply chain cost increases.

Fluctuations in global shipping fees, rising raw material

costs and policy adjustments in some sawnwood exporting

countries have increased import costs and squeezed the

profit margins of enterprises.

Sudden halt of China-US timber trade. Beginning June

2025 China suspended imports of American logs (due to

quarantine issues) resulting in a significant decline in the

arrival of American sawnwood. Although it was not the

main reason for the decrease in the total import volume of

sawnwood, this move exacerbated the fluctuations in the

import pattern. The last reason for the decline was that the

price for imported sawnwood rose.

In conclusion, the significant reduction in sawnwood

imports in 2025 was the result of the combined effects of

demand contraction and cost pressure and the industry as a

whole is currently in a period of deep adjustment.

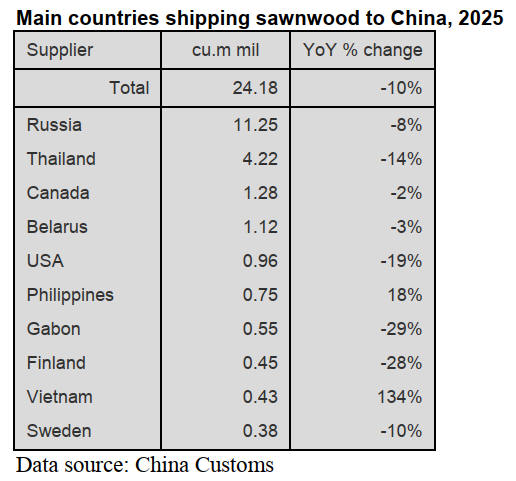

Decline in sawnwood imports from Russia

According to data from China Customs, Russia was the

largest supplier of China’s sawnwood imports in 2025 but

sawnwood imports from Russia fell 8% to 11.25 million

cubic metres, accounting for 47% of the national total at a

value of US$2.383 billion, down 5% on 2024. The average

price for imported sawnwood from Russia in 2025 was

US$212 per cubic metre, a year on year decline of 0.5%.

China's imports of sawnwood from Russia decreased both

in volume and value in 2025. Meanwhile, the increase in

transportation costs and the restricted logistics channels

have further intensified the pressure on the industry.

Although the trial operation of the Russian-Chinese Arctic

shipping route is expected to reduce transportation costs

by 28% and shorten delivery time by 14 days, it has not

yet established a large-scale transportation capacity.

Furthermore, the adjustment of the Chinese construction

and real estate market has led to a decrease in the demand

for sawnwood. Coupled with the increasingly strict

environmental policies, this has also prompted Chinese

timber merchants to accelerate the diversification of their

supply chains, thereby reducing their purchases of Russian

sawnwood to some extent.

China's sawnwood imports from the Philippines and

Vietnam increased significantly by 18% and 134% in

2025. China’s sawnwood imports from Thailand dropped

to 4.22 million cubic metres valued at US$1.103 million,

down 14% in volume and 12% in value on 2024 levels.

The average price for imported sawnwood from Thailand

in 2025 was US$262 per cubic metre, a year on year

increase of 3%.

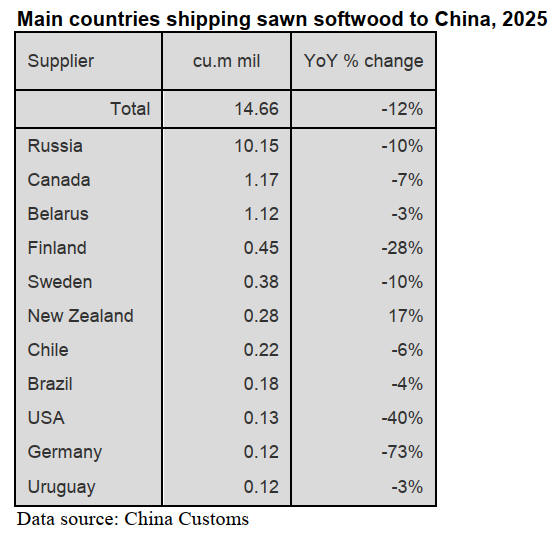

Rise in sawn softwood imports from New Zealand

China’s sawn softwood imports from New Zealand, alone

among the top suppliers, rose 17% to 280,000 cubic

meters in 2025. The volume of sawnwood imported by

China from New Zealand increased in 2025. The main

reasons can be summarised as follows.

