|

Report from

North America

Imports of sawn tropical hardwood dipped in

November

After surging 25% in October, US imports of sawn

tropical hardwood dipped slightly in November, falling

4% from the October high. Despite the dip, the volume of

18,321 cubic metres imported was well above average for

the year and 8% over that of November 2024.

A 12% rise in imports from top-supplier Brazil and a

doubling of imports from Cameroon mitigated declines of

more than 20% from most of the other leading trade

partners.

Keruing imports fell 78% and imports of Ipe fell 38%

while imports of Sapelli rose 29%. Total imports of sawn

tropical hardwood are up 6% over the previous year

through November.

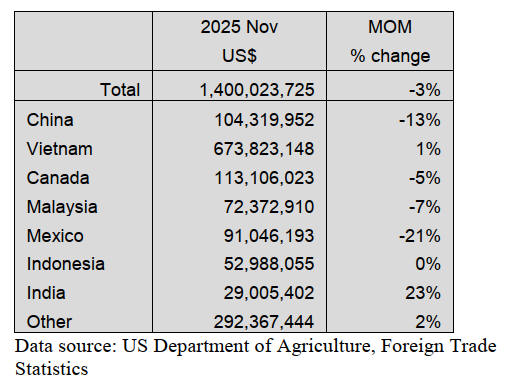

Hardwood plywood imports tumbled 18% in November

US imports of hardwood plywood fell for a second

consecutive month in November, declining 18% from the

previous month. At 232,877 cubic metres, November

imports were 9% less than in November 2024. The decline

was driven by a 64% drop in imports from Indonesia,

which fell to their lowest level since June 2023.

Also showing sharp declines were Imports from Vietnam,

down 32%, and from Russia, down 35%. Through

November, imports of hardwood plywood for 2025

outpace 2024 by 23%.

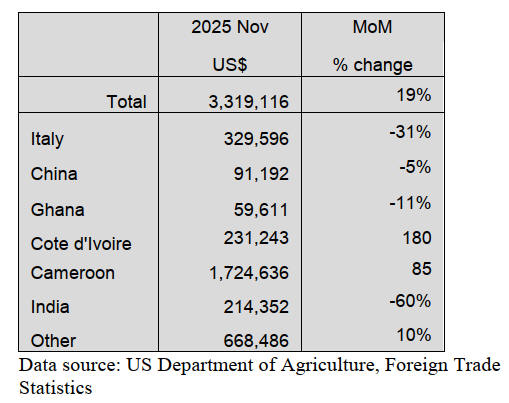

Veneer imports were strong in November

Imports of tropical hardwood veneer surged for a second

straight month in November, rising another 19% from the

previous month after a 95% gain in October. At more than

US$3.3 million, imports for the months were 125% higher

than in November 2024.

Imports from Cameroon soared 85% and accounted for

more than half of the imports for the month. Imports from

Cote d’Ivoire also rose sharply, up 180% from the

previous month. Total imports of tropical hardwood

veneer are up 20% over the previous year through

November.

Moulding imports rebound

After three months of decreases, US imports of hardwood

moulding rebounded somewhat in November, rising 10%

from October’s totals. At US$14.5 million, imports for

the month were 4% higher than in November 2024.

Strong gains in imports from Brazil, Malaysia and Canada

more than offset a 34% decline in imports from China

which have fallen to their lowest level since March 2023.

Year to date, total imports of hardwood moulding are up

10% versus 2024.

Hardwood flooring imports lag previous year

Through November, imports of both hardwood flooring

and assembled flooring panels trail 2024 imports by

significant margins. US imports of hardwood flooring slid

6% in November. At US$5.7 million, imports trailed the

November 2024 total by 21%.

Imports from China fell 72% in November and are down

46% for the year heading into December. Imports from

Brazil are down 51% for the year so far despite a 40%

monthly gain in November. It is likely that total imports of

hardwood flooring will end 2025 down from the previous

year as year-to-date imports are 6% behind 2024 through

November.