Changes in the domestic timber supply structure in China.

The country has continuously implemented a ban on

commercial logging of domestic natural forests resulting

in a significant reduction in large diameter log resources.

Sawmills have increased their reliance on imported raw

materials, especially for a stable supply of sawn softwood.

The market competitiveness of New Zealand timber. New

Zealand's timber is mainly composed of radiata pine. It is

stable and of uniform specifications. Moreover, due to the

upgrade of the China-New Zealand Free Trade

Agreement, China has abolished tariffs on 12 related tax

items of wood and paper products imported from New

Zealand. Approximately 99% of the wood and paper enjoy

tax-free treatment, thereby reducing the import cost of

sawn softwood.

Substitution effect and supply chain diversification. Due to

the impact of international circumstances the import

volume of timber from traditional supply countries such as

the United States and Germany has significantly

decreased. Chinese enterprises have accelerated the

diversification of their supply chains. As a stable and

reliable supply country New Zealand's exports of

sawnwood to China have increased.

In conclusion, the increase in China's imports of

sawnwood from New Zealand in 2025 was the result of

the combined effects of domestic resource constraints,

policy benefits, supply chain adjustments and changes in

the international situation.

Drop in sawn hardwood imports from Thailand

China’s sawn hardwood imports from Thailand, as the

largest supplier, dropped 14% to 4.22 million cubic metres

in 2025, accounting for 49% of the national total.

China's sawn hardwood imports from Thailand are mainly

rubberwood and fell in 2025 although China's imports of

sawn rubberwood have continued to grow in recent years.

Overall, the contraction of domestic demand and the

shortage of rubberwood raw materials as well as the rising

acquisition costs in Thailand affected the import

performance of Thai rubberwood in the Chinese market in

2025. The specific conditions are as follows:

The adjustment of some downstream industries in China

has weakened the willingness and ability to purchase raw

materials. Especially during the traditional consumption

peak season the impact of demand boosting policies was

less than expected which further led to a decline in the

rubberwood import volume.

The instability in the acquisition of rubberwood raw

materials within Thailand has become increasingly

prominent. On the one hand, uncertainty in the price trend

of rubberwood in recent years has affected the pace of

logging resulting in unstable rubberwood raw material

supply. On the other hand, adverse weather conditions

such as heavy rains have continuously driven up the costs

of rubberwood and processing. As a result, Thai exporters

have had to raise prices which, in turn, has led to an

increase in the annual import unit price.

China’s sawn hardwood imports from USA, Gabon,

Myanmar, Romania and Malaysia fell 15%, 29%, 16%,

11% and 13% respectively in 2025.

In contrast, China’s sawn hardwood imports in 2025 from

Vietnam and PNG surged 140% and 221% respectively.

Decline in sawn tropical hardwood imports

China’s sawn tropical hardwood imports in 2025 were

6.88 million cubic metres valued at US$2.052 billion, a

year on year decrease of 8% in volume and 4% in value

and accounted for about 28% of the national total.

Thailand still was the largest supplier of sawn tropical

hardwood imports and 2025 sawn tropical hardwood

imports from Thailand totalled 4.22 million cubic metres

valued at US$1.103 billion, a year on year decrease of

14% in volume and 12% in value, accounting for 61% of

the national total.

China's imports of tropical sawn hardwood from the

Philippines have increased significantly, jumping from the

third largest supplier to the second largest supplier,

replacing Gabon.

The Philippines was the second largest supplier of China’s

sawn tropical hardwood imports in 2025 and China’s

tropical sawn hardwood imports from the Philippines rose

18% to 750,000 cubic metres, but imports from Gabon

dropped 29% year on year to 550,000 cu.m.

The top three countries supplied 80% of China’s tropical

sawn hardwood requirements in 2025, namely Thailand

(61%), the Philippines (11%) and Gabon (8%) in 2025.

The main reasons for the decrease in China's sawn tropical

hardwood imports in 2025 was as follows.

The sluggish domestic real estate market has led to a

decrease in demand for tropical timber. Additionally, sawn

tropical hardwood industry is facing the following

challenges, including frequent fluctuations in log prices,

continuous increases in labour costs, the sluggish

construction market and the impact of US tariffs and anti-

dumping policies.

Moreover, reduced enterprise orders, rising freight costs

have further constrained local enterprises and enterprises

lack the motivation to import sawn tropical hardwood.

|