Imports of assembled flooring panels were down 12%

versus 2024 through November, despite a 24% surge in

November imports over the previous month. Even with the

gain, November imports were 27% lower than in the

previous November.

As with hardwood flooring imports, panel imports from

China tumbled 53% for the month and were down 45% for

the year. Imports from Thailand resumed in November

after four months of no reported activity, as imports for the

year from that country are down 60%.

US wooden furniture imports drop to lowest level since

COVID

US imports of wooden furniture fell for a fourth

consecutive month in November, hitting their lowest level

since the 2020 COVID epidemic. November imports fell

3% from the previous month to just over US$1.4 billion,

which is 23% lower than in November 2024 and is the

lowest level of imports since June 2020. Imports from

Mexico (down 21%) and imports from China (down 13%)

saw the steepest declines. Total US imports of wooden

furniture are down 8% versus 2024 through November.

Meanwhile, the whole of the US furniture market remains

flat, according to tracking by Smith Leonard. New orders

were down 8% in October compared to the prior month of

September 2025 (following the 15% increase from August

2025). New orders were also down 1% in October 2025

compared to October 2024. However, year to date through

October 2025, new orders remain flat compared to 2024.

See: https://usatrade.census.gov/index.php?do=login

and

https://www.smith-leonard.com/2025/12/30/december-2025-

furniture-insights/

US furniture market projected to nearly double by 2035

The US furniture market, valued at US$178.9 billion in

2025 is forecast to reach US$345.5 billion by 2035,

growing at a compound annual growth rate (CAGR) of

6.8%, according to Astute Analytica. Residential furniture

dominates, accounting for 61% of sales, with wood

products making up 39% and seating furniture

representing 34% of the market.

The industry is supported by ongoing home renovations,

remote work trends, and technological advances in

production that lower costs and allow for greater product

customization. E-commerce and direct-to-consumer

channels are also driving growth.

Employment and manufacturing remain strong, with

269,177 workers across 5,649 establishments as of March

2025. The home furnishings sector is set to expand from

$217.53 billion in 2024 to $286.39 billion by 2029,

buoyed by projected home sales growth of 9% in 2025 and

13% in 2026.

Consumer behavior is evolving, with many delaying

purchases but planning to buy in predictable cycles. Forty

percent of sofa and sectional buyers who postponed

purchases intend to buy in the first half of 2025, while

bedroom and outdoor furniture see staggered buying

patterns. Challenges include intensifying omnichannel

competition, potential housing market slowdowns, and

supply chain disruptions from tariffs and geopolitical

tensions.

See: https://finance.yahoo.com/news/united-states-furniture-

market-set-120000635.html?guccounter=1

Tariffs drove construction materials prices up 2.8% in

2025

Construction input prices decreased 0.6% in December

compared to the previous month, according to an

Associated Builders and Contractors analysis of US

Bureau of Labor Statistics’ Producer Price Index data.

Nonresidential construction input prices decreased 0.7%

for the month.

Overall construction input prices are 2.8% higher than a

year ago, while nonresidential construction input prices

are 3.2% higher.

Prices increased in two of three energy categories in

December. Natural gas and unprocessed energy materials

prices were up 34.8% and 5.5%, respectively, while crude

petroleum prices were down 2.7% in December.

“Construction materials prices posted a welcome decline

in December, yet key inputs are still experiencing rapid

escalation,” said ABC Chief Economist Anirban Basu.

“This is especially true for materials most exposed to

tariffs.

“Prices for commodities less exposed to tariffs, like

asphalt or crushed stone, will likely remain tame in the

coming months due to soft demand for construction

services,” said Basu. “While that may limit increases in

overall materials prices, trade policy will continue to put

upward pressure on certain materials. This has not

significantly dimmed contractor optimism; 7 in 10 ABC

members expect their profit margins to remain stable or

grow over the next two quarters, according to ABC’s

Construction Confidence Index.”

See: https://www.bls.gov/ppi/

and

https://www.abc.org/News-Media/News-Releases/abc-tariffs-

drive-construction-materials-prices-up-28-in-2025

